COVID-19 Pandemic, Sustainability of Macroeconomy, and Choice of Monetary Policy Targets: A NK-DSGE Analysis Based on China

Economics and Management School, Wuhan University, Wuhan 430072, China

*

Author to whom correspondence should be addressed.

Sustainability 2021, 13(6), 3362; https://0-doi-org.brum.beds.ac.uk/10.3390/su13063362

Submission received: 3 February 2021

/

Revised: 16 March 2021

/

Accepted: 16 March 2021

/

Published: 18 March 2021

(This article belongs to the Special Issue Monetary and Financial Sustainability in a Post COVID-19 World)

Abstract

:This paper studies the impact of the COVID-19 pandemic on the sustainability of Chinese economic growth, government debt, and income inequality by constructing a new Keynesian dynamic stochastic general equilibrium (NK-DSGE) model. The choice of monetary policy targets is then analyzed to hedge the impact of the pandemic. We find that: (1) the aggregate demand and labor demand shocks caused by the COVID-19 pandemic posed serious challenges to the sustainable development of the economy and debt, and increased social inequality; (2) when the impact of the pandemic is mainly reflected in the recession in aggregate demand, monetary policy should pay more attention to the target of price stability; (3) when the impact of the pandemic is mainly reflected in a decline in labor demand, monetary policy should focus more on the target of economic growth; (4) when the pandemic has a significant impact on both aggregate demand and labor demand, a monetary policy which focuses more on the target of economic growth is conducive to minimizing welfare losses. Targeted policy implications, such as selecting monetary policy targets according to different manifestations of the impact of the COVID-19 pandemic and placing emphasis on monetary policy tools to stimulate consumption, alleviate unemployment, and alleviate social inequality, are suggested to improve the sustainability of the Chinese economy.

1. Introduction

Since 2020, the COVID-19 pandemic has posed a severe challenge to the sustainability of Chinese macroeconomic operations [1]. In this context, discussion about the impact of the COVID-19 pandemic on sustainable economic development and policy response in China has attracted great attention from academics and generated a variety of opinions. As far as the impact of the COVID-19 pandemic on the Chinese macroeconomy is concerned, in the early stage of the outbreak, the Chinese government adopted a strict traffic blockade represented by a “lockdown” and national home quarantine. The impact of the COVID-19 pandemic was mainly reflected in the supply chain—namely, the industrial chain was impeded, the labor supply was limited, and the production and supply of products was stagnant. However, since the second quarter of 2020, the Chinese campaign for pandemic prevention and control has won a decisive victory, and the momentum of concentrated outbreaks of COVID-19 has been significantly curbed. Therefore, the series of strict emergency prevention and control measures taken by China in the early stages have been gradually phased out, and regular prevention and control measures such as social distancing and local quarantine on a small scale have been adopted [2]. In this situation, as people have resumed work and normal life, the supply of labor has gradually recovered and the industrial chain reopened. The impact of the pandemic on the Chinese macroeconomy has gradually moved from the supply side to the demand side. In particular, the global macroeconomic downturn caused by the spread of the pandemic in various regions around the world and the resulting uncertainty about future economic expectations [3,4], coupled with the combined effects of regular control measures and the global economic recession, have resulted in a significant contraction in domestic and foreign aggregate demand. At the same time, the profitability of enterprises has declined, and they have been forced to expand their scale of layoffs. As a result, the demand for labor in the enterprise sector has decreased, and the unemployment problem has become increasingly prominent.

Monetary policy, as an important part of macro control policies, has been given high priority in order to cope with the great uncertainty caused by the COVID-19 pandemic on the demand side of the Chinese economy at the present stage. On the one hand, monetary policy should ensure the sustainable growth of the economy and the realization of employment targets. On the other hand, monetary policy should also pay attention to the stability of the currency value and avoid hyperinflation.

In order to respond to the COVID-19 pandemic and promote the sustainability of economic development, on the one hand, the People’s Bank of China has taken a series of measures such as reducing the deposit reserve ratio, enhancing the implementation of structural monetary policy, and creating monetary policy tools that directly reach the entity economy to increase liquidity and reduce the financing cost, consequently ensuring the realization of the goals of keeping growth and employment stable. On the other hand, compared with unconventional monetary policies such as unlimited quantitative easing, zero interest rates, and negative interest rates adopted by developed economies, including the Federal Reserve and the European Central Bank in response to the pandemic [5,6], the policy stance of the central bank of China has generally been more restrained, and it has become one of the few countries in the world that still maintains a normal monetary policy after the pandemic. In response to pandemic shocks, the People’s Bank of China has not resorted to indiscriminate strong stimulus, but this emphasizes that a prudent monetary policy should be flexible, appropriate, pay attention to policy pertinence, and look to the future. The above phenomenon has also led to much discussion. In the face of the serious shock caused by the COVID-19 pandemic, what choice should monetary policy target between promoting sustainable economic growth and maintaining price stability? When faced with different types of pandemic shocks, will there be differences in the choice of monetary policy targets? Therefore, in the context of the long-term impact of the COVID-19 pandemic, analyses on how to choose monetary policy targets to alleviate the various adverse shocks brought about by the pandemic and its impact on social welfare provide policy references for China and other countries in the world in their attempt to promote the sustainability of macroeconomic growth and improve people’s livelihood and welfare.

In the current work, we construct a new Keynesian dynamic stochastic general equilibrium (NK-DSGE) model with heterogeneous households, two kinds of firms, a fiscal sector, and a central bank which considers the probability of a pandemic and simulates how to select a monetary policy target when facing two types of problems—namely, the aggregate demand recession and labor demand decline caused by the COVID-19 pandemic. The research yields several main findings: (1) The aggregate demand and labor demand shocks caused by the COVID-19 pandemic posed a serious challenge to the sustainable development of the Chinese economy. While increasing the downward pressure on the economy, they weakened the sustainability of government debt and increased social inequality. (2) When the impact of the pandemic is mainly reflected in a decline in aggregate demand, monetary policy should pay more attention to the target of price stability to maintain the stability of the currency value. (3) When the impact of the pandemic is mainly reflected in rising unemployment and declining labor demand, monetary policy should focus more on the target of economic growth to tackle employment issues. (4) When the COVID-19 pandemic has a significantly adverse impact on both aggregate demand and labor demand, monetary policy should focus on the target of economic growth in the long term to minimize social welfare losses.

The remainder of the paper is organized as follows. Section 2 reviews literature on the effects of the COVID-19 pandemic and the choice of monetary policy targets. Section 3 lays out the NK-DSGE model. Section 4 reports the calibration and estimation of the model parameters. Section 5 presents and discusses the results. Section 6 concludes the research.

2. Literature Review

This study is related to various strands of the literature. To date, several studies have been conducted on the macroeconomic impacts of the COVID-19 pandemic. First, many papers have explored the influences on aggregated demand and private consumption. Kim et al. [7] argued that the consumption spending of small business owners declined by roughly 40% due to the pandemic, especially in the areas of travel, restaurants, and personal services. Similarly, Baker et al. [8] used transaction-level household financial data to investigate the impact of the pandemic on household consumption and found that consumption increased at the beginning of the pandemic; however, spending then decreased sharply due to greater levels of social distancing. Moreover, the impacts of the COVID-19 pandemic on demand forecasts should not be ignored—for example, Balla-Elliott et al. [9] claim that the COVID-19 pandemic will affect the reopening of firms through the channel of demand forecasts, and business owners will delay their post-lockdown reopening due to a low level of expected demand based on a nationwide survey of small businesses.

The pandemic also brings about adverse shocks to labor demand and employment due to the unsustainability of economic growth. Fang et al. [10] reviewed 100 million jobs posted on online platforms in China and found that the amount of new jobs posted within the first 13 weeks after the Wuhan lockdown on 23 January 2020, was about one-third lower than that in the same period in the previous years. Furthermore, Brada et al. [11] deployed the employment data of Central and Eastern Europe countries during the COVID-19 pandemic and pointed out that recovery from the effects of the pandemic on employment would be very slow, with a two-year recovery period. Goswami et al. [12] noticed that the heterogeneous effects of the COVID-19 pandemic on unemployment among different groups in India and pointed out that the labor force in the secondary and tertiary sectors has suffered larger unemployment and economic losses. Some researchers have turned their focus to the adverse effects of eradicating extreme poverty in China and argued that households in the bottom four quintiles will be more likely to fall back into poverty more due to the rising off-farm unemployment caused by the COVID-19 pandemic [13].

