Intellectual Capital: ISVA, the Alternative Way of Calculating Creating Value in Agricultural Entities—Case of Poland

Department of Law and Enterprise Management in Agribusiness, Faculty of Economics and Social Sciences, Poznan University of Life Sciences, 60-637 Poznan, Poland

Sustainability 2020, 12(7), 2645; https://0-doi-org.brum.beds.ac.uk/10.3390/su12072645

Submission received: 30 January 2020

/

Revised: 25 March 2020

/

Accepted: 25 March 2020

/

Published: 26 March 2020

(This article belongs to the Special Issue 3rd International Forum on Agri-Food Logistics Towards the Sustainability of Logistics in the Agri-Food Supply Chains)

Abstract

:In the knowledge-based economy, knowledge is regarded as a strategic resource that helps entities to become market leaders. This strategy has been successfully used for years by companies operating in various sectors of the economy. The exception, however, is agriculture, which has been seen for years as a sector with low knowledge intensity and is one that is skeptical about the possibility of using knowledge. This is important especially in that the use of it is, for many managers, still unconscious, and, therefore, this factor remains unused in practice. This paper describes the Intellectual Sources of Value Added (ISVA), an alternative method for analyzing the productivity of tangible and intangible inputs affecting the value-adding process in agricultural holdings. The reasons for developing the concept of that indicator were the imperfections found in the Value-Added Intellectual Coefficient (VAIC™), a widely adopted method authored by A. Pulić. However, the index of efficiency of intellectual capital (VAIC), recognized as suitable for research purposes, demonstrates certain methodological imperfections, including the simultaneous use of resource- and flow-based values. In addition to certain relevant reservations, the above has other consequences, including the declining trend followed by the efficiency of working capital calculated using this formula. In a situation where working capital is observed to grow, this would mean that funds are irrationally invested in assets with a decreasing capacity to add value. This results in drawing a false picture of economic realities of agricultural holdings which, by nature, demonstrate a high share of physical asset consumption in total production costs. As another consequence, the calculated value of the indicator becomes unacceptable in the long run. The use of the ISVA indicator allowed the author to obtain homogeneous results in terms of methodology and confirming the regularities observed in practice. In addition, the research confirmed not only the fact that agricultural enterprises have intellectual capital resources, but also the high efficiency of their use, exceeding the efficiency of use of traditional ones. It also indicates the desirability of continuing research using measures that will enable the monitoring of intellectual capital and their use in agricultural enterprises.

1. Introduction

For years, companies have been investing in structural and human capital to improve their market competitiveness. They use skills and knowledge of employees to increase the efficiency and/or effectiveness of management of their resources, and to offer products to the market and improve their financial results on that basis [1]. There is no doubt that, today, the “human dimension” is particularly important for achieving both the goals of a single organization and most of the goals of the supply chain in which it operates [2]. This applies to almost all sectors of the economy, with the exception of agriculture. In this sector, the inclusion of human and intellectual resources in management comes with some delay, usually via other areas of agribusiness that have links with agriculture in the food supply chain. It is particularly important that, according to researchers’ opinions, Intellectual Capital (IC) is closely related to the problem of sustainable development at the micro-level, i.e., sustainable management of the enterprise. This style of management, shaped by intellectual capital, enables the organization to respond flexibly to changing environmental conditions and—as a result—to build its market value [3,4,5].

In her previous studies [6], the author relied on Value-Added Intellectual Coefficient (VAIC™), a widely recognized method which allows the demonstration of the considerable efficiency of intellectual capital used in agricultural holdings. However, in an effort to eliminate, at least partially, the doubts as to the relevance of the VAIC indicator (including from the perspective of accounting and finance sciences), the author made an attempt to develop an alternative indicator, Intellectual Sources of Value Added (ISVA), which allows the assessment of the sources of value added in Polish agricultural enterprises. This method is assumed to comply with the fundamental economic principles, i.e., be calculated based on homogeneous data of input values that express the cumulated cost streams incurred during the accounting period, grouped by the function they have in adding value.

In this research, the author attempted answer following questions:

- Are both methods of calculation (VAIC™ and ISVA) consistent with fundamental economic principles?

- How much are VAIC™ results consistent with the actual contribution of physical and intellectual capital to adding value in an agricultural holding?

- How much are ISVA results consistent with the actual productivity of tangible and intangible (intellectual) inputs in adding value in an agricultural holding?

- What are the efficiency of physical and intellectual capital and the productivity of tangible and intangible inputs of agricultural holdings, established based on calculation results delivered by the two methods?

- Does the proposed alternative measure, ISVA, allow better evaluation of productivity of tangible and intangible expenditures to be involved in creation of value added?

The following sections attempt to answer these questions, beginning with a review of the relevant literature, followed by a description of the method used and the results obtained, and finally an indication of the need for further research in this field.

2. Background

Most studies addressing the contribution of intellectual capital to new business value have been focused on operators in knowledge-intensive industries (computers, telecommunications, etc.). Their main purpose has been to determine the actual impact of knowledge on competitiveness and financial performance. These are primarily case studies describing methodology created specifically for businesses interested in the use of intellectual capital. The best-known example of this approach is the Skandia model developed by Edvinsson [7]. Other concepts proposed by Stewart [8], Gu and Lev [9], Roos and Roos [10], and Urbanek [11], together with the results that they produced, became a framework for scientific analyses related to determining the effects of the use of intellectual capital in enterprises. They also stimulated the exploration of relevant measurement methods complementary to traditional financial analysis [12,13]. All of these activities served as a starting point for a new field of scientific research, one which is still open.

The first studies in this field to be carried out in the agricultural sector date back to the 1950s and 1960s. Topics included analysis of the use of intangible assets [14], the efficiency of Research and Development (R&D) investments [15], the assessment of agriculture-related and education services [16], the role of knowledge and intangible resources in agriculture [17], and the importance of intangible resources to integration processes [18]. However, no definition was given for intellectual capital, a category that emerged in agriculture through the research carried out in the biotech companies that provide support services for that sector [19,20]. While these papers contributed to the popularity of the concept of intellectual capital in the agricultural sector, they did not translate into relevant research.

Despite the rather high number of intellectual capital models, it is usually assumed that intellectual capital consists of three large components: Human, structural, and relational capital (Bontis [21], Sveiby [22], Roos and Rose [10], and others). However, in the case of agriculture entities, it is difficult to measure relational capital, especially in quantitative terms. Therefore, in the conducted research, it was decided to use a simplified model, based on the concept of A. Pulic [23,24], according to which intellectual capital consists of human and structural capital and—what is important—both of them based on the physical capital (material and financial) accumulated by the enterprise, jointly contributing to the creation of added value.

This study focuses on Polish agricultural holdings that deliver financial reports in accordance with international accounting standards. The documents required under the standards (balance sheet and Profit and Loss (P&L) account) provide a unified and reliable basis for calculations. These data enable research to be carried out and comparisons to be made with operators in other sectors, whether domestic or international.

Polish agriculture has undergone major changes since the shift to a market economy more than 30 years ago. This is reflected in both the number of farms (from 2.9 million in 2002 to 1.4 million in 2018) and the average area of a farm (from 5.7 ha of agricultural land in 2002 to 10.81 ha in 2018). In addition, Poland saw the emergence of a (still small) group of farms with areas of above 50 ha (ca. 34,700), which deliver their entire output to the market. According to 2018 Central Statistical Office data [25], that group included 759 farms with areas of 500 ha or more, accounting for 6.9% of the total farmland in Poland. The study population was sampled from this group. Large and very large farms deliver nearly 90% of marketable agricultural output [26,27]. Poland has been an EU member for 15 years (since 2004), and has consequently received financial support under the Common Agricultural Policy during that period. Today, it is estimated that ca. 100,000 farms have reached a level comparable to that of their EU-12 peers [28]. This is especially true in relation to knowledge, measured by the level of education of farm managers, the techniques and technologies employed, and the extensive use of farm machinery. Farms of this group are capable of effectively competing in the market. Their managers are, in fact, businesspeople who manage their resources, including intellectual capital, which plays an increasingly important role. The effectiveness of their actions depends on whether they are able to monitor and analyze the conditions and effects of resource use. To do this, they need to have the right toolkits. Physical resources are monitored based on economic indices. When it comes to intangible resources, primarily including intellectual capital, the existing indices need to be adjusted to the agricultural context.

