What Drives Stocks during the Corona-Crash? News Attention vs. Rational Expectation

Faculty of Business and Economics, TU Dortmund University, Chair of Finance, Otto-Hahn-Str. 6, 44227 Dortmund, Germany

*

Author to whom correspondence should be addressed.

†

These authors contributed equally to this work.

Sustainability 2020, 12(12), 5014; https://0-doi-org.brum.beds.ac.uk/10.3390/su12125014

Submission received: 28 April 2020

/

Revised: 15 June 2020

/

Accepted: 17 June 2020

/

Published: 19 June 2020

(This article belongs to the Special Issue The Influence of COVID-19 on Sustainable Economy)

Abstract

:We explore if the corona-crash 2020 was driven by news attention or rational expectations about the pandemic’s economic impact. Using a sample of 64 national stock markets covering 94% of the world’s GDP, we find the stock markets’ decline to be mainly associated with higher news attention and less with rational expectation. We estimate the economic cost from the news hype to amount to USD 3.5 trillion for the US and USD 200 billion on average for the rest of the G8 countries.

1. Introduction

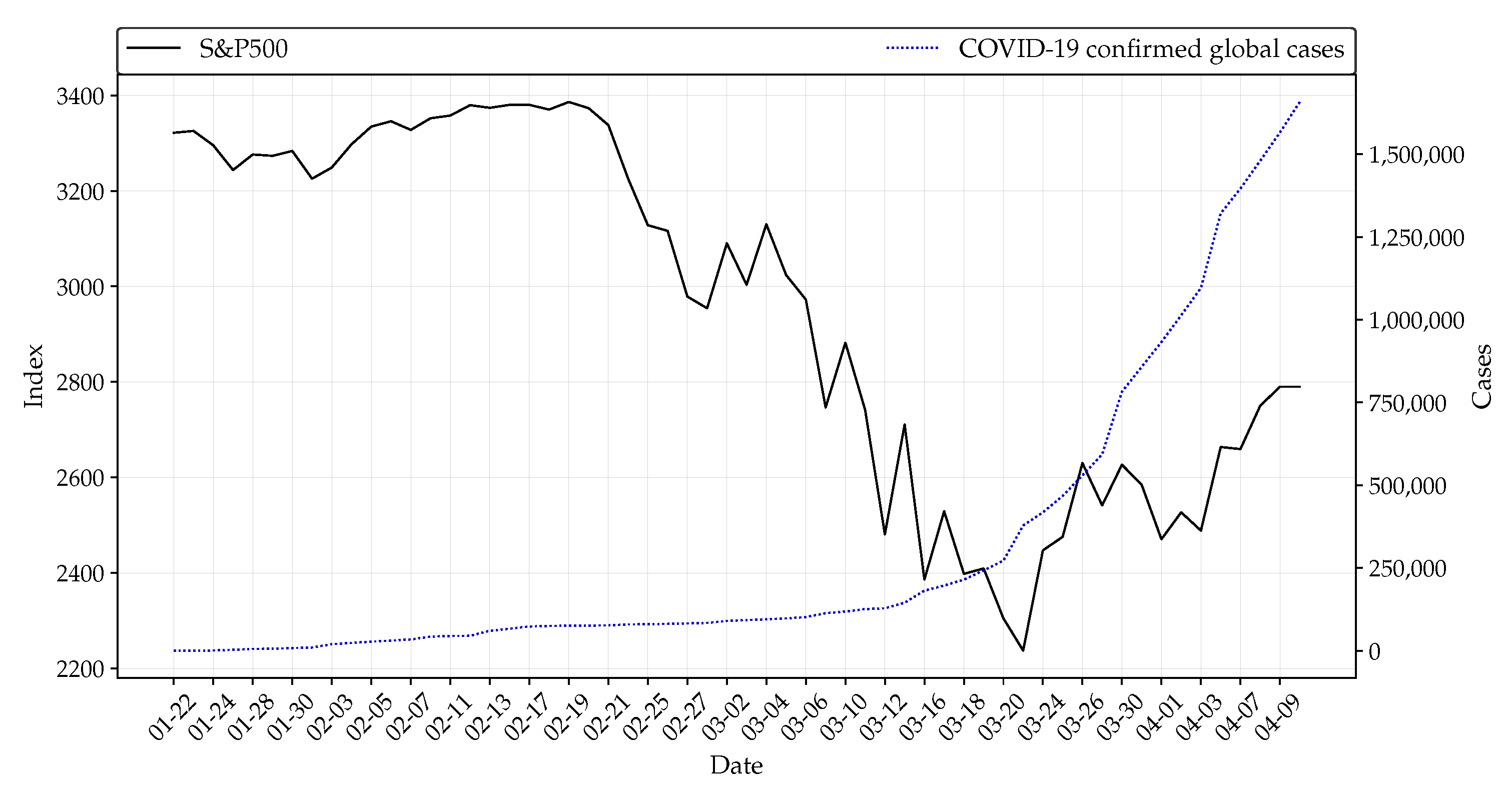

The spread of the coronavirus Sars-CoV-2 causing the disease called COVID-19 hit the world’s economy unprepared. The increasing number of infections has not only led to countermeasures by the affected countries’ governments but also resulted in a severe decline in stock markets. For instance, the S&P500 dropped by 33% from its all-time high during the corona stock market crash (see Figure 1).

While several recent studies show negative stock market reactions to the most severe pandemic since the spanish flu in 1918 [1,2,3], the question still remains to what extent this was driven by (bounded) rational expectations. In this paper we explore whether such expectations prevail over a news hype which could have driven traders into panic mode. Our aim is to study the short-term effects on global financial markets during the ongoing COVID-19 crisis.

As proxies for bounded rational expectation we use both the growth rates from the exponential fit as well as the epidemiologists’ susceptible–infectious–recovered (SIR) model by Hethcote [4]. This is because without countermeasures in place, a pandemic grows exponentially [5], while in later stages the growth of infections starts following a logistic function with increasing herd immunity. We refer to the concept of bounded rationality, because if models are not correctly specified by individuals with cognitive limitations, they might result in non-rational expectations [6,7]. However, we believe that the underlying models used in this study represent the best alternatives to approximate the severity of the current COVID-19 pandemic. For brevity, we denote our measures of bounded rational expectation as rational expectation throughout the paper.

