Sustainability as a “New Normal” for Modern Businesses: Are SMEs of Pakistan Ready to Adopt It?

,

,  ,

,  ,

,  ,

,  ,

,

Abstract

:1. Introduction

2. Literature Review

{kind=link}

{kind=link}

{kind=link}

| Theory | Description |

|---|---|

| Institutional theory | Social institutions are imperative to establish a moral code for organizations [38,39] |

| Agency theory | CSR is an outcome of self-serving behavior of management at shareholders’ expense [40] |

| Stakeholder theory | CSR is principally the outcome of developing associations with actors/entities that are affected or can affect the businesses [41] |

| Resource based view | CSR is regarded as a potential capability that can generate competitive advantage [42] |

3. Methodology

4. Results

“………… to my knowledge, CSR is a concept that urges businesses to think of poor and deprived individuals of the society…….. SME-1

“……….. I am not confident about my knowledge of CSR, but from what I have heard it is related to charity, donations, and like that……….SME-8

“………..CSR means, we have to consider society while achieving our business objectives, which means supporting community in education and helping poor employees, etc. ……….. SME 4”

“………Yes, I can define it in that it is the responsibility of businesses to positively contribute for all stakeholders including customer, employees, society, and environment…….SME 2”

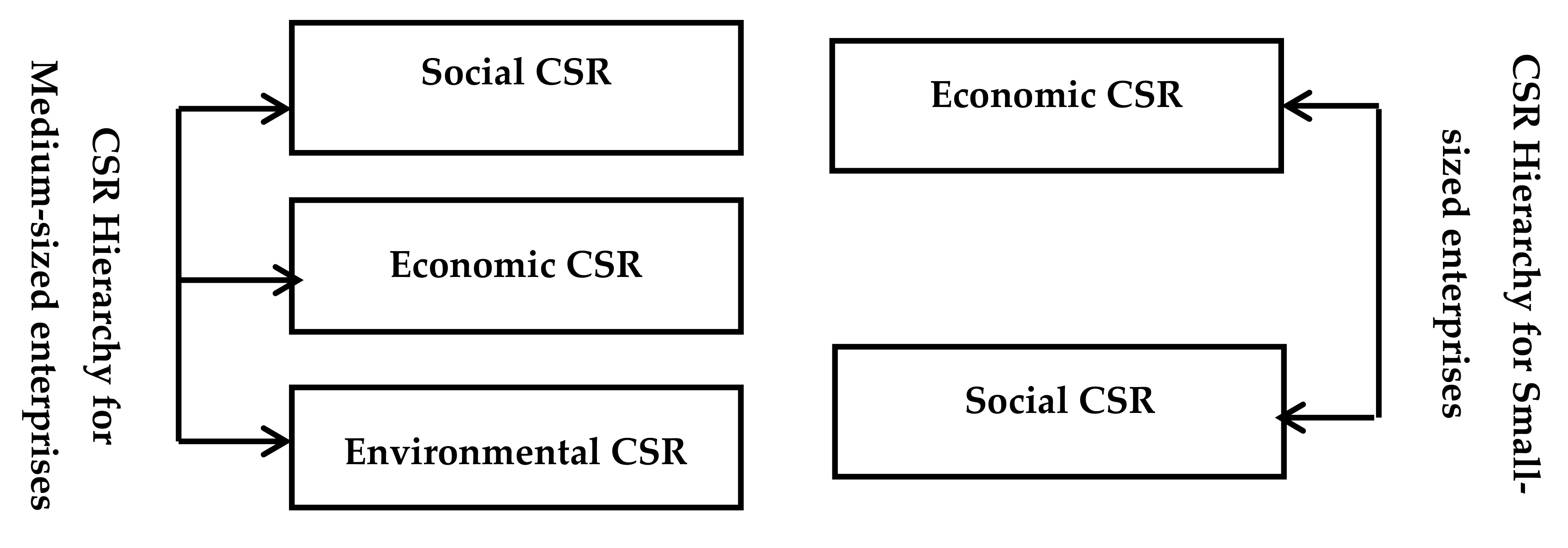

4.1. Social Dimension of CSR

“………..Our organization is not a big player in the industry, even though we contribute in different community building activities, for example, I can tell you that our organization supported one school in a remote area last year. The school was in poor condition and there was even no furniture available for the children. We managed almost fifty chairs for the students of that school………… SME-3”