Numerous papers emphasize the need to support agricultural holdings with external sources of knowledge, seen as an important driver of innovativeness. Authors making such statements include Komnenic, Tomic and Tomic [29], Subrata, G., and Ingersent, K. [30], Lee, Yoo, and Choi et al. [31], and Vega-Jurado and Gutiérrez-Gracia et al. [32]. Most papers analyze lines of agricultural production whose final effects are niche products that are easily convertible into a final product (e.g., horticulture, vineyards and vine growing, production of mushrooms or ornamental plants, etc.). However, there is no mention of the measurement of impacts of knowledge and intangible assets on mass production lines (e.g., agricultural raw materials such as cereals, milk, or meat). Existing papers make only some indirect references to intellectual capital resources, emphasizing the importance of intangible assets (primarily knowledge) as a source of successful changes. Papers addressing the role to be played by intellectual capital in agricultural holding management have only started to emerge in recent years [33,34,35]. The topic has also been dealt with by C. Cavicchi and E. Vagnoni [36], who noted that the literature on the role of intellectual capital in agriculture is still deficient when it comes to identifying and assessing the competences needed to develop a competitive edge in that sector. Intellectual capital in agriculture should also be researched in the context of its future [37], and especially in the context of its sustainable development [38,39]. Another interesting fact is that the literature very rarely focuses on countries where agriculture is both a highly developed (industrialized) and a highly subsidized sector.

Research related to the measurement of agricultural resources, relationships between them, and the effectiveness of their use mostly relies on traditional methods based upon information on measurable resources. Usually, particular categories are expressed as quantities and values, and are calculated per unit of area or labor [30,40,41,42,43,44]. These yardsticks, exhibiting an acceptable level of imperfection, did not raise any objections among scientists and practitioners. However, they did not include means of measuring intangible assets. Although agriculture also needs to seek competitive advantages based on people and knowledge, the measurement of intangible assets is still met with skepticism in that sector. However, the existing set of instruments does not preclude either the initiation of research in this area or the practical implementation of relevant outcomes. Guided by the suggestions of Sveiby [22], the researchers opted for a group of methods based on return on assets. This is because both the structure of these indices and the essential sources of calculation data refer to classical indicators used in the financial analysis of enterprises. Hence, they are also applicable in agricultural enterprises that keep accounting records. Considering the specificities of the agricultural sector, the suitability of the following methods was tested: Knowledge Capital Earnings (KCE™), Intellectual Value Added (IVA), and the Value-Added Intellectual Coefficient (VAIC™) developed by A. Pulić [23,24]. An essential feature of the first method is that it attempts to measure intellectual capital based on a conventional division of corporate assets into physical and financial capital and on an assumed rate of return on capital employed. IVA follows a similar procedure, and is underpinned by the concept of residual profit, based on the return on assets and on a ratio between profit/loss and the various categories of assets which generate them. Both methods are therefore highly subjective, because different research assumptions may be adopted [6]. VAIC™ (which is commonly used and is based on generally available, highly uniform, and reliable accounting data) was the basis for creating a measure tailored to the needs of analyses in agricultural enterprises.

3. Materials and Methods

Calculation of VAIC™ is done to start the analytical procedure by determining the amount of Value Added (VA), defined as the difference between the operating profit/loss and expenditure incurred by the enterprise (VA = OUT−IN). In this approach, value added is the total of operating profit, labor costs, impairment losses, and depreciation. Next, the efficiency of value-added generation from physical resources (CEE), which A. Pulić assumes to be the book value of net assets (CEO), is calculated as follows:

where:

CEE: Capital Employed Efficiency, and

CE: Value of net assets.

Afterwards, Human Capital (HC) value is calculated. According to A. Pulić, this is the equivalent of the amount of costs triggered, i.e., the sum of all expenditure on staff incurred by the enterprise and the efficiency of human capital (HCE), as per the formula as follows:

where:

HCE: Human Capital Efficiency, and

HC: Human Capital.

The third element is the efficiency of structural capital, which A. Pulić defines as the difference between value added and human capital (VA − HC). This is expressed as the ratio between structural capital and value added, calculated as follows:

where:

SCE: Efficiency of structural capital, and

SC: Structural capital value.

It should be noted that Pulić observed an inversely proportional relationship between the size of the enterprise’s human capital and the size of the structural capital. As a result, structural capital is calculated differently from other indicators (HCE and CEE).

The indicator of total efficiency of tangible and intangible assets in value-added generation (VAIC™) is expressed as follows:

or:

where:

In practice, Intellectual Capital Efficiency (ICE) is referred to as the efficiency rate of intellectual capital. VAIC indicates the efficiency of use of tangible and intangible assets in value-added creation, which means the efficiency of all enterprise assets. The higher the value of VAIC, the better the enterprise’s ability to transform its resources into measurable financial values is. However, unlike in classic profitability indicators (ROA, ROE), the baseline is the generated value added (rather than business profits); the function of intangible resources (intellectual capital) is also covered. In other words, VAIC describes the relationships which enable the creation of value added compared to material and financial capital, human capital, and structural capital employed. In accordance with A. Pulić’s assumptions, the aggregated indicator of corporate value added (which is how the author himself alternatively refers to the index he proposed) corresponds to its Market Value (MV). Thus, it takes into account the impact of macroeconomic factors (including the country’s economic situation and the international context), sectoral factors (general nature of the industry, liquidity, revenue and profits, changes in the competitive environment, phases of the business cycle, etc.), and factors related to the operator in question. These factors differentiate the values of the indicator. Some authors believe this precludes the ability to make comparisons across industries (Kasiewicz et al. [45]), while, according to other ones, this allows the assessment and comparison of the contribution of intellectual capital components to value added in different industries (Kunasz [46]).

VAIC™ allows the measurement of the contribution of human capital to value added (Kasiewicz at al. [45]) irrespective of whether a company is or is not listed on a stock exchange, and may be useful in monitoring ongoing operations. This feature became the reason for using the above method in Polish agricultural enterprises. Most of them are not listed on the stock exchange, and any attempts to evaluate them or determine their market value are vague and methodologically complex (Józwiak and Kagan [47], Kozioł and Parlińska [48], Kondraszczuk [49]). The second reason for why the author decided to tackle this topic is the underestimation of the importance of human capital for organizations, especially the insufficient recognition of opportunities provided by it.

Although VAIC became a recognized business indicator of intellectual capital outcomes, discussions are still ongoing in the scientific community on whether it complies with the fundamental economic principles, according to which productive inputs may take the form of resources and flows. A. Pulić’s method makes these categories equal. This results in an equal treatment of all contributors to value added (being considered as resources). The consequence of this simplification is the absence of an economically important distinction between the resource- and flow-based nature of productive inputs. This is particularly important for labor inputs, which, when equated with a resource, made it possible for the employee market to emerge (Domański [50], Polak [51]). Today’s labor market is a labor flow market where parties sell and buy the right to use an individual’s predispositions (knowledge, skills, and experience) on defined conditions. The labor flow embedded in human resources and economically used in an enterprise is reflected by expenditure on staff. Within a specific period, usually one year, it is equivalent to the cumulative amount of pecuniary remunerations disbursed together with mandatory and optional benefits. A similar distinction between the two economic aspects of capital inputs leads to the conclusion that the total tangible resources of the enterprise (measured by A. Pulić as the net asset value) do not participate in the value-added creation process; instead, a contribution to value added is made by flows of tangible enterprise resources (measured as the value of consumption they bring to products and services). Its cumulative year-end value is the sum of depreciation and consumption of materials, energy, and external services. The methodological heterogeneity of components used in the VAIC calculation algorithm enables an unjustified, equal treatment of data retrieved from financial reports of static nature (resources) and dynamic nature (flows, expenses) included in the balance sheet and P&L account. Another argument for the flow-based assessment of intellectual capital is that the economic performance of an enterprise, traditionally measured as net profit, reflects the balance of cumulative incomes and costs within a specific period, and represents the flows which ultimately affect the changes in productive input resources at a given time (usually, the end of the year).

Taking the above into consideration, the author made an attempt to develop an alternative to VAIC based on a homogenous category of flows.