News attention is proxied by Google’s abnormal search volume [8]. We hereby refer to the concept of rational inattention. Although news may be biased and incomplete, investors and especially retail investors may nonetheless rely on them to make their investment decisions because fitting models on real data is time consuming and requires cognitive effort which may be too costly [9]. However, when relying on news as the primary source of information for investment decision making, investors are confronted with the negativity bias. As psychological literature shows, people pay increased attention to negative information [10,11,12]. In the economic context, Carroll [13] and Garz [14] even highlight repeated media coverage leading the public into forming rather pessimistic “expectations” than rational expectations.

Using stock market indices from 64 countries, covering 94% of the world’s GDP, we find the stock markets’ decline to be mainly associated with higher news attention and less with rational expectation. Over our entire observation period, a one standard deviation increase in news attention leads to a decrease of 0.279 standard deviations of market returns, while a one standard deviation increase in our rational expectation measure results in a decrease of 0.131 standard deviations of market returns. This imposes significant economic costs. For instance, we estimate the economic cost for the US stock market resulting from the news hype to amount to USD 3.5 trillion until April 2020.

Our findings also imply investors should rather focus on news attention than on rational expectation when making their investment decisions during a crisis. Comparing three different investment strategies, we find a strategy focusing on news attention during the corona crisis to outperform both a buy and hold strategy and a strategy based on rational expectation. This is in line with the findings from psychology highlighting the increased attention to negative information.

The remainder of this paper is structured into a literature review, a description of the data and methodology used, followed by a discussion of the results, and a final conclusion.

2. Literature Review

There is an evolving strand of literature on the impact of COVID-19 on global financial markets. Baker et al. [15], Liu et al. [1], Zhang et al. [2], and Ali et al. [16] show the COVID-19 pandemic having induced an enormous level of uncertainty accompanied by high market volatility and significant negative market returns across all affected countries. Zaremba et al. [17] even show that countries’ policy interventions increase stock market volatility.

Higher growth rates of confirmed COVID-19 cases also result in negative effects for companies as investors and analysts became extremely concerned about corporate debt and liquidity [18,19,20]. Especially, companies whose corporate identity is related to the term ‘corona’ are experiencing additional pressure and exhibit abnormal losses [21].

Contagion effects of the crisis have been analyzed by Conlon and McGee [22], Corbet et al. [23] and Ji et al. [24] who focus on cryptocurrencies, gold, and commodity futures. During the COVID-19 pandemic Bitcoin does not act as a safe-haven nor does it offer any hedging opportunities. Gold and soybean futures, however, are seen as safe-havens in the current crisis. Moreover, Sharif et al. [3] examine the relationship between the COVID-19 outbreak, the oil price and the US stock market. They show that news concerning oil prices and the pandemic appear to be a driver of the US financial market. This is in line with the paper by Mamaysky [25] who shows news sentiment to explain volatility among several asset classes in the US.

Based on the studies mentioned above investigating the stock markets’ reaction to the crisis, our paper contributes by disentangling potential drivers, namely news attention and rational expectation. Furthermore, we contribute to the literature by measuring the economic costs resulting from news attention.

3. Data and Methodology

We obtained daily data on confirmed COVID-19 cases per country from 22 January 2020 to 9 April 2020 from Johns Hopkins University and daily Google search volume (SVI) for the keyword “corona” for each affected country as well as daily closing prices of the country’s lead stock market index from Trading Economics. Our final sample consisted of daily data for 64 countries covering 94% of the world’s GDP. Table A1 in the Appendix A holds a list of countries covered.

To estimate the news attention we calculated an abnormal Google search volume index (ASVI), which was also commonly used to measure retail investor attention [8,26]. Plante [27] shows search volume to strongly correlate with news attention as the amount of news the public is confronted with translates into a rise of related Google searches. Since we investigate a rather small time window, we adjusted the measure proposed by Da et al. [8] by calculating our news coverage variable () as the natural log of the search volume on trading day minus the natural log of the median search volume over the previous five trading days.

To estimate rational expectations of the corona pandemic we turn to epidemiological models. For infectious diseases such as COVID-19, the spread of infections is initially characterized by an exponential growth in time [28]. Using the data from Johns Hopkins University, we fit the number of infections to an exponential growth model with being the number of infections at time t, being the initial value of P, and b being the exponential growth rate. We calculated daily exponential growth rates by fitting the exponential growth model and used the change in growth rates between two days as proxy for a rational investor’s expectation.

In later stages of the pandemic and as countermeasures unfold, the exponential growth is weakened and the infections start following a logistic function. This is incorporated in the epidemiological standard model—the Susceptible–Infectious–Recovered model (SIR) [4,29]. This model uses both the number of infected individuals and the number of susceptible and recovered individuals in a population. Based on the assumption of immunity of recovered individuals the SIR model derives from a set of differential equations as the transmissions between the groups of individuals are formulated as derivatives. Following Ma [30] the model equations are

where is the number of susceptible individuals at time t, is the number of infected individuals at time t, is the number of recovered individuals, is the transmission rate per infectious individual, and is the recovery rate. The overall number of individuals is considered as a constant. The expected growth rate of the SIR model can be calculated as . As above, we also fit the SIR model at each time step and use the changes in growth rates between t and as an independent variable for a rational investor’s expectation in additional regression models.

Table 1 provides descriptive statistics for the variables in our sample. Mean daily log returns of the stock market indices were negative over our observation period indicating the massive impact of the COVID-19 pandemic. The lower mean of compared to the median of is related to large drops on single days, especially on “Black Thursday” 12 March 2020 where the S&P500 dropped by 10% marking the worst day since the stock market crash in 1987 [31]. The changes of the exponential growth rates and SIR growth rates exhibited a positive mean. News coverage based on the ASVI for the keyword “corona” had a positive mean of .

To examine the impact of news attention and rational investor expectation on the development of stock markets during the COVID-19 crisis, we consider the following straightforward regression model

where i is the country and t denotes the trading day. is the stock market return for country i at time t. The expected exponential growth rate is used as our measure for rational expectation, while measures news attention for the keyword “corona”. We use the lagged log returns of the national stock market indices to control for all other market effects [32].

Since with a lagged dependent variable the regressors are no longer exogenous and the ordinary least squares (OLS) estimator is biased and inconsistent (e.g., [33]), we estimate the model using the generalized method of moments (GMM) estimator, which provides consistent and unbiased estimates for dynamic panel data models—especially for panel datasets with small time periods T relative to the number of individuals N [34,35].