“………Supporting the local community in the field of education is something that we really love to promote. We don’t have huge resources, but we want to support educational activities of local community. You might be aware that in our locality there is a campus of one large university; we each year sponsor two students who are deserving and unable to pay their semester fees. Although we intend to sponsor more students, in the current situation it looks difficult………. SME-4”

“………..We agree with your question regarding social responsibility of the business; in this regard, we are proud that we have different employee supporting programs just like health insurance and family support fund. Under these programs, the medical facility of our employees is totally free, and if some of our employees are having genuine problems on the part of his/her family, we do have a separate fund to support that employee. In this connection, we have a committee that reviews the matter and recommends the case of an employee for family support to the competent authorities to approve the family support fund………SME-4”

“……….Of course, we regard poor employees at our workplace under the philosophy of corporate social responsibility; poor employees at our workplace are supported financially. We have developed a fund for that purpose into which our organization contributes each month. This fund is invested in causes like marriage support of a poor worker’s daughter and the like. Furthermore, we have also a facility of employee loan without charging any interest to support a poor worker, financially………SME-6”

“……..As you know, we belong to a medium-sized business, and lack of resources is something that restricts us in many decisions. But our senior management (owner) is concerned with charity; for example, we donate funds to an NGO that manages food for the poor on daily bases. Although our donation is not sufficient enough, still we feel that at least we have something for charity on our part to contribute positively for society………SME-7”

4.2. Economic Dimension of CSR

“………..We have long term economic orientation here in our organization, because looking for short term economic prosperity is something that will not be working to improve the real economic health of our organization. We do understand, if we collapse financially, nothing will stay with us either the employees or the creditors. So we have much concern for economic outcomes, and this is not a shame to acknowledge that economic benefit is the one for which we are here………SME-9”

“……..We believe in price fairness and industry cost structure; we never try to charge huge profit margins from our customers, because we believe that charging extra profit margin is a short term philosophy, which is not going to help us in long run. Likewise, we go after economic efficiencies to reduce our unit cost and increase profit on fair grounds………SME-5”

“……… As you can see, we have a small scaled business, and it is logical to predict resource deficit in our organization. So to be honest, first thing is first, and yes we are largely concerned with economic orientation for our organization………SME-3”

“……… Look, this is something which is logical to think as a businessman, because being identified as a small business, yes we are concerned to improve our economic health, but we do desire not to harm society as well…….. SME-1”

4.3. Environmental Dimension of CSR

“………..Being a foreign qualified, I do have concerns for the environment, but this is pretty unfortunate that in our country nobody cares about it. I don’t remember ever since I have been managing this organization that some government official or agency approached us to ask us to contribute for environment……..SME-2”

“………Organizations in our sector are less concerned with the environmental dimension of CSR; as per my understanding, we feel that CSR is all about participating in social causes and community building activities. This is what we have been doing since we are operating here………SME-9”

“………. Yes, of course we consider the environment during our business operations; for example, last year we installed a new plant that uses less electricity and emits less greenhouse gases. Further, we also go for plantation as a tool to reduce our environmental footprint………SME-7”

“……… To address the issue of environmental degradation, we have improved our waste management mechanism; likewise, we have also replaced one of our old plants that was consuming more fuel and giving less efficiency………. SME-4”

“…….. To be honest, we believe that we do not emit huge amount of hazardous gases, because we belong to a small-scaled business. To my understanding, this responsibility is to be shouldered by large businesses……SME-8”

“……… Not at all, as I mentioned earlier, we have some donations for poor under the umbrella of CSR, but the specific context you are talking about barely exists here………. SME-1”

5. Discussion

Theoritical and Practical Implications

6. Conclusions

Limitations and Direction for Future

Author Contributions

Funding

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- El-Bassiouny, D.; El-Bassiouny, N. Diversity, corporate governance and CSR reporting. Manag. Environ. Qual. Int. J. 2019, 30, 116–136. [Google Scholar] [CrossRef]

