Mandatory CSR Disclosure, CSR Assurance, and the Cost of Debt Capital: Evidence from Taiwan

1

Department of Accounting, Tamkang University, New Taipei City 251301, Taiwan

2

Securities and Futures Bureau, Financial Supervisory Commission, Taipei City 106237, Taiwan

*

Author to whom correspondence should be addressed.

Sustainability 2021, 13(4), 1768; https://0-doi-org.brum.beds.ac.uk/10.3390/su13041768

Submission received: 31 December 2020

/

Revised: 2 February 2021

/

Accepted: 3 February 2021

/

Published: 6 February 2021

(This article belongs to the Special Issue Corporate Social Responsibility (CSR) and CSR Reporting)

Abstract

:This study examined the impact of mandatory corporate social responsibility (CSR) disclosure, CSR assurance and the reputation of assurance providers (accounting firms) on the cost of debt capital. Our difference-in-difference research design in conjunction with univariate and multiple regression analysis was assessed using a large sample of firms listed on the Taiwan Stock Exchange and the Taipei Exchange. Our empirical results revealed that mandatory CSR assurance on CSR disclosure provided by accounting firms tended to reduce the cost of debt capital. However, contrary to expectations, the reputation of the accounting firm (Big 4 accounting firms vs. non-Big 4 accounting firms) tasked with providing CSR assurance did not have a significant effect on the cost of debt capital. These results have implications for firms seeking an assurance provider as well as for Big 4 accounting firms. These results also provide specific evidence relevant to government agencies seeking to update policies and extend the scope of mandatory CSR assurance to other environmentally sensitive industries.

1. Introduction

Over the past decade, countries around the world have paid close attention to the issue of corporate social responsibility (CSR). Investors in global capital markets are concerned about the disclosure of corporate social responsibility reports, and information related to CSR is an important issue driving investment decisions [1,2].

In response to global demand for CSR reporting and various food safety and environmental or pollution incidents in Taiwan, the Financial Supervisory Commission (FSC) of Taiwan announced in 2014 that CSR reporting would become mandatory for listed companies in the food-related industries, the chemical industry, and the finance sector (e.g., banking, insurance, and securities), as well as firms with paid-in capital exceeding NT$10 billion. Since 2015, these firms have had to abide by the “Rules Governing the Preparation and Filing of Corporate Social Responsibility Reports by Taiwan Stock Exchange (TWSE) and Taipei Exchange (TPEx) Listed Companies” in publishing annual CSR reports by referring to the Global Reporting Initiatives (GRI) Standards published by the GRI, Sector Disclosure, and other applicable rules according to its sector features.

According to statistics from the CSRone sustainability reporting platform, there has been a dramatic increase in the number of CSR reports published in recent years, with more than half of all listed companies obtaining CSR assurance services from third parties for their CSR reports in Taiwan. The use of a third party for assurance has been shown to enhance trust in the content of reports [2,3,4], in accordance with the reputation of the organization that prepared it. Investors who are confident in the verity of disclosed CSR-related information are more likely to regard the firm as a safe or worthy investment, and stakeholders can use this information to gain insights into the nonfinancial operations of the firm.

From the perspective of stakeholder theory, the primary objective in disclosing a CSR report is to strengthen communication between the company and its stakeholders, while providing investors and other stakeholders with a valuable reference by which to evaluate operational risks and performance [2,5,6]. Independent third parties providing assurance services can enhance transparency and credibility [2,3] by preventing “greenwashing” in the preparation of CSR reports [7,8,9]. Previous research has also demonstrated that having a CSR report assured by a third party can have a positive impact on the operations of a company. Moroney [10] reported that the quality of assured CSR reports (voluntary compliance) is significantly higher than that of reports without such assurances. Casey and Grenier [11] reported that investors view CSR reports as an indication of control over social and environmental risks. Most previous studies have focused on issues pertaining to voluntary CSR reporting or issues of voluntary assurance on CSR reporting. However, there are few studies that focused on mandatory CSR reporting and assurance. In the current study, we focused on mandatory CSR reporting and explored the association between mandatory CSR assurance and the cost of debt capital of firms.

One of our primary objectives in this study was to determine whether submitting CSR reports for mandatory assurance affects the cost of debt capital, which plays an important role in financing and operational decision-making. This study is based on the hypothesis that the disclosure of CSR-related information reduces information asymmetry between creditors and management, thereby reducing the risk faced by creditors allowing them to lower the required rate of returns. Our second objective in this study was to determine whether CSR assurances from Big 4 accounting firms carry more weight than do those from non-Big 4 accounting firms in terms of their effect on the cost of debt capital. This study also hypothesized that accounting professionals (and particularly those in the Big 4 accounting firms) are better qualified than their non-accounting or small counterparts to undertake assurance services, due to their skill set and stringent ethical standards emphasizing independence and objectivity. Under these conditions, it is reasonable to assume that assurances from Big 4 accounting firms would have a more pronounced effect than those from non-accounting firms and non-Big 4 firms on reducing the cost of debt capital

This study used the Taiwanese corporate environment as a framework to discuss the research questions outlined above. The environment of Taiwan provides a useful setting in which to examine the impact of CSR assurance on a firm’s performance such as cost of capital for several reasons. First, much of the previous research on voluntary CSR has had to contend with the issue of endogeneity [12], which makes it impossible to determine the causal relationship between independent and dependent variables. In the current corporate environment of Taiwan, food-related industries are subject to mandatory assurance, which eliminates much of the uncertainty and the risk of self-selection bias. By employing the difference-in-difference research design, which is according to the regulation of mandatory CSR setting, we can significantly alleviate the endogenous problem. Therefore, we expected that this would make it easier to discern relationships between research variables and their impact on research issues.

Second, there have been a number of major food safety incidents in Taiwan. The “fake oil incident” in 2014 prompted a major movement against unscrupulous food manufacturers. Note that, since 2007, the “Act Governing Food Safety and Sanitation” has undergone 14 amendments, many of which have focused on the need for credible CSR content and full disclosure. We believe that it should be possible to observe the effects of CSR assurance in enhancing the credibility of information disclosure by examining the changes that occurred following the adoption of regulations requiring mandatory CSR assurance in food-related industries.

Third, previous reports have pointed out that there is little demand to adopt CSR assurance practices in the USA [11], due to the previous establishment of strict regulatory measures as an alternative approach to enhancing the credibility of CSR disclosures. In addition, the stringent monitoring of highly leveraged companies by U.S. banks [11] enhances the credibility of disclosed information. Taiwan does not provide the same degree of legal protection for investors, and punishments for transgressions are poorly monitored [13]. Many companies that must abide by mandatory CSR reporting regulations must also publish CSR reports; however, the authenticity of the information in those reports is difficult to verify. If mandatory CSR assurance works the way it was intended, then it should have a significant impact on the cost of debt capital in Taiwan.

The remainder of this paper is organized as follows. In Section 2, we present a review of the literature on CSR disclosure, CSR assurance, and the cost of capital. We also develop our research hypotheses. In Section 3, we outline sample selection, data sources, variable definitions, and empirical modeling. Section 4 provides a summary of the empirical results and analysis. In Section 5, we discuss the results of our analyses and implications for research, practice and national policy. Section 6 presents conclusions, research limitations, and suggestions for future work.

2. Literature Review and Hypothesis Development

2.1. Background on Taiwan’s Mandatory CSR Disclosure and Assurance

As CSR is a growing global trend, Taiwan and its regulators have kept in line with international practices in promoting CSR. Competent authorities and related agencies have promoted CSR in the capital market system, market investment, and practical advancement of CSR in order to increase companies’ awareness of their social responsibilities and fully advance companies’ implementation of CSR. In terms of the capital market system, the Financial Supervisory Commission (FSC) continued to provide revisions on regulations for the disclosure of CSR information in 2008, and the Taiwan Stock Exchange (TWSE) and Taipei Exchange (TPEx) announced the “Corporate Social Responsibility Best Practice Principles for TWSE/TPEx Listed Companies” and “Ethical Corporate Management Best Practice Principles for TWSE/TPEx Listed Companies” in 2010 to guide listed companies in Taiwan in fulfilling their corporate social responsibilities and ethical corporate management, and thus step closer to sustainable development.

Following a number of serious food safety and environmental incidents, the FSC in Taiwan issued a decree, in September 2014, requiring that firms in food-related industries (companies in the food industry and companies whose food and beverage revenue accounts for 50% or more of their total revenue), as well as the finance sector, chemical industry, and firms with paid-in capital exceeding NT10 billion publish CSR reports since fiscal year 2015. On 26 November and 4 December of 2014, the TWSE and the TPEx respectively announced regulations requiring listed companies in food-related industries to publish CSR reports with assurance from a registered CPA of accounting firms since fiscal year 2015. There have been significant improvements in both quantity and quality of these reports.