4. Results and Discussion

Table 2 shows the regression results where for the purpose of comparison, all variables are scaled to have a standard deviation of one and weighted by their country’s GDP.

In Model (1), we used the expected exponential growth rate and news attention as our main independent variables. We also included the one-day lagged market return as an independent variable. As the results show, all regression coefficients were negative and statistically significant. However, the coefficient on news attention was larger in magnitude than the coefficient on our rational expectation variable; thus indicating news attention to be the dominant driver of the drop in stock prices over the entire observation period. To put this into perspective, a one standard deviation increase in news attention leads to a decrease of 0.279 standard deviations of market returns, while a one standard deviation increase in our rational expectation variable results in a decrease of 0.131 standard deviations of market returns. Further, the coefficient on the one-day lagged market return was larger in magnitude compared to our rational expectation variable. This implies yesterday’s market development to have a larger impact than the rational expectation for tomorrow.

In Model (2), we estimated the model using the changes in growth rates of our SIR model as the independent variable. The coefficients on the one-day lagged market return and news attention are negative, similar in size, and also statistically significant. The coefficient on our rational expectation variable, however, is not statistically significant. This is mostly in line with our results found in Model (1) indicating the large impact of news attention on stock markets during the COVID-19 crisis.

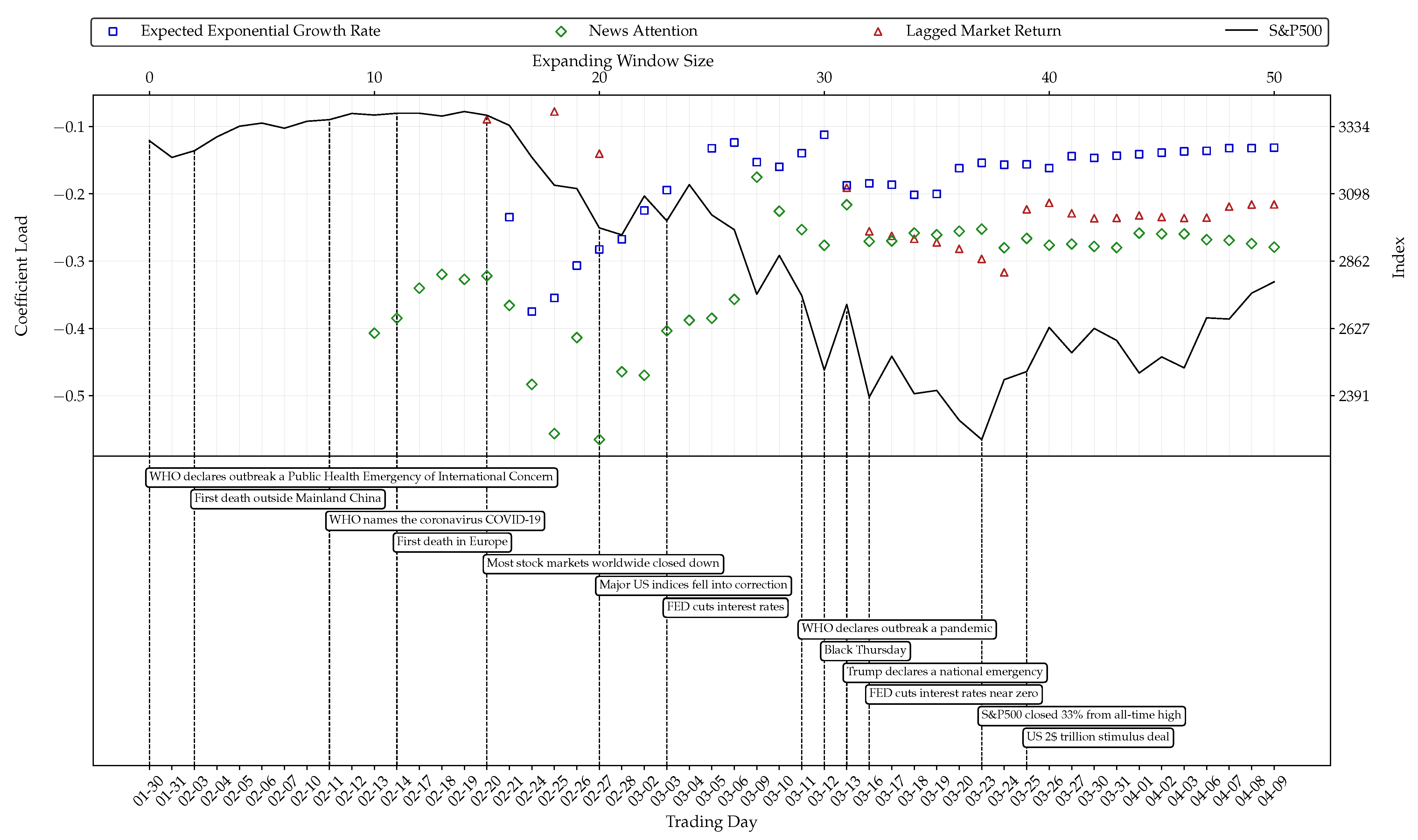

Figure 2 displays statistically significant coefficients from expanding window regressions using the GMM estimator with the same model specification as used in Model (1). We also show the development of the S&P500 and present major news events during the corona crisis as points of reference.

Our first estimation window contained data for the period from 30 January 2020 through 12 February 2020. From this point on, we gradually expand our sample by adding data for one additional trading day. Hence, the last estimation is based on our entire sample for the period from 30 January 2020 through 9 April 2020. As shown in Figure 2, we find negative and statistically significant coefficients on news attention for almost all window sizes, which are also larger in magnitude compared to our rational expectation variable. Thus, this supports our findings from Table 2 showing news attention to have an important impact on the stock price development during the COVID-19 crisis.

Figure 2 also shows, for small window sizes ranging from 10 to 15, the rational expectation variable not to be statistically significant in our model. By extending the window sizes (16 to 30), the coefficients on our rational expectation variable become significant, which goes along with the drop in stock markets. However, the coefficients on news attention are nonetheless larger in magnitude for most window sizes. Furthermore, by extending our window size the coefficients on our variables exhibit less volatility.