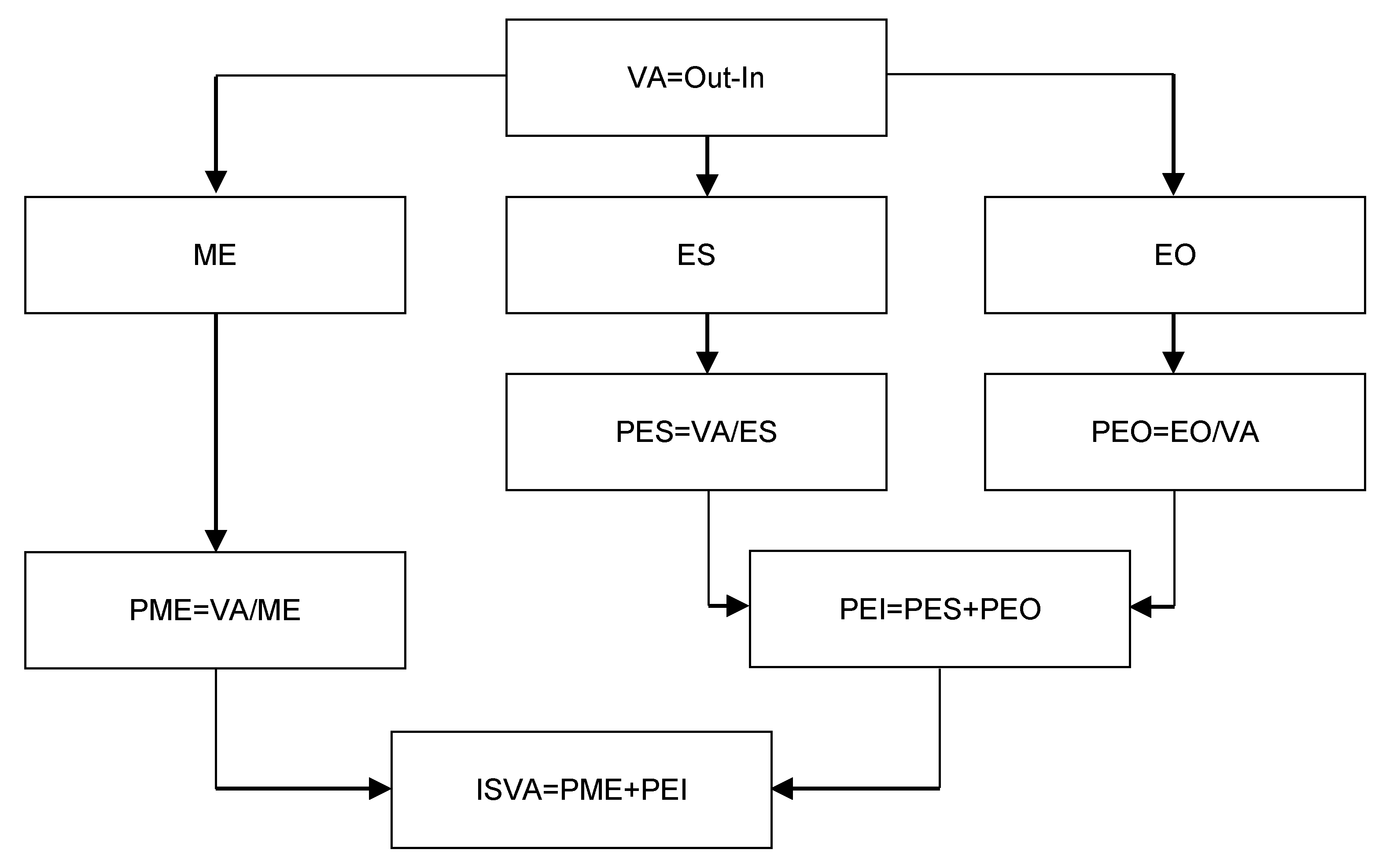

The yardstick proposed by the author, referred to as “Intellectual Sources of Value Added” (ISVA), is objective in showing the efficiency of material expenditure (consumption of fixed and current assets) and intellectual inputs (the use of knowledge, skills, experience, and other factors related to human labor) used in business operations [6,52] (see Figure 1.). The efficiency of inputs was assumed to be a reliable indicator of productivity, which also reveals the roles of tangible and intangible sources of value added [53].

The efficiency of value-added creation based on material expenditure is calculated as follows:

where:

PME: Productivity of tangible (material) expenditure,

VA: Value added, and

ME: Tangible (material) expenditure.

The productivity of expenditure on staff is calculated as:

where:

PES: Productivity of expenditure on staff,

VA: Value added, and

ES: Expenditure on staff.

The productivity of organizational and operational expenditure is:

where:

PEO: Productivity of organizational and operational expenditure of a company,

VA: Value added, and

EO: Other organizational and operational expenditures (calculated as total expenditure minus tangible expenditure and expenditure on staff).

ISVA (intellectual sources of value added) was calculated as the total of the above sub-indices:

The index calculated as the productivity of expenditure on staff plus productivity of organizational expenditure provides information on the productivity of corporate expenditure on intellectual (intangible) inputs, and is calculated as follows:

where:

PEI: Productivity of intellectual expenditure,

PES: Productivity of expenditure on staff, and

PEO: Productivity of organizational and operational expenditure of a company.

Research assumptions:

- Value added is the total of: Depreciation, remuneration, social insurance and other employee benefits, agricultural tax and fees, interest, income tax, and net profit.

- Material expenditure reflects the consumption of fixed and current assets (total of depreciation and material, energy, and external service consumption).

- Intellectual expenditure reflects the labor inputs (total of remuneration, social insurance, and other employee benefits) and other organizational and operational inputs (total of taxes and fees, other prime costs, and other operating costs).

- The sum of tangible and intangible inputs (expenditure) expresses the total value of expenditure incurred in the reporting period.

4. Results

The research assumptions were validated using numerical data from 120 Polish farms that delivered financial reports from 2005 to 2018 and operated as limited-liability companies.

