Factors Driving Success of Cost Management Practices in Integrated Project Delivery (IPD)

,

,  ,

,

Abstract

:1. Introduction

2. Contextual Background

2.1. Integrated Project Delivery (IPD)

2.2. Earned Value Management

2.3. Activity-Based Costing

2.4. D/5D BIM Automation

3. IPD Literature and Research Gap

4. Research Method

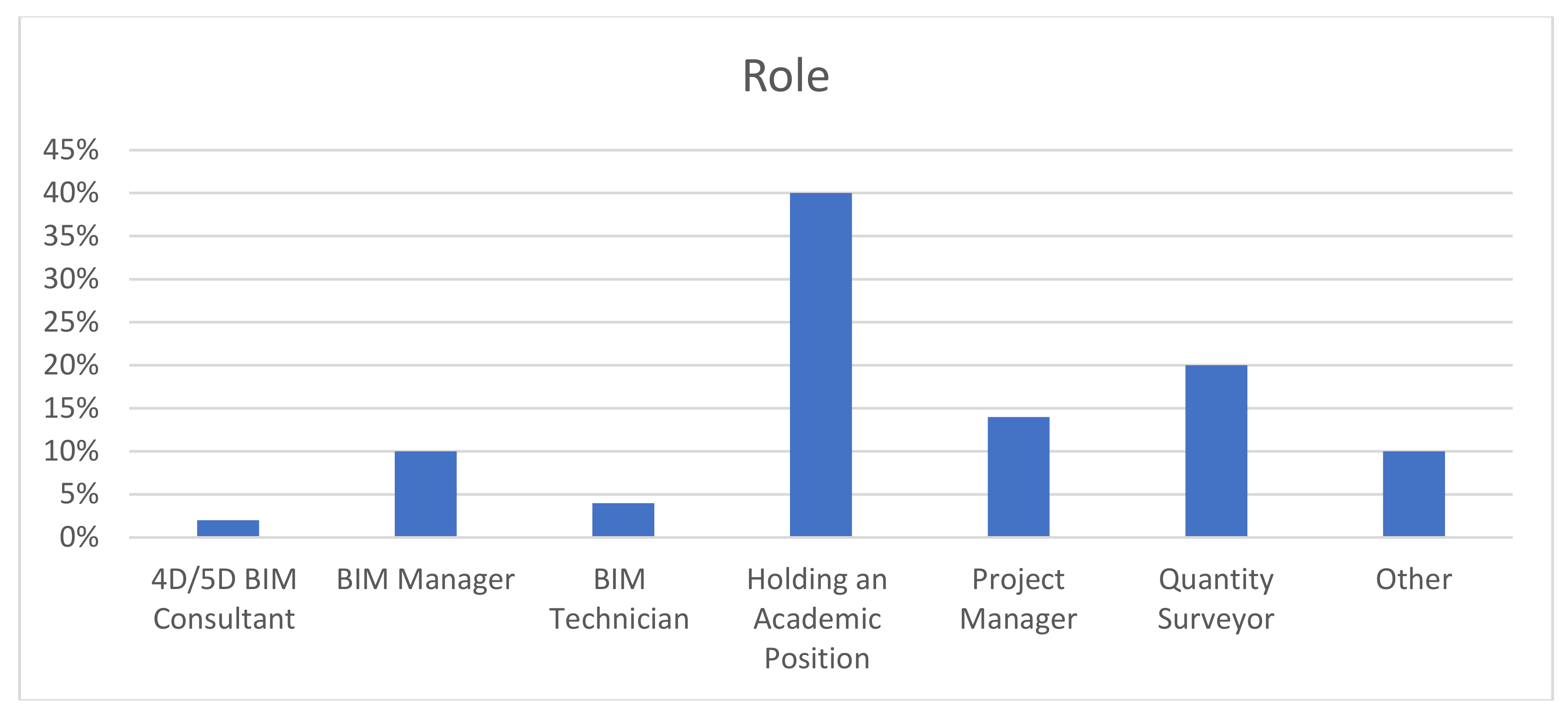

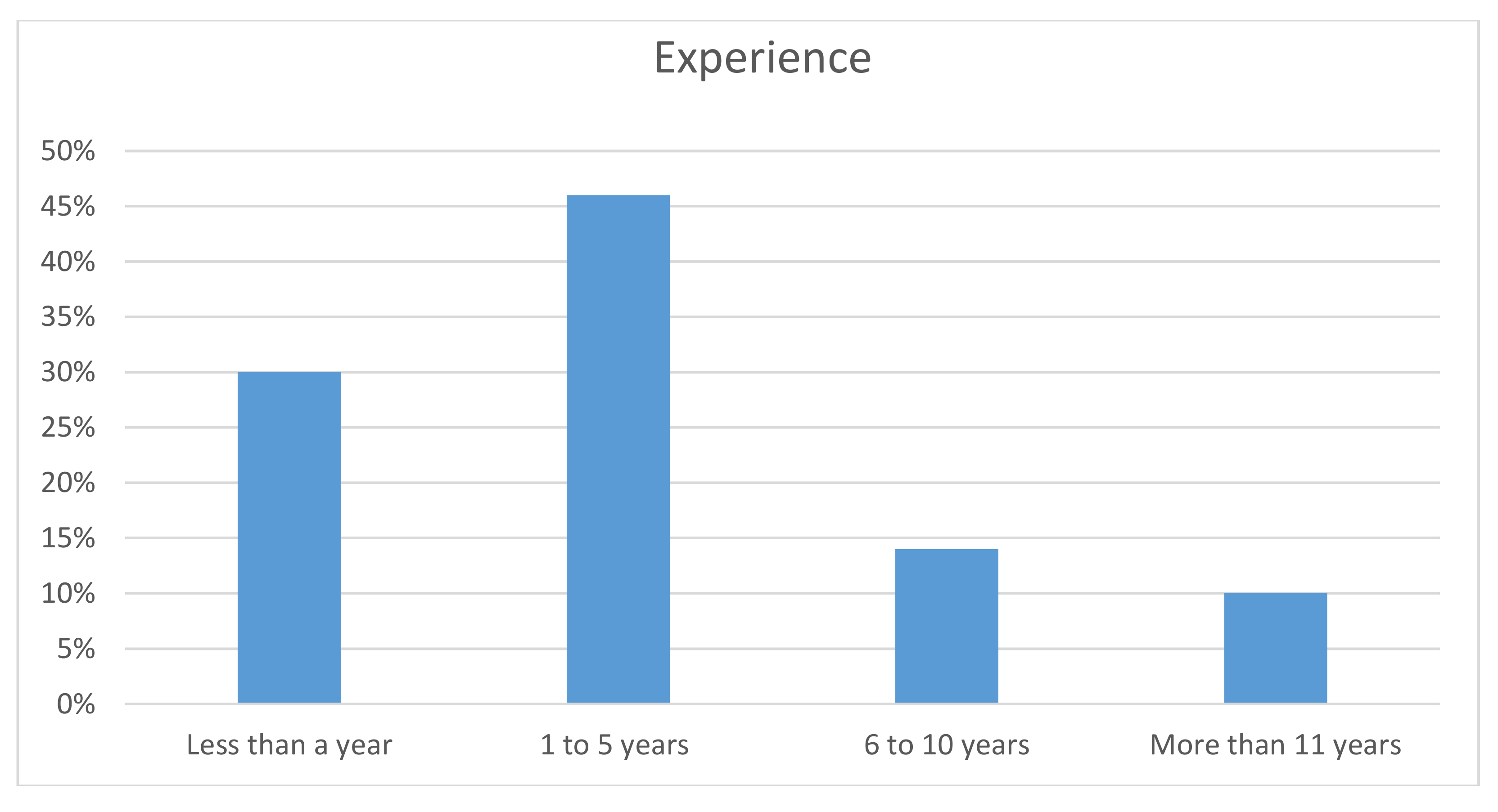

Participants’ Profiles

5. Antecedents of Success

5.1. Success Factors of IPD Process

5.2. Improving IPD Implementation

6. Discussion

7. Conclusions

Author Contributions

Funding

Conflicts of Interest

References

- Ashcraft, H.W. Integrated project delivery: A prescription for an ailing industry. Const. Law Int. 2014, 9, 21. [Google Scholar]

- Ahmad, I.; Azhar, N.; Chowdhury, A. Enhancement of IPD Characteristics as Impelled by Information and Communication Technology. J. Manag. Eng. 2019, 35, 04018055. [Google Scholar] [CrossRef]

- Asmar, M.E.; Hanna, A.S.; Loh, W.-Y. Evaluating Integrated Project Delivery Using the Project Quarterback Rating. J. Constr. Eng. Manag. 2016, 142, 04015046. [Google Scholar] [CrossRef]

- Manata, B.; Miller, V.; Mollaoglu, S.; Garcia, A.J. Measuring Key Communication Behaviors in Integrated Project Delivery Teams. J. Manag. Eng. 2018, 34, 06018001. [Google Scholar] [CrossRef]