4.1. Investment Strategies

To test whether an investor focusing on news attention rather than rational expectation is more successful during the corona crisis, we constructed three different portfolios: a “buy-and-hold portfolio”, which invests into the stock market index only, a “news attention” portfolio, and a “rational expectation” portfolio. We assume no transaction costs and do not allow short selling. The news attention investor, as well as the rational expectation investor, buys each stock market index at the beginning and uses buy and sell signals for her investment decisions until the end of the time period. Each investor only holds one stock market index in her portfolio instead of building an efficient portfolio which contains all the companies of the respective stock market index. We use the coefficients from the expanding window regressions in Figure 2 as buy and sell signals. Both the news attention and the rational investor increase or decrease their portfolio holdings according to the trading signal at each point in time.

Table 3 reports the mean returns of the three different portfolios. Panel A compares the mean returns of the buy-and-hold portfolio with the mean returns of the news attention portfolio. Although both portfolios realized a negative mean return during the crisis, the loss from the news attention portfolio was at least percentage points smaller than the loss from the buy-and-hold portfolio. In Panel B, we compare the buy and hold portfolio with the rational investor portfolio. Again both portfolios realized a negative return, but the mean return of the rational expectation portfolio was higher. Finally, Panel C compares the mean returns of the news attention portfolio with the mean returns of the rational investor portfolio. The loss from the news attention portfolio was at least percentage points smaller compared to the rational investor portfolio. This stresses that an investor focussing on news attention during the corona crisis to outperform both a buy-and-hold investor as well as a rational expectation investor. Further, it underlines the findings from psychology literature showing the increased attention to negative information.

4.2. Economic Costs

To estimate the economic costs resulting from the focus on news rather than rational expectation, we first performed one-day-ahead predictions per country using our econometric model’s estimators:

As shown above, we estimated a model including our coefficient for news attention as well as a model excluding our coefficient for news attention. We then accumulate the estimated returns and calculate the difference to separate the effect of trading based on news attention from trading based on rational expectation. Finally, we multiply this difference with the market capitalization of the respective stock market to estimate the economic costs per country. Table 4 reports the results for the G8 countries.

As the results show, trading based on news attention during the corona crisis has a large impact on the respective stock markets. For instance, the economic cost for the US stock market amount to approx. USD 3,469,174 million. In relation to the market capitalization, the effect is even larger for Germany where the economic cost due to trading based on news attention amount to approx. USD 276,017 million.

4.3. Robustness

For robustness purposes, we also estimated OLS regressions using the log returns of the national stock market indices as the dependent variable, while using our rational expectation variable and news attention as the main independent variables of interest. We also included the lagged log return of the S&P500 as a control variable. Using the lagged log return of the S&P500 allowed us to receive consistent OLS coefficient estimates because there was no dynamic adjustment in the econometric model. Moreover, empirical literature since the 1990s has shown a considerable comovement between national stock market indices; especially when global shocks affect markets [36,37,38]. As the US stock market is the most influential in the world [39,40], we expect the lagged log return of the S&P500 to be an appropriate predictor for the performance of the national stock market indices on the next trading day. Table 5 presents the regression results.

The results show a similar picture to the one found in the GMM regressions. In Model (1), where the rational expectation variable based on the exponential growth model is used as an independent variable, we find negative and statistically significant coefficients on the variables news attention and rational expectation. In line with the results of the GMM regressions, news attention has a greater influence compared to the rational investor expectation. In Model (2), where the rational expectation variable based on the SIR model is used as an independent variable, we only find a statistically significant coefficient on news attention. In both models, however, we do not find statistically significant coefficients on the lagged log return of the S&P500.

As further robustness checks, we first use the keyword “coronavirus” to construct our news attention variable and estimate all GMM and OLS regressions once more. Second, we adjust the way we calculate our measure for news attention. Instead of using the search volume over the previous five trading days to calculate our news attention measure, we consider the average search volume over the entire sample period. The results do not change qualitatively compared to our previous findings.

5. Conclusions

Financial markets have been on an unprecedented decline during the COVID-19 crisis, indicating wide implications for market participants and policy makers. In this paper, we have analyzed whether the current drop in financial markets is mainly driven by news attention or rational investor expectation.

By investigating a sample of 64 national stock markets, news attention has a significantly negative impact on financial markets. This effect is larger in magnitude compared to the impact of a rational investor’s expectation. This imposes significant economic costs. For instance, we estimate the economic cost for the US stock market resulting from the news hype to amount to USD 3.5 trillion until April 2020.

We contribute to the evolving body of research in several ways. We not only disentangle the potential drivers of the stock market reactions but also quantify the impact of news attention on financial markets. Our findings also imply investors should rather focus on news attention than on rational expectation when making their investment decisions during a crisis. Especially, professional investors should, apart from searching for safe-havens, adjust their investment strategy accordingly in order to minimize potential losses.

Finally, as with all research studies our paper has certain limitations. Since we investigate a rather small time window, we are only able to measure the short term effect of news attention and investors’ rational expectation on global stock markets during the COVID-19 crisis. Further, although we checked the robustness of our news attention measure, there might also be additional proxies which might capture news attention.

Author Contributions

Conceptualization, N.E., M.K., D.N. and P.P.; data curation, N.E., M.K. and D.N.; formal analysis, N.E., M.K. and D.N.; investigation, N.E., M.K. and D.N.; methodology, N.E., M.K., D.N. and P.P.; project administration, N.E. and P.P.; resources, N.E., M.K., D.N. and P.P.; software, N.E., M.K. and D.N.; supervision, P.P.; validation, N.E., M.K. and D.N.; visualization, N.E., M.K. and D.N.; writing—original draft, N.E., M.K. and D.N.; writing—review and editing, N.E., M.K., D.N. and P.P. All authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding.

Acknowledgments

The authors wish to thank the team of the center for Finance, Risk and Resource management of the Technical University of Dortmund for their technical and administrative support. Further, we acknowledge financial support by Deutsche Forschungsgemeinschaft and Technische Universität Dortmund/TU Dortmund Technical University within the funding programme Open Access Publishing.

Conflicts of Interest

The authors declare no conflict of interest.

Appendix A

{kind=link}

{kind=link}

Table A1.

This table shows the global stock market indices used in this study. ISO codes for each country are reported. For each country we select stock market indices which come from Trading Economics. Our sample covers 64 countries accounting for 94% of the world’s GDP and containing countries of each economic region: East Asia and Pacific (10), Europe and Central Asia (32), Latin America and Carribean (8), Middle East and North Africa (3), North America (2), South Asia (3) and Sub-Saharan Africa (6).