- Lu, W.; Yeo, B. Time-Varying Relations between Seven Dimensions of CSR and Firm Risk. Bus. Prof. Ethics J. 2020, 39, 319–345. [Google Scholar] [CrossRef]

- Lis, B.; Neßler, C. CSR in Germany: A European Perspective. In Rethinking Business Responsibility in a Global Context; Springer: Berlin/Heidelberg, Germany, 2020; pp. 125–133. [Google Scholar]

- Norbit, N.; Nawawi, A.; Salin, A.S.A.P. Corporate social responsibility practices among the SMEs in Malaysia–a preliminary analysis. Manag. Account. Rev. 2017, 16, 17–40. [Google Scholar] [CrossRef]

- Susith, F.; Stewart, L.; Martine, K.; Murugesh, A. CSR practices in Sri Lanka: An exploratory analysis. Soc. Responsib. J. 2015, 11, 4. [Google Scholar]

- Zou, Z.; Liu, Y.; Ahmad, N.; Sial, M.S.; Badulescu, A.; Zia-Ud-Din, M.; Badulescu, D. What Prompts Small and Medium Enterprises to Implement CSR? A Qualitative Insight from an Emerging Economy. Sustainability 2021, 13, 952. [Google Scholar] [CrossRef]

- Bowen, H.R.; Johnson, F.E. Social Responsibility of the Businessman; Harper: New York, NY, USA, 1953. [Google Scholar]

- Lawler, E.E.; Worley, C.G. Designing organizations for sustainable effectiveness. Organ. Dyn. 2012, 4, 265–270. [Google Scholar] [CrossRef]

- Carroll, A.B. A three-dimensional conceptual model of corporate performance. Acad. Manag. Rev. 1979, 4, 497–505. [Google Scholar] [CrossRef] [Green Version]

- WBCSD. World Business Council for Sustainable Development. Available online: www.wbcsd.org (accessed on 11 November 2020).

- Michael, B. Corporate social responsibility in international development: An overview and critique 1. Corp. Soc. Responsib. Environ. Manag. 2003, 10, 115–128. [Google Scholar] [CrossRef] [Green Version]

- Dahlsrud, A. How corporate social responsibility is defined: An analysis of 37 definitions. Corp. Soc. Responsib. Environ. Manag. 2008, 15, 1–13. [Google Scholar] [CrossRef]

- Cho, C.H.; Michelon, G.; Patten, D.M.; Roberts, R.W. CSR report assurance in the USA: An empirical investigation of determinants and effects. Sustain. Account. Manag. Policy J. 2014, 5, 130–148. [Google Scholar] [CrossRef]

- Golob, U.; Bartlett, J.L. Communicating about corporate social responsibility: A comparative study of CSR reporting in Australia and Slovenia. Public Relat. Rev. 2007, 33, 1–9. [Google Scholar] [CrossRef]

- Ahmad, N.; Scholz, M.; Ullah, Z.; Arshad, M.Z.; Sabir, R.I.; Khan, W.A. The nexus of CSR and co-creation: A roadmap towards consumer loyalty. Sustainability 2021, 13, 523. [Google Scholar] [CrossRef]

- Mohammed, A.; Rashid, B. A conceptual model of corporate social responsibility dimensions, brand image, and customer satisfaction in Malaysian hotel industry. Kasetsart J. Soc. Sci. 2018, 39, 358–364. [Google Scholar] [CrossRef]

- Beddewela, E.; Fairbrass, J. Seeking legitimacy through CSR: Institutional pressures and corporate responses of multinationals in Sri Lanka. J. Bus. Ethics 2016, 136, 503–522. [Google Scholar] [CrossRef] [Green Version]

- Lattemann, C.; Fetscherin, M.; Alon, I.; Li, S.; Schneider, A.M. CSR communication intensity in Chinese and Indian multinational companies. Corp. Gov. Int. Rev. 2009, 17, 426–442. [Google Scholar] [CrossRef]

- Dobers, P.; Halme, M. Corporate social responsibility and developing countries. Corp. Soc. Responsib. Environ. Manag. 2009, 16, 237–249. [Google Scholar] [CrossRef] [Green Version]

- Idemudia, U. Corporate social responsibility and developing countries: Moving the critical CSR research agenda in Africa forward. Prog. Dev. Stud. 2011, 11, 1–18. [Google Scholar] [CrossRef]