- Pishdad-Bozorgi, P. Case Studies on the Role of Integrated Project Delivery (IPD) Approach on the Establishment and Promotion of Trust. Int. J. Constr. Educ. Res. 2017, 13, 102–124. [Google Scholar] [CrossRef]

- Hamzeh, F.; Rached, F.; Hraoui, Y.; Karam, A.J.; Malaeb, Z.; El Asmar, M.; Abbas, Y. Integrated project delivery as an enabler for collaboration: A Middle East perspective. Built. Environ. Proj. Asset Manag. 2019. [Google Scholar] [CrossRef]

- Ghassemi, R.; Becerik-Gerber, B. Transitioning to Integrated Project Delivery: Potential barriers and lessons learned. Lean Constr. J. 2011, 1, 32–52. [Google Scholar]

- Sun, W.; Mollaoglu, S.; Miller, V.; Manata, B. Communication Behaviors to Implement Innovations: How Do AEC Teams Communicate in IPD Projects? Proj. Manag. J. 2015, 46, 84–96. [Google Scholar] [CrossRef]

- Fischer, M.; Khanzode, A.; Reed, D.P.; Ashcraft, H.W., Jr. Integrating Project Delivery; John Wiley & Sons Inc.: Hoboken, NJ, USA, 2017; ISBN 978-0470587355. [Google Scholar]

- Durdyev, S.; Hosseini, M.R.; Martek, I.; Ismail, S.; Arashpour, M. Barriers to the use of integrated project delivery (IPD): A quantified model for Malaysia. Eng. Constr. Archit. Manag. 2019. [Google Scholar] [CrossRef]

- Kent, D.C.; Becerik-Gerber, B. Understanding construction industry experience and attitudes toward integrated project delivery. J. Constr. Eng. Manag. 2010, 136, 815–825. [Google Scholar] [CrossRef]

- Smith, R.E.; Mossman, A.; Emmitt, S. Editorial: Lean and integrated project delivery special issue. Lean Constr. J. 2011, 1–16. [Google Scholar] [CrossRef] [Green Version]

- Ma, Z.; Zhang, D.; Li, J. A dedicated collaboration platform for Integrated Project Delivery. Autom. Constr. 2018, 86, 199–209. [Google Scholar] [CrossRef]

- Liu, M.M.; Bates, A.J. Compensation Structure and Contingency Allocation in Integrated Project Delivery. In Proceedings of the 120th ASEE Annual Conference and Exposition, Atlanta, GA, USA, 18 June 2013. [Google Scholar]

- Zhang, L.; Li, F. Risk/reward compensation model for integrated project delivery. Eng. Econ. 2014, 25, 558–567. [Google Scholar] [CrossRef] [Green Version]

- Zhang, L.; Chen, W. The analysis of liability risk allocation for Integrated Project Delivery. In Proceedings of the 2nd International Conference on Information Science and Engineering, Hangzhou, China, 4–6 December 2010; pp. 3204–3207. [Google Scholar]

- Elghaish, F.; Abrishami, S.; Hosseini, M.R. Integrated project delivery with blockchain: An automated financial system. Autom. Constr. 2020, 114, 103182. [Google Scholar] [CrossRef]

- Allison, M.; Ashcraft, H.; Cheng, R.; Klawens, S.; Pease, J. Integrated Project Delivery: An Action Guide for Leaders. Available online: https://conservancy.umn.edu/handle/11299/201404 (accessed on 26 June 2020).

- Elghaish, F.; Abrishami, S.; Abu Samra, S.; Gaterell, M.; Hosseini, M.R.; Wise, R. Cash flow system development framework within integrated project delivery (IPD) using BIM tools. Int. J. Constr. Manag. 2019, 1–16. [Google Scholar] [CrossRef] [Green Version]

- Elghaish, F.; Abrishami, S.; Hosseini, M.R.; Abu-Samra, S.; Gaterell, M. Integrated project delivery with BIM: An automated EVM-based approach. Autom. Constr. 2019, 106, 102907. [Google Scholar] [CrossRef]

- Pishdad-Bozorgi, P.; Srivastava, D. Assessment of Integrated Project Delivery (IPD) Risk and Reward Sharing Strategies from the Standpoint of Collaboration: A Game Theory Approach. In Proceedings of the Construction Research Congress 2018, New Orleans, LA, USA, 18 September 2018. [Google Scholar]

- Roy, D.; Malsane, S.; Samanta, P.K. Identification of Critical Challenges for Adoption of Integrated Project Delivery. Lean Constr. J. 2018, 1, 1–15. [Google Scholar]