4.1. VAIC™

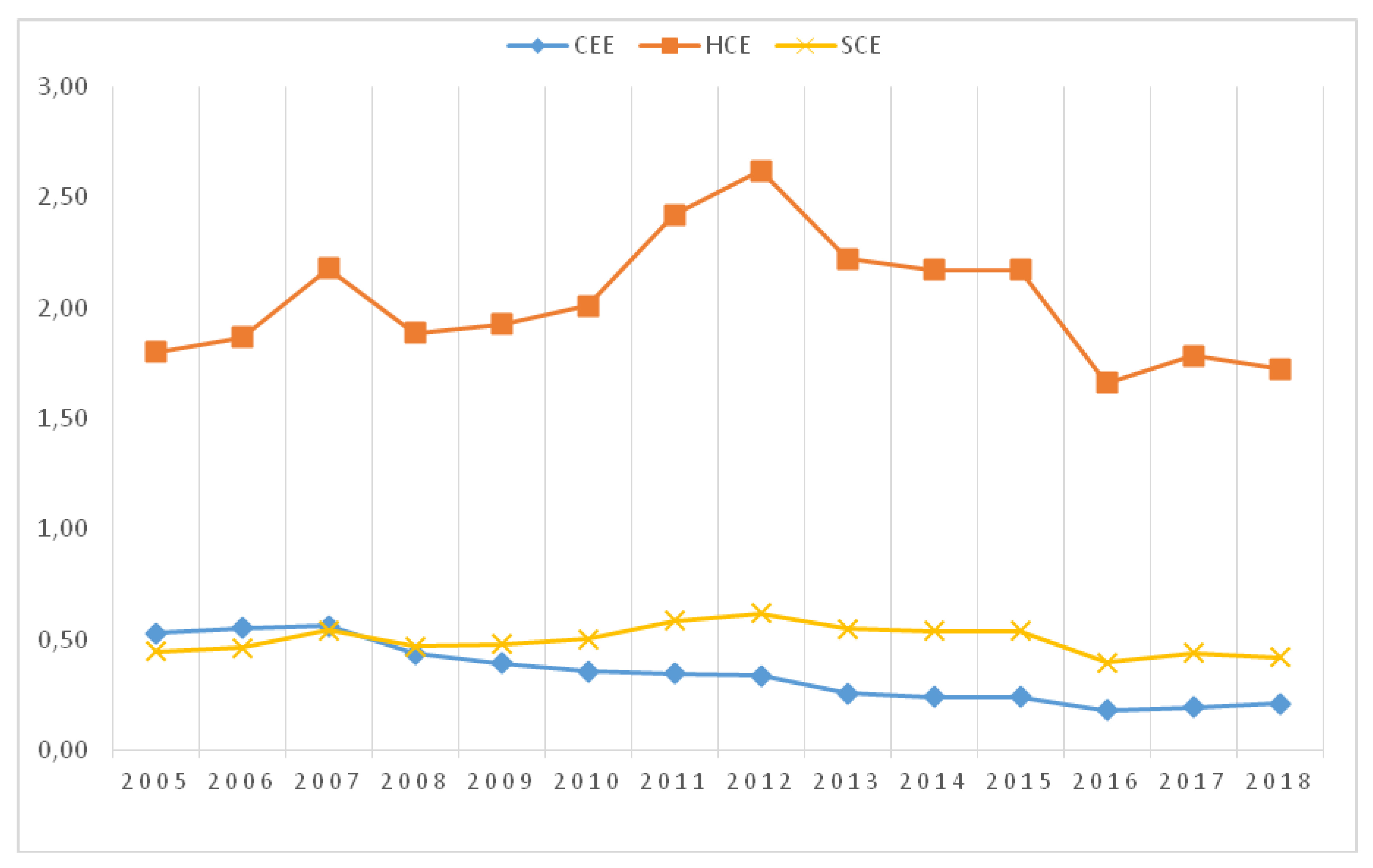

The analysis of sub-indexes suggests that the changes in VAIC were the consequence of two divergent trends: A decline in physical capital efficiency (from ca. 0.5 to 0.3) and a periodical change in intellectual capital efficiency (from ca. 1.7 to 2.6). Suppression of the increasing trend of human capital productivity use for the period after 2012 is connected with changes in the political, social, and economic environment of Polish agricultural entities (among others, Gross Domestic Product, fluctuation). There, it is significant that, even if physical capital efficiency decreases, the effectiveness of intellectual capital grows. This indicates the more flexible behavior of intellectual resources associated with employees and organizations (Table 1, Figure 2).

The above is a likely description of the situation where human labor becomes less and less substitutable with solutions derived from technological progress, though it was traditionally the case (Niezgoda [54]), Czyżewski [55]). In Poland, directly after joining the European Union, labor was efficiently substituted with capital (Wójcik and Nowak [56]). Note, however, that this can only occur if intellectual resources (knowledge, skills, experience, and organization) grow in parallel. What is also worrying is the low efficiency of structural capital use, even though both physical and structural capital are on the rise. With such an important level of financial and material expenditure in the agricultural business, it seems that the contribution of financial and material resources to structural capital (i.e., to the construction of the Information and Communication Technologies (ICT) infrastructure and databases, implementation of process software, etc.) should be much greater than the calculated amount.

The VAIC structure can be observed to follow a clear trend in the fourteen-year study period. Human capital efficiency (HCE) has a predominant share, varying in the range of 64.9% to 73.3% (70.7% on average). This confirms the importance of employee knowledge and skills in adding business value. The second most important component was structural capital efficiency (SCE) with a share ranging from 16.0% to 17.9% (17.4% on average), which emphasizes the importance of collective organizational efficiency of enterprises covered by this study. Note also that both HCE and SCE followed an upward trend, though to different extents (Table 2).

In the enterprises surveyed, the resources evolved at a different pace, which affected not only the levels of sub-indexes (CEE, HCE, SCE), but also the total Value-Added Intellectual Coefficient (VAIC). Two patterns were observed:

- Human capital was the most efficient in the value-adding process;

- in the enterprises surveyed, the share of intellectual capital efficiency (ICE = HCE + SCE) in the overall efficiency indicator was above 80%.

In total, intangible resources (HC and SC) contributed over 80% to value added while representing ca. 1/4 of physical and intangible resources. The average VAIC level for all enterprises in the study period was 2.9 (with CEE = 0.3, HCE = 2.0, SCE = 0.5). It follows from the above that an increase in human capital resources contributes to growth in value added more than other resources.

The level of physical capital employed was increasing faster than the value-added growth rate, and, therefore, its efficiency (CEE) was decreasing relatively steadily in the enterprises surveyed. This could suggest that a unit increase in value added requires an ever-increasing level of physical resources (physical capital), while intangible resources (intellectual capital) bring many more benefits.

4.2. ISVA

The calculations give grounds for concluding that, in 2005–2018, material and intangible inputs grew at a similar annual rate of ca. 13%. The growth rate is slightly higher for material inputs, reflecting the general trends followed by Polish large-scale agricultural holdings after the accession to the EU in 2004, i.e., a commitment to improve their technical and production equipment (expressed as the total of depreciation, materials and energy used, and external services). The above also suggests that the agricultural holdings surveyed are capable of absorbing new technical and technological solutions, can switch to better seed, breeding material, and other productive inputs, and use a growing share of outsourced services. At the same time, modernization processes remain strictly related to qualitative improvements in human capital; according to the relevant literature, this involves several processes, including an increase in wages [57,58,59,60,61]. This study corroborates that relationship (i.e., the growth rate of wages was similar to that of material inputs throughout the study period). Organizational and operational expenditure grew at the relatively fastest rate. This illustrates how much needs to be done to align the working environment with the requirements of a knowledge economy, especially as regards meeting the employees’ true needs (making repairs, providing office equipment) and empowering them with ICT tools (Internet, computers, databases, etc.). The above finding is also justified in the literature [62,63]. The required modernization efforts, the related expenditure, and the changing economic conditions resulted in relatively slower changes in value-added generation. This is confirmed by the values of sub-indices and of the cumulative ISVA index, as calculated under this test procedure (Table 3, Figure 3).

ISVA fluctuated around an average level of 2.7 (from 2.4 to 3.2). The productivity of intangible inputs (expenditure on organization and staff) had a decisive impact on ISVA (with 1.7 units of value added per 2.7 units of expenditure). The productivity of tangible inputs ranged from 0.5 to 0.7 and made a much smaller contribution to value added. Moreover, the productivity of intangible and tangible (material) changed at a similar pace (Figure 2), but the value growth was mainly driven by intangible inputs. This means that the agricultural enterprises covered by this study made effective use of complementarities between these inputs and were able to effectively generate new value based on synergies. The increased use of tangible (material) inputs due to the use of technically more efficient machinery and equipment, sophisticated seed, and breeding material enforced the improvement in employee knowledge and skills.

When plotted on a graph, these developments show a nearly linear growth of inputs (at various levels and growth rates), among which tangible (material) inputs prevail. However, intangible inputs (expenditure on human and organizational capital) are the most productive. In the longer term, this may result in higher productivity of total expenditure, driven by progress in technology and ITC and by employee knowledge and skills.

These findings are also confirmed by the analysis of the mix of inputs used in value-added creation processes in the agricultural enterprises surveyed. On average, the quantity of material inputs accounts for nearly 75% of the total inputs used, compared with 22.9% for expenditure on staff and 3.1% for organizational and operational expenditure (Table 4).

The analysis of tangible and intangible resources used in the agricultural enterprises surveyed is cause for thought regarding the need to consider these categories as a combined pool of agricultural resources. The use of intellectual assets is one of the key methods for making farming processes more efficient in a context of complex socioeconomic aspects affecting both the enterprises and their environment.

5. Discussion

It is difficult to find comprehensive empirical studies—other than those carried out by the author of this paper [64,65,66,67]—on the use of intellectual capital in agricultural holdings in Poland. This is due to numerous barriers, both objective (including differences in organizational and legal forms, difficulties in retrieving data from a sufficiently long period, etc.) and subjective (researchers see agriculture as a sector which poorly absorbs knowledge and is therefore of little interest for such studies). A few papers are available, which present case studies of specific operators or compare them within small groups (e.g., [68]) compare the findings from three mushroom production companies based on Calculated Intangible Value) or consider agriculture on a comprehensive basis, as an industry [69]. However, the findings of Łobos and Szewczyk [68] (calculated based on Calculated Intangible Value (CIV) are in line with the studies carried out by the present author; that is, the companies considered differ in the value of their intangible assets, which is largely consistent with the estimation of their economic standing.

Considering the above, it may be concluded that reasonable grounds exist for continued research efforts in this field. At the same time, note that the operational particularities of agricultural holdings pose a considerable barrier in accessing reliable analytical data. Therefore, there is a need to further develop methods based on financial statements that include ISVA, as described in this paper.