Table A1.

This table shows the global stock market indices used in this study. ISO codes for each country are reported. For each country we select stock market indices which come from Trading Economics. Our sample covers 64 countries accounting for 94% of the world’s GDP and containing countries of each economic region: East Asia and Pacific (10), Europe and Central Asia (32), Latin America and Carribean (8), Middle East and North Africa (3), North America (2), South Asia (3) and Sub-Saharan Africa (6).

| ID | ISO | Country | Market Index | ID | ISO | Country | Market Index |

|---|---|---|---|---|---|---|---|

| 1 | AUS | Australia | ASX200 | 33 | KEN | Kenya | NSE20 |

| 2 | AUT | Austria | ATX | 34 | KOR | South Korea | KOSPI |

| 3 | BEL | Belgium | BEL20 | 35 | LBN | Lebanon | BLOM |

| 4 | BGR | Bulgaria | SOFIX | 36 | LKA | Sri Lanka | CSE |

| 5 | BRA | Brazil | BOVESPA | 37 | LUX | Luxembourg | LUXX |

| 6 | BWA | Botswana | BSI DCI | 38 | LVA | Latvia | OMX Riga |

| 7 | CAN | Canada | TSX | 39 | MAR | Morocco | MASI |

| 8 | CHE | Switzerland | SMI | 40 | MEX | Mexico | IPC |

| 9 | CHL | Chile | IGPA | 41 | MUS | Mauritius | SEMDEX |

| 10 | CHN | China | SSE | 42 | MYS | Malaysia | FTSE KLCI |

| 11 | COL | Colombia | IGBC | 43 | NGA | Nigeria | NSE 30 |

| 12 | CYP | Cyprus | CSE | 44 | NLD | Netherlands | AEX |

| 13 | CZE | Czech Republic | SE PX | 45 | PAK | Pakistan | KSE100 |

| 14 | DEU | Germany | DAX | 46 | PER | Peru | PEN |

| 15 | DNK | Denmark | OMX20 | 47 | PHL | Philippines | PSEi |

| 16 | ECU | Ecuador | BVQA | 48 | POL | Poland | WIG |

| 17 | ESP | Spain | IBEX 35 | 49 | PRT | Portugal | PSI20 |

| 18 | EST | Estonia | OMX Tallinn | 50 | ROU | Romania | BET |

| 19 | FIN | Finland | HEX25 | 51 | RUS | Russia | MICEX |

| 20 | FRA | France | CAC 40 | 52 | SGP | Singapore | STI |

| 21 | GBR | United Kingdom | FTSE 100 | 53 | SRB | Serbia | BELEX15 |

| 22 | GHA | Ghana | GSE-CI | 54 | SVK | Slovakia | SAX |

| 23 | GRC | Greece | ASE | 55 | SVN | Slovenia | SBITOP |

| 24 | HRV | Croatia | CROBEX | 56 | SWE | Sweden | OMX30 |

| 25 | HUN | Hungary | BUX | 57 | THA | Thailand | SET50 |

| 26 | IDN | Indonesia | JCI | 58 | TUN | Tunisia | TUNINDEX |

| 27 | IND | India | SENSEX | 59 | TUR | Turkey | XU100 |

| 28 | IRL | Ireland | ISEQ | 60 | TWN | Taiwan | TWSE |

| 29 | ISL | Iceland | SE ICEX | 61 | USA | United States | DJIA |

| 30 | ITA | Italy | FTSE MIB | 62 | VEN | Venezuela | IBVC |

| 31 | JAM | Jamaica | Jamaica SE | 63 | VNM | Vietnam | VNINDEX |

| 32 | JPN | Japan | NIKKEI 225 | 64 | ZAF | South Africa | JALSH |

References

- Liu, H.; Manzoor, A.; Wang, C.; Zhang, L.; Manzoor, Z. The COVID-19 outbreak and affected countries stock markets response. Int. J. Environ. Res. Public Health 2020, 17, 2800. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Zhang, D.; Hu, M.; Ji, Q. Financial markets under the global pandemic of COVID-19. Financ. Res. Lett. 2020. [Google Scholar] [CrossRef]

- Sharif, A.; Aloui, C.; Yarovaya, L. COVID-19 pandemic, oil prices, stock market, geopolitical risk and policy uncertainty nexus in the US economy: Fresh evidence from the wavelet-based approach. Int. Rev. Financ. Anal. 2020. [Google Scholar] [CrossRef]

- Hethcote, H.W. Three Basic Epidemiological Models; Springer: Berlin/Heidelberg, Germany, 1989; pp. 119–144. [Google Scholar]

- De Silva, E.; Ferguson, N.M.; Fraser, C. Inferring pandemic growth rates from sequence data. J. R. Soc. Interface 2012, 9, 1797–1808. [Google Scholar] [CrossRef] [Green Version]

- De Grauwe, P. Lectures in Behavioral Macroeconomics; Princeton University Press: Princeton, NJ, USA, 2012. [Google Scholar]

- De Grauwe, P.; Gerba, E. The role of cognitive limitations and heterogeneous expectations for aggregate production and credit cycle. J. Econ. Dyn. Control 2018, 91, 206–236. [Google Scholar] [CrossRef]

- Da, Z.; Engelberg, J.; Gao, P. In Search of Attention. J. Financ. 2011, 66, 1461–1499. [Google Scholar] [CrossRef]

- Huang, L.; Liu, H. Rational inattention and portfolio selection. J. Financ. 2007, 62, 1999–2040. [Google Scholar] [CrossRef]

- Baumeister, R.F.; Bratslavsky, E.; Finkenauer, C.; Vohs, K.D. Bad Is Stronger Than Good. Rev. Gen. Psychol. 2001, 5, 323–370. [Google Scholar] [CrossRef]

- Cacioppo, J.T.; Gardner, W.L. Emotion. Annu. Rev. Psychol. 1999, 50, 191–214. [Google Scholar] [CrossRef]

- Rozin, P.; Royzman, E.B. Negativity Bias, Negativity Dominance, and Contagion. Personal. Soc. Psychol. Rev. 2001, 5, 296–320. [Google Scholar] [CrossRef]

- Carroll, C.D. Macroeconomic expectations of households and professional forecasters. Q. J. Econ. 2003, 118, 269–298. [Google Scholar] [CrossRef] [Green Version]

- Garz, M. Unemployment expectations, excessive pessimism, and news coverage. J. Econ. Psychol. 2013, 34, 156–168. [Google Scholar] [CrossRef]

- Baker, S.R.; Bloom, N.; Davis, S.J.; Terry, S.J. COVID-Induced Economic Uncertainty. 2020. Available online: https://www.nber.org/papers/w26983 (accessed on 18 June 2020).