- Jones, B. Integrated project delivery (IPD) for maximizing design and construction considerations regarding sustainability. Procedia Eng. 2014, 95, 528–538. [Google Scholar] [CrossRef] [Green Version]

- Mesa, H.A.; Molenaar, K.R.; Alarcón, L.F. Exploring performance of the integrated project delivery process on complex building projects. Int. J. Proj. Manag. 2016, 34, 1089–1101. [Google Scholar] [CrossRef]

- Singleton, M.S. Implementing Integrated Project Delivery on Department of the Navy Construction Projects; Colorado State University: Fort Collins, CO, USA, 2010. [Google Scholar]

- Talebi, S.; Koskela, L.; Tzortzopoulos, P.; Kagioglou, M. Tolerance management in construction: A conceptual framework. Sustainability 2020, 12, 1039. [Google Scholar] [CrossRef] [Green Version]

- Talebi, S.; Koskela, L.; Tzortzopoulos, P.; Kagioglou, M.; Krulikowski, A. Deploying Geometric Dimensioning and Tolerancing in Construction. Buildings 2020, 10, 62. [Google Scholar] [CrossRef] [Green Version]

- Talebi, S.; Koskela, L.; Shelbourn, M.; Tzortzopoulos, P. Critical Review of Tolerance Management in Construction. In Proceedings of the International Group of Lean Construction, Boston, MA, USA, 20–22 July 2016. [Google Scholar]

- Talebi, S. Improvement of Dimensional Tolerance Management in Construction. Available online: http://eprints.hud.ac.uk/id/eprint/35070/ (accessed on 22 June 2020).

- Elghaish, F.; Abrishami, S.; Hosseini, M.R.; Abu-Samra, S. Revolutionising cost structure for integrated project delivery: A BIM-based solution. Eng. Constr. Archit. Manag. 2020. [Google Scholar] [CrossRef]

- AIA. Integrated Project Delivery: A Guide. Available online: https://www.aia.org/resources/64146-integrated-project-delivery-a-guide (accessed on 26 June 2020).

- PMI. A Guide to the Project Management Body of Knowledge (PMBOK® Guide), 5th ed.; Project Management Institute: Newtown Square, PA, USA, 2013; ISBN 8925598620. [Google Scholar]

- Pajares, J.; López-Paredes, A. An extension of the EVM analysis for project monitoring: The Cost Control Index and the Schedule Control Index. Int. J. Proj. Manag. 2011, 29, 615–621. [Google Scholar] [CrossRef]

- Khamooshi, H.; Abdi, A. Project duration forecasting using earned duration management with exponential smoothing techniques. J. Manag. Eng. 2016, 33, 04016032. [Google Scholar] [CrossRef] [Green Version]

- Naeni, L.M.; Shadrokh, S.; Salehipour, A. A fuzzy approach for the earned value management. Int. J. Proj. Manag. 2011, 29, 764–772. [Google Scholar] [CrossRef]

- Lipke, W.; Zwikael, O.; Henderson, K.; Anbari, F. Prediction of project outcome: The application of statistical methods to earned value management and earned schedule performance indexes. Int. J. Proj. Manag. 2009, 27, 400–407. [Google Scholar] [CrossRef]

- Chou, J.-S.; Chen, H.-M.; Hou, C.-C.; Lin, C.-W. Visualized EVM system for assessing project performance. Autom. Constr. 2010, 19, 596–607. [Google Scholar] [CrossRef]

- Kim, Y.-W.; Han, S.-H.; Yi, J.-S.; Chang, S. Supply chain cost model for prefabricated building material based on time-driven activity-based costing. Can. J. Civ. Eng. 2016, 43, 287–293. [Google Scholar] [CrossRef]

- Kim, Y.-W.; Ballard, G. Activity-Based Costing and Its Application to Lean Construction. In Proceedings of the 9th Annual Conference of the International Group for Lean Construction, National University of Singapore, Singapore, 16 August 2001. [Google Scholar]

- Wang, P.; Du, F.; Lei, D.; Lin, T.W. The choice of cost drivers in activity-based costing: Application at a Chinese oil well cementing company. Int. J. Manag. 2010, 27, 367. [Google Scholar]

- Tsai, W.H.; Hung, S.-J. A fuzzy goal programming approach for green supply chain optimisation under activity-based costing and performance evaluation with a value-chain structure. Int. J. Prod. Res. 2009, 47, 4991–5017. [Google Scholar] [CrossRef]