- Jamali, D.; Karam, C.; Yin, J.; Soundararajan, V. CSR logics in developing countries: Translation, adaptation and stalled development. J. World Bus. 2017, 52, 343–359. [Google Scholar] [CrossRef]

- Baniya, R.; Rajak, K. Attitude, Motivation and barriers for csr engagement among travel and tour operators in Nepal. J. Tour. Hosp. Educ. 2020, 10, 53–70. [Google Scholar] [CrossRef]

- Saleem, I.; Siddique, I.; Akmal, A.; Khan, M.S.M.; Khan, M.U.; Sultan, S. Impact assessment of ISO 9000 series on the organizational performance: Empirical evidence from small and medium enterprise (SME) sector of Pakistan. Afr. J. Bus. Manag. 2011, 5, 10885–10892. [Google Scholar]

- D’amboise, G.; Muldowney, M. Management theory for small business: Attempts and requirements. Acad. Manag. Rev. 1988, 13, 226–240. [Google Scholar] [CrossRef]

- Chege, S.M.; Wang, D. Information technology innovation and its impact on job creation by SMEs in developing countries: An analysis of the literature review. Technol. Anal. Strateg. Manag. 2020, 32, 256–271. [Google Scholar] [CrossRef]

- Arshad, M.Z.; Khan, W.; Arshad, M.; Ali, M.; Shahdan, A.; Ishak, W. Importance and Challenges of SMEs: A Case of Pakistani SMEs. J. Res. Lepid. 2020, 51, 701–707. [Google Scholar] [CrossRef]

- Pakistan Today. SBP to Increase Financial Assistance for SMEs. Available online: https://profit.pakistantoday.com.pk/2018/08/27/sbp-to-increase-financial-assistance-for-smes/ (accessed on 4 January 2021).

- Laudal, T. Drivers and barriers of CSR and the size and internationalization of firms. Soc. Responsib. J. 2011, 7, 234–256. [Google Scholar] [CrossRef]

- Majeed, S.; Aziz, T.; Saleem, S. The effect of corporate governance elements on corporate social responsibility (CSR) disclosure: An empirical evidence from listed companies at KSE Pakistan. Int. J. Financ. Stud. 2015, 3, 530–556. [Google Scholar] [CrossRef]

- Chen, K.; Pan, Y. Sustainability of China’s listed commercial banks under background of the ‘new normal’. Asia-Pac. J. Account. Econ. 2020, 27, 685–702. [Google Scholar] [CrossRef]

- Ikram, M.; Sroufe, R.; Mohsin, M.; Solangi Yasir, A.; Shah Syed Zulfiqar, A.; Shahzad, F. Does CSR influence firm performance? A longitudinal study of SME sectors of Pakistan. J. Glob. Responsib. 2019, 11, 27–53. [Google Scholar] [CrossRef]

- Carroll, A.B. The pyramid of corporate social responsibility: Toward the moral management of organizational stakeholders. Bus. Horiz. 1991, 34, 39–48. [Google Scholar] [CrossRef]

- Saunila, M.; Rantala, T.; Ukko, J.; Havukainen, J. Why invest in green technologies? Sustainability engagement among small businesses. Technol. Anal. Strateg. Manag. 2019, 31, 653–666. [Google Scholar] [CrossRef]

- Freeman, R.E. Strategic Management: A Stakeholder Approach; Cambridge University Press: Cambridge, UK, 2010. [Google Scholar]

- Barney, J.B. Resource-based theories of competitive advantage: A ten-year retrospective on the resource-based view. J. Manag. 2001, 27, 643–650. [Google Scholar] [CrossRef]

- Khan, M.P.; Talib, N.A.; Kowang, T.O. Development of Sustainability Framework Based on the Theory of Resource Based View. Int. J. Acad. Res. Bus. Soc. Sci. 2018, 8, 636–647. [Google Scholar] [CrossRef] [Green Version]

- Yu, H.-C.; Kuo, L.; Kao, M.-F. The relationship between CSR disclosure and competitive advantage. Sustain. Account. Manag. Policy J. 2017, 8, 547–570. [Google Scholar] [CrossRef]