Regarding the comparison of the presented results of this study, it can be pointed out that:

- The importance of intangible assets in creation of value added was proven by both methods.

- The same fluctuation of productivity of human expenditures (HCE and PES) is the result of the similar way of calculation.

- There is a significant difference as concerns the productivity of tangible expenditures (CEE and PME). While CEE constantly declines, PME fluctuates similarly to human expenditures (PES). This behavior seems to be more realistic and coherent with changes in the functioning of enterprises enforced by internal and external conditions;

- Differences concerning fluctuation of productivity of structural capital (SCE and PEO) need further analysis, especially because there is not a precise definition of this factor in either method.

It should be underlined that VAICTM, though formally and mathematically correct, gives results of a doubtful practical nature. Under these circumstances, an investigation should be initiated to find a method that provides a more adequate reflection of business conditions in the agricultural sector. The result is ISVA, which provides a much more complete picture of patterns found in farming processes carried out by agricultural enterprises. The productivity of material expenditures (PME) calculated in accordance with the ISVA concept is high and grows steadily in line with the principles of rational management.

While not free of deficiencies, ISVA—an alternative, empirically tested method for determining the efficiency of intellectual capital in adding value to agricultural enterprises—could become a more precise tool for the comprehensive evaluation of agricultural holdings and more. In particular, this includes the comparison with empirical findings brought by VAIC™, according to which the sub-indicator of physical capital efficiency reveals a consistent decline in efficiency levels. This could suggest that the management make economically unsound decisions by investing in physical assets with a decreasing rate of financial efficiency. In the ISVA model, the sub-indicator of productivity of tangible inputs reveals a relatively stable level throughout the study period. Periodic volatility is compatible with the productivity of other inputs, and reflects the internal reorganization and changes in market conditions surrounding the agricultural holdings. At the same time, this indicator reflects the principle of complementarity of tangible and intellectual (human and structural) inputs.

Note that the efficiency of human capital and productivity of employee expenditure are identical in the two methods. This means that both of them identically define the equivalent of human capital and employee expenditure as cumulative cost streams relating to remunerations and benefits.

6. Conclusions

This paper presents the outcomes of efforts made to implement existing methods for assessing the effectiveness of intellectual capital, as well as the author’s own ISVA, which bridges a gap in the theory and practice of intellectual capital management in agricultural holdings. As a consequence, the following was concluded:

- ISVA is based on calculations that rely solely on flows (streams), which is consistent with fundamental economic principles, in opposition to VAICTM, the index of use efficiency of intellectual capital initially found to be suitable for research purposes. This demonstrates certain methodological flaws, as indicated by other authors, including the simultaneous use of resource- and flow-based values, which is inconsistent with fundamental economic principles and is unacceptable to the author of this paper.

- For VAICTM, the index results of empirical tests pointed out results of the calculation of tangible assets that were not coherent with reality.

- For ISVA, the index results of empirical tests pointed out results of the calculation of tangible and intangible assets that were more coherent with reality.

- The empirical tests of the VAICTM and ISVA methods enabled identification of the importance of intangible inputs and confirmed their important contribution to value added in the surveyed agricultural holdings.

- ISVA is better alternative method for determining the factors that contribute to creation of value added of agricultural enterprises, and complements the new tool proposed for comprehensive business evaluation in accordance with the assumptions of the economics of complexity [54].

The Intellectual Sources of Value Added (ISVA) is an indicator which makes it possible to assess the productivity of economically homogeneous categories of tangible (material) and intangible expenditure flows incurred by enterprises in value-adding processes. The results of detailed analyses using the ISVA method show that it reflects the processes taking place in the business practice of agricultural enterprises well.

The outcomes of the intellectual capital measurement methods listed in this paper provide an incentive for further studies on their suitability as a set of complementary indexes for business analysis of agricultural enterprises.

It should be kept in mind that the following recommendations are made for further research:

- Extending the scope of research to entities from other agribusiness links.

- Establishing benchmarks for the efficiency of using intellectual capital in other agribusiness enterprises. These values could be the benchmark for assessing the use of intangible assets.

- Extending research by making comparisons with companies in other sectors and countries.

A change in farming conditions, which results from economic megatrends on the one hand and from partly irreversible environmental shifts on the other, requires farmers to change the way that they see their resources. Processes related to knowledge and intellectual capital should play a leading role in the implemented business models, and need to be monitored with the use of specialized tools. The author believes the ISVA method presented in this paper to be an interesting measurement instrument suitable for use in day-to-day management operations for both agricultural holdings and operators active in other sectors.

Funding

This research received no external funding

Conflicts of Interest

The author declares no conflict of interest.

References

- Hunt, S.D.; Lambe, C.J. Marketing’s Contribution to Business Strategy: Market Orientation, Relationship Marketing and Resource-Advantage Theory. Int. J. Manag. Rev. 2000, 2, 17–43. [Google Scholar] [CrossRef]

- Van Hoek, R.I.; Chatham, R.; Wilding, R. Managers in supply chain management, the critical dimension. Supply Chain Manag. 2002, 7, 119–125. [Google Scholar] [CrossRef]

- Leśniewski, M.A. Kapitał intelektualny w kształtowaniu zrównoważonego rozwoju przedsiębiorstw. Ekon. I Organ. Przedsiębiorstwa 2015, 3, 14–25. [Google Scholar]

- Dal Mas, F. The Relationship between Intellectual Capital and Sustainability: An Analysis of Practitioner’s Thought. In Intellectual Capital Management as a Driver of Sustainability; Matos, F., Vairinhos, V., Selig, P., Edvinsson, L., Eds.; Springer: Berlin/Heidelberg, Germany, 2019. [Google Scholar]

- Januškaitė, V.; Užienė, L. Intellectual Capital as a Factor of Sustainable Regional Competitiveness. Sustainability 2018, 10, 4848. [Google Scholar] [CrossRef] [Green Version]

- Kozera-Kowalska, M. Kapitał Intelektualny w Tworzeniu Wartości Dodanej Przedsiębiorstw Rolnych; Poznan University of Life Sciences Publisher: Poznań, Poland, 2017. [Google Scholar]

- Edvisson, L.; Malone, M.S. Intellectual Capital: The Proven Way to Establish Your Company’s Real Value by Measuring Its Hidden Brainpower; Piatkus: London, UK, 1997. [Google Scholar]

- Stewart, T.A. Intellectual Capital. The New Wealth of Organizations; Nicholas Brealey Publishing: London, UK, 2003. [Google Scholar]

- Gu, F.; Lev, B. Intangible Assets: Measurements, Drivers, Usefulness, 2002. Available online: https://pdfs.semanticscholar.org/4d25/211f5ce58a92e9be781eebfd591ecae38985.pdf (accessed on 25 August 2018).

- Roos, G.; Roos, J. Measuring your company’s intellectual performance. Long Range Plan. 1997, 30, 413–426. [Google Scholar] [CrossRef]

- Urbanek, G. Pomiar Kapitału Intelektualnego i Aktywów Niematerialnych Przedsiębiorstwa; Wyd. Uniwersytetu Łódzkiego: Łódź, Poland, 2007. [Google Scholar]

- Dobija, M.; Indulska, M. Accountants and Accounting for Human Resources Accountability and Intellectual Entrepreneurship; Kwiatkowski, S., Edvinsson, L., Eds.; Knowledge Café for Intellectual Entrepreneurship: Warsaw, Poland, 1999. [Google Scholar]

- Pherson, P.K.M.; Pike, S. Accounting, empirical measurement and intellectual capital. J. Intellect. Cap. 2011, 2, 246–260. [Google Scholar] [CrossRef] [Green Version]

- White, F.C. Valuation of intangible capital in agriculture. J. Agric. Appl. Econ. 1995, 27, 437–445. [Google Scholar] [CrossRef] [Green Version]

- Alston, J.M. An analysis of Growth of US Farmland Prices 1963–1982. Am. J. Agric. Econ. 1986, 68, 1–9. [Google Scholar] [CrossRef]

- Allaire-Arrive, V. Protecting and Capitalizing on Intangible Agricultural Assets 2007. Available online: http://www.momagri.org/UK/points-of-view/Protecting-and-Capitalizing-on-Intangible-Agricultural-Assets_216.html (accessed on 12 March 2019).