The impact of the COVID-19 pandemic on various countries is also different. Tian [14] found that although the COVID-19 pandemic would bring serious challenges to China in the first quarter of 2020, it could be controlled quickly and effectively thanks to the strong measures taken by the Chinese government in self-protection, mobility control, resource allocation, professional health, and other aspects. Furthermore, the policies implemented by China to help SMEs, such as tax reduction and credit support, have also strongly stimulated the economic recovery. By contrast, the impact of the COVID-19 pandemic on India has been even more severe. Sahoo and Ashwani [15] simulated the economic losses of India caused by the COVID-19 pandemic in different circumstances and found that even in the most optimistic case, the Indian economy would barely maintain a weak growth of 0.5% in 2020, with the worst impact on trade, manufacturing, and MSME sectors. Achim et al. [16] pointed out that cultural background would affect the anti-pandemic effect of each country, that is, under the western democratic system, excessively advocating individualism would increase the difficulty of fighting against the COVID-19 pandemic, while countries advocating collectivism would be more effective in responding to the pandemic. In addition, the increased proportion of immigrants and the elderly will also increase the transmission rate and mortality of the COVID-19 pandemic. In addition to the above perspectives, other studies have investigated the complex macroeconomic impacts of the COVID-19 pandemic on the industrial economy, the financial market, commodity price volatility, productivity, asset price, etc. Most of these papers hold the opinion that the adverse effects caused by the COVID-10 pandemic are more serious than those of the global financial crisis in 2008, so we must handle this challenge prudently [17,18,19,20,21].

Our research is also related to the literature analyzing the choice of monetary policy targets. Existing studies have pointed out the monetary policy which focuses on two primary objectives—namely, price stability and economic growth [22,23]. Besides these, there are some studies that suggest monetary policy should also pay attention to other subordinate goals, such as financial stability, asset prices, and exchange rates [24,25]. Yet other studies shed light on the choice of monetary policy in specific countries. For example, Liu et al. [26] pointed out that the leading monetary policy goal in China was price stability, followed by output stability and interest rate smoothing. Zhu et al. [27] pointed out that the Bank of England had paid relatively more attention to inflation targets over the past 16 years. Besides this, Hossain and Arwatchanakarn [28] relied on quarterly data from Thailand and suggested that money growth has a significant distributed-lag impact on inflation. Sánchez [29] shed light on the dilemma of the choice of monetary policy under the conditions of inflation uncertainty and unemployment uncertainty, finding that it was best to disclose the inflation target and conceal the unemployment target by building a two-stage game model.

Previous literature has conducted some discussions on related issues, however, there are still some deficiencies. In contrast, the innovations of this paper mainly concern other issues. (1) The research perspective of the existing literature on the impact of the COVID-19 pandemic and the corresponding monetary policy is relatively broad. The literature also lacks micro foundation and model simulation, so it has limited pertinency. Based on Chinese data, this paper incorporates the probability of a concentrated outbreak of COVID-19 in the model framework so that the research results are more in line with the actual situation in China. (2) Existing studies have a narrow perspective on the impact of the pandemic and focus only on the impact on basic macro variables such as output, consumption, and investment. This paper introduces fiscal factors into the model and constructs an income inequality index based on the income gap between two types of households so as to investigate the impact of the pandemic on the sustainability of government debt and income inequality. Therefore, this research enriches the perspectives of existing literature and could also provide recommendations on the choice of monetary policy targets for other countries and regions in the context of the COVID-19 pandemic.

3. Model

In this section, we built an NK-DSGE (new Keynesian dynamic stochastic general equilibrium) model. The model is a closed-economy DSGE model with heterogeneous households, labor intermediaries, final goods producers, intermediate goods producers, fiscal authority, and a central bank. Besides this, to take into account the features of the COVID-19 pandemic, we adopt the method of describing disaster risks and probability shocks, which lead to physical capital and total factor productivity declines [30,31]. Thus, we include the COVID-19 pandemic probability shocks in the model through a similar method. The rest of the model is classical, and we include inertia in consumption, adjustment of costs in investment, price stickiness, wage stickiness, and the costs of capital utilization.

3.1. Households

According to the principle of Ricardian equivalence, the effects of macroeconomic policy will be weakened if some households can maximize their levels of utility throughout the whole life cycle. Thus, the household section consists of two types of households in this model. Ricardian households can have free access to the financial market, which means that they can hold government bonds, make investment decisions, and bring future income to the present. Correspondingly, non-Ricardian households are subject to liquidity constraints, which implies that they do not have access to the financial market and credit market.

3.1.1. Ricardian Households

The model assumed that each Ricardian household maximizes its intertemporal utility function in terms of consumption and leisure . The utility maximization problem of this household is defined as:

where t indexes time, is the discount rate, and denote the consumption and labor supply of Ricardian households, is the inverse of the Frisch elasticity of labor supply, h is habit formation in consumption. The aggregated demand shock, follows an AR(1) process:

where the aggregated demand COVID-19 pandemic shock follows as:

The macroeconomy switches from normal times to the COVID-19 pandemic state with the probability in the (t + 1) period. When the outbreak of COVID-19 has the probability in the t+1 period, a share ΔD of the original aggregated demand will be destroyed. Otherwise, . follows a logarithm AR(1) process:

where denotes pandemic probability shock in aggregated demand, and .

The Ricardian households’ budget constraint is given by:

The law of motion for capital stock follows:

where is a parameter for the adjustment cost of investment and denotes the depreciation rate of private capital.

Thus, the Ricardian household chooses optimal consumption , labor supply , bond holdings , utilization rate of capital , investment , and capital stock to maximize utility function (1), subject to the constraints (5) and (7).

3.1.2. Non-Ricardian Households

The utility function of non-Ricardian households is identical to that of Ricardian households, but they choose optimal consumption and labor supply subject to their current income. Thus, their utility function is given as:

The non-Ricardian households’ budget constraint is given by:

Similarly, the non-Ricardian household chooses optimal consumption , labor supply to maximize utility function (8), subject to the constraints (9).

3.2. Labor Intermediaries and Wage Stickiness

Labor intermediaries aggregate the heterogeneous labor supplied by households into homogeneous labor. The final labor demand is given as:

where denotes the substitution between heterogeneous labor types.

In line with Calvo [32], only percent of households can change their wages to optimally each period. However, percent of households have to peg their last period’s wages. Thus, the aggregated wage is given as:

Then, we can obtain the function of optimal wages:

3.3. Final Goods Firms

The final goods firms sell aggregate intermediate goods in a perfect competition market. According to Dixit and Stiglitz [33], the production function of final goods firms can be described as:

where denotes the substitution between heterogeneous intermediate goods.

According to Equation (13), the demand function of intermediate goods is given as:

3.4. Intermediate Goods Firms

The intermediate goods firms produce capital and labor supplied by households into intermediate goods in a monopolistic competition market. Intermediate goods are produced according to the Cobb-Douglas production function:

where adjusted capital ; denotes total factor productivity; and according to motion law:

where is the total factor productivity shock and .

The cost minimization problem of intermediate goods firms can be given as:

where denotes labor demand shock and can be described as:

Similar to aggregated demand shock, the labor demand shocks caused by the COVID-19 pandemic follow as:

When the probability of the outbreak of COVID-19 is in the t+1 period, a share of labor demand will decline. Otherwise, . follows a logarithm AR(1) process:

where denotes pandemic probability shock in labor demand, and .

Solving (17) subject to production function (15), we can obtain the expression of optimal adjusted capital and labor demand as follows:

Identical to the form of wage stickiness, we assume there are price-setting frictions in the macroeconomy. Namely, only percent of households can change prices to optimally each period. However, the remaining households have to peg the last period prices. Thus, the motion law of price level is given as:

Furthermore, the profit maximization problem of intermediate goods firms is as follows:

where denotes total costs, and .

Solving (24), the optimal price level is given as:

where denotes the shadow price of wealth.

3.5. Central Bank

According to Sargent and Surico [34], the central bank set the policy rate following the rule which is given as:

where is the steady-state value of the policy rate, denotes the persistence of the policy rate, and are sensitive parameters for policy response to inflation gap and output gap, stands for monetary policy shock, and .

3.6. Fiscal Authority

Fiscal authority acquires revenue from bond issuance and taxation; meanwhile, fiscal authority has to pay for bonds that were issued in the last period and various public expenditures. Therefore, the fiscal authority’s budget constraint implies that:

where is public expenditure.