- Ali, M.; Alam, N.; Rizvi, S.A.R. Coronavirus (COVID-19)—An epidemic or pandemic for financial markets. J. Behav. Exp. Financ. 2020, 27, 100341. [Google Scholar] [CrossRef] [PubMed]

- Zaremba, A.; Kizys, R.; Aharon, D.Y.; Demir, E. Infected Markets: Novel Coronavirus, Government Interventions, and Stock Return Volatility around the Globe. Financ. Res. Lett. 2020. [Google Scholar] [CrossRef]

- Al-Awadhi, A.M.; Alsaifi, K.; Al-Awadhi, A.; Alhammadi, S. Death and contagious infectious diseases: Impact of the COVID-19 virus on stock market returns. J. Behav. Exp. Financ. 2020, 27, 100326. [Google Scholar] [CrossRef] [PubMed]

- Ramelli, S.; Wagner, A.F. Feverish Stock Price Reactions to COVID-19. 2020. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3560319 (accessed on 18 June 2020).

- Boubaker, S.; Sensoy, A. Financial contagion during COVID–19 crisis. Financ. Res. Lett. 2020. [Google Scholar] [CrossRef]

- Corbet, S.; Hou, Y.; Hu, Y.; Lucey, B.; Oxley, L.; Chi Minh City, H. Aye Corona! The contagion effects of being named Corona during the COVID-19 pandemic. Financ. Res. Lett. 2020. [Google Scholar] [CrossRef]

- McGee, R.; Conlon, T. Safe Haven or Risky Hazard? Bitcoin during the Covid-19 Bear Market. Financ. Res. Lett. 2020. [Google Scholar] [CrossRef]

- Corbet, S.; Larkin, C.; Lucey, B.; Chi Minh City, H. The contagion effects of the COVID-19 pandemic: Evidence from Gold and Cryptocurrencies. Financ. Res. Lett. 2020. [Google Scholar] [CrossRef]

- Chen, W.; Yan, X. Searching for safe-haven assets during the COVID-19 pandemic. Int. Rev. Financ. Anal. 2020, 71, 101526. [Google Scholar]

- Mamaysky, H. Financial Markets and News about the Coronavirus. 2020. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3565597 (accessed on 18 June 2020).

- Ben-Rephael, A.; Da, Z.; Israelsen, R.D. It depends on where you search: Institutional investor attention and underreaction to news. Rev. Financ. Stud. 2017, 30, 3009–3047. [Google Scholar] [CrossRef]

- Plante, M. OPEC in the news. Energy Econ. 2019, 80, 163–172. [Google Scholar] [CrossRef]

- Anderson, R.M.; May, R.M. Infectious Diseases of Humans: Dynamics and Control; Oxford University Press: Oxford, UK, 1990. [Google Scholar]

- Kermack, W.; McKendrick, A. Contributions to the mathematical theory of epidemics. Bull. Math. Biol. 1991, 53, 33–55. [Google Scholar] [PubMed]

- Ma, J. Estimating epidemic exponential growth rate and basic reproduction number. Infect. Dis. Model. 2020, 5, 129–141. [Google Scholar] [CrossRef] [PubMed]

- McCabe, C.; Ostroff, C. Stocks Plunge 10% in Dow’s Worst Day Since 1987. The Wall Street Journal. 12 March 2020, p. 1. Available online: https://www.wsj.com/articles/global-stocks-follow-u-s-markets-lower-11583975524 (accessed on 18 June 2020).

- Cochrane, J.H. Asset Pricing; Princeton University Press: Princeton, NJ, USA, 2000. [Google Scholar]

- Grubb, D.; Symons, J. Bias in regressions with a lagged dependent variable. Econom. Theory 1987, 3, 371–386. [Google Scholar] [CrossRef]

- Hansen, L.P. Large Sample Properties of Generalized Method of Moments Estimators. Econometrica 1982, 50, 1029–1054. [Google Scholar] [CrossRef]

- Arellano, M.; Bond, S. Some Tests of Specification for Panel Data: Monte Carlo Evidence and an Application to Employment Equations. Rev. Econ. Stud. 1991, 58, 277. [Google Scholar] [CrossRef] [Green Version]

- Brooks, R.; Del Negro, M. The rise in comovement across national stock markets: Market integration or IT bubble? J. Empir. Financ. 2004, 11, 659–680. [Google Scholar] [CrossRef] [Green Version]

- Karolyi, G.A.; Stulz, R.M. Why do markets move together? An investigation of U.S.-Japan stock return comovements. J. Financ. 1996, 51, 951–986. [Google Scholar] [CrossRef]

- Longin, F.; Solnik, B. Is the correlation in international equity returns constant: 1960–1990? J. Int. Money Financ. 1995, 14, 3–26. [Google Scholar] [CrossRef]

- Eun, C.S.; Shim, S. International Transmission of Stock Market Movements. J. Financ. Quant. Anal. 1989, 24, 241–256. [Google Scholar] [CrossRef]

- Madaleno, M.; Pinho, C. International Stock Market Indices Comovements: A New Look. Int. J. Financ. Econ. 2012, 17, 89–102. [Google Scholar] [CrossRef]

Figure 1.

This figure shows the S&P500 stock market index and global confirmed COVID-19 cases for the period from 22 January 2020 to 9 April 2020. The figure is our own contribution based on stock market data from Trading Economics and COVID-19 infection data from Johns Hopkins University.

Figure 1.

This figure shows the S&P500 stock market index and global confirmed COVID-19 cases for the period from 22 January 2020 to 9 April 2020. The figure is our own contribution based on stock market data from Trading Economics and COVID-19 infection data from Johns Hopkins University.

Figure 2.

The effect of news attention and rational investor expectation on global stock markets. This figure provides expanding window regression results from the estimation of the model: , where i is the country and t denotes the trading day starting from 30 January 2020 to 9 April 2020 with a minimum window size of 10. We use the GMM estimator from Arellano and Bond [35]. The dependent variable is the log return of each stock market index . The control variable is the lagged log return of each stock market index . The expected exponential growth rate is our measure for rational expectation, while measures news attention for the keyword “corona” (based on ASVI). The variables are weighted by GDP and scaled to have a standard deviation of one. The instrument in the GMM estimation is . GMM coefficients are reported with a significance level of 5%. The figure is our own contribution based on stock market data from Trading Economics and COVID-19 infection data from Johns Hopkins University.