- Aggarwal, V.S.; Jha, A. Pressures of CSR in India: An institutional perspective. J. Strategy Manag. 2019, 12, 227–242. [Google Scholar] [CrossRef]

- Espinoza-Ramos, G.R. ‘Unwritten Rules’ in Social Partnerships: Defining Corporate Social Responsibility (CSR) Through Institutional Theory in the Peruvian Mining Industry. In Responsible Business in a Changing World; Springer: Berlin/Heidelberg, Germany, 2020; pp. 235–245. [Google Scholar]

- Li, F.; Li, T.; Minor, D. CEO power, corporate social responsibility, and firm value: A test of agency theory. Int. J. Manag. Financ. 2016, 12, 611–628. [Google Scholar] [CrossRef]

- Theodoulidis, B.; Diaz, D.; Crotto, F.; Rancati, E. Exploring corporate social responsibility and financial performance through stakeholder theory in the tourism industries. Tour. Manag. 2017, 62, 173–188. [Google Scholar] [CrossRef] [Green Version]

- Kofford, S.; Clark, A.; Jones Christensen, L.M. Barriers to Imitation in Strategic CSR: Organizational Authenticity and the Resource-Based View. In Proceedings of Academy of Management Proceedings; Academy of Management: Briarcliff Manor, NY, USA, 2020; p. 21329. [Google Scholar]

- Germanwatch. Global Climate Risk Index 2020. Available online: www.germanwatch.org (accessed on 19 October 2020).

- Mahmood, M.T.; Shahab, S.; Hafeez, M. Energy capacity, industrial production, and the environment: An empirical analysis from Pakistan. Environ. Sci. Pollut. Res. 2020, 27, 4830–4839. [Google Scholar] [CrossRef]

- Maniora, J. Mismanagement of sustainability: What business strategy makes the difference? Empirical evidence from the USA. J. Bus. Ethics 2018, 152, 931–947. [Google Scholar] [CrossRef]

- Elliott, D.; Husbands, S.; Hamdy, F.C.; Holmberg, L.; Donovan, J.L. Understanding and improving recruitment to randomised controlled trials: Qualitative research approaches. Eur. Urol. 2017, 72, 789–798. [Google Scholar] [CrossRef] [Green Version]

- Willis, D.G.; Sullivan-Bolyai, S.; Knafl, K.; Cohen, M.Z. Distinguishing features and similarities between descriptive phenomenological and qualitative description research. West. J. Nurs. Res. 2016, 38, 1185–1204. [Google Scholar] [CrossRef]

- IQAir. Air Quality in Pakistan. Available online: https://www.iqair.com/us/pakistan (accessed on 3 January 2021).

- Awan, U.; Khattak, A.; Kraslawski, A. Corporate social responsibility (CSR) priorities in the small and medium enterprises (SMEs) of the industrial sector of Sialkot, Pakistan. In Corporate Social Responsibility in the Manufacturing and Services Sectors; Springer: Berlin/Heidelberg, Germany, 2019; pp. 267–278. [Google Scholar]

- Neeley, T.B.; Dumas, T.L. Unearned status gain: Evidence from a global language mandate. Acad. Manag. J. 2016, 59, 14–43. [Google Scholar] [CrossRef]

- Bello, F.G.; Kamanga, G. Drivers and barriers of corporate social responsibility in the tourism industry: The case of Malawi. Dev. South. Afr. 2020, 37, 181–196. [Google Scholar] [CrossRef]

- Gioia, D.A.; Corley, K.G.; Hamilton, A.L. Seeking qualitative rigor in inductive research: Notes on the Gioia methodology. Organ. Res. Methods 2013, 16, 15–31. [Google Scholar] [CrossRef]

- Forsman-Hugg, S.; Katajajuuri, J.M.; Riipi, I.; Mäkelä, J.; Järvelä, K.; Timonen, P. Key CSR dimensions for the food chain. Br. Food J. 2013, 115, 30–47. [Google Scholar] [CrossRef]

- Azmat, F.; Zutshi, A. Perceptions of corporate social responsibility amongst immigrant entrepreneurs. Soc. Responsib. J. 2012, 8, 63–76. [Google Scholar] [CrossRef]