- Tsai, W.-H.; Yang, C.-H.; Chang, J.-C.; Lee, H.-L. An Activity-Based Costing decision model for life cycle assessment in green building projects. Eur. J. Oper. Res. 2014, 238, 607–619. [Google Scholar] [CrossRef]

- Omar, H.; Dulaimi, M. Using BIM to automate construction site activities. Build. Inf. Model. BIM Des. Constr. Oper. 2015, 149, 45. [Google Scholar] [CrossRef] [Green Version]

- Hartmann, T.; Gao, J.; Fischer, M. Areas of Application for 3D and 4D Models on Construction Projects. J. Constr. Eng. Manag. 2008, 134, 776–785. [Google Scholar] [CrossRef]

- Hamledari, H.; McCabe, B.; Davari, S.; Shahi, A. Automated schedule and progress updating of IFC-based 4D BIMs. J. Comput. Civ. Eng. 2017, 31, 04017012. [Google Scholar] [CrossRef]

- Wang, K.-C.; Wang, W.-C.; Wang, H.-H.; Hsu, P.-Y.; Wu, W.-H.; Kung, C.-J. Applying building information modeling to integrate schedule and cost for establishing construction progress curves. Autom. Constr. 2016, 72, 397–410. [Google Scholar] [CrossRef]

- Aibinu, A.; Venkatesh, S. Status of BIM adoption and the BIM experience of cost consultants in Australia. J. Prof. Issues Eng. Educ. Pract. 2013, 140, 04013021. [Google Scholar] [CrossRef]

- Lee, S.-K.; Kim, K.-R.; Yu, J.-H. BIM and ontology-based approach for building cost estimation. Autom. Constr. 2014, 41, 96–105. [Google Scholar] [CrossRef]

- El-Omari, S.; Moselhi, O. Integrating automated data acquisition technologies for progress reporting of construction projects. Autom. Constr. 2011, 20, 699–705. [Google Scholar] [CrossRef] [Green Version]

- Turkan, Y.; Bosche, F.; Haas, C.T.; Haas, R. Automated progress tracking using 4D schedule and 3D sensing technologies. Autom. Constr. 2012, 22, 414–421. [Google Scholar] [CrossRef]

- Turkan, Y.; Bosché, F.; Haas, C.T.; Haas, R. Toward automated earned value tracking using 3D imaging tools. J. Constr. Eng. Manag. 2013, 139, 423–433. [Google Scholar] [CrossRef] [Green Version]

- Eastman, C.; Teicholz, P.; Sacks, R.; Liston, K. BIM Handbook: A Guide to Building Information Modeling for Owners, Managers, Designers, Engineers and Contractors; Wiley: Hoboken, NJ, USA, 2011; ISBN 9781118021699. [Google Scholar]

- Hosseini, M.R.; Maghrebi, M.; Akbarnezhad, A.; Martek, I.; Arashpour, M. Analysis of Citation Networks in Building Information Modeling Research. J. Constr. Eng. Manag. 2018, 144, 04018064. [Google Scholar] [CrossRef]

- Kahvandi, Z.; Saghatforoush, E.; Ravasan, A.Z.; Mansouri, T. An FCM-Based Dynamic Modelling of Integrated Project Delivery Implementation Challenges in Construction Projects. Lean Constr. J. 2018, 87, 63–87. [Google Scholar]

- Tillmann, P.A.; Do, D.; Ballard, G. A Case Study on the Success Factors of Target Value Design. In Proceedings of the 25th Annual Conference of the International Group for Lean Construction, Heraklion, Greece, 9 July 2017; pp. 563–570. [Google Scholar]

- Alves, T.d.C.L.; Lichtig, W.; Rybkowski, Z.K. Implementing Target Value Design: Tools and Techniques to Manage the Process. Health Environ. Res. Des. J. 2017, 10, 18–29. [Google Scholar] [CrossRef] [PubMed]

- Ballard, G.; Dilsworth, B.; Do, D.; Low, W.; Mobley, J.; Phillips, P.; Reed, D.; Sargent, Z.; Tillmann, P.; Wood, N. How to Make Shared Risk and Reward Sustainable. In Proceedings of the 23rd Annual Conference of the International Group for Lean Construction, Perth, WA, Australia, 9 July 2015; pp. 257–266. [Google Scholar]

- Pishdad-Bozorgi, P.; Moghaddam, E.H.; Karasulu, Y. Advancing Target Price and Target Value Design Process in IPD Using BIM and Risk-Sharing Approaches. In Proceedings of the 49th ASC Annual International Conference California Polytechnic State University, San Luis Obispo, CA, USA, 20 April 2013. [Google Scholar]