The fiscal authority targets public expenditures and taxes using the countercyclical policy rule:

where and denote the steady-state value of public expenditure and taxation. and are the persistence of public expenditure and taxation, respectively. Besides this, and denote the sensitive parameters of public expenditure policy response to the output gap and debt gap. Similarly, and denote the sensitive parameters of the tax policy response to the output and debt gaps. and are public expenditure shock and tax shock, and .

3.7. Market Clearing Condition

In equilibrium, the bond market, goods market, labor market, and capital market are all clear. The final goods market clearing condition is given as:

3.8. Inequality Index

Finally, for investigating the impacts of the COVID-19 pandemic on social inequality, we construct an inequality index by the wage income gap between Ricardian households and non- Ricardian households [35], which is given as:

4. Calibration and Bayesian Estimation

4.1. Calibration

We calibrated most of the static parameters in the model according to previous literature. Table 1 summarizes our baseline calibration values.

The Chinese government will take strict measures, such as the lockdown of cities, which have serious impacts on macroeconomic sustainability only when the number of confirmed cases reached a certain threshold. Therefore, we regard more than 500 new cases in mainland China on the same day as the typical manifestation of a large-scale outbreak of the pandemic in 2020, so we calibrate (the probability of an outbreak of COVID-19) as 0.0822. Moreover, we set the reduction rate of aggregated demand and the reduction rate of labor demand as 0.1413 and 0.2932 through statistical data from the 1st quarter of 2020, when the COVID-19 pandemic was most serious in China.

Lastly, we fixed the values of some fiscal variables to the statistical data of China. Based on the average ratio of fiscal expenditure to GDP between 2014 and 2018, we set . Similarly, according to the tax data during 2014 to 2018, the steady-state of the ratio of tax revenue to GDP is .

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Table 1.

Calibrated parameters.

| Parameters | Description | Value | Source |

|---|---|---|---|

| Discount factor | 0.98 | Zhang [36] | |

| External consumption habit of households | 0.61 | Zhang [36] | |

| Ratio of Ricardian households | 0.6 | Ferrara et al. [37] | |

| The reciprocal of Frisch labor supply elasticity | 2 | Liu et al. [38] | |

| Depreciation rate of private capital | 0.025 | Bekiros et al. [39] | |

| Investment adjustment cost | 1.728 | Auray et al. [40] | |

| Capital utilization parameters | 0.0048 | Bekiros et al. (2018) [39] | |

| Substitution elasticity between heterogeneity labors | 2 | Smets and Wouters [41] | |

| Wage stickiness | 0.5 | Smets and Wouters [41] | |

| Substitution elasticity between intermediate products | 6 | Xiao et al. [42] | |

| Price stickiness | 0.75 | Xiao et al. [42] | |

| Private capital share to output | 0.49 | Zhang and Zhang [43] | |

| The steady-state ratio of government debt to aggregate output | 0.44 | Jin and Xiong [44] |

4.2. Bayesian Estimation

We used the quarterly data of seven observable variables from China for the period 1996Q1 to 2020Q3 in the Bayesian estimation: real output, consumption, private investment, consumer price inflation, real government expenditure, and real tax revenue. The real output refers to GDP and was deflated by the inflation rate. For consumption, we used the total retail sales of consumer goods and converted them from a nominal value to a real value using the commodity retail price index. For private investment, we used investment in fixed assets in the private sector. Besides this, consumer price inflation refers to the CPI index in China. Real government expenditure and real tax revenue correspond to relevant official statistical data directly and were also deflated using the inflation rate. All the observable variables series were deseasoned, and the HP-filtered and cyclic components were chosen for the estimate. These data were obtained from the National Bureau of Statistics in China and the Wind database.

According to Eric [45], we set the prior means of monetary policy rule response parameter to the output gap and to inflation gap to 1.49 and 0.75, respectively. In addition, we chose the prior means of fiscal policy rule response parameters , , , and to be 0.5, 0.5, 0.2, and 0.2, which were in line with Bhattarai and Trzeciakiewicz [46]. Lastly, according to common methods in existing studies, the prior means of all persistent parameters in the model were set to 0.7.

Table 2 reports the prior distributions, means, and standard deviations of the estimated parameters, corresponding posterior means, and 90% intervals.

5. Results and Discussion

In this section, based on the NK-DSGE model, we firstly investigate the impact of the COVID-19 pandemic on various macroeconomic variables in China. Next, combined with debates in the existing literature, we simulate the changes in extreme values of macroeconomic variables with the variation in the feedback coefficient of monetary policy in response to policy targets when the macroeconomy is faced with a positive pandemic probability shock in aggregate demand (increase in the probability of COVID-19 pandemic and decrease in aggregate demand) and a positive pandemic probability shock in labor demand (increase in the probability of COVID-19 pandemic and decrease in labor demand). The last part explores how central banks choose appropriate policy targets in the long run, in order to alleviate welfare losses caused by COVID-19 pandemic shocks.

5.1. Impact of COVID-19 Pandemic on the Sustainability of the Macroeconomy

First, we simulate the impact of a 1% positive pandemic probability shock of aggregate demand and a 1% positive pandemic probability shock of labor demand on the sustainable development of the Chinese macroeconomy. The results are shown in Figure 1 and Figure 2. The period number is shown on the horizontal axis in both figures, while the vertical axis reflects the deviation degree of each macroeconomic variable from the steady-state level in the face of a pandemic probability shock.