According to statistics from the CSRone sustainability reporting platform, the number of companies in Taiwan providing CSR reports rose by 250% from 2014 to 2015. This was partly because it became mandatory for companies with over NT$10 billion in capital, as well as companies in the financial, chemical and food and beverages industry to publish reports (this includes retailers as long as 50% of a firm’s revenues are derived from food or beverages). In Taiwan, 77% of the top companies published CSR reports in 2015, which places Taiwan above the global average of 73% of top companies reporting. The number of Taiwanese CSR reports reached a record high of 528 in 2019 and more than half of all listed companies obtained CSR assurance services from third parties for their CSR reports.

Taiwan has received international recognition in CSR and sustainable development due to the competent authority’s active advancement. Taiwan ranked seventh among 25 important economies surveyed in Bloomberg’s ESG Disclosure Score in January 2018, and ranked first in the Asia Pacific and Japan region. Eighteen Taiwanese companies were included in the Dow Jones Sustainability Index (DJSI) in 2017, making Taiwan the highest-ranking emerging market in terms of weighted market value.

2.2. Literature Review

2.2.1. CSR Disclosure and CSR Assurance

The credibility of CSR disclosures is important to investors who rely on them to formulate investment decisions. One approach to enhancing the credibility of CSR disclosures is to have a third party assess them, and then provide assurance as to their verity [14]. The third party should be an independent reporting entity with sufficient knowledge and professional capabilities to evaluate CSR information. The assurance provider should also have undergone suitable training, be familiar with the assurance services, and have the ability to collect evidence. Finally, the third party should work actively to ensure quality control [15].

Cohen et al. [16] reported that retail investors clearly prefer to obtain CSR information through audited filings or from third parties, possibly reflecting a concern with the integrity and reliability of the nonfinancial disclosures. Cohen et al. [17] indicated that professional investors are increasingly seeking CSR information and have a strong preference for independent assurance of nonfinancial information. Mock et al. [18] described the growth of corporate information assurance in the financial service sector, noting that companies in the EU are likely to continue providing the strongest CSR assurance. After conducting interviews with the senior management of various Swedish companies, Park and Brorson [19] identified the need to improve the credibility of CSR reports as the main factor spurring companies to seek CSR assurance. Jones and Solomon [20] reported that managers use assurance as a tool to strengthen the credibility of CSR reports, with the aim of leaving a good impression on external stakeholders. Simnett et al. [21] reported that the demand for CSR assurance is particularly acute in mining, finance, and public utilities, based on widespread perceptions of social and environmental risk.

CSR assurance providers differ considerably in the scope, independence, and external standards [22,23,24]. Providing information related to the management of social and environmental risk allows companies to improve their reputation and makes it easier to obtain resources [25,26,27]. Empirical results have shown that CSR reports are value relevant [28], i.e., they provide benefits related to capital markets, such as reduced capital costs, increased analyst coverage, fewer analyst forecast errors, and fewer analysts forecast disagreements [29]. Strict management and supervision can be used as an alternative approach to increasing the credibility of CSR. A belief that CSR reports are subject to strict reviews by regulatory agencies increases the likelihood that users will rely on the overall credibility of CSR reports [30].

2.2.2. CSR Disclosure and the Cost of Capital

Most previous studies examining the association between disclosure and the cost of capital have focused on financial disclosure [31,32,33]. There appears to be consensus that the quality of financial disclosures is negatively correlated with the cost of capital [34]. Increasing the availability of CSR disclosures makes it easier for investors to comprehend the economic risks for investors and creditors [35], thereby enhancing their willingness to provide loans under agreeable conditions [36,37,38,39,40].

Diamond and Verrecchia [41] reported that disclosing information to reduce information asymmetry makes it easier for companies to attract investors and increase the liquidity of their stocks, thereby reducing the cost of capital. Botosan [42] reported that companies that are less affected by financial analysts are able to reduce the cost of capital by voluntarily disclosing more information. Increasing transparency can also reduce the cost of supervision by investors and, in so doing, reduce the rate of return required by investors [43]. Xu et al. [44] reported that firms required to issue CSR disclosure reports enjoyed a reduction in the cost of debt capital following implementation of the mandate.

In exploring the relationship between financial accounting information and corporate performance, Bushman and Smith [45] determined that accounting information plays a key role in governance by facilitating the management of company assets, informing investment decisions, and curbing opportunistic behavior by management. Under these conditions, many investors would be willing to relax the rate of returns they demand and in so doing reduce the cost of capital. Sloan [46] claimed that the disclosure of financial accounting information sheds light on corporate governance mechanisms and helps to reduce agency costs.

The cost of capital is associated with financial disclosures as well as nonfinancial disclosures, and numerous studies have demonstrated the value relevance of CSR information [47,48,49]. CSR can help companies avoid government supervision and in so doing reduce the cost of compliance. Emphasizing one’s commitment to CSR in marketing campaigns can also appeal to consumers who are cognizant of social issues, thereby boosting sales and financial performance [50,51]. It has also been shown that socially conscious investors are willing to pay a premium to support firms with a commitment to social responsibility [34].

2.3. Research Hypotheses

Frankel et al. [52] determined that many companies voluntarily make comprehensive disclosures based on the expectation that this will lower the cost of capital. This suggests that companies struggling with the cost of capital have a greater incentive to be more forthcoming with regard to disclosures. Other studies have linked voluntary disclosures to factors affecting the cost of capital. Healy et al. [53] reported that some companies expand their disclosure policy prior to public financing in order to reduce the cost of capital. Sengupta [54] also reported a negative relationship between the scope of voluntary disclosures and the cost of debt capital.

Previous studies have made it clear that the provision of CSR disclosures that are relevant, accurate, and reliable can enhance the confidence of many stakeholders in the verity of the claims [55]. Nonetheless, without some form of assurance, CSR reports appear to other stakeholders as unproven hyperbole of limited practical value [56,57]. Moroney [10] indicated that the quality of assured CSR reports is significantly higher than that of reports without such assurances. Adopting a worldwide sample, Ballou et al. [58] determined that voluntary assurance on CSR disclosure improves CSR quality. Likewise, Michelon et al. [59] demonstrated that voluntary assurance on sustainability disclosures is associated with increased likelihood of sustainability restatements. Clarkson et al. [60] reported a positive association between the extent and/or level of sustainability disclosures and the decision to obtain assurance. CSR assurance is meant to bolster the confidence of stakeholders in the authenticity of the reports provided by management [2,21].

Due to relative novelty of this topic, there has been relatively little research on the degree to which CSR assurance by external sources affects capital markets. It has been shown that providing assurance can have a positive impact on the credibility of reports from external sources [61], thereby increasing the awareness of report users [62]. Casey and Grenier [11] reported that compared with companies that do not provide CSR assurance, CSR assurance is associated with lower cost of capital and fewer forecast errors by analysts. Martínez-Ferrero and García-Sánchez [63] also found evidence of lower cost of capital for companies that publish and assure their CSR reports. Assurance alleviates uncertainty and ex-ante information and the monitoring and control cost of ex-post supervision [64] as financial statement audits [65,66], resulting in lower cost of capital for those companies audited by external auditors.

According to stakeholder theory, we can infer from a few previous studies [11,63] that the publication of CSR reports is a manifestation of information disclosure, and that creditors are important stakeholders. Creditors are primarily interested in long-term solvency (i.e., sustainably), and CSR reports are important tools by which to assess a company’s ability to maintain value and respond to risk. Nonetheless, creditors must be confident that all CSR claims are truthful and all disclosures comprehensive. This level of confidence can only be achieved by having a qualified third party thoroughly evaluate the claims before providing assurance as to their authenticity. Therefore, we posit the following hypothesis:

Hypothesis 1 (H1).

Mandatory CSR assurance as to the authenticity of CSR reports is negatively associated with the cost of debt capital.

Nearly fifty years ago, several Taiwanese accounting firms became affiliates or members of the U.S. Big international accounting. Long-term cooperation between U.S. and Taiwanese auditing industries has created a similar auditing market structure in both countries. For the international accounting firm affiliations, since 2003, Taiwanese four largest international accounting firms, i.e., the Big 4, has included PricewaterhouseCoopers, Ernst & Young, Deloitte, and KPMG.

Many accounting firms have expanded the scope of their services to include the assessment and assurance of CSR claims. In fact, the skills used by accountants in the auditing of financial statements are ideally suited to the provision of CSR assurance. Thus, the high standards and corresponding reputations of the four major accounting firms further strengthens the public confidence in their ability to provide reliable assurance services [21]. Furthermore, the four major accounting firms (PricewaterhouseCoopers, Ernst & Young, Deloitte, and KPMG) are better able than their smaller counterparts to navigate transnational networks across industries [21].

Huggins et al. [15] posited that the risk model used for the auditing of financial statements depends on understanding the company as a whole, and their ability to deal effectively with observed discrepancies. The reputation of the Big 4 accounting firms is based on their integrity, independence, professional skepticism, and expertise [67,68]. External auditors must abide by a code of ethical conduct when issuing CSR assurance; however, Moroney et al. [10] determined that very few non-accounting firms providing similar services address the issue of ethics on their websites. This suggests that accounting firms are more likely than non-accounting firms to provide reliable CSR assurance services [61,69].