- Ross, J. Introduction to Project Alliancing. In Proceedings of the Alliance Contracting Conference, Brisbane, QLD, Australia, 20 June 2003. [Google Scholar]

- Palinkas, L.A.; Horwitz, S.M.; Green, C.A.; Wisdom, J.P.; Duan, N.; Hoagwood, K. Purposeful sampling for qualitative data collection and analysis in mixed method implementation research. Adm. Policy Ment. Health Ment. Health Serv. Res. 2015, 42, 533–544. [Google Scholar] [CrossRef] [Green Version]

- Etikan, I.; Musa, S.A.; Alkassim, R.S. Comparison of convenience sampling and purposive sampling. Am. J. Theor. Appl. Stat. 2016, 5, 1–4. [Google Scholar] [CrossRef] [Green Version]

- Talebi, S. Exploring Advantages and Challenges of Adaptation and Implementation of BIM in Project Life Cycle. In Proceedings of the 2nd BIM International Conference on Challenges to Overcome, Lisbon, Portugal, 17–21 July 2014. [Google Scholar]

- Field, A. Discovering Statistics Using IBM SPSS Statistics; Sage: London, UK, 2013; ISBN 1446274586. [Google Scholar]

- Javali, S.B.; Gudaganavar, N.V.; Raj, S.M. Effect of Varying Sample Size in Estimation of Coefficients of Internal Consistency; Webmedcentral: Chennai, India, 2011. [Google Scholar]

- Rowlinson, S. Building information modelling, integrated project delivery and all that. Constr. Innov. 2017, 17, 45–49. [Google Scholar] [CrossRef]

- Kreuze, J.G.; Newell, G.E. ABC and life-cycle costing for environmental expenditures. Strateg. Financ. 1994, 75, 38. [Google Scholar]

- Kumar, N.; Mahto, D. Current trends of application of activity based costing (ABC): A review. Glob. J. Manag. Bus. Res. Account. Audit. 2013, 13, 1–16. [Google Scholar]

- Ashcraft, H.W. IPD Framework Hanson Bridgett LLP. Available online: https://www.hansonbridgett.com/Publications/~/media/Files/Publications/IPD_Framework.pdf (accessed on 26 June 2020).

- Assaf, S.A.; Bubshait, A.A.; Atiyah, S.; Al-Shahri, M. The management of construction company overhead costs. Int. J. Proj. Manag. 2001, 19, 295–303. [Google Scholar] [CrossRef]

- Succar, B. Building information modelling framework: A research and delivery foundation for industry stakeholders. Autom. Constr. 2009, 18, 357–375. [Google Scholar] [CrossRef]

- Azhar, S.; Khalfan, M.; Maqsood, T. Building information modelling (BIM): Now and beyond. Constr. Econ. Build. 2012, 12, 15–28. [Google Scholar] [CrossRef] [Green Version]

{kind=link}

{kind=link}

{kind=link}

| Authors | Contribution and Limitations |

|---|---|

| Elghaish, Abrishami, Hosseini and Abu-Samra [30] | Providing a new approach to develop a fair compensation structure of the IPD-based BIM and activity-based costing (ABC). |

| Elghaish, Abrishami, Abu Samra, Gaterell, Hosseini and Wise [19] | Developing a methodology to develop the project budget by estimating the minimum and maximum potential cash inflow to enable project parties to make the right decision before the construction stage commence. |

| Elghaish, Abrishami, Hosseini, Abu-Samra and Gaterell [20] | Providing a fair model to estimate the three main transactions in the IPD projects, which are reimbursed cost, profit and cost saving. |

| Kahvandi, et al. [54] | Exploring various key critical success factors, largely from a managerial perspective, with limited attention to cost estimation issues. |

| Pishdad-Bozorgi and Srivastava [21] | A model to share risks and rewards using a game theory approach, particularly for cases in which project cost exceed the profit-at-risk percentage. Their study only provided an overview of the model with future empirical research needed to assess its practicality and quantify its impacts. |

| Alves, et al. [55] | Presenting various techniques commonly used for TVD and applicable to the IPD context. |

| Tillmann, et al. [56] | Discussed the underlying mechanisms of cost estimation within IPD-oriented projects and exploring the factors that influence success. Despite the study’s contributions, it does not focus on the tactics of allocating overhead resources. |

| Ballard, et al. [57] | Recommended a set of procedures to enhance the chance of success in IPD cost estimation processes. Although the authors acknowledged that following TVD principles is a critical success factor, no explicit technique or procedure was recommended to make the recommendations useful in practical terms. |