- Arbe Montoya, A.I.; Hazel, S.J.; Matthew, S.M.; McArthur, M.L. Why do veterinarians leave clinical practice? A qualitative study using thematic analysis. Vet. Rec. 2021, 188, 49–58. [Google Scholar] [CrossRef]

- Camilleri, M.A. Reconceiving corporate social responsibility for business and educational outcomes. Cogent Bus. Manag. 2016, 3, 1142044. [Google Scholar] [CrossRef]

- Mohrman, S.A.; Lawler, E.E., III. Designing organizations for sustainable effectiveness. J. Organ. Eff. People Perform. 2014, 41, 265–270. [Google Scholar]

- Carlini, J.; Grace, D. The corporate social responsibility (CSR) internal branding model: Aligning employees’ CSR awareness, knowledge, and experience to deliver positive employee performance outcomes. J. Mark. Manag. 2021, 1–29. Available online: https://0-www-tandfonline-com.brum.beds.ac.uk/doi/full/10.1080/0267257X.2020.1860113 (accessed on 10 February 2021). [CrossRef]

- Gaither, B.M.; Austin, L.; Schulz, M. Delineating CSR and social change: Querying corporations as actors for social good. Public Relat. Inq. 2018, 7, 45–61. [Google Scholar] [CrossRef]

- Torugsa, N.A.; O’Donohue, W.; Hecker, R. Proactive CSR: An empirical analysis of the role of its economic, social and environmental dimensions on the association between capabilities and performance. J. Bus. Ethics 2013, 115, 383–402. [Google Scholar] [CrossRef] [Green Version]

- Bevan, E.A.; Yung, P. Implementation of corporate social responsibility in Australian construction SMEs. Eng. Constr. Archit. Manag. 2015, 22, 295–311. [Google Scholar] [CrossRef]

- Zutshi, A.; Creed, A.; Panwar, R.; Willis, L. Corporate social responsibility (CSR): Curators’ specific responses from Australian museums and art galleries. Curr. Issues Tour. 2020, 1–17. Available online: https://0-www-tandfonline-com.brum.beds.ac.uk/doi/full/10.1080/13683500.2020.1729104 (accessed on 10 February 2021). [CrossRef]

- Diab, A.; Metwally, A.B.M. Institutional complexity and CSR practices: Evidence from a developing country. J. Account. Emerg. Econ. 2020, 10, 655–680. [Google Scholar] [CrossRef]

- Hassan, Z.; Nareeman, A. Impact of CSR practices on customer satisfaction and retention: An empirical study on foreign MNCs in Malaysia. SSRN 2013. [CrossRef]

- Sun, H.; Rabbani, M.R.; Ahmad, N.; Sial, M.S.; Cheng, G.; Zia-Ud-Din, M.; Fu, Q. CSR, Co-Creation and Green Consumer Loyalty: Are Green Banking Initiatives Important? A Moderated Mediation Approach from an Emerging Economy. Sustainability 2020, 12, 10688. [Google Scholar] [CrossRef]

- Ndubisi, N.O.; Zhai, X.A.; Lai, K.-h. Small and medium manufacturing enterprises and Asia’s sustainable economic development. Int. J. Prod. Econ. 2020, 107971. [Google Scholar] [CrossRef]

- Taylor, J.; Vithayathil, J.; Yim, D. Are corporate social responsibility (CSR) initiatives such as sustainable development and environmental policies value enhancing or window dressing? Corp. Soc. Responsib. Environ. Manag. 2018, 25, 971–980. [Google Scholar] [CrossRef]

- Moscato, D. Corporate Social Responsibility Committing to Social and Environmental Impact. Handb. Financ. Commun. Invest. Relat. 2018, 221. [Google Scholar]

- Kuroda, K.; Ishida, Y. CSR in Japan: Toward Integration and Corporate–CSO Partnership. In Corporate Social Responsibility and the Three Sectors in Asia; Springer: Berlin/Heidelberg, Germany, 2017; pp. 45–71. [Google Scholar]

- Santos, M. CSR in SMEs: Strategies, practices, motivations and obstacles. Soc. Responsib. J. 2011, 7, 490–508. [Google Scholar] [CrossRef]