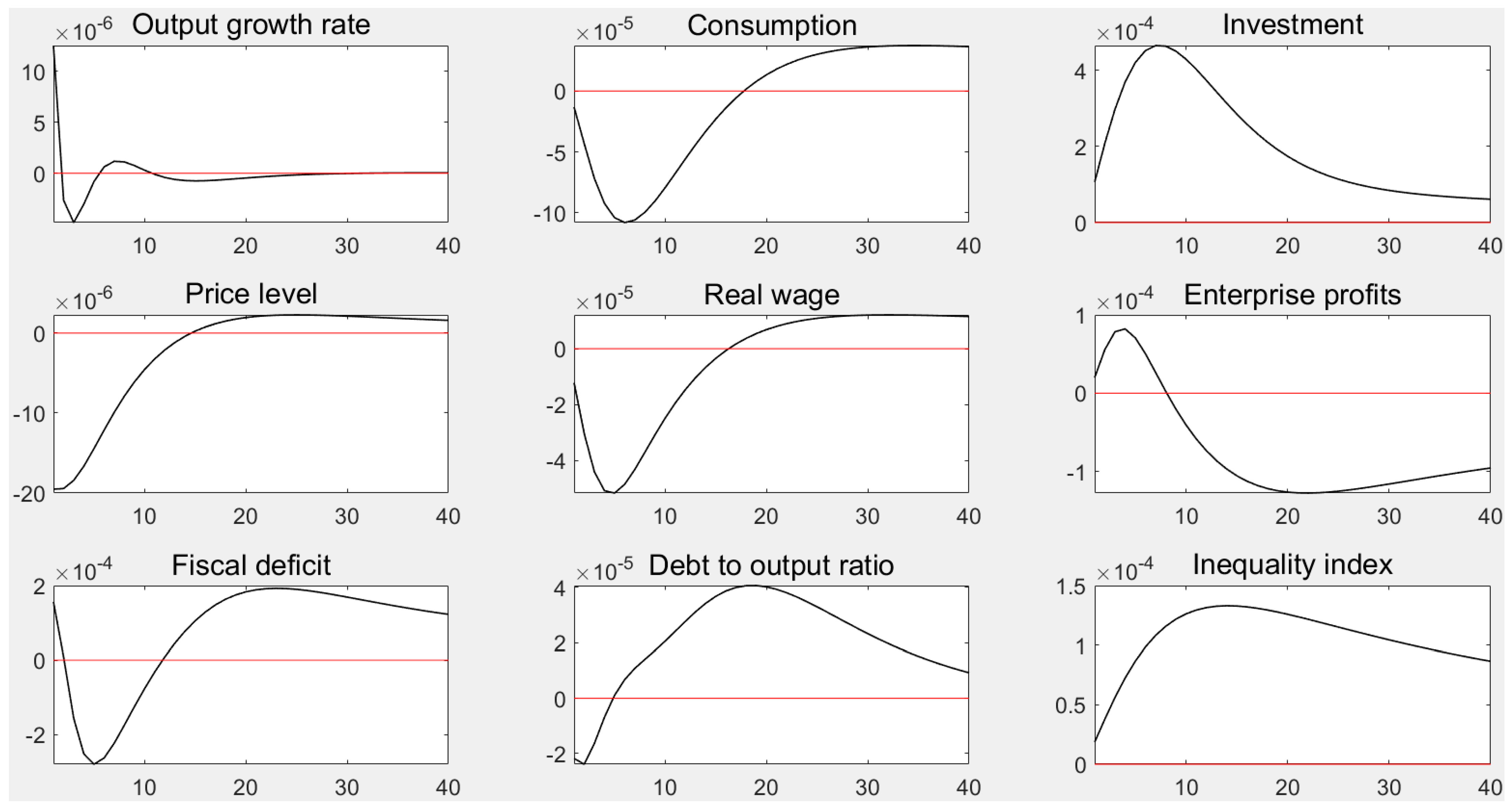

As can be seen from the simulation results in Figure 1, the positive pandemic probability shock of aggregate demand brings great challenges to the sustainable operation of the Chinese macroeconomy. There are some specific points: (1) in order to cope with the COVID-19 pandemic, China has widely taken prevention and control measures such as locking down entire cities. Affected by factors such as the closure of business places, the probability of disease impact led to a significant decline in consumption, and the consumption fell to the lowest point at the sixth period after the shock. At the same time, it should be noted that, after the 18th period, consumption will turn from negative to positive and be higher than the previous steady-state level, which means that with the gradual stabilization and effective control of the pandemic in China, compensatory consumption may rebound strongly. (2) According to the fiscal policy rules constructed in the model, both expenditure and tax react to the output gap. As a result, the government will increase public expenditure in response to the economic downturn caused by the pandemic. In addition, the decrease in consumption means a corresponding increase in savings, and savings will eventually be transformed into investment. Due to the superposition of these two factors, investment will increase. However, with the exit of the earlier stimulus policies, investment will decrease rapidly and gradually return to its steady-state level after the 10th period, indicating that the short-term increase in investment is not sustainable. (3) According to the clearing conditions of the product market, the joint effect of consumption and investment determines the variation trend of output growth rate. Therefore, when a pandemic probability shock of aggregate demand occurs, the output growth rate only increases briefly at the beginning of the policy stimulus and turns negative soon, which is also consistent with economic intuition. The contraction in aggregate demand caused by the COVID-19 pandemic will interrupt the continuous expansion of output. (4) Since the COVID-19 pandemic has weakened the sustainability of economic growth and exacerbated the malaise of consumption, the real wages of labor force and enterprise profits will also decline, especially enterprise profits, which will remain in a negative range for a long time. (5) Due to the decline of consumer demand, the price of production factors also drops, which leads to the decline in price level and deflation. (6) The contraction in aggregate demand caused by the COVID-19 pandemic not only worsens the above economic situation but also severely weakens fiscal sustainability. In Figure 1, on the one hand, in order to stimulate the macroeconomy, the government has to increase expenditure and reduce taxes in the long run, but on the other hand, due to the reduction in income sources of micro-economic subjects such as individuals and enterprises, the government’s tax revenue also decreases. The combined effect of the two leads to an expansion of fiscal deficit. According to the budget constraint identity of the financial sector, in order to make up for the deficit the government has to increase its debt, resulting in a significant increase in the debt to output ratio, which eventually increases the unsustainability of government debt and intensifies the probability of financial risk and systemic financial risk. (7) It is worth noting that the impact also causes an increase in the inequality index measured by the income gap of the two types of families. The pandemic has a more negative impact on non-Ricardian families, which are economically disadvantaged compared to the Ricardian families, thus aggravating the social polarization between the rich and the poor.

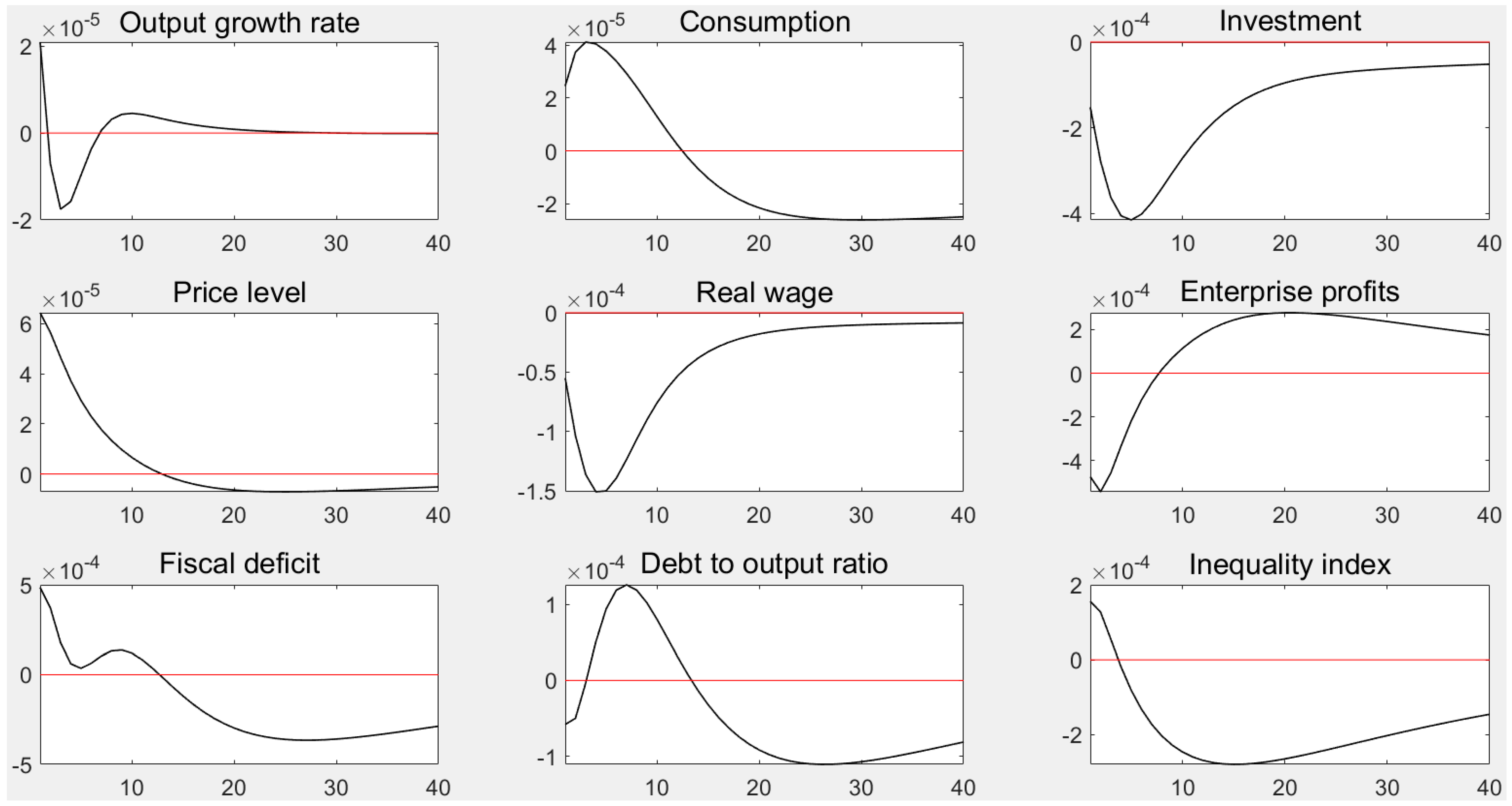

Next, in Figure 2 the pandemic probability shock of labor demand has also seriously affected the sustainable development of the Chinese macroeconomy. When comparing the values of the vertical axis, we can see that the decline in labor demand caused by the COVID-19 pandemic has a more prominent adverse impact on the macroeconomy. Similar to the pandemic probability shock of aggregate demand in Figure 1, the pandemic probability shock of labor demand also brings adverse effects, such as a decline in output growth rate, consumption, real wages, and enterprise profits, as well as an increase in fiscal deficit, debt-to-output ratio, and inequality; the mechanism is similar to the simulated situation in Figure 1. However, compared with the results in Figure 1, the impact of the pandemic probability shock of labor demand on some macroeconomic variables is also slightly different. Firstly, the pandemic probability shock of labor demand leads to a significant decrease in investment rather than an increase, as shown in Figure 1. The reason for this is that the contraction of labor demand leads to a sharp increase in unemployment, resulting in a decrease in the income of the household and enterprise sectors, thus inhibiting the investment willingness and investment ability of the private sector. Secondly, unlike the deflation caused by the pandemic probability shock of aggregate demand, the pandemic probability shock of labor demand leads to a rise in price level and inflation. Thirdly, the impact of the shock on the inequality index was weaker than that of the pandemic probability shock of aggregate demand, but it also led to an increase in inequality at the beginning. However, after the fifth period the sharp rebound of real wage level is beneficial for non-Ricardian families who mainly rely on labor, which leads to a reduction in inequality in the later period.