The Big 4 accounting firms are heavily invested in maintaining their reputations of integrity, and they also enjoy the benefits afforded by economies of scale [70,71], which allows investments in the latest technological innovations. We expect that CSR reports with assurance from the Big 4 accounting firms have a more pronounced effect than do those from non-Big 4 firms in reducing the cost of debt capital. Therefore, we posit the following hypothesis:

Hypothesis 2 (H2).

The beneficial effects of mandatory assurance on the cost of debt capital are stronger when the assurance provider is a Big 4 accounting firm.

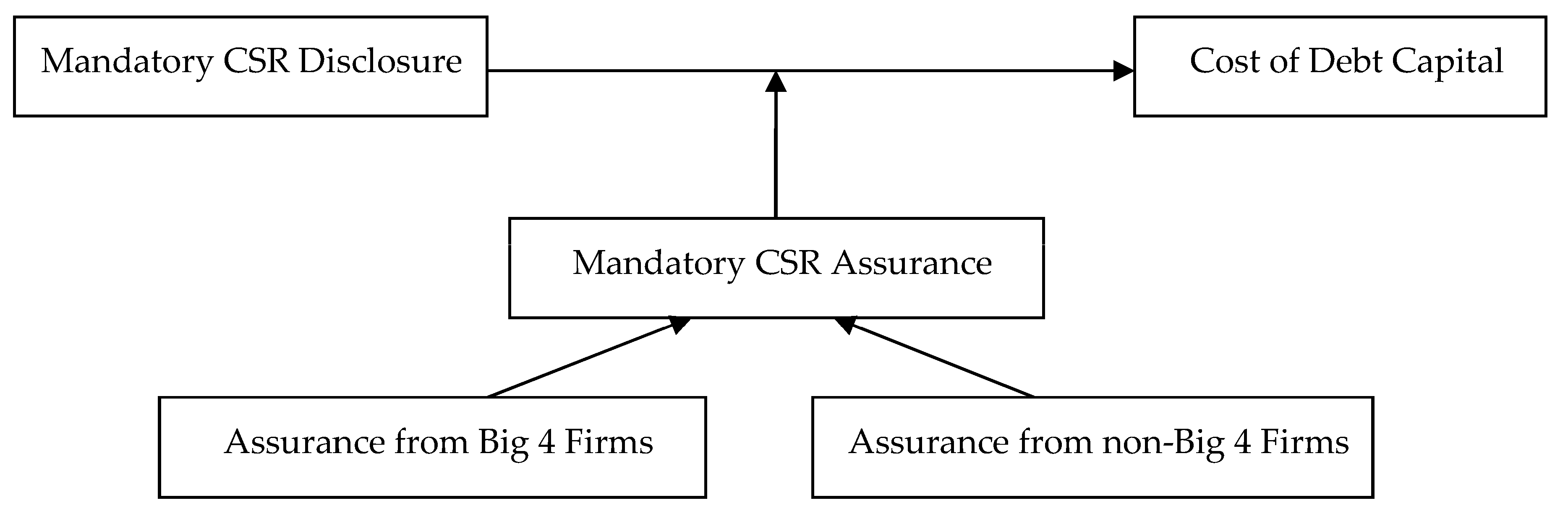

Figure 1 presents our research framework of the relationships between mandatory CSR disclosure and cost of debt capital and the impact of the mandatory CSR assurance on the cost of debt capital with assurance from Big 4 accounting firms or non-Big 4 accounting firms.

3. Research Methods

3.1. Data Sources and Sample Selection

This study focused on companies listed on the Taiwan Stock Exchange and the Taipei Exchange. As the regulations of mandatory CSR disclosure and CSR assurance has been in effect from 2015, and the number of CSR reports increased significantly since 2015, we consider 2010–2014 the pre-adoption period and 2015–2018 the post-adoption period. Thus, we only included the companies that published CSR reports between 2010 and 2018 in accordance with FSC regulations. These companies are listed in the “List of Listed Companies That Should File CSR Reports” and “Survey by the Taipei Exchange on Mandatory Requirement for Preparation of CSR Reports”, published by the FSC. All financial data and CSR-related information required for empirical analysis were collected from the database of the Taiwan Economics Journal (TEJ).

We adopted the difference-in-difference method for the assignment of samples to the experiment group and control group. The experiment group included listed companies in food-related industries (with mandatory assurance), whereas the control group included listed companies that were required to publish CSR reports (without mandatory assurance). The sample selection process is described as follows. We first collected data pertaining to listed companies that are subject to mandatory CSR disclosure during any year within the study period. Then, we excluded all firms that made voluntary disclosures or assurances. This was done to eliminate the problem of endogeneity. We also excluded firms in the finance sector, as well as firms for which data was missing. Preprocessing reduced the initial sample to 803 firm-year observations. The sample selection process is summarized in Table 1.

3.2. Variable Definitions

3.2.1. Dependent Variable: Cost of Debt Capital (COD)

We adopted the model proposed by Francis et al. [72] in our analysis of the association between CSR assurance and the cost of debt capital. Note that the cost of debt capital (COD) was measured by the ratio of interest expenses for a given year divided by the average total short-term and long-term debt. This estimate of the cost of debt capital is a historic pretax interest rate based on cumulative debt financing decisions of each firm in the sample [72].

3.2.2. Independent Variables

The independent variables were described as follows.

- Food-related industry (FR): For the main independent variable (FR), a value of 1 was assigned if it met the industry definition, and otherwise 0.

- Mandatory disclosure period (MDP): For mandatory disclosure period (MDP), a value of 1 was assigned if the company were subject to mandatory CSR disclosure after 2015 (the starting year of mandatory disclosure), and otherwise 0.

- Mandatory assurance (MA): For mandatory assurance (MA), a value of 1 was assigned in cases where CSR assurance was mandatory, and otherwise 0.

- Big 4 accounting firms (BIG4): For Big 4 accounting firms (BIG4), a value of 1 was assigned if CSR assurance was provided by a Big 4 accounting firm, and otherwise 0.

3.2.3. Control Variables

The control variables in the empirical model were derived from previous research [34,54,73,74] and described as follows.

- Company size (SIZE): First, we consider the company size (Size). Larger companies have relatively low credit risk, such that investors are more willing to lower the required rate of returns [73].

- Market-to-book ratio (MB): We also considered the market-to-book ratio (MB). Brav et al. [74] reported that the market-to-book ratio is negatively correlated with borrowing costs, and companies with a higher market-to-book ratio face lower borrowing costs.

- Systemic risk (BETA): Another issue was systemic risk (BETA). Sharfman and Fernando [34] reported that systemic risk is significantly positively correlated with the cost of debt capital. Investors tend to increase the required rate of returns as a way to bear systemic risk.

- Debt-to-equity ratio (DE): We further examined debt-to-equity ratio (DE). Creditors view a debt-to-equity ratio as an indication of long-term solvency, wherein a higher ratio indicates higher risk and corresponding higher cost of debt capital. Sengupta [54] reported that DE is positively correlated with the cost of debt capital.

- Times-interest-earned ratio (TIE): Another important issue is the times-interest-earned ratio (TIE), which is an indicator of a company’s ability to repay interest on borrowings, wherein a higher ratio indicates better solvency. Sengupta [54] reported that a higher TIE is negatively correlated with the cost of debt capital.

- Standard deviation of stock returns (STD): Finally, we considered the standard deviation of stock returns (STD). Sengupta [54] used this metric as a proxy for market risk. In the current study, STD was based on the standard deviation of daily stock returns for a given firm.

Descriptions of variables are detailed in Appendix A.

3.3. Research Model

To test H1, we established Model (1), pertaining to all companies for which CSR disclosure is mandatory, as follows:

CODi = β0 + β1FR + β2MDP + β3FR × MDP + β4SIZE + β5MB + β6BETA + β7DE + β8 TIE + β9 STD + ΣβαIND + εi

We expected that coefficient β3 of FR × MDP would be negative in support of H1, which would mean that the cost of debt capital in food-related firms (with mandatory CSR disclosure and assurance) would be lower than that of firms in other industries (with mandatory CSR disclosure but without mandatory assurance).

To enhance the robustness of our analysis, we established Model (2) to test H1, which pertains only to companies in food-related industries (with and without mandatory CSR assurance).

CODi = β0 + β1MA + β2SIZE + β3MB + β4BETA + β5DE + β6 TIE + β7 STD + εi

We expected that coefficient β1 of MA would be negative in support of H1, which would mean that the cost of debt capital in food-related firms (with mandatory CSR assurance) would be lower than that of other food-related firms (without mandatory CSR assurance).

Note that we also referred to previous research on the impact of CSR reports on cost of capital [34], and this incorporated industry-specific dummy variables (IND) into Model (1).

To test H2, we focused exclusively on CSR reports for which assurance was provided by a CPA using Model (3), as follows:

CODi = β0 + β1MA + β2BIG4 + β3MA × BIG4 + β4SIZE + β5MB + β6BETA + β7DE + β8 TIE + β9 STD + εi

We expected that coefficient β3 of MA × BIG4 would be negative in support of H2. Thus, if CSR assurance were provided by a Big 4 accounting firm, then the cost of debt capital should be lower than that of companies for which assurance was provided by a non-Big 4 accounting firm.