- Moor, L.; Craig, L. Intellectual Capital in Enterprise Success: Strategy Revisited; John Wiley and Sons Inc.: Hoboken, NJ, USA, 2008; pp. 5–8. [Google Scholar]

- Goldsmith, P.; Gow, H. Strategic positioning under agricultural structural change: A critique of long jump co-operative ventures. Int. Food Agribus. Manag. 2005, 8, 1–21. [Google Scholar]

- Fulton, M.; Giannakas, K. Agricultural biotechnology and industry structure. J. Agrobiotechnology Ind. Struct. 2002, 4, 137–151. [Google Scholar]

- Sporleder, T.L.; Moss, L.E. Knowledge Capital, Intangible Assets, and Leverage, Evidence from US Agricultural Biotechnology Firms. Int. Food Agribus. Manag. Rev. 2004, 7, 26–36. [Google Scholar]

- Bontis, N. Assessing knowledge assets: A review of the models used to measure intellectual capital. Int. J. Manag. Rev. 2001, 3, 41–60. [Google Scholar] [CrossRef]

- Sveiby, K.-E. Methods for Measuring Intangibles Assets, 2001 (updated 27 April 2010). Available online: http://www.sveiby.com/articles/IntangibleMethods.htm (accessed on 29 July 2015).

- Pulic, A. Measuring the performance of intellectual potential in knowledge economy. In Proceedings of the 2nd World Congress on Measuring and Managing Intellectual Capital, McMaster University, Hamilton, ON, Canada, 21–24 January 1998; McMaster University: Hamilton, ON, Canada, 1998. [Google Scholar]

- Pulic, A. VAIC- An Accounting Tool for IC Management, 2000. Available online: http://www.measuring-ip.at/papers/ham99txt.htm (accessed on 20 December 2013).

- Rocznik Statystyczny Rzeczypospolitej Polskiej 2018. Available online: https://stat.gov.pl/download/gfx/portalinformacyjny/pl/defaultaktualnosci/5515/2/18/1/rocznik_statystyczny_rzeczypospolitej_polskiej_2018_.pdf (accessed on 21 September 2019).

- Ryś-Jurek, R. Porównanie sytuacji ekonomicznej polskich indywidualnych gospodarstw rolnych z gospodarstwami innych krajów UE w latach 2000–2005. Probl. World Agric. 2007, 2, 114–123. [Google Scholar]

- Józwiak, W. Polskie Rolnictwo i Gospodarstwa Rolne w Pierwszej i Drugiej Dekadzie XXI Wieku; Institute of Agricultural and Food Economics National Research Institute: Warszawa, Poland, 2013. [Google Scholar]

- Czubak, W.; Sadowski, A. Wpływ modernizacji wspieranych funduszami UE na zmiany sytuacji majątkowej w gospodarstwach rolnych w Polsce. J. Agribus. Rural Dev. 2014, 2, 45–57. [Google Scholar]

- Komnenic, B.; Tomic, D.V.; Tomic, G.R. Measuring efficiency of intellectual capital in agriculture sector of Vojvodina. Appl. Stud. Agribus. Commer. 2010, 4, 25–31. [Google Scholar] [CrossRef] [PubMed]

- Ghatak, S.; Ingersent, K. Agriculture and Economic Development; Harvester Press: Brighton, UK, 1984. [Google Scholar]

- Lee, K.; Yoo, J.; Choi, M.; Zo, H.; Ciganek, A.P. Does External Knowledge Sourcing Enhance Market Performance? Evidence from the Korean Manufacturing Industry. PLoS ONE 2016, 11, e0168676. [Google Scholar] [CrossRef] [PubMed]

- Vega-Jurado, J.; Gutiérrez-Gracia, A.; Fernández-de-Lucio, I. Does external knowledge sourcing matter for innovation? Evidence from the Spanish manufacturing industry. Ind. Corp. Chang. 2009, 18, 637–670. [Google Scholar] [CrossRef]

- Scafarto, V.; Ricci, F.; Scafarto, F. Intellectual capital and firm performance in the global agribusiness industry: The moderating role of human capital. J. Intellect. Cap. 2016, 17, 530–552. [Google Scholar] [CrossRef]

- Boljanovic, J.D.; Dobrijevic, G.; Cerovic, S.; Alcakovic, S.; Djokovic, F. Knowledge-based bioeconomy: The use of intellectual capital in food industry of Serbia. Amfiteatru Econ. 2018, 20, 717–731. [Google Scholar] [CrossRef]

- Yasnolob, I.; Chayka, T.; Gorb, O.; Shvedenko, P.; Protas, N.; Tereshchenko, I. Intellectual Rent in the Context of the Ecological, Social, and Economic Development of the Agrarian Sector of Economics. J. Environ. Manag. Tour. 2017, 7, 1442–1450. [Google Scholar]

- Cavicchi, C.; Vagnoni, E. Intellectual Capital in Support of Farm Businesses’ Strategic Management: A Case Study. J. Intellect. Cap. 2018, 19, 692–711. [Google Scholar] [CrossRef]

- Barrett, C.B.; Carter, M.R.; Timmer, C.P. A century-long perspective on agricultural development. Am. J. Agric. Econ. 2010, 92, 447–468. [Google Scholar] [CrossRef]

- Boehlje, M.; Roucan-Kane, M.; Bröring, S. Future agribusiness challenges: Strategic uncertainty, innovation and structural change. Int. Food Agribus. Manag. Rev. 2011, 14, 53–82. [Google Scholar]

- Cavicchi, C.; Vagnoni, E. Does intellectual capital promote the shift of healthcare organizations towards sustainable development? Evidence from Italy. J. Clean. Prod. 2017, 153, 275–286. [Google Scholar] [CrossRef]

- Parker, W. Agriculture and the environment: A codependent future requiring new technology, systems and expertise. In Proceedings of the 18th International Farm Managment Congress Methven, Christchurch, New Zealand, 20–25 March 2011; Congress Proceedings. ISBN 978-92-990056-7-5. Available online: http://ifmaonline.org/wp-content/uploads/2014/08/11_PL_Parker_P363-366.pdf (accessed on 27 August 2019).

- Hill, B.; Ray, D. Economics for Agriculture: Food, Farming and the Rural Economy; Macmillan Education: Basingstoke, UK; London, UK, 1987. [Google Scholar]

- Chavas, J.-P.; Aliber, M. An analysis of economic efficiency in agriculture: A nonparametric approach. J. Agric. Resour. Econ. 1993, 18, 1–16. [Google Scholar]

- Klepacki, B. Economic condition of peasant farms in the transformation period. Probl. Agric. Econ. 1997, 2–3, 37–46. [Google Scholar]

- Gębska, M.; Filipiak, T. Basics of Economics and Organization of Farms; Warsaw University of Life Sciences: Warszawa, Poland, 2006. [Google Scholar]

- Kasiewicz, S.; Rogowski, W.; Kicińska, M. Intellectual Capital as Seen by Stakeholders; Oficyna Ekonomiczna Publishing House: Krakow, Poland, 2006; pp. 93–94. [Google Scholar]

- Kunasz, M. Using VAIC™ to analyze the efficiency of the value adding process based on tangible and intangible assets: Research findings. Problemy Jakości 2006, 3, 15–21. [Google Scholar]

- Jóźwiak, W.; Kagan, A. Commercial farms vs. large-scale agricultural holdings. Agric. Sci. Yearb. 2008, 95, 22–30. [Google Scholar]

- Kozioł, D.; Parlińska, A. Factors affecting the value of agricultural property. Sci. Yearb. Assoc. Agric. Agribus. Econ. 2009, 11, 120–125. [Google Scholar]

- Kondraszczuk, T. Specific elements of financial analyses and assessments in the agriculture sector. Sci. J. Univ. Szczec. Financ. Financ. Mark. Insur. 2009, 20, 243–257. [Google Scholar]

- Domański, H. A Happy Slave Goes to Work: Attitudes towards Economic Activity of Women in 23 Countries; Publishing House IFiS PAN: Warsaw, Poland, 1999. [Google Scholar]

- Polak, T. Challenges and threats faced by the labor market in the context of today’s socio-economic transformation. Sel. Probl. Contemp. Econ. 2010, 4, 23–38. [Google Scholar]