5.2. Choice of Monetary Policy Targets and Sustainability of Macroeconomic

Based on the simulation of the impact of two pandemic probability shocks on macroeconomic sustainability above, this part mainly investigates how to choose monetary policy targets in order to reduce the adverse impact of the COVID-19 pandemic on the economy. In Figure 3 and Figure 4, the solid line and the dashed line, respectively, simulate the variation trend of the impact of extreme values of the COVID-19 pandemic shock on various macroeconomic variables when the response coefficients of monetary policy to the two main goals of price stability and economic growth increase from zero to sic, respectively.

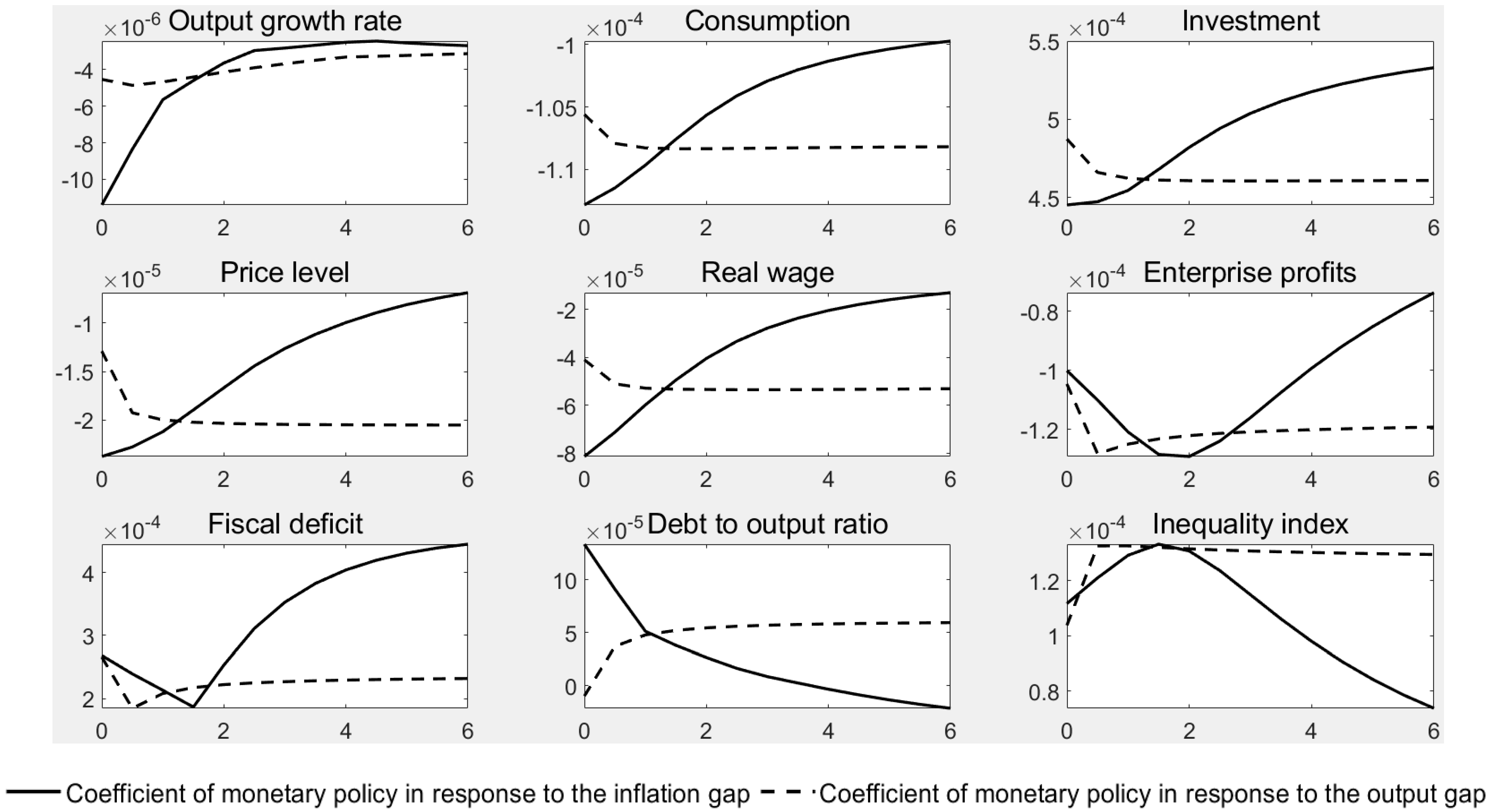

Based on the results of Figure 1 and Figure 3 simulates the changing trend of minimum values of output growth rate, consumption, price level, real wage, and enterprise profiles and maximum values of investment, fiscal deficit, debt to output ratio, and inequality index when the feedback coefficient of monetary policy objectives changes. As can be seen from the solid line in Figure 1, when faced with the pandemic probability shock of aggregate demand, a monetary policy focusing on price stability is more conducive to ensuring the sustainable operation of the Chinese macroeconomy. Specifically, as the monetary policy pays more attention to the inflation gap, the minimum values of output growth rate, consumption, and enterprise profits all increase significantly, indicating that a monetary policy that pays more attention to price stability is helpful to alleviate the downward pressure on the economy caused by the COVID-19 pandemic and restrain the decline in the profitability of enterprises. As far as the sustainability of government debt goes, a monetary policy that pays more attention to price stability leads to an expansion of fiscal deficit. However, its positive effect on promoting economic recovery is more than the negative effect of debt expansion, and the combined effect of the two leads to a significant downward trend of debt output ratio, which enhances the sustainability of government debt. Finally, the change in the monetary policy’s feedback coefficient on the inflation gap shows an inverted U-shaped relationship with the inequality index. When the feedback coefficient is less than two, a monetary policy focusing more on price stability will exacerbate the gap between the rich and the poor, and when the response coefficient further increases the monetary policy will restrain the rise in inequality. Compared with the above results, with the increase in the response coefficient of monetary policy to the output gap, the effect of promoting economic sustainability is only reflected in a reduction in fiscal deficit and a reduction in inequality and other specific areas, and the effect of the overall policy is less than that of a monetary policy that pays more attention to price stability in the case of the pandemic probability shock of aggregate demand.