Figure 2.

The effect of news attention and rational investor expectation on global stock markets. This figure provides expanding window regression results from the estimation of the model: , where i is the country and t denotes the trading day starting from 30 January 2020 to 9 April 2020 with a minimum window size of 10. We use the GMM estimator from Arellano and Bond [35]. The dependent variable is the log return of each stock market index . The control variable is the lagged log return of each stock market index . The expected exponential growth rate is our measure for rational expectation, while measures news attention for the keyword “corona” (based on ASVI). The variables are weighted by GDP and scaled to have a standard deviation of one. The instrument in the GMM estimation is . GMM coefficients are reported with a significance level of 5%. The figure is our own contribution based on stock market data from Trading Economics and COVID-19 infection data from Johns Hopkins University.

Table 1.

The table reports descriptive statistics for the entire sample. The sample contains a total of 3366 observations. We observe 64 countries over a time period of 51 trading days starting from 30 January 2020 to 9 April 2020. The market return variable is defined by the log return series of each stock market index. For the rational investor’s expectation we use the changes of the exponential growth rates and as an alternative the changes of the susceptible–infectious–recovered (SIR) growth rates. We calculate our news attention variable as the abnormal Google search volume index (ASVI) for the keyword “corona”. The stock market data come from Trading Economics. COVID-19 data for the fitted growth rates come from Johns Hopkins University.

Table 1.

The table reports descriptive statistics for the entire sample. The sample contains a total of 3366 observations. We observe 64 countries over a time period of 51 trading days starting from 30 January 2020 to 9 April 2020. The market return variable is defined by the log return series of each stock market index. For the rational investor’s expectation we use the changes of the exponential growth rates and as an alternative the changes of the susceptible–infectious–recovered (SIR) growth rates. We calculate our news attention variable as the abnormal Google search volume index (ASVI) for the keyword “corona”. The stock market data come from Trading Economics. COVID-19 data for the fitted growth rates come from Johns Hopkins University.

| Observations | Minimum | Maximum | Mean | Median | Std. | |

|---|---|---|---|---|---|---|

| Market Return | 3366 | −0.1854 | 0.1554 | −0.004 | −0.0002 | 0.0294 |

| Exponential Growth Rate | 3366 | −1.3481 | 2.2777 | 0.0006 | −0.0022 | 0.1527 |

| SIR Growth Rate | 3366 | −1.7375 | 2.5254 | 0.0047 | 0 | 0.245 |

| News Attention | 3366 | −1.9459 | 3.4012 | 0.0469 | 0 | 0.4284 |

Table 2.

The effect of news attention and rational investor expectation on global stock markets. This table provides regression results from the estimation of the model: , where i is the country and t denotes the trading day starting from 30 January 2020 to 9 April 2020. We use the generalized method of moments (GMM) estimator from Arellano and Bond [35]. The dependent variable is the log return of each stock market index . The control variable is the lagged log return of each stock market index . The expected exponential growth rate is our measure for rational expectation in Model (1), while measures news attention for the keyword “corona” (based on ASVI). In Model (2) we use the expected SIR growth rate for rational expectation. The instrument in the GMM estimation is . The stock market data come from Trading Economics. COVID-19 data for the fitted growth rates come from Johns Hopkins University. Robust standard errors are reported in parentheses. ,, denote significance at the 10%, 5% and 1% level.

Table 2.

The effect of news attention and rational investor expectation on global stock markets. This table provides regression results from the estimation of the model: , where i is the country and t denotes the trading day starting from 30 January 2020 to 9 April 2020. We use the generalized method of moments (GMM) estimator from Arellano and Bond [35]. The dependent variable is the log return of each stock market index . The control variable is the lagged log return of each stock market index . The expected exponential growth rate is our measure for rational expectation in Model (1), while measures news attention for the keyword “corona” (based on ASVI). In Model (2) we use the expected SIR growth rate for rational expectation. The instrument in the GMM estimation is . The stock market data come from Trading Economics. COVID-19 data for the fitted growth rates come from Johns Hopkins University. Robust standard errors are reported in parentheses. ,, denote significance at the 10%, 5% and 1% level.

| Dependent Variable: Market Return | Model (1) | Model (2) |

|---|---|---|

| Lagged Market Return | −0.216 | −0.212 |

| (0.090) | (0.094) | |

| Expected Exponential Growth Rate | −0.131 | |

| (0.033) | ||

| Expected SIR Growth Rate | −0.019 | |

| (0.054) | ||

| News Attention | −0.279 | −0.293 |

| (0.017) | (0.016) | |

| Observations | 3264 | 3264 |

| Countries | 64 | 64 |

| Trading days | 51 | 51 |

| Estimation method | GMM | GMM |

| Robust Standard Errors | yes | yes |

| Country fixed effects | yes | yes |

| Time fixed effects | no | no |

Table 3.

Trading strategies of three different types of investors. This table shows mean returns of each investor’s portfolio covering 64 stock market indices for the period from 21 February 2020 through 9 April 2020. We assume no transaction costs and no short selling. The buy-and-hold investor buys a stock market index at the beginning and sells it at the end of the time period. The news attention investor as well as the rational expectation investor buys each stock market index at the beginning and uses buy and sell signals until the end of the time period. As trading signals, we primarily use the coefficients from the expanding window regressions in Figure 2. Both the news attention and the rational investor increase or decrease their portfolio by X% (according to the trading signal) at each point in time. For robustness purposes, we also use weighted coefficients and the change in coefficients as additional trading signals. We perform a two-sided t-test to test whether the portfolio mean returns of the strategies significantly differ from each other. Additionally, we perform a one-sided t-test to test whether the difference of the mean returns of the two strategies significantly differs from zero. ,, denote significance at the 10%, 5% and 1% level.

Table 3.