4. Results and Discussion

4.1. Descriptive Statistics

Panels A and B in Table 2 summarize the descriptive statistics of the respective variables for Model (1), Model (2), and Model (3). The average cost of debt capital (COD) under all samples was 2.488%. After deleting irrelevant observations (e.g., voluntary CSR disclosures and assurance), food-related firms accounted for approximately 27.4% of the instances of mandatory CSR disclosure. The mandatory disclosure period (MDP) values revealed that during the study period (2010 to 2018), the observations subject to mandatory CSR disclosure (with or without assurance) accounted for 19.9% of all samples. The average market-to-book (MB) ratio of 1.586 revealed that the average market value of shareholder equity exceeded the book value of shareholder equity, which is indicative of greater growth opportunity. The average debt-to-equity ratio (DE) of 1.437 revealed that the average end-of-period book value of long-term liabilities was greater than the market value of common equity. The average/median DE (1.437/0.148) and average/median TIE (1788.834/15.75) indicate a seriously right-skewed situation.

Panel B in Table 2 presents the descriptive statistics of firms in food-related industries. Post-2015 observations (with mandatory CSR reporting) accounted for 25.4% of the sample (MA). Note that 84.6% of the sample received CSR assurance from Big 4 accounting firms (BIG4).

Table 3 illustrates the univariate analysis of each variable divided into 2 × 2 separate groups of non-food-related firms (FR = 0) before and after mandatory CSR disclosure (MDP = 0 and MDP = 1), and food-related firms (FR = 1) before and after mandatory CSR disclosure (MDP = 0 and MDP = 1). Our results revealed that in non-food-related industries, the cost of debt capital (COD) was significantly higher before mandatory disclosure than after mandatory disclosure. In food-related industries, the COD was significantly higher before mandatory disclosure than after mandatory disclosure. Note that in food-related industries, the difference in the mean COD before and after mandatory disclosure was −0.954. In non-food-related industries, the difference in the mean COD before and after mandatory disclosure was −0.531. Clearly, the reduction in the cost of debt capital was more pronounced in food-related firms. This suggests that mandatory assurance can help to reduce the cost of debt capital.

4.2. Empirical Model and Regression Analysis

Table 4 lists the results of regression analysis. First, we tested H1 pertaining to a possible correlation between CSR reporting and the cost of debt capital. The results in Panels A and B of Table 4 revealed that FR × MDP (−0.519) and the coefficient of MA (−0.884) both reached the 10% level of significance. This result indicates that mandating the assurance of CSR reports tended to lower the cost of debt capital. This is consistent with the findings in previous studies [52,53,54]. Frankel et al. [52] determined that many companies voluntarily make disclosures based on the expectation that this will lower the cost of capital. Healy et al. [53] reported that some companies expand their disclosure policy prior to public financing in order to reduce the cost of capital. Sengupta [54] also reported a negative relationship between the scope of voluntary disclosures and the cost of debt capital. Nonetheless, most of these studies have focused exclusively on issues pertaining to voluntary CSR assurance.

Then, we tested H2 pertaining to a possible correlation between the reputation of the accounting firm (Big 4 vs. non-Big 4) and the cost of debt capital. The empirical results for Model (3) (Panel B in Table 4) did not reveal a significant difference between the cost of debt for companies that used Big 4 accounting firms and that of companies using non-Big 4 firms. Most of the companies that provided CSR assurance (84.6%) were working with Big 4 accounting firms; however, there is no evidence to support the assertion that Big 4 firms provided any advantage over their non-Big 4 counterparts in reducing the cost of debt capital. Thus, these results do not support H2.

As for control variables, the values of systemic risk (BETA) and stock return volatility (STD) in Panel A of Table 4 are significantly positively correlated with the cost of debt capital. This is consistent with the findings in previous studies [54,75]. This means that higher systemic risk or higher stock return volatility prompts lenders to increase the cost of debt. We adopted the variance inflation factor (VIF) to test the collinearity of each variable. The highest VIF value was 5.38, and the average VIF value was 1.8, indicating that collinearity was not an issue in this analysis.

4.3. Sensitivity Analysis: IFRS Adoption

In May 2009, the FSC announced that starting on 1 January 2013, all companies listed in Taiwan would be required to adopt IFRS protocols in the preparation of financial statements. This policy had a profound impact on the financial operations of thousands of companies, and numerous studies addressed the impact of IFRS adoption on the cost of capital. For example, Li [76] reported that the mandatory adoption of IFRS protocols would ensure uniformity in reporting and reduce the cost of capital. Thus, we conducted further analysis on the effects of CSR assurance for the period from 2013 to 2018 in order to verify that mandatory CSR reporting indeed had an impact on the cost of debt capital even under the new accounting rules.

Table 5 presents the results of regression analysis for the study period from 2013 to 2018. The empirical results for Models (1) and (2) in panels A and B of Table 5 revealed that the coefficient values of FR × MDP and MA (−0.945 and −1.712, respectively) reached the level of significance. These results support H1, indicating that mandatory CSR reporting can reduce the cost of debt capital. This is consistent with our main results.

The empirical results for Model (3) in panel B of Table 5 did not reach the level of significance. These results do not support H2, which indicates that the reputation of the accounting firm providing CSR assurance has no effect on the cost of debt capital. This is consistent with our main results and the findings reported by Li [76].

5. Discussion

5.1. Discussion of Results

On the basis of the tenets of stakeholder theory, we first sought to determine whether the reduction in cost of debt capital because of CSR reports is greater if these statements are assured by external and independent assurance providers from accounting firms. For this purpose, we assess the cost of capital change between those firms that have to assure their CSR reports and those that do not. Then, we sought to determine whether this possible greater decrease in cost of debt capital related to assurance varies depending on the size or reputation of accounting firms. More specifically, we assess whether the reduction is greater when the assurance provider is a big and well-known accounting firm termed as the Big 4. For this purpose, we assess if mandatory assurance by top tier accounting firms is associated with lower cost of capital than mandatory assurance provided by non-Big 4 accounting firms.

We found that mandating the disclosure of CSR information reduced cost of debt capital by decreasing investors’ uncertainty and information asymmetries. We also found that such effects were more pronounced in firms that seek assurance from external sources. However, there was no evidence to support to our hypothesis that the beneficial effects of mandatory assurance on the cost of debt capital are stronger when the assurance provider is a Big 4 accounting firm. That is, companies have the opportunity to decrease cost of debt capital to a greater extent by reporting social and environmental information with an assurance statement. Nevertheless, the decrease in cost of debt capital is not different from those reports independently assured by a Big 4 accounting firm.

This paper contributes to literature in several ways. First, this research extends the previous work on the consequences of CSR assurance. Although a large number of studies have investigated the economic consequences of corporate CSR disclosure, there is very little empirical evidence that demonstrates a link between the assurance of CSR disclosure and the cost of debt capital.

Second, previous studies have usually focused on the disclosure of the consequences of CSR in developed countries such as the USA or European countries [34]. In the current study, we examined the relationship between assurance on CSR disclosure and the results of companies in emerging countries such as Taiwan and introduced theories to explain Taiwan’s mandatory CSR assurance to enrich the literature. Debt financing is an important channel for listed companies to conduct external financing. Furthermore, the fact that CSR assurance is mandatory in Taiwanese regulatory environment means that the effect on the cost of debt capital may be more pronounced than in countries with a more lenient regulatory system.

Third, there is a potential causal relationship between CSR disclosure and the cost of capital. Taiwan is one of the few countries that enforces CSR disclosures for listed companies (the food-related industries, the chemical industry, and the finance sector, as well as firms with paid-in capital exceeding a certain amount) and has mandated CSR assurance for the food-related industries (companies in the food industry and companies whose food and beverage revenue accounts for 50% or more of their total revenue). Only by studying mandatory disclosures and mandatory assurance can causality reverse through voluntary disclosures and assurance be avoided. Our research design using the difference-in-difference method largely alleviated the problem of endogeneity, thereby ensuring that any observed effects on the cost of debt capital are attributable to CSR assurance.

5.2. Implications for Research

In recent years, conflicting results have called into question the sign and even the existence of an association between CSR disclosure and cost of capital [12]. A number of studies have posited endogeneity bias as a potential explanation for the inconsistencies in empirical findings and an apparent contradiction between observed phenomena and the underlying theory [31,32,77]. In the current corporate environment of Taiwan, the fact that food-related industries are subject to mandatory assurance eliminated much of the uncertainty and the risk of endogeneity bias.

The primary objective in disclosing a CSR report is to strengthen communication between the company and its stakeholders. Previous research has also demonstrated that disclosing a CSR report or having it verified by a third party can have a positive impact on operations [10,11,52,54,58,59,60]. Nonetheless, most previous studies have focused exclusively on issues pertaining to voluntary CSR assurance [52,53,54].

The findings from the results of our study support the observations in previous research. First, increasing the availability of CSR information was shown to reduce information asymmetry, unfavorable selection costs, and overall risks [29,32,34,51,78,79]. Second, CSR assurance by external sources was shown to strengthen the effect on the reduction of the cost of capital [11,63], since it has a positive impact on the credibility of external assurance reports [61]. Third, we determined that the market is largely oblivious to whether assurance services are provided by Big 4 accounting firms, although stakeholders recognize their skills and abilities in professional financial auditing [62,80,81].