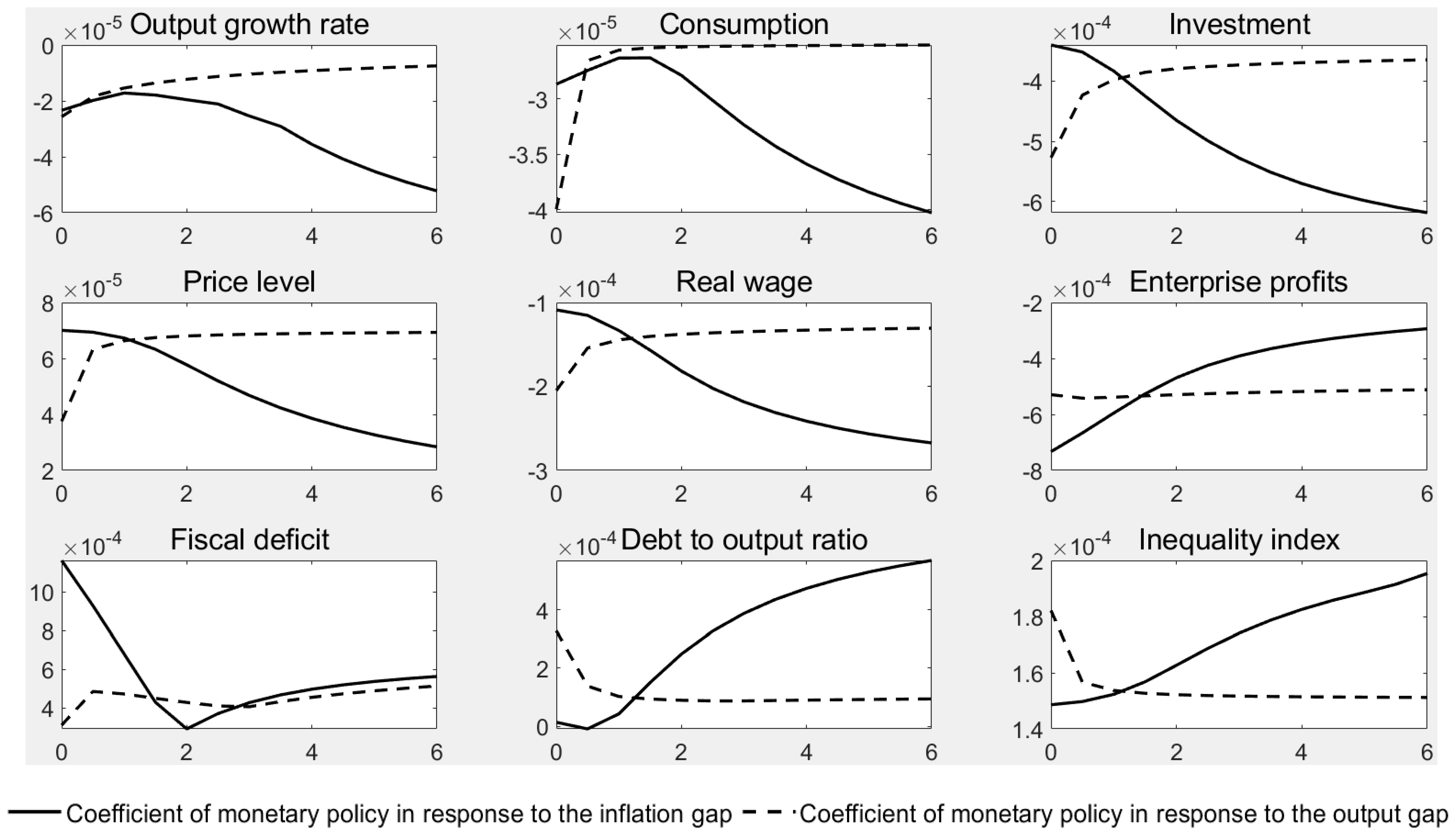

Figure 4 investigates the correlation between the choice of monetary policy target and sustainable economic growth when faced with the pandemic probability shock of labor demand. However, a monetary policy that pays more attention to the goal of economic growth plays a better role in ensuring the sustainable operation of the macroeconomy, which is different from the conclusion in Figure 3. Specifically, with the increase in the response coefficient of monetary policy to the output gap, the minimum values of output growth rate, consumption, and investment all increase significantly, indicating that the monetary policy has alleviated the adverse impact of the decline in labor demand caused by the COVID-19 pandemic on the sustainable operation of the macroeconomy. In addition, a monetary policy that pays more attention to the output gap not only promotes the recovery of output, but also brings about a decline in the debt to output ratio, thus increasing the sustainability of government debt. In view of the fact that economically weaker non-Ricardian households are more vulnerable to unemployment caused by a decline in labor demand and the increase in monetary policy’s response coefficient to the output gap promotes economic recovery and employment, the policy also significantly reduces income inequality among different income groups. Although the effect of a monetary policy focusing on economic growth goals is overall positive, there are also limitations. Firstly, the regulation effect of the policy on real wages is weak. At the same time, it further aggravates deflation and weakens the profitability of enterprises. Secondly, only when the response coefficient of monetary policy to the output gap is less than one, the monetary policy can exert a significant regulatory effect on the macroeconomy. However, with the further increase in the response coefficient, the policy effect shows a marginal decreasing trend, which indicates that the space for future policy is limited.

5.3. Choice of Monetary Policy Targets and Long-Term Welfare Loss

In Section 5.2, this paper mainly investigates the cases where the COVID-19 pandemic has adverse effects on aggregate demand and labor demand separately. However, the COVID-19 pandemic often has a huge impact on both in many practical cases, and the impact of the COVID-19 pandemic and monetary policy regulation on different economic subjects is often heterogeneous. Based on the approach of Gali and Monacelli [47] and Prasad and Zhang [48], this paper constructs the long-term welfare loss function of Ricardian and non-Ricardian families from a broader and longer-term perspective to investigate the choice of monetary policy target when the COVID-19 pandemic acts on aggregate demand and labor demand. According to the utility functions of the two types of household sectors, the total social welfare loss functions obtained by the Ricardian family, non-Ricardian family, and the weighted average of the two are set as follows:

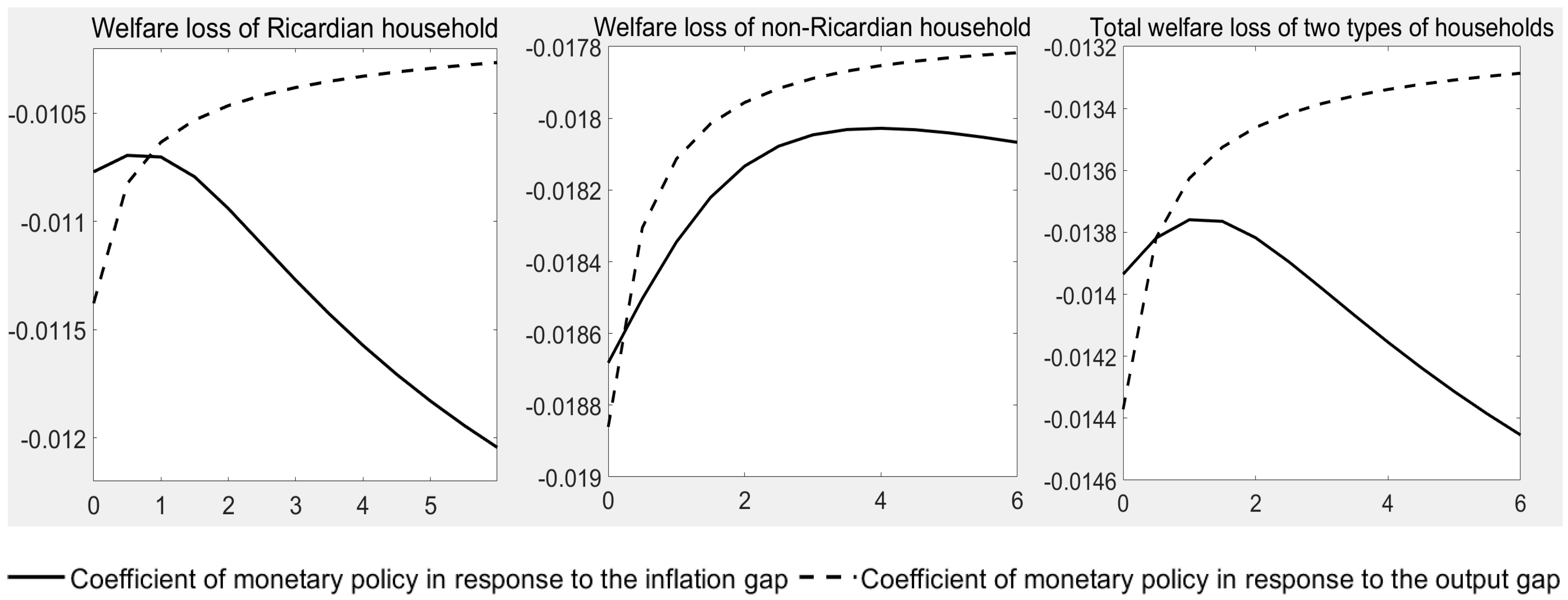

In Figure 5, the solid line and the dashed line simulate the change in the welfare loss caused by the COVID-19 pandemic when the monetary policy changes the response coefficient of the inflation gap and the output gap from zero to six, respectively. First of all, by comparing the values on the vertical axis in the figure, it can be seen that the welfare loss caused by the COVID-19 pandemic on the economically weaker non-Ricardian families is greater than the welfare loss caused to the Ricardian families, which also confirms the necessity of the above investigation of income inequality. Existing studies also provide theoretical support for this phenomenon. Sydenstricker [49] and Mamelund [50] found that public health events would exert different effects on groups with different economic and social status based on the study of the 1918 pandemic. Moreover, economically vulnerable groups will suffer higher infection rates and mortality in the pandemic. Arthi and Parman [51] also reached similar conclusions in their study on the COVID-19 pandemic. Bargain and Aminjonov [52] observed the situation of Africa and Latin America during the COVID-19 period and pointed out that the poor save little and work in informal employment. Therefore, the blockade measures caused by the COVID-19 would make this group fall into extreme poverty. As far as Ricardian families are concerned, with the increase in the response parameter of monetary policy to the output gap, the welfare loss is reduced obviously, but with an increase in the response parameter of monetary policy to inflation gap the welfare loss increases. For non-Ricardian families, the increase in monetary policy’s attention to the inflation gap and output gap is beneficial to reduce the welfare loss caused by the COVID-19 pandemic. By contrast, a monetary policy that pays more attention to the economic growth target still has a better effect on reducing the welfare loss. The right figure in Figure 5 depicts the impact of monetary policy target choice on the whole social welfare loss. The conclusion is similar to the situation of non-Ricardian families—that is, only focusing more on the economic growth target can monetary policy significantly reduce the loss of welfare at this time. Therefore, monetary policy should pay more attention to economic growth targets in the long run, thereby ensuring sustainable social welfare when the COVID-19 pandemic has a significant adverse impact on both aggregate demand and labor demand. This result is roughly in line with that of other papers that argue for abandoning the containment policy, stating that stimulating output expansion too early ultimately leads to a decline in social welfare [53].