- Kong, L.; Sial, M.S.; Ahmad, N.; Sehleanu, M.; Li, Z.; Zia-Ud-Din, M.; Badulescu, D. CSR as a Potential Motivator to Shape Employees’ View towards Nature for a Sustainable Workplace Environment. Sustainability 2021, 13, 1499. [Google Scholar] [CrossRef]

- Raza, A.; Saeed, A.; Iqbal, M.K.; Saeed, U.; Sadiq, I.; Faraz, N.A. Linking corporate social responsibility to customer loyalty through co-creation and customer company identification: Exploring sequential mediation mechanism. Sustainability 2020, 12, 2525. [Google Scholar] [CrossRef] [Green Version]

- Inekwe, M.; Hashim, F.; Yahya, S.B. CSR in developing countries–the importance of good governance and economic growth: Evidence from Africa. Soc. Responsib. J. 2020. [CrossRef]

- Nguyen, H.T.; Le, D.M.D.; Ho, T.T.M.; Nguyen, P.M. Enhancing sustainability in the contemporary model of CSR: A case of fast fashion industry in developing countries. Soc. Responsib. J. 2020. [CrossRef]

- LaGore, W.; Mahoney, L.; Thorne, L. An implicit-explicit examination of differences in CSR practices between the USA and Europe. Soc. Bus. Rev. 2020, 15, 165–187. [Google Scholar] [CrossRef]

- Lajmi, A. Relevance of voluntary environmental and social reporting in the French context: Does CSR assurance matter? Environ. Econ. 2020, 11, 54. [Google Scholar] [CrossRef]

- Lawler, E.E., III; Conger, J.A. The sustainable effectiveness governance model: Moving corporations beyond the philanthropy paradigm. Organ. Dyn. 2014, 44, 97–103. [Google Scholar]

| No | Established | Size | Staff | Location | Focus | Sector | Interviewing Person |

|---|---|---|---|---|---|---|---|

| SME 1 | 2013 | Small | 15–25 | Lahore | Domestic | Textile | Owner–Manager |

| SME 2 | 1998 | Medium | 115–135 | Lahore | Domestic | Chemical | Manager production |

| SME 3 | 2015 | Small | 20–35 | Lahore | Domestic | Apparel | Owner–Manager |

| SME 4 | 2000 | Medium | 70–80 | Lahore | Export | Apparel | Manager |

| SME 5 | 2001 | Medium | 90–125 | Lahore | Export | Chemical | Unit Manager |

| SME 6 | 2000 | Medium | 80–85 | Lahore | Domestic | Textile | Manager operations |

| SME 7 | 2009 | Medium | 50–65 | Lahore | Domestic | Textile | Unit-Manager |

| SME 8 | 2012 | Small | 30–35 | Lahore | Export | Accessories | Owner–Manager |

| SME 9 | 2014 | Medium | 115–120 | Lahore | Export | Accessories | Manager production |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Ahmad, N.; Mahmood, A.; Han, H.; Ariza-Montes, A.; Vega-Muñoz, A.; Din, M.u.; Iqbal Khan, G.; Ullah, Z. Sustainability as a “New Normal” for Modern Businesses: Are SMEs of Pakistan Ready to Adopt It? Sustainability 2021, 13, 1944. https://0-doi-org.brum.beds.ac.uk/10.3390/su13041944

Ahmad N, Mahmood A, Han H, Ariza-Montes A, Vega-Muñoz A, Din Mu, Iqbal Khan G, Ullah Z. Sustainability as a “New Normal” for Modern Businesses: Are SMEs of Pakistan Ready to Adopt It? Sustainability. 2021; 13(4):1944. https://0-doi-org.brum.beds.ac.uk/10.3390/su13041944

Chicago/Turabian StyleAhmad, Naveed, Asif Mahmood, Heesup Han, Antonio Ariza-Montes, Alejandro Vega-Muñoz, Mohi ud Din, Ghazanfar Iqbal Khan, and Zia Ullah. 2021. "Sustainability as a “New Normal” for Modern Businesses: Are SMEs of Pakistan Ready to Adopt It?" Sustainability 13, no. 4: 1944. https://0-doi-org.brum.beds.ac.uk/10.3390/su13041944