5.3. Implications for Theory and Practice

Our study results present a number of implications for theory and practice. According to stakeholder theory, in addition to being responsible to investors, companies should also take into account the interests of the stakeholders [82]. Our results support previous assertions that the disclosure of the CSR report is regarded as a means of communing with stakeholders [83]. However, from the perspective of stakeholders, third-party assurance represents its achievements and efforts in CSR reports [84]. Furthermore, according to signaling theory, assurance is believed to be a signal of information. It establishes legitimacy with external stakeholders and affect corporate reputation [26]. Our results also have implications for firms seeking an assurance provider as well as for Big-4 accounting firms. Previous research has shown that obtaining independent assurance of CSR reporting has capital market benefits [2,5] and that these benefits are amplified when accountants provide the assurance [58,59,60]. The results of this research suggest that firms need not deal with the added financial burden of engaging Big-4 accounting firms in seeking CSR assurance based on the cost-effective considerations. It may be advisable for Big-4 accounting firms to provide added value in the provision of assurance services, rather than simply meeting baseline government regulations.

5.4. Implications for National Policy

Legitimacy theory is also adopted in this study as part of the theoretical framework. The theory of legitimacy posits that companies can use third-party assurance to justify their social activities and to use them as a strategic tool to influence the public’s perception of corporate behavior [1,85]. Because the legitimacy theory emphasizes that corporate organization consider the rights of investors and also the rights of the general public [86]. According to stakeholder and legitimacy theories, this study provides important information to regulatory bodies or government agencies working to update policies.

From an international perspective, we must be informed of the fact that CSR disclosure is voluntary, and that the assurance market is still an unregulated market in many countries [58,59]. In most previous CSR literature, the principle of voluntarism is predominant and implies that CSR activities are discretionary [58,59,60,87,88]. Nevertheless, a growing number of governments are enacting CSR-related laws and regulations (e.g., Denmark, France, Philippines, Spain, Argentina, Brazil, India, Norway, Taiwan, and the European Union). Even the EU has changed the definition of CSR to include a mandatory dimension, introducing the importance of policy measures and regulations to prevent unfair CSR disclosure and greenwashing behaviors [89]. Our research demonstrated that governments have a significant interest in CSR and exercise influence on firms’ CSR activities.

Previous research has presented theoretical and empirical evidence supporting a competitive advantage of using accounting firms as assurance providers [58,59,60]. The governments and regulatory bodies can help the financial market to be efficient by promoting the quality of CSR disclosure and CSR assurance. Our results suggest that regulatory bodies or policymakers can plan to expand the scope of mandatory CSR assurance provided by accounting firms to other environmentally sensitive firms, industries or sectors, lower the threshold of paid-in capital of firms regarding mandatory CSR assurance, and strengthen supervision in order to bolster the confidence of investors. Moreover, Gatti et al. [89] proposed that greenwashing could be better prevented with a combination of voluntary and mandatory aspects. Thus, we also suggest that policymakers consider making stricter CSR assurance standards to decrease greenwashing and information overload.

6. Conclusions

In September 2014, the Taiwanese government has made it compulsory for all TWSE/TPEx-listed companies with capital over NT$10 billion and specifically chemical, food, and finance companies to prepare an annual CSR report from the fiscal year 2015 onwards. Immediately, the TWSE and the TPEx in November and December 2014, respectively, announced regulations requiring listed companies in food-related industries (firms in the food industry and firms whose food and beverage revenue accounts for 50% or more of their total revenue) to publish CSR reports with assurance from a registered CPA of accounting firms. This regulatory situation is ideally suited to analyzing the association between CSR assurance and firm performance (i.e., cost of capital). This regulatory climate also makes it possible to focus on firms that are required to publish a CSR report and explore the impact of mandatory CSR assurance on the cost of debt capital.

The environment of Taiwan provides a useful setting to employ a difference-in-difference research design for assessing the degree to which these regulations affected the cost of debt capital. Our empirical results from Model (1) and Model (2) both revealed that mandating the assurance of CSR reports tended to lower the cost of debt capital.

Contrary to expectations, however, we determined that the reputation of the accounting firm (Big 4 vs. non-Big 4) tasked with the provision of CSR assurance did not have a significant effect on the cost of debt capital. Our findings are consistent with previous research [52,53,54,90] and support theoretical predictions, which suggested a negative association between CSR disclosure and the cost of capital. Furthermore, the result from Model (3) provides additional evidence that the assurance services provided by Big 4 accounting firms do not differ significantly from those provided by non-Big 4 accounting firms for reducing the cost of debt capital. These results have implications for firms seeking an assurance provider as well as for Big-4 accounting firms. It may be advisable to provide added value in the provision of assurance services, rather than simply meeting baseline government regulations.

Most previous studies on external assurance for CSR reports have been conducted in the context of the USA or Europe. In this study, we extended this research to firms in emerging markets. Nevertheless, this paper has a number of limitations to be addressed in future research on this topic. Thus, the above inferences should be taken with the following caveats.

First, the main limitation of this study is the fact that mandatory CSR disclosure has been in effect for a relatively short period of time, thereby making it impossible to observe these effects in a large number of firms over the long term. Future studies could enhance this relevant issue by taking a longer data period or utilizing a fixed- (or random-) effect panel model to estimate the results.

Second, the quality of the content disclosed in CSR reports varied considerably. Stipulating that firms have CSR reports assessed by CPAs increases operating costs; however, it can also provide a number of benefits. Thus, in the future, researchers may employ a case study approach to obtain a more comprehensive understanding of firms’ decisions related to CSR reports and obtaining assurance from external sources.

Third, according to the regulatory setting in Taiwan, CSR disclosure and CSR assurance for food-related firms and other specific industries in our sample are all mandatory. Hence, we did not include board or ownership structure variables as the control variable in our model. In the future, researchers could include those control variables to examine the effect of CSR disclosure and CSR assurance on the cost of debt capital.

Finally, in the current study, we focused exclusively on the cost of debt capital. In the future, researchers could assess whether mandatory CSR compliance provides other benefits for firms, investors, or the government.

Author Contributions

Conceptualization, L.K. and P.-W.K.; methodology, P.-W.K. and C.-C.C.; software, L.K. and C.-C.C.; validation, L.K., P.-W.K., and C.-C.C.; formal analysis, C.-C.C.; resources, L.K. and P.-W.K.; data curation, L.K. and C.-C.C.; writing—original draft preparation, C.-C.C.; writing—review and editing, L.K. and P.-W.K.; visualization, P.-W.K. All authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

Not applicable.

Acknowledgments

We thank anonymous reviewers and the editors for their very helpful recommendations.

Conflicts of Interest

The authors declare no conflict of interest.

Appendix A

| Variables | Definition |

| COD | The cost of debt capital of the firm. The ratio of interest expenses for a given year divided by the average total short-term and long-term debt. |

| FR | A dummy variable equals to 1 if the firm met the industry definition (firms in the food industry and firms whose food and beverage revenue accounts for 50% or more of their total revenue), and otherwise 0. |

| MDP | A dummy variable equals to 1 if the firm were subject to mandatory CSR disclosure after 2015, and otherwise 0. |

| MA | A dummy variable equals to 1 if CSR assurance of the firm was mandatory, and otherwise 0. |

| BIG4 | A dummy variable equals to 1 if CSR assurance of the firm was provided by a Big 4 accounting firm, and otherwise 0. |

| SIZE | Firm size is measured as the natural logarithm of total assets of the firm. |

| MB | The market-to-book ratio is measured as market capitalization divided by the book value of the firm. |

| BETA | The annual systemic risk of the firm is measured as a stock’s risk reflected by measuring the fluctuation of its price changes relative to the overall market in the CAPM formula. |

| DE | The debt-to-equity ratio is measured as total debt divided by total equity of the firm. |

| TIE | The times-interest-earned ratio is measured as the sum of income before extraordinary items and interest expense divided by the interest expense of the firm. |

| STD | The standard deviation of daily stock returns of the firm. |

References

- Cohen, J.R.; Simnett, R. CSR and Assurance Services: A Research Agenda. Audit. J. Pract. Theory 2015, 34, 59–74. [Google Scholar] [CrossRef]

- Zhang, W.J.; Kuo, H.C. The relationship of corporate social responsibility reports’ reason for issuance, assurance, and assurance type to stock price reaction. J. Valuat. 2019, 13, 17–58. [Google Scholar]

- Wallace, W.A. The economic role of the audit in free and regulated markets: A look back and a look forward. Res. Account. Regul. 2010, 17, 267–298. [Google Scholar] [CrossRef]

- Chiu, A.-A.; Chen, L.-N.; Hu, J.-C. A Study of the Relationship between Corporate Social Responsibility Report and the Stock Market. Sustainability 2020, 12, 9200. [Google Scholar] [CrossRef]

- Kim, J.; Cho, K.; Park, C.K. Does CSR Assurance affect the relationship between CSR performance and fnancial performance? Sustainability 2019, 11, 5682. [Google Scholar] [CrossRef] [Green Version]