| Zhang and Li [15] | Developed a risk-reward compensation mechanism by combining risk perception and the Nash bargaining solution (NBS) techniques. However, this model does not consider the method of sharing actual risk-reward amongst participants and overlooked the impact of IPD compensation structure in successful profit/cost-saving sharing. |

| Zhang and Li [15] | Combined risk perception and the Nash bargaining solution (NBS) techniques to formulate a risk-reward compensation model. However, the model was not sufficiently comprehensive to cover all possible types of engineering data, lacked empirical validity and, hence, required empirical studies. |

| Liu and Bates [14] | Articulated a probabilistic contingency calculation model to predict proper contingency to minimise cost overrun; nevertheless, a mechanism to share pain/gain percentages remain unexplored. |

| Pishdad-Bozorgi, et al. [58] | Discussed the potential of integration between TVD, BIM and IPD cost estimation. |

| Ross [59] | Proposed risk-reward sharing model as the risk-reward ratio is measured by the overall performance score (OPS), which is a scale between 0 and 100, where 0 to 50 represents the pain scope, and 50 to 100 represent the gain range. After computing the risk-reward ration using OPS, the project participants should share this ratio in correspondence with the contract. |

| Factors | Frequency | Percentage | Valid Percentage | Cumulative Percentage |

|---|---|---|---|---|

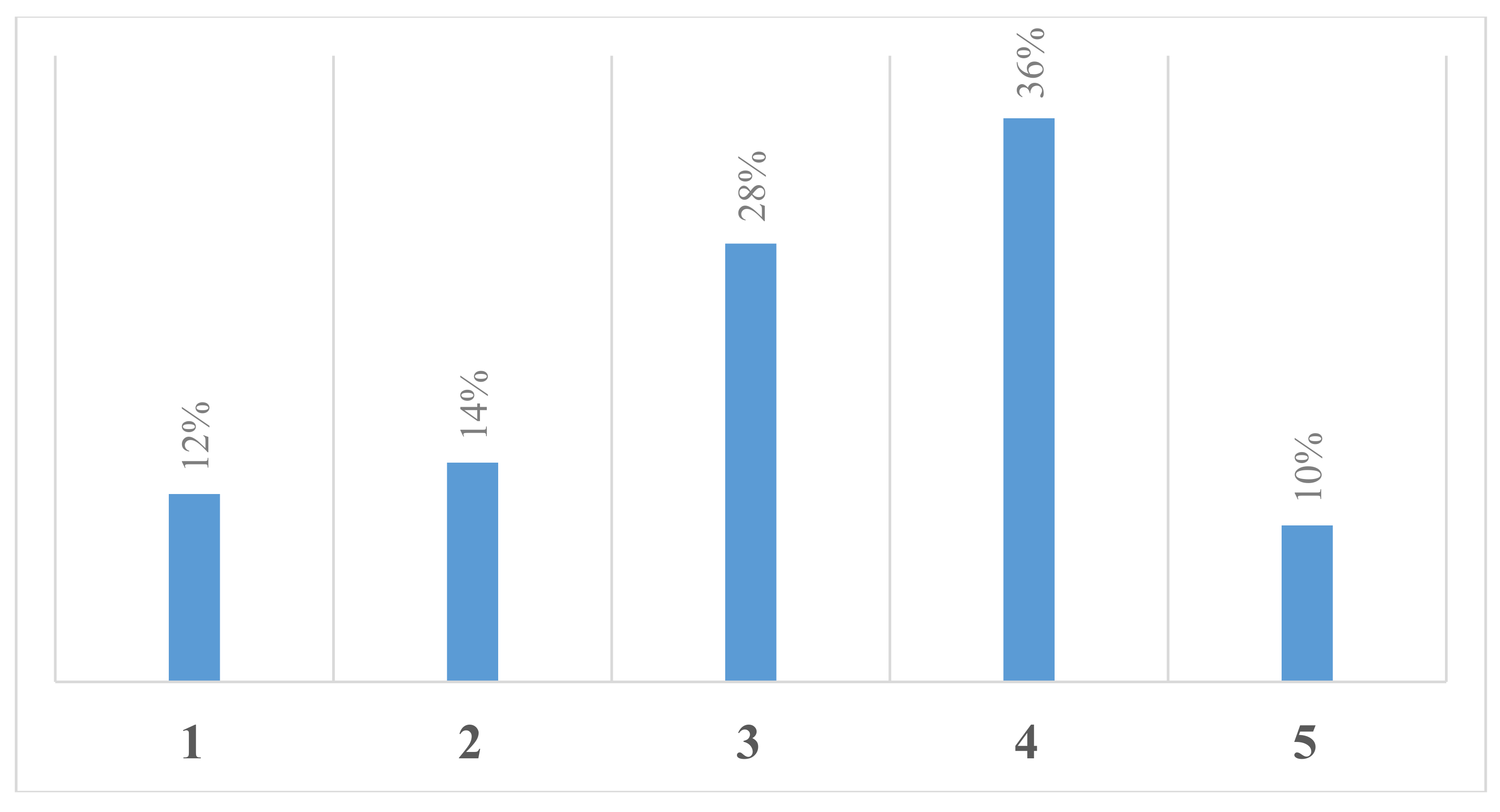

| There is no a tendering stage and using an open pricing technique. | 13 | 26.0 | 26.0 | 32.0 |

| The allocation of responsibilities and risks should be clear and understandable. | 9 | 18.0 | 18.0 | 50.0 |

| The compensation approach (Risk-rewards sharing) is flexible. | 10 | 20.0 | 20.0 | 70.0 |

| The early involvement of all participants | 15 | 30.0 | 30.0 | 100.0 |

| Other | 3 | 6.0 | 6.0 | 6.0 |

| Total | 50 | 100.0 | 100.0 |

| Factors | Category | Questions | Range | Minimum | Maximum | Mean | Std. Deviation |

|---|---|---|---|---|---|---|---|

| F1 | ABC and EVM Integration | Integrating EVM into IPD can easily facilitate its implementation regarding sharing risk-reward between owner/non-owner parties. | 4 | 1 | 5 | 3.36 | 0.964 |

| F2 | ABC and EVM Integration | Using an automated model to show the due payment for all parties based on their achievement against planned values. | 4 | 1 | 5 | 3.58 | 0.906 |