Trading strategies of three different types of investors. This table shows mean returns of each investor’s portfolio covering 64 stock market indices for the period from 21 February 2020 through 9 April 2020. We assume no transaction costs and no short selling. The buy-and-hold investor buys a stock market index at the beginning and sells it at the end of the time period. The news attention investor as well as the rational expectation investor buys each stock market index at the beginning and uses buy and sell signals until the end of the time period. As trading signals, we primarily use the coefficients from the expanding window regressions in Figure 2. Both the news attention and the rational investor increase or decrease their portfolio by X% (according to the trading signal) at each point in time. For robustness purposes, we also use weighted coefficients and the change in coefficients as additional trading signals. We perform a two-sided t-test to test whether the portfolio mean returns of the strategies significantly differ from each other. Additionally, we perform a one-sided t-test to test whether the difference of the mean returns of the two strategies significantly differs from zero. ,, denote significance at the 10%, 5% and 1% level.

| Trading Signal | |||

|---|---|---|---|

| Coefficient | Weighted | Coefficient | |

| Coefficient | Change | ||

| Panel A | |||

| Buy and hold portfolio | −0.2001 | −0.2001 | −0.2001 |

| News attention portfolio | −0.0255 | −0.0412 | −0.1492 |

| Difference | −0.1747 | −0.1590 | −0.0510 |

| Panel B | |||

| Buy and hold portfolio | −0.2001 | −0.2001 | −0.2001 |

| Rational investor portfolio | −0.0405 | −0.1049 | −0.1636 |

| Difference | −0.1597 | −0.0952 | −0.0366 |

| Panel C | |||

| Rational investor portfolio | −0.0405 | −0.1049 | −0.1636 |

| News attention portfolio | −0.0255 | −0.0412 | −0.1492 |

| Difference | −0.0150 | −0.0637 | −0.0144 |

Table 4.

Economic costs of news attention during the corona crisis. This table reports the results for the G8 countries. We perform one-day-ahead predictions per country for the period from 21 February 2020 through 9 April 2020 using the following models and our coefficients from the GMM estimation: Model (1) includes our coefficient for news attention (), while Model (2) excludes our coefficient for news attention (). We then cumulate the estimated returns and calculate the difference to separate the effect of trading based on news attention from trading based on rational expectation. We multiply this difference with the market capitalization of the respective stock market to estimate the economic costs per country. Market capitalization data come from Compustat Capital IQ.

Table 4.

Economic costs of news attention during the corona crisis. This table reports the results for the G8 countries. We perform one-day-ahead predictions per country for the period from 21 February 2020 through 9 April 2020 using the following models and our coefficients from the GMM estimation: Model (1) includes our coefficient for news attention (), while Model (2) excludes our coefficient for news attention (). We then cumulate the estimated returns and calculate the difference to separate the effect of trading based on news attention from trading based on rational expectation. We multiply this difference with the market capitalization of the respective stock market to estimate the economic costs per country. Market capitalization data come from Compustat Capital IQ.

| Country | Market Capitalization (in Million USD) | Economic Cost (in Million USD) | Economic Cost (in %) |

|---|---|---|---|

| Canada | 1,592,169 | −173,742 | −10.91 |

| France | 2,022,046 | −284,826 | −14.09 |

| Germany | 1,252,274 | −276,017 | −22.04 |

| Italy | 352,545 | −34,631 | −9.82 |

| Japan | 3,458,684 | −166,053 | −4.80 |

| Russia | 691,092 | −73,904 | −10.69 |

| United Kingdom | 3,182,449 | −419,499 | −13.18 |

| United States | 28,256,391 | −3,469,174 | −12.28 |

Table 5.

The effect of news attention and rational investor expectation on global stock markets. This table provides regression results from the estimation of the model: , where i is the country and t denotes the trading day starting from 30 January 2020 to 9 April 2020. The dependent variable is the log return of each stock market index . The control variable is the lagged log return of the S&P500 stock market index . The expected exponential growth rate is our measure for rational expectation in Model (1), while measures news attention for the keyword “corona” (based on ASVI). In Model (2) we use the expected SIR growth rate as our rational expectation variable. The stock market data come from Trading Economics. COVID-19 data for the fitted growth rates come from Johns Hopkins University. Robust standard errors are reported in parentheses. ,, denote significance at the 10%, 5% and 1% level.

Table 5.

The effect of news attention and rational investor expectation on global stock markets. This table provides regression results from the estimation of the model: , where i is the country and t denotes the trading day starting from 30 January 2020 to 9 April 2020. The dependent variable is the log return of each stock market index . The control variable is the lagged log return of the S&P500 stock market index . The expected exponential growth rate is our measure for rational expectation in Model (1), while measures news attention for the keyword “corona” (based on ASVI). In Model (2) we use the expected SIR growth rate as our rational expectation variable. The stock market data come from Trading Economics. COVID-19 data for the fitted growth rates come from Johns Hopkins University. Robust standard errors are reported in parentheses. ,, denote significance at the 10%, 5% and 1% level.

| Dependent Variable: Market Return | Model (1) | Model (2) |

|---|---|---|

| Lagged S&P500 Market Return | −0.006 | −0.006 |

| (0.045) | (0.044) | |

| Expected Exponential Growth Rate | −0.039 | |

| (0.019) | ||

| Expected SIR Growth Rate | −0.012 | |

| (0.012) | ||

| News Attention | −0.226 | −0.231 |

| (0.019) | (0.021) | |

| Observations | 3264 | 3264 |

| Countries | 64 | 64 |

| Trading days | 51 | 51 |

| Estimation method | OLS | OLS |

| Robust Standard Errors | yes | yes |

| Country/Time fixed effects | no | no |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Engelhardt, N.; Krause, M.; Neukirchen, D.; Posch, P. What Drives Stocks during the Corona-Crash? News Attention vs. Rational Expectation. Sustainability 2020, 12, 5014. https://0-doi-org.brum.beds.ac.uk/10.3390/su12125014

AMA Style

Engelhardt N, Krause M, Neukirchen D, Posch P. What Drives Stocks during the Corona-Crash? News Attention vs. Rational Expectation. Sustainability. 2020; 12(12):5014. https://0-doi-org.brum.beds.ac.uk/10.3390/su12125014

Chicago/Turabian StyleEngelhardt, Nils, Miguel Krause, Daniel Neukirchen, and Peter Posch. 2020. "What Drives Stocks during the Corona-Crash? News Attention vs. Rational Expectation" Sustainability 12, no. 12: 5014. https://0-doi-org.brum.beds.ac.uk/10.3390/su12125014

Note that from the first issue of 2016, this journal uses article numbers instead of page numbers. See further details here.