- Cho, S.J.; Chung, C.Y.; Young, J. Study on the Relationship between CSR and Financial Performance. Sustainability 2019, 11, 343. [Google Scholar] [CrossRef] [Green Version]

- Hopwood, A.G. Accounting and the environment. Account. Organ. Soc. 2009, 34, 433–439. [Google Scholar] [CrossRef]

- Gray, R. Is accounting for sustainability actually accounting for sustainability…and how would we know? An exploration of narratives of organisations and the planet. Account. Organ. Soc. 2010, 35, 47–62. [Google Scholar] [CrossRef]

- Lyon, T.P.; Maxwell, J.W. Greenwash: Corporate environmental disclosure under threat of audit. J. Econ. Manag. Strategy 2011, 20, 3–41. [Google Scholar] [CrossRef]

- Moroney, R.; Windsor, C.; Aw, Y.T. Evidence of assurance enhancing the quality of voluntary environmental disclosures: An empirical analysis. Account. Financ. 2012, 52, 903–939. [Google Scholar] [CrossRef]

- Casey, R.J.; Grenier, J.H. Understanding and contributing to the enigma of corporate social responsibility (CSR) assurance in the United States. Audit. J. Pract. Theory 2015, 34, 97–130. [Google Scholar] [CrossRef]

- Nikolaev, V.; Van Lent, L. The endogeneity bias in the relation between cost-of-debt capital and corporate disclosure policy. Eur. Account. Rev. 2005, 14, 677–724. [Google Scholar] [CrossRef]

- Jaggi, B.; Chin, C.-L.; Lin, H.-W.W.; Lee, P. Earnings forecast disclosure regulation and earnings management: Evidence from Taiwan IPO firms. Rev. Quant. Financ. Account. 2006, 26, 275–299. [Google Scholar] [CrossRef]

- Simnett, R.; Nugent, M. Developing an Assurance Standard for Carbon Emissions Disclosures. Aust. Account. Rev. 2007, 17, 37–47. [Google Scholar] [CrossRef]

- Huggins, A.; Green, W.J.; Simnett, R. The competitive market for assurance engagements on greenhouse gas statements: Is there a role for assurers from the accounting profession? Curr. Issues Audit. 2011, 5, A1–A12. [Google Scholar] [CrossRef] [Green Version]

- Cohen, J.; Holder-Webb, L.; Nath, L.; Wood, D. Retail Investors’ Perceptions of the Decision-Usefulness of Economic Performance, Governance, and Corporate Social Responsibility Disclosures. Behav. Res. Account. 2011, 23, 109–129. [Google Scholar] [CrossRef]

- Cohen, J.R.; Holder-Webb, L.; Zamora, V.L. Nonfinancial Information Preferences of Professional Investors. Behav. Res. Account. 2015, 27, 127–153. [Google Scholar] [CrossRef]

- Mock, T.J.; Rao, S.S.; Srivastava, R.P. The Development of Worldwide Sustainability Reporting Assurance. Aust. Account. Rev. 2013, 23, 280–294. [Google Scholar] [CrossRef]

- Park, J.; Brorson, T. Experiences of and views on third-party assurance of corporate environmental and sustainability reports. J. Clean. Prod. 2005, 13, 1095–1106. [Google Scholar] [CrossRef]

- Jones, M.J.; Solomon, J.F. Social and environmental report assurance: Some interview evidence. Account. Forum 2010, 34, 20–31. [Google Scholar] [CrossRef]

- Simnett, R.; Nugent, M.; Huggins, A.L. Developing an International Assurance Standard on Greenhouse Gas Statements. Account. Horiz. 2009, 23, 347–363. [Google Scholar] [CrossRef] [Green Version]

- Deegan, C.; Cooper, B.J.; Shelly, M. An investigation of TBL report assurance statements: UK and European evidence. Manag. Audit. J. 2006, 21, 329–371. [Google Scholar] [CrossRef]

- Manetti, G.; Becatti, L. Assurance Services for Sustainability Reports: Standards and Empirical Evidence. J. Bus. Ethics 2009, 87, 289–298. [Google Scholar] [CrossRef] [Green Version]

- O’Dwyer, B.; Owen, D.L. Assurance statement practice in environmental, social and sustainability reporting: A critical evaluation. Br. Account. Rev. 2005, 37, 205–229. [Google Scholar] [CrossRef]

- Hall, R. The strategic analysis of intangible resources. Strateg. Manag. J. 1992, 13, 135–144. [Google Scholar] [CrossRef]

- O’Dwyer, B.; Owen, D.; Unerman, J. Seeking legitimacy for new assurance forms: The case of assurance on sustainability reporting. Account. Organ. Soc. 2011, 36, 31–52. [Google Scholar] [CrossRef]

- Suchman, M.C. Managing legitimacy: Strategic and institutional approaches. Acad. Manag. Rev. 1995, 20, 571–610. [Google Scholar] [CrossRef] [Green Version]

- Margolis, J.D.; Walsh, J.P. Misery Loves Companies: Rethinking Social Initiatives by Business. Adm. Sci. Q. 2003, 48, 268–305. [Google Scholar] [CrossRef] [Green Version]

- Dhaliwal, D.S.; Radhakrishnan, S.; Tsang, A.; Yang, Y.G. Nonfinancial disclosure and analyst forecast accuracy: International evidence on corporate social responsibility disclosure. Account. Rev. 2012, 87, 723–759. [Google Scholar] [CrossRef]

- Black & Veatch. 2011 Strategic Directions Survey Results: Managing the Transition in the Electric Utility Industry. Available online: https://www.infrastructureusa.org/2011-strategic-directions-survey-results-managing-the-transition-in-the-electric-utility-industry/ (accessed on 28 November 2020).

- Core, J.E. A review of the empirical disclosure literature: Discussion. J. Account. Econ. 2001, 31, 441–456. [Google Scholar] [CrossRef] [Green Version]

- Healy, P.M.; Palepu, K.G. Information asymmetry, corporate disclosure, and the capital markets: A review of the empirical disclosure literature. J. Account. Econ. 2001, 31, 405–440. [Google Scholar] [CrossRef]

- Leuz, C.; Wysocki, P.D. Economic Consequences of Financial Reporting and Disclosure Regulation: A Review and Suggestions for Future Research. SSRN 2008, 1105398. [Google Scholar] [CrossRef]

- Dhaliwal, D.S.; Li, O.Z.; Tsang, A.; Yang, Y.G. Voluntary nonfinancial disclosure and the cost of equity capital: The initiation of corporate social responsibility reporting. Account. Rev. 2011, 86, 59–100. [Google Scholar] [CrossRef]

- Lackmann, J.; Ernstberger, J.; Stich, M. Market Reactions to Increased Reliability of Sustainability Information. J. Bus. Ethics 2012, 107, 111–128. [Google Scholar] [CrossRef]

- Glosten, L.R.; Milgrom, P.R. Bid, ask and transaction prices in a specialist market with heterogeneously informed traders. J. Financ. Econ. 1985, 14, 71–100. [Google Scholar] [CrossRef] [Green Version]

- Merton, R.C. A simple model of capital market equilibrium with incomplete information. J. Financ. 1987, 42, 483–510. [Google Scholar] [CrossRef]

- Mazumdar, S.C.; Sengupta, P. Disclosure and the Loan Spread on Private Debt. Financ. Anal. J. 2005, 61, 83–95. [Google Scholar] [CrossRef]

- Hughes, J.S.; Liu, J.; Liu, J. Information asymmetry, diversification, and cost of capital. Account. Rev. 2007, 82, 705–729. [Google Scholar] [CrossRef]

- Lambert, R.; Leuz, C.; Verrecchia, R.E. Accounting information, disclosure, and the cost of capital. J. Account. Res. 2007, 45, 385–420. [Google Scholar] [CrossRef] [Green Version]

- Diamond, D.W.; Verrecchia, R.E. Disclosure, liquidity, and the cost of capital. J. Financ. 1991, 46, 1325–1359. [Google Scholar] [CrossRef]

- Botosan, C.A. Disclosure level and the cost of equity capital. Account. Rev. 1997, 323–349. [Google Scholar]

- Lombardo, D.; Pagano, M. Law and Equity Markets: A Simple Model. In Corporate Governance Regimes: Convergence and Diversity; Oxford University Press: Oxford, UK, 1999; pp. 343–362. Available online: https://ssrn.com/abstract=209312 (accessed on 28 November 2020). [CrossRef] [Green Version]

- Xu, H.; Xu, X.; Yu, J. The Impact of Mandatory CSR Disclosure on the Cost of Debt Financing: Evidence from China. Emerg. Mark. Financ. Trade 2019, 1–15. [Google Scholar] [CrossRef]

- Bushman, R.M.; Smith, A.J. Financial accounting information and corporate governance. J. Account. Econ. 2001, 32, 237–333. [Google Scholar] [CrossRef] [Green Version]

- Sloan, R.G. Financial accounting and corporate governance: A discussion. J. Account. Econ. 2001, 32, 335–347. [Google Scholar] [CrossRef]