- Kozera-Kowalska, M.; Baum, R. Measurement of intellectual capital in agricultural enterprises: A case study in Poland. In Proceedings of the Economics and Finance Conferences, International Institute of Social and Economic Sciences, Rome, Italy, 10–13 September 2018; pp. 209–220. [Google Scholar]

- Kulawik, J. Monitoring system for the efficiency and productivity of agricultural enterprises. Zagadnienia Ekonomiki Rolnej 2009, 3, 33–49. [Google Scholar]

- Niezgoda, M. Effectiveness of substituting human labor with capital in large-scale agricultural holdings. Ann. Pol. Assoc. Agric. Agribus. Econ. 2009, 11, 314–319. [Google Scholar]

- Czyżewski, B. Resource productivity in Polish agriculture in the context of sustainable development. Econ. Stud. 2012, 2, 165–189. [Google Scholar]

- Wójcik, E.; Nowak, A. Analysis of the substitution of human labor with capital in commercial farms in the first years after Poland joined the EU. Sci. J. Wars. Univ. Life Sci. Financ. Mark. 2012, 8, 505–517. [Google Scholar]

- Tamura, R. Human capital and the switch from agriculture to industry. J. Econ. Dyn. Control 2002, 27, 207–242. [Google Scholar] [CrossRef]

- Huffman, W.E.; Orazem, P.F. Agriculture and human capital in economic growth: Farmers, schooling and nutrition. In Handbook of Agricultural Economics; Evenson, R., Pingali, P., Eds.; Elsevier: Amsterdam, The Netherlands, 2007; Volume 3, pp. 2281–2341. [Google Scholar]

- Bogoviz, A.V.; Alekseev, A.N.; Lobova, S.V.; Telegina, Z.A.; Barcho, M.K. The human component of the process of improving productivity in the agrarian sector. Qual. Access Success 2018, 19, 166–170. [Google Scholar]

- Bukraba-Rylska, I. O potrzebie i korzyściach z badania wsi i rolnictwa w Polsce. Wieś i Rolnictwo 2018, 179, 13–30. [Google Scholar]

- Zegar, J. Rolnictwo w rozwoju obszarów wiejskich. Wieś i Rolnictwo 2018, 179, 31–48. [Google Scholar]

- Kalinowski, J. Technologie informatyczne a konkurencyjność w rolnictwie: Wybrane aspekty. Roczniki Naukowe Stowarzyszenia Ekonomistów Rolnictwa i Agrobiznesu 2008, 4, 161–166. [Google Scholar]

- Kocira, S.; Lorencowicz, E. Wykorzystanie technik komputerowych w gospodarstwach rodzinnych. Inżynieria Rolnicza 2011, 15, 77–83. [Google Scholar]

- Kozera, M. Kapitał Intelektualny w Rolnictwie–Zrozumieć, Zmierzyć, Zastosować. Prace Naukowe Uniwersytetu Ekonomicznego we Wrocławiu 2012, 262, 177–187. [Google Scholar]

- Kozera, M.; Kaliowski, S. Intellectual capital—Non-material element of farm businesses economic succes. In Proceedings of the International Conference on Management of Human Resources, Management—Leadership—Strategy—Competitiveness, Godollo, Hungary, 14–15 June 2012; Szent Istvan University: Godollo, Hungary, 2012; pp. 405–413. [Google Scholar]

- Kozera, M. Efektywność wykorzystania kapitału intelektualnego w przedsiębiorstwach rolniczych Wielkopolski. Przedsiębiorczość I Zarządzanie 2014, 15, 165–179. [Google Scholar]

- Kozera, M. Efektywność wykorzystania kapitału intelektualnego przedsiębiorstw rolniczych w Polsce. Roczniki Naukowe Ekonomii Rolnictwa i Rozwoju Obszarów Wiejskich 2015, 102, 37–46. [Google Scholar]

- Łobos, K.; Szewczyk, M. Pomiar kapitału intelektualnego i jego wpływ na efektywność przedsiębiorstw produkujących podłoże pod uprawę pieczarek. J. Agribus. Rural Dev. 2013, 1, 143–152. [Google Scholar]

- Wilkin, J. Can economics be beautiful? Discussing the subject matter and methods of economics. Economist 2009, 3, 295–313. [Google Scholar]

Figure 1.

Calculation procedure for the intellectual sources of value added (ISVA) concept. Abbreviations are defined below Figure 1.

Figure 1.

Calculation procedure for the intellectual sources of value added (ISVA) concept. Abbreviations are defined below Figure 1.

Figure 2.

Productivity of the Value-Added Intellectual Coefficient (VAICTM). Source: Table 1. CEE-Capital Employed Efficiency; HCE-Human Capital Efficiency, SCE-Structural Capital Efficiency.

Figure 2.

Productivity of the Value-Added Intellectual Coefficient (VAICTM). Source: Table 1. CEE-Capital Employed Efficiency; HCE-Human Capital Efficiency, SCE-Structural Capital Efficiency.

Figure 3.

Productivity of intellectual sources of value added (ISVA). Source: Table 3. PME-productivity of tangible (material) expenditure, PES-Productivity of expenditure on staff, PEO-Productivity of organizational and operational expenditure of a company.

Figure 3.

Productivity of intellectual sources of value added (ISVA). Source: Table 3. PME-productivity of tangible (material) expenditure, PES-Productivity of expenditure on staff, PEO-Productivity of organizational and operational expenditure of a company.

{kind=link}

{kind=link}

{kind=link}

Table 1.

Level of value added and the productivity of its creation from expenditure on tangible and intangible inputs in agricultural holdings covered by this study, including the average (Ave.) for 2005–2018.

Table 1.

Level of value added and the productivity of its creation from expenditure on tangible and intangible inputs in agricultural holdings covered by this study, including the average (Ave.) for 2005–2018.

| Specification | Years | |||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 2005 | 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | Ave. | ||

| Expenditure (thousand PLN) | ||||||||||||||||

| Value of Net Assets (CE) | 3273 | 3358 | 4415 | 5316 | 6002 | 6978 | 8869 | 10358 | 11479 | 12455 | 12455 | 13003 | 13219 | 12051 | 8802 | |

| Intangible | Human Capital (HC) | 963 | 996 | 1137 | 1225 | 1222 | 1240 | 1263 | 1337 | 1323 | 1374 | 1374 | 1404 | 1435 | 1461 | 1268 |

| Structural Capital Value (SC) | 771 | 863 | 1341 | 1088 | 1131 | 1250 | 1796 | 2166 | 1617 | 1610 | 1610 | 927 | 1126 | 1058 | 1311 | |

| Value Added (VA) | 1733 | 1860 | 2478 | 2312 | 2353 | 2490 | 3059 | 3502 | 2940 | 2984 | 2984 | 2331 | 2562 | 2518 | 2579 | |

| Productivity of Expenditure (%) | ||||||||||||||||

| Capital Employed Efficiency (CEE) | 0.53 | 0.55 | 0.56 | 0.43 | 0.39 | 0.36 | 0.34 | 0.34 | 0.26 | 0.24 | 0.24 | 0.18 | 0.19 | 0.21 | 0.34 | |

| Intangible | Human Capital Efficiency (HCE) | 1.80 | 1.87 | 2.18 | 1.89 | 1.93 | 2.01 | 2.42 | 2.62 | 2.22 | 2.17 | 2.17 | 1.66 | 1.78 | 1.72 | 2,03 |

| Efficiency of Structural Capital (SCE) | 0.44 | 0.46 | 0.54 | 0.47 | 0.48 | 0.50 | 0.59 | 0.62 | 0.55 | 0.54 | 0.54 | 0.40 | 0.44 | 0.42 | 0.50 | |

| Value Added Intellectual Coefficient (VAICTM) | 2.77 | 2.88 | 3.28 | 2.79 | 2.80 | 2.87 | 3.35 | 3.58 | 3.03 | 2.95 | 2.95 | 2.24 | 2.42 | 2.35 | 2.88 | |

Source: Own study.

Table 2.

Structure of tangible and intangible inputs for the Value-Added Intellectual Coefficient (VAIC) for the agricultural companies surveyed, including the average (Ave.) for 2005–2018.

Table 2.