| F3 | Cost Estimation/Budgeting | Providing a separate cash flow for each participant including the proposed proportional cash in based on agreed profit-at-risk percentage. | 3 | 2 | 5 | 3.60 | 0.700 |

| F4 | Cost Estimation/Budgeting | Adopting ABC to develop a list of activities to enable getting reliable cash-out curve (S curve) by considering all costs (direct, indirect, and overhead). | 3 | 2 | 5 | 3.64 | 0.749 |

| F5 | Risk-reward sharing and ICT | Developing an EVM-based web report to enable tracking of the project by all participants as well as easy access from different devices. | 4 | 1 | 5 | 3.64 | 0.942 |

| F6 | Cost Estimation/Budgeting | Utilising ABC to identify the different sources of overhead cost clearly. | 4 | 1 | 5 | 3.68 | 0.935 |

| F7 | Risk-reward sharing and ICT | A fair allocation system with clear implementation models can enhance implementing IPD. | 4 | 1 | 5 | 3.72 | 0.927 |

| F8 | ABC and EVM Integration | Adapting EVM with ABC to identify risk-reward sharing fairly through developing mathematical models for all potential cases. | 4 | 1 | 5 | 3.82 | 0.896 |

| F9 | Risk-reward sharing and ICT | Providing an EVM grid to locate the cost performance ratio (CPR) and schedule performance ratio (SPR) to determine the holistic view of project progress. | 3 | 2 | 5 | 3.86 | 0.808 |

| F10 | General | Using a comprehensive process for cost management within the entire IPD stages to increase its implementation and minimise the waste of time and resources. | 4 | 1 | 5 | 3.98 | 0.820 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Elghaish, F.; Hosseini, M.R.; Talebi, S.; Abrishami, S.; Martek, I.; Kagioglou, M. Factors Driving Success of Cost Management Practices in Integrated Project Delivery (IPD). Sustainability 2020, 12, 9539. https://0-doi-org.brum.beds.ac.uk/10.3390/su12229539

Elghaish F, Hosseini MR, Talebi S, Abrishami S, Martek I, Kagioglou M. Factors Driving Success of Cost Management Practices in Integrated Project Delivery (IPD). Sustainability. 2020; 12(22):9539. https://0-doi-org.brum.beds.ac.uk/10.3390/su12229539

Chicago/Turabian StyleElghaish, Faris, M. Reza Hosseini, Saeed Talebi, Sepehr Abrishami, Igor Martek, and Michail Kagioglou. 2020. "Factors Driving Success of Cost Management Practices in Integrated Project Delivery (IPD)" Sustainability 12, no. 22: 9539. https://0-doi-org.brum.beds.ac.uk/10.3390/su12229539