- Al-Tuwaijri, S.A.; Christensen, T.E.; Hughes, K. The relations among environmental disclosure, environmental performance, and economic performance: A simultaneous equations approach. Account. Organ. Soc. 2004, 29, 447–471. [Google Scholar] [CrossRef]

- Margolis, J.D.; Walsh, J.P. People and Profits? The Search for a Link between a Company’s Social and Financial Performance; Psychology Press: East Sussex, UK, 2001. [Google Scholar]

- Orlitzky, M.; Schmidt, F.L.; Rynes, S.L. Corporate Social and Financial Performance: A Meta-Analysis. Organ. Stud. 2003, 24, 403–441. [Google Scholar] [CrossRef]

- Anderson, J.C.; Frankle, A.W. Voluntary social reporting: An iso-beta portfolio analysis. Account. Rev. 1980, 467–479. [Google Scholar]

- Richardson, A.J.; Welker, M. Social disclosure, financial disclosure and the cost of equity capital. Account. Organ. Soc. 2001, 26, 597–616. [Google Scholar] [CrossRef]

- Frankel, R.; McNichols, M.; Wilson, G.P. Discretionary disclosure and external financing. Account. Rev. 1995, 135–150. [Google Scholar]

- Healy, P.M.; Hutton, A.P.; Palepu, K.G. Stock Performance and Intermediation Changes Surrounding Sustained Increases in Disclosure. Contemp. Account. Res. 1999, 16, 485–520. [Google Scholar] [CrossRef]

- Sengupta, P. Corporate disclosure quality and the cost of debt. Account. Rev. 1998, 459–474. [Google Scholar]

- Marx, B.; van Dyk, V. Sustainability reporting and assurance: An analysis of assurance practices in South Africa. Meditari Account. Res. 2011, 19, 39–55. [Google Scholar] [CrossRef]

- Jenkins, R. Corporate Codes of Conduct: Self-Regulation in a Global Economy, Technology, Business and Society Paper no. 2; United Nations Research Institute for Social Development: Geneva, Switzerland, 2001. [Google Scholar]

- Utting, P. Beyond social auditing: Micro and macro perspectives. In Proceedings of the EU Conference on “Responsible Sources: Improving Global Supply Chains Management”, Brussels, Belgium, 18 November 2005. [Google Scholar]

- Ballou, B.; Chen, P.C.; Grenier, J.H.; Heitger, D.L. Corporate social responsibility assurance and reporting quality: Evidence from restatements. J. Account. Public Policy 2018, 37, 167–188. [Google Scholar] [CrossRef]

- Michelon, G.; Patten, D.M.; Romi, A.M. Creating legitimacy for sustainability assurance practices: Evidence from sustainability restatements. Eur. Account. Rev. 2019, 28, 395–422. [Google Scholar] [CrossRef]

- Clarkson, P.; Li, Y.; Richardson, G.; Tsang, A. Causes and consequences of voluntary assurance of CSR reports. Account. Audit. Account. J. 2019, 32, 2451–2474. [Google Scholar] [CrossRef]

- Pflugrath, G.; Roebuck, P.; Simnett, R. Impact of assurance and assurer’s professional affiliation on financial analysts’ assessment of credibility of corporate social responsibility information. Audit. J. Pract. Theory 2011, 30, 239–254. [Google Scholar] [CrossRef]

- Hodge, K.; Subramaniam, N.; Stewart, J. Assurance of sustainability reports: Impact on report users’ confidence and percep-tions of information credibility. Aust. Account. Rev. 2009, 19, 178–194. [Google Scholar] [CrossRef]

- Martínez-Ferrero, J.; García-Sánchez, I.M. Sustainability assurance and cost of capital: Does assurance impact on credibility of corporate social responsibility information? Bus. Ethics Eur. Rev. 2017, 26, 223–239. [Google Scholar] [CrossRef]

- Jensen, M.C.; Meckling, W.H. Theory of the firm: Managerial behavior, agency costs and ownership structure. J. Financ. Econ. 1976, 3, 305–360. [Google Scholar] [CrossRef]

- Blackwell, D.W.; Noland, T.R.; Winters, D.B. The Value of Auditor Assurance: Evidence from Loan Pricing. J. Account. Res. 1998, 36, 57–70. [Google Scholar] [CrossRef]

- Kim, J.B.; Simunic, D.A.; Stein, M.T.; Yi, C.H. Voluntary audits and the cost of debt capital for privately held firms: Korean evidence. Contemp. Account. Res. 2011, 28, 585–615. [Google Scholar] [CrossRef]

- Knechel, W.R.; Wallage, P.; Eilifsen, A.; Van Praag, B. The Demand Attributes of Assurance Services Providers and the Role of Independent Accountants. Int. J. Audit. 2006, 10, 143–162. [Google Scholar] [CrossRef]

- Wallage, P. Assurance on sustainability reporting: An auditor’s view. Audit. J. Pract. Theory 2000, 19, 53–65. [Google Scholar] [CrossRef]

- Gray, R. Current Developments and Trends in Social and Environmental Auditing, Reporting and Attestation: A Review and Comment. Int. J. Audit. 2000, 4, 247–268. [Google Scholar] [CrossRef]

- DeAngelo, L.E. Auditor size and audit quality. J. Account. Econ. 1981, 3, 183–199. [Google Scholar] [CrossRef]

- Beatty, R.P. Auditor reputation and the pricing of initial public offerings. Account. Rev. 1989, 693–709. [Google Scholar]

- Francis, J.R.; Khurana, I.K.; Pereira, R. Disclosure Incentives and Effects on Cost of Capital around the World. Account. Rev. 2005, 80, 1125–1162. [Google Scholar] [CrossRef]

- Pittman, J.A.; Fortin, S. Auditor choice and the cost of debt capital for newly public firms. J. Account. Econ. 2004, 37, 113–136. [Google Scholar] [CrossRef]

- Brav, A.; Michaely, R.; Roberts, M.; Zarutskie, R. Evidence on the trade-off between risk and return for IPO and SEO Firms. Financ. Manag. 2009, 38, 221–252. [Google Scholar] [CrossRef]

- Sharfman, M.P.; Fernando, C.S. Environmental risk management and the cost of capital. Strateg. Manag. J. 2008, 29, 569–592. [Google Scholar] [CrossRef]

- Li, S. Does mandatory adoption of International Financial Reporting Standards in the European Union reduce the cost of equity capital? Account. Rev. 2010, 85, 607–636. [Google Scholar] [CrossRef]

- Zhang, G. Private information production, public disclosure, and the cost of capital: Theory and implications. Contemp. Ac-count. Res. 2001, 18, 363–384. [Google Scholar] [CrossRef]

- Clarkson, P.M.; Li, Y.; Richardson, G.D.; Vasvari, F.P. Revisiting the relation between environmental performance and en-vironmental disclosure: An empirical analysis. Account. Organ. Soc. 2008, 33, 303–327. [Google Scholar] [CrossRef]

- El Ghoul, S.; Guedhami, O.; Kwok, C.C.Y.; Mishra, D.R. Does corporate social responsibility affect the cost of capital? J. Bank Financ. 2011, 35, 2388–2406. [Google Scholar] [CrossRef]

- Kolk, A.; Perego, P. Determinants of the adoption of sustainability assurance statements: An international investigation. Bus. Strategy Environ. 2010, 19, 182–198. [Google Scholar] [CrossRef] [Green Version]

- Simnett, R.; Vanstraelen, A.; Chua, W.F. Assurance on Sustainability Reports: An International Comparison. Account. Rev. 2009, 84, 937–967. [Google Scholar] [CrossRef]

- Freeman, R.E. Strategic management: A stakeholder approach. Adv. Strateg. Manag. 1983, 1, 31–60. [Google Scholar]

- Ballou, B.; Heitger, D.L.; Landes, C.E. The future of corporate sustainability reporting: A rapidly growing assurance op-portunity. J. Account. 2006, 22, 5–74. [Google Scholar]

- Kolk, A.; van der Veen, M.L.; Hay, K.; Wennink, D. KPMG International Survey of Corporate Sustainability Reporting 2002; KPMG Global Sustainability Services: De Meern, The Netherlands, 2002. [Google Scholar]

- Patten, D.; Guidry, R. Market reactions to the first-time issuance of corporate sustainability reports: Evidence that quality matters. Sustain. Account. Manag. Policy J. 2010, 1, 33–50. [Google Scholar]

- Janamrung, B.; Issarawornrawanich, P. The association between corporate social responsibility index and performance of firms in industrial products and resources industries: Empirical evidence from Thailand. Soc. Responsib. J. 2015, 11, 893–903. [Google Scholar] [CrossRef]

- Farooq, M.B.; De Villiers, C. Sustainability assurance: Who are the assurance providers and what do they do? In Challenges in Managing Sustainable Business: Reporting, Taxation, Ethics and Governance; Palgrave Macmillan: Cham, Switzerland, 2019; pp. 137–154. [Google Scholar]

- Dentchev, N.A.; Van Balen, M.; Haezendonck, E. On voluntarism and the role of governments in CSR: Towards a contin-gency approach. Bus. Ethics Eur. Rev. 2015, 24, 378–397. [Google Scholar] [CrossRef]

- Gatti, L.; Seele, P.; Rademacher, L. Grey zone in—Greenwash out. A review of greenwashing research and implications for the voluntary-mandatory transition of CSR. Int. J. Corp. Soc. Responsib. 2019, 4, 1–15. [Google Scholar] [CrossRef]

- Leuz, C.; Verrecchia, R. The economic consequences of increased disclosure. J. Account. Res. 2000, 38, 91–124. [Google Scholar] [CrossRef]

Figure 1.