6. Conclusions and Policy Recommendations

Based on the reality of Chinese macroeconomic operation, we constructed a NK-DSGE model and simulated the negative impact of the COVID-19 pandemic on the macroeconomy. Then, the choice of monetary policy to promote sustainable economic growth was discussed. The conclusions are as follows: (1) the outbreak of the COVID-19 pandemic led to a decline in the aggregate demand and labor demand that both brought serious challenges to Chinese macroeconomic sustainable operation, causing superficial problems including a fall in the economic growth rate, consumption shrinkage, and declines in real wages and corporate profits. The COVID-19 pandemic increased the fiscal deficit, weakened the sustainability of government debt, and increased social inequality to a certain extent as well. (2) When the adverse impact of the COVID-19 pandemic on the macroeconomy is mainly reflected in a decline in aggregate demand, monetary policy should pay more attention to the target of price stability, thereby promoting economic recovery, ensuring the sustainability of government debt, and narrowing social inequalities. (3) When the adverse impact of the COVID-19 pandemic is mainly reflected in a decline in labor demand, a monetary policy that focuses more on the target of economic growth has a better effect. However, with the increase in the output gap, monetary policy also faces the limitation of diminishing marginal effect. (4) When the COVID-19 pandemic has a significant impact on aggregate demand and labor demand, a monetary policy that focuses more on the target of economic growth has a significant effect on mitigating the welfare losses of both two kinds of heterogeneous families and aggregate social welfare losses, while a monetary policy that pays more attention to price stability can only mitigate the welfare loss of non-Ricardian families. Therefore, monetary policy should focus more on the economic growth target in the long run when facing the COVID-19 pandemic.

According to the above results and conclusions, we put forward the following policy recommendations in order to provide a useful reference for policy practice.

- (1)

- China, as well as other countries around the world, should maintain sufficient vigilance against the adverse impacts of the COVID-19 pandemic on the sustainable operation of the macroeconomy. In particular, the unemployment caused by the COVID-19 pandemic should be paid more attention to, and positive measures should be taken accordingly.

- (2)

- When the negative impacts of the COVID-19 pandemic are mainly reflected in a contraction in aggregated demand, monetary policy should be devoted to keeping the currency value stable, with the careful implementation of quantitative easing, zero interest rates, and unconventional monetary policy to avoid devaluation caused by the excessive issuance of currency, maintain the real purchasing power of household wages, and promote consumption to offset the impact on aggregate demand.

- (3)

- When the adverse impacts of the COVID-19 pandemic are mainly reflected in a decline of labor demand, monetary policy should turn to focus on the target of economic growth. Governments should ensure a certain economic growth rate to increase social employment, alleviate unemployment problems, and ensure the sustainability of economic development by increasing the utilization rate of labor elements.

- (4)

- When the COVID-19 pandemic poses a major threat to both the aggregated demand and labor demand, the central bank should use economic growth as its long-term policy target when deciding monetary policy. The recovery of household consumption and employment rely on sustainable economic growth and reduce social welfare loss. In addition, since non-Ricardian families suffer more from welfare loss during the COVID-19 pandemic, central banks should give more consideration to the appeals of the economically disadvantaged while choosing monetary policy targets and strive to reduce inequality.

- (5)

- The research of this paper is of great significance to other countries in the world as well. For developing countries in Africa and Latin America, which were severely affected by the pandemic, the unemployment caused by the COVID-19 pandemic should be controlled to a minimum, and the rising unemployment rate should prevent the economically disadvantaged from falling into extreme poverty and further aggravating social inequality. For developed countries, the unconventional monetary policies such as quantitative easing, zero interest rate and negative interest rate, which aim at promoting economic growth, can effectively alleviate the unemployment and economic recession brought by the COVID-19 pandemic. However, we should not ignore the financial risks that these policies may lead to in the long term and its spillover effect to other countries.

Since this study is mainly based on Chinese practice in the monetary policy, only the choice of price monetary policy under the impact of the COVID-19 pandemic is investigated. However, in order to cope with the deep economic recession caused by the pandemic, many countries have adopted unconventional monetary policy tools such as quantitative easing, which not only stimulate economic growth and employment, but also bring significant inflation pressure and lead to currency devaluation. In this regard, the relevant theories of Austrian economics can provide ideas for the analysis of the adverse consequences of expansionary monetary policy. Mises [54] pointed out that expansionary monetary policy would distort the redistribution of income and wealth but would not bring a general increase in living standards. Specifically, expansionary monetary policy is beneficial to those who receive the new currency first, while the fixed income group who receive the new currency later or not will suffer losses, resulting in permanent changes in the structure of income, wealth, and demand. In addition, Huerta de Soto [55], based on the Austrian business cycle theory developed by Mises [54,56], Hayek [57], and Rothbard [58] criticized the expansionary monetary policy implemented based on Keynesian ideas, arguing that the credit expansion would lead to the imbalance between investment and savings, and the voluntary savings level would be insufficient to sustain the new investment projects financed by credit expansion. Similarly, Albinowski [59] and Mulligan [60] suggested that credit growth reduces the share of savings in total deposits, causing an investment boom and unsustainable business expansion. Hence, based on related theories of Austrian economics, Hoffmann et al. [61], Keeler [62], and Newman [63] pointed out that overly expansionary monetary policies can cause various adverse consequences, such as overinvestment cycles, distortions in the economic structure, disturbing relative prices, and an unsustainable credit boom. Further, Bagus [64] studied the situation after the financial crisis in 2008 and pointed out that the zero interest rate policy would lead to the institutionalization of the real negative interest rate, thus causing a moral hazard, stimulating the development of a bubble economy, and damaging the stability of the financial system, while withdrawing from zero interest rate policy would be politically costly.

Apart from debates on expansionary monetary policy, the effect of the classical Taylor rule has also been doubted. Machaj [65] studied a 2001–2008 real estate bubble and argued that we cannot avoid the macroeconomic bubble simply following the Taylor rule, because the Taylor rule has many variants, lacks the precise definition, and it is not in line with the coordination of the market economy. Hence, the Taylor rule is imperfect for monetary policy practice.

Therefore, in future research, we can pay more attention to the target selection of unconventional monetary policies represented by quantitative easing, zero interest rates, and negative interest rates in the face of the COVID-19 pandemic, that is, how the unconventional monetary policies should balance the maintenance of currency stability and economic recovery. In terms of the model framework, future studies can further extend the model to the open economy environment, so as to explore the spillover effects of the unconventional monetary policies launched by European and American countries after the COVID-19 pandemic on the monetary policies of other countries. In addition, we can try to introduce more methods of monetary policy adjustment to the model except for the classical Taylor rule. Lastly, including commercial banks and other financial sectors in the model framework, and then investigating the transmission channel of monetary policy through the financial sector is also a direction worth expanding in future research in this field.

Author Contributions

X.Z., conceptualization, methodology, formal analysis, investigation, data collection, writing—original draft preparation. Y.Z. (Yimeng Zhang), validation, formal analysis, writing—review and editing. Y.Z. (Yunchan Zhu), conceptualization, methodology, writing—review and editing, supervision. All authors have read and agreed to the published version of the manuscript.

Funding

This research was financially supported by the National Natural Science Foundation of China, grant number 71573194, and the National Social Science Fund of China, grant number 15ZDB158.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

Publicly available datasets were analyzed in this study. These data were obtained from the National Bureau of Statistics in China (http://www.stats.gov.cn/) and the Wind database (https://www.wind.com.cn/NewSite/edb.html).