Structure of tangible and intangible inputs for the Value-Added Intellectual Coefficient (VAIC) for the agricultural companies surveyed, including the average (Ave.) for 2005–2018.

| Specification | Years | |||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 2005 | 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | Ave. | ||

| Expenditure (%) | ||||||||||||||||

| Value of Net Assets (CE) | 65.38 | 64.36 | 64.05 | 69.69 | 71.83 | 73.70 | 74.35 | 74.73 | 79.61 | 80.67 | 80.67 | 84.80 | 83.77 | 82.71 | 75.02 | |

| Intangible | Expenditure on Staff (ES) | 19.23 | 19.09 | 16.50 | 16.05 | 14.62 | 13.10 | 10.59 | 9.65 | 9.18 | 8.90 | 8.90 | 9.16 | 9.10 | 10.02 | 12.43 |

| Expenditure on Organization (EO) | 15.39 | 16.55 | 19.45 | 14.26 | 13.54 | 13.20 | 15.06 | 15.62 | 11.21 | 10.43 | 10.43 | 6.04 | 7.14 | 7.26 | 12.54 | |

| Value Added (VA) | 100 | 100 | 100 | 100 | 100 | 100 | 100 | 100 | 100 | 100 | 100 | 100 | 100 | 100 | 100 | |

| Productivity of Expenditure (%) | ||||||||||||||||

| Capital Employed Efficiency (CEE) | 19.09 | 19.20 | 17.10 | 15.57 | 14.01 | 12.45 | 10.29 | 9.45 | 8.46 | 8.12 | 8.12 | 8.01 | 8.01 | 8.88 | 11.91 | |

| Intangible | Human Capital Efficiency (HCE) | 64.89 | 64.71 | 66.41 | 67.59 | 68.81 | 70.04 | 72.21 | 73.26 | 73.38 | 73.60 | 73.60 | 74.21 | 73.80 | 73.27 | 70.70 |

| Efficiency of Structural Capital (SCE) | 16.02 | 16.09 | 16.49 | 16.84 | 17.18 | 17.51 | 17.50 | 17.29 | 18.16 | 18.28 | 18.28 | 17.77 | 18.18 | 17.85 | 17.39 | |

| Value Added Intellectual Coefficient (VAIC) | 100 | 100 | 100 | 100 | 100 | 100 | 100 | 100 | 100 | 100 | 100 | 100 | 100 | 100 | 100 | |

Source: Own study.

Table 3.

Level of value added and the productivity of its creation from expenditure on tangible and intangible inputs in agricultural holdings covered by this study, including the average for 2005–2018.

Table 3.

Level of value added and the productivity of its creation from expenditure on tangible and intangible inputs in agricultural holdings covered by this study, including the average for 2005–2018.

| Specification | Years | |||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 2005 | 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | Ave. | ||

| Expenditure (thousand PLN) | ||||||||||||||||

| Material Expenditure (ME) | 2902 | 3166 | 3642 | 3996 | 3794 | 3816 | 4189 | 4714 | 4533 | 4781 | 4781 | 4545 | 4451 | 4377 | 4120 | |

| Intangible | Expenditure on Staff (ES) | 963 | 966 | 1137 | 1225 | 1222 | 1240 | 1263 | 1337 | 1323 | 1374 | 1374 | 1374 | 1435 | 1461 | 1268 |

| Expenditure on Organization (EO) | 130 | 127 | 137 | 160 | 152 | 163 | 182 | 212 | 223 | 187 | 187 | 177 | 206 | 217 | 175 | |

| Value Added (VA) | 1733 | 1860 | 2478 | 2312 | 2353 | 2490 | 3059 | 3502 | 2940 | 2984 | 2984 | 2331 | 2562 | 2518 | 2579 | |

| Productivity of Expenditure (%) | ||||||||||||||||

| Productivity of Material Expenditure (PME) | 0.60 | 0.59 | 0.68 | 0.58 | 0.62 | 0.65 | 0.73 | 0.74 | 0.65 | 0.62 | 0.62 | 0.51 | 0.58 | 0.58 | 0.63 | |

| Intangible | Productivity of Expenditure on Staff (PES) | 1.80 | 1.87 | 2.18 | 1.89 | 1.93 | 2.01 | 2.42 | 2.62 | 2.22 | 2.17 | 2.17 | 1.66 | 1.78 | 1.72 | 2.03 |

| Productivity of Expenditure on Organization (PEO) | 0.07 | 0.07 | 0.06 | 0.07 | 0.06 | 0.07 | 0.06 | 0.06 | 0.08 | 0.06 | 0.06 | 0.08 | 0.08 | 0.09 | 0.07 | |

| Intellectual Sources of Value Added (ISVA) | 2.47 | 2.52 | 2.91 | 2.54 | 2.61 | 2.73 | 3.21 | 3.42 | 2.95 | 2.86 | 2.86 | 2.25 | 2.44 | 2.39 | 2.73 | |

Source: Own study.

Table 4.

Structure of tangible and intangible inputs for intellectual sources of value added (ISVA) for the agricultural companies surveyed, including the average (Ave.) for 2005–2018.

Table 4.

Structure of tangible and intangible inputs for intellectual sources of value added (ISVA) for the agricultural companies surveyed, including the average (Ave.) for 2005–2018.

| Specification | Years | |||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 2005 | 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | Ave. | ||

| Expenditure (%) | ||||||||||||||||

| Material Expenditure (ME) | 72.65 | 73.82 | 74.09 | 74.26 | 73.42 | 73.12 | 74.35 | 75.27 | 74.56 | 75.39 | 75.39 | 74.19 | 73.05 | 72.29 | 73.99 | |

| Intangible | Expenditure on Staff (ES) | 24.10 | 23.22 | 23.13 | 22.76 | 23.64 | 23.76 | 22.42 | 21.35 | 21.77 | 21.66 | 21.66 | 22.92 | 23.56 | 24.12 | 22.86 |

| Expenditure on Organization (EO) | 3.25 | 2.96 | 2.78 | 2.98 | 2.94 | 3.12 | 3.23 | 3.38 | 3.67 | 2.95 | 2.95 | 2.88 | 3.39 | 3.58 | 3.15 | |

| Value Added (VA) | 100 | 100 | 100 | 100 | 100 | 100 | 100 | 100 | 100 | 100 | 100 | 100 | 100 | 100 | 100 | |

| Productivity of Expenditure (%) | ||||||||||||||||

| Productivity of Material Expenditure (PME) | 24.16 | 23.28 | 23.35 | 22.82 | 23.76 | 23.94 | 22.74 | 21.70 | 22.02 | 21.83 | 21.83 | 22.81 | 23.58 | 24.12 | 23.00 | |

| Intangible | Productivity of Expenditure on Staff (PES) | 72.82 | 74.01 | 74.76 | 74.45 | 73.77 | 73.66 | 75.41 | 76.53 | 75.41 | 75.97 | 75.97 | 73.82 | 73.12 | 72.27 | 74.43 |

| Productivity of Expenditure on Organization (PEO) | 3.03 | 2.70 | 1.89 | 2.73 | 2.47 | 2.40 | 1.85 | 1.77 | 2.57 | 2.19 | 2.19 | 3.37 | 3.30 | 3.61 | 2.58 | |

| Intellectual Sources of Value Added (ISVA) | 100 | 100 | 100 | 100 | 100 | 100 | 100 | 100 | 100 | 100 | 100 | 100 | 100 | 100 | 100 | |

Source: Own study.

© 2020 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Kozera-Kowalska, M. Intellectual Capital: ISVA, the Alternative Way of Calculating Creating Value in Agricultural Entities—Case of Poland. Sustainability 2020, 12, 2645. https://0-doi-org.brum.beds.ac.uk/10.3390/su12072645

AMA Style

Kozera-Kowalska M. Intellectual Capital: ISVA, the Alternative Way of Calculating Creating Value in Agricultural Entities—Case of Poland. Sustainability. 2020; 12(7):2645. https://0-doi-org.brum.beds.ac.uk/10.3390/su12072645

Chicago/Turabian StyleKozera-Kowalska, Magdalena. 2020. "Intellectual Capital: ISVA, the Alternative Way of Calculating Creating Value in Agricultural Entities—Case of Poland" Sustainability 12, no. 7: 2645. https://0-doi-org.brum.beds.ac.uk/10.3390/su12072645

Note that from the first issue of 2016, this journal uses article numbers instead of page numbers. See further details here.