Research framework.

{kind=link}

Table 1.

Sample selection.

| Number of Observations | |||

|---|---|---|---|

| Food-Related Industries | Non-Food-Related Industries | Total | |

| Firms with CSR disclosure | 280 | 1845 | 2125 |

| Less: | |||

| Voluntary CSR disclosure and assurance | (35) | (1095) | (1130) |

| Financial institutions | - | (103) | (103) |

| Missing data | (25) | (64) | (89) |

| Final sample of this study | 220 | 583 | 803 |

Table 2.

Summary Statistics.

| Panel A Model (1) | |||||

| Variables | Mean | SD | Min | Median | Max |

| COD (%) | 2.488 | 3.102 | 0.930 | 1.820 | 3.154 |

| FR | 0.236 | 0.468 | 0.000 | 0.000 | 1.000 |

| MDP | 0.173 | 0.335 | 0.000 | 0.000 | 1.000 |

| FR × MDP | 0.065 | 0.279 | 0.000 | 0.000 | 1.000 |

| SIZE | 15.300 | 1.423 | 10.467 | 16.240 | 19.268 |

| MB | 1.586 | 1.768 | 0.323 | 1.242 | 1.984 |

| BETA | 0.758 | 0.832 | 0.395 | 0.754 | 1.225 |

| DE | 1.437 | 7.934 | 0.016 | 0.148 | 0.502 |

| TIE | 1788.834 | 26,757.680 | −2259.74 | 15.750 | 177,197.700 |

| STD | 1.738 | 1.456 | 1.294 | 1.736 | 2.681 |

| Panel BModel (2) and Model (3) | |||||

| Variables | Mean | SD | Min | Median | Max |

| COD (%) | 2.654 | 5.153 | 0.843 | 1.975 | 3.249 |

| MA | 0.254 | 0.482 | 0.000 | 0.000 | 1.000 |

| BIG4 | 0.846 | 0.329 | 0.000 | 1.000 | 1.000 |

| MA × BIG4 | 0.247 | 0.481 | 0.000 | 0.000 | 1.000 |

| SIZE | 14.985 | 1.569 | 12.247 | 15.743 | 18.123 |

| MB | 2.345 | 2.342 | 0.869 | 1.523 | 3.256 |

| BETA | 0.584 | 0.961 | 0.186 | 0.521 | 0.852 |

| DE | 0.242 | 0.242 | 0.005 | 0.196 | 0.314 |

| TIE | 1785.834 | 11,836.750 | −13.570 | 21.295 | 44,308.090 |

| STD | 1.694 | 1.734 | 0.982 | 1.842 | 2.873 |

Note: Detailed descriptions of variables can be found in Appendix A.

Table 3.

Univariate analysis.

| FR = 0 | MDP = 0 | MDP = 1 | Diff. in Means |

| Variables | Mean | Mean | |

| COD | 2.422 | 1.891 | −0.531 * |

| SIZE | 16.678 | 15.564 | −1.114 *** |

| MB | 1.485 | 1.168 | −0.317 ** |

| BETA | 0.848 | 0.678 | −0.170 ** |

| DE | 1.956 | 0.285 | −1.671 |

| TIE | 2143.944 | 183.989 | −1959.955 |

| STD | 1.933 | 1.780 | −0.153 |

| N | 498 | 85 | 583 |

| FR = 1 | MDP = 0 | MDP = 1 | Diff. in Means |

| Variables | Mean | Mean | |

| COD | 2.723 | 1.769 | −0.954 ** |

| SIZE | 15.427 | 15.536 | 0.109 |

| MB | 1.904 | 2.203 | 0.299 |

| BETA | 0.647 | 0.448 | −0.199 *** |

| DE | 0.233 | 0.196 | −0.037 |

| TIE | 683.073 | 4423.530 | 3740.458 ** |

| STD | 1.791 | 1.454 | −0.337 *** |

| N | 145 | 75 | 220 |

Note: *, **, and *** denote statistical significance at the 10%, 5%, and 1% levels, respectively.

Table 4.

Multiple regression analysis.

| Panel A | Panel B | |||

|---|---|---|---|---|

| Dependent Variable COD | Dependent Variable COD | |||

| Variables | Model (1) | Variables | Model (2) | Model (3) |

| Constant | 1.128 | Constant | −1.682 | −2.332 |

| (0.62) | (−0.31) | (−0.41) | ||

| FR | −1.083 ** | MA | −0.884 * | 0.958 |

| (−2.12) | (−1.28) | (0.51) | ||

| MDP | −0.014 | BIG4 | - | 0.875 |

| (−0.03) | (0.78) | |||

| FR × MDP | −0.519 * | MA × BIG4 | - | −2.154 |

| (−1.46) | (−1.07) | |||

| SIZE | 0.050 | SIZE | 0.138 | 0.136 |

| (0.47) | (0.41) | (0.38) | ||

| MB | 0.215 *** | MB | 0.229 * | 0.229 * |

| (2.47) | (1.53) | (1.5) | ||

| BETA | 0.409 * | BETA | −0.386 | −0.464 |

| (1.38) | (−0.42) | (−0.54) | ||

| DE | −0.025 ** | DE | −1.545 | −1.463 |

| (−2.03) | (−0.94) | (−0.86) | ||

| TIE | −0.000 | TIE | −0.000 | −0.000 |

| (−0.76) | (−0.32) | (−0.29) | ||

| STD | 0.712 *** | STD | 1.416 *** | 1.445 *** |

| (5.06) | (2.88) | (2.96) | ||

| Industry | Yes | Industry | - | - |

| Adj. R2 | 0.178 | Adj. R2 | 0.213 | 0.229 |

| N | 803 | N | 235 | 235 |

Note: *, **, and *** denote statistical significance at the 10%, 5%, and 1% levels, respectively.

Table 5.

Multiple regression analysis.

| Panel A | Panel B | |||

|---|---|---|---|---|

| Dependent Variable COD | Dependent Variable COD | |||

| Variables | Model (1) | Variables | Model (2) | Model (3) |

| Constant | 3.245 * | Constant | 0.178 | −1.024 |

| (1.28) | (0.03) | (−0.12) | ||

| FR | −1.618 ** | MA | −1.712 ** | 0.281 |

| (−2.09) | (−2.05) | (0.11) | ||

| MDP | −0.316 | BIG4 | - | 1.223 |

| (−0.71) | (0.65) | |||

| FR × MDP | −0.945 * | MA × BIG4 | - | −2.323 |

| (−1.32) | (−0.94) | |||

| SIZE | 0.024 | SIZE | 0.033 | 0.036 |

| (0.14) | (0.06) | (0.07) | ||

| MB | 0.238 ** | MB | 0.142 | 0.154 |

| (1.78) | (0.68) | (0.71) | ||

| BETA | −0.464 | BETA | −2.478 | −2.812 |

| (−0.79) | (−1.12) | (−1.23) | ||

| DE | −0.021 | DE | −0.876 | −0.586 |

| (−0.62) | (−0.33) | (−0.22) | ||

| TIE | −0.000 | TIE | −0.000 | −0.000 |

| (−0.76) | (−0.43) | (−0.36) | ||

| STD | 0.573 *** | STD | 2.623 *** | 2.722 *** |

| (3.25) | (2.71) | (2.76) | ||

| Industry | Yes | Industry | - | - |

| Adj. R2 | 0.072 | Adj. R2 | 0.067 | 0.062 |

| N | 495 | N | 125 | 125 |

Note: *, **, and *** denote statistical significance at the 10%, 5%, and 1% levels, respectively.

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Kuo, L.; Kuo, P.-W.; Chen, C.-C. Mandatory CSR Disclosure, CSR Assurance, and the Cost of Debt Capital: Evidence from Taiwan. Sustainability 2021, 13, 1768. https://0-doi-org.brum.beds.ac.uk/10.3390/su13041768

AMA Style

Kuo L, Kuo P-W, Chen C-C. Mandatory CSR Disclosure, CSR Assurance, and the Cost of Debt Capital: Evidence from Taiwan. Sustainability. 2021; 13(4):1768. https://0-doi-org.brum.beds.ac.uk/10.3390/su13041768

Chicago/Turabian StyleKuo, Lopin, Po-Wen Kuo, and Chun-Chih Chen. 2021. "Mandatory CSR Disclosure, CSR Assurance, and the Cost of Debt Capital: Evidence from Taiwan" Sustainability 13, no. 4: 1768. https://0-doi-org.brum.beds.ac.uk/10.3390/su13041768

Note that from the first issue of 2016, this journal uses article numbers instead of page numbers. See further details here.