Conflicts of Interest

The authors declare no conflict of interest.

References

- Guo, Y.M.; Shi, Y.R. Impact of the VAT reduction policy on local fiscal pressure in China in light of the COVID-19 pandemic: A measurement based on a computable general equilibrium model. Econ. Anal. Policy 2021, 69, 253–264. [Google Scholar] [CrossRef]

- Fokas, A.S.; Cuevas-Maraver, J.; Kevrekidis, P.G. A quantitative framework for exploring exit strategies from the COVID-19 lockdown. Chaos Solitons Fractals 2020, 140, 110244. [Google Scholar] [CrossRef] [PubMed]

- Altig, D.; Baker, S.; Barrero, J.M.; Bloom, N.; Bunn, P.; Chen, S.; Davis, S.J.; Leather, J.; Meyer, B.; Mihaylov, E.; et al. Economic uncertainty before and during the COVID-19 pandemic. J. Public Econ. 2020, 191, 104291. [Google Scholar] [CrossRef] [PubMed]

- Wielen, W.; Barrios, S. Economic sentiment during the COVID pandemic: Evidence from search behaviour in the EU. J. Econ. Bus. 2020. [Google Scholar] [CrossRef]

- Bhar, R.; Malliaris, A.G. Modeling U.S. monetary policy during the global financial crisis and lessons for Covid-19. J. Policy Model. 2020, in press. [Google Scholar] [CrossRef]

- Chen, H.C.; Yeh, C.W. Global financial crisis and COVID-19: Industrial reactions. Financ. Res. Lett. 2021, in press. [Google Scholar] [CrossRef]

- Kim, O.S.; Parker, J.A.; Schoar, A. Revenue Collapses and the Consumption of Small Business Owners in the Early Stages of the COVID-19 Pandemic. NBER Working Paper 2020, No. 28151. Available online: http://www.nber.org/papers/w28151.pdf (accessed on 11 November 2020).

- Baker, S.R.; Farrokhnia, R.A.; Meyer, S.; Pagel, M.; Yannelis, C. How Does Household Spending Respond to an Epidemic? Consumption during the 2020 COVID-19 Pandemic. NBER Working Paper 2020, No. 26949. Available online: http://www.nber.org/papers/w26949.pdf (accessed on 20 November 2020).

- Balla-Elliott, D.; Cullen, Z.B.; Glaeser, E.L.; Luca, M.; Stanton, C.T. Business Reopening Decisions and Demand Forecasts during the COVID-19 Pandemic. NBER Working Paper 2020, No. 27362. Available online: http://www.nber.org/papers/w27362.pdf (accessed on 20 November 2020).

- Fang, H.; Ge, C.; Huang, H.; Li, H. Labor Demand: Evidence from 100 Million Posted Jobs in China. NBER Working Paper 2020, No. 28072. Available online: http://www.nber.org/papers/w28072.pdf (accessed on 4 December 2020).

- Brada, J.C.; Gajewski, P.; Kutan, A.M. Economic resiliency and recovery, lessons from the financial crisis for the COVID-19 pandemic: A regional perspective from Central and Eastern Europe. Int. Rev. Financ. Anal. 2021, in press. [Google Scholar] [CrossRef]

- Goswami, B.; Mandal, R.; Nath, H.K. Covid-19 pandemic and economic performances of the states in India. Econ. Anal. Policy 2021, 69, 461–479. [Google Scholar] [CrossRef]

- Goswami Luo, R.; Liu, C.; Gao, J.; Wang, T.; Zhi, H.; Shi, P.; Huang, J. Impacts of the COVID-19 pandemic on rural poverty and policy responses in China. J. Integr. Agric. 2020, 19, 2946–2964. [Google Scholar] [CrossRef]

- Tian, W. How China managed the COVID-19 pandemic. Asian Econ. Pap. 2021, 20, 101–134. [Google Scholar] [CrossRef]

- Sahoo, P.; Ashwani. COVID-19 and Indian economy: Impact on growth, manufacturing, trade and MSME sector. Glob. Bus. Rev. 2020, 21, 1159–1183. [Google Scholar] [CrossRef]

- Achim, M.V.; Văidean, V.L.; Borlea, S.N.; Florescu, D.R. The Lesson of COVID-19 Pandemic for Democracy Within Cultural context (17 April 2020). Available online: https://ssrn.com/abstract=3646503 (accessed on 10 March 2021). [CrossRef]

- Choi, S.Y. Industry volatility and economic uncertainty due to the COVID-19 pandemic: Evidence from wavelet coherence analysis. Financ. Res. Lett. 2020, 37, 101783. [Google Scholar] [CrossRef]

- Mishra, A.K.; Rath, B.N.; Dash, A.K. Does the Indian financial market nosedive because of the COVID-19 outbreak, in comparison to after demonetisation and the GST? Emerg. Mark. Financ. Trade 2020, 56, 2162–2180. [Google Scholar] [CrossRef]

- Bakas, D.; Triantafyllou, A. Commodity price volatility and the economic uncertainty of pandemics. Econ. Lett. 2020, 193, 109283. [Google Scholar] [CrossRef]

- Bloom, N.; Bunn, P.; Mizen, P.; Smietanka, P.; Thwaites, G. The Impact of Covid-19 on Productivity. NBER Working Paper 2020, No. 28233. Available online: http://www.nber.org/papers/w28233.pdf (accessed on 20 November 2020).

- Caballero, R.J.; Simsek, A. A Model of Asset Price Spirals and Aggregate Demand Amplification of A “COVID-19” Shock. NBER Working Paper 2020, No. 27044. Available online: http://www.nber.org/papers/w27044.pdf (accessed on 2 December 2020).

- Taylor, J.B. Discretion versus policy rules in practice. Carnegie Rochester Conf. Ser. Public Policy 1993, 39, 195–224. [Google Scholar] [CrossRef]

- Reschreiter, A. The effects of the monetary policy regime shift to inflation targeting on the real interest rate in the United Kingdom. Econ. Model. 2011, 28, 754–759. [Google Scholar] [CrossRef]

- Chadha, J.S.; Sarno, L.; Valente, G. Monetary policy rules, asset prices, and exchange rates. Imf Staff Pap. 2004, 51, 529–552. Available online: https://0-www-jstor-org.brum.beds.ac.uk/stable/30035961 (accessed on 10 December 2020).

- Nair, A.R.; Anand, B. Monetary policy and financial stability: Should central bank lean against the wind? Cent. Bank Rev. 2020, 20, 133–142. [Google Scholar] [CrossRef]

- Liu, D.; Zhang, Y.; Sun, W. Commitment or discretion? An empirical investigation of monetary policy preferences in China. Econ. Model. 2020, 85, 409–419. [Google Scholar] [CrossRef]

- Zhu, S.; Kavanagh, E.; O’Sullivan, N. Inflation targeting and financial conditions: UK monetary policy during the great moderation and financial crisis. J. Financ. Stab. 2021, 53. [Google Scholar] [CrossRef]

- Hossain, A.A.; Arwatchanakarn, P. Does money have a role in monetary policy for price stability under inflation targeting in Thailand? J. Asian Econ. 2017, 53, 37–55. [Google Scholar] [CrossRef]

- Sánchez, M. Inflation uncertainty and unemployment uncertainty: Why transparency about monetary policy targets matters. Econ. Lett. 2012, 117, 119–122. [Google Scholar] [CrossRef]

- Gourio, F. Disaster Risk and Business Cycles. Am. Econ. Rev. 2012, 102, 2734–2766. [Google Scholar] [CrossRef] [Green Version]

- Isoré, M.; Szczerbowicz, U. Disaster risk and preference shifts in a New Keynesian model. J. Econ. Dyn. Control. 2017, 79, 97–125. [Google Scholar] [CrossRef] [Green Version]

- Calvo, G.A. Staggered prices in a utility maximizing framework. J. Monet. Econ. 1983, 12, 383–398. [Google Scholar] [CrossRef]

- Dixit, A.K.; Stiglitz, J.E. Monopolistic competition and optimum product diversity. Am. Econ. Rev. 1977, 67, 297–308. Available online: https://0-www-jstor-org.brum.beds.ac.uk/stable/1831401 (accessed on 20 December 2020).

- Sargent, T.J.; Surico, P. Two illustrations of the quantity theory of money: Breakdowns and revivals. Am. Econ. Rev. 2011, 101, 109–128. [Google Scholar] [CrossRef] [Green Version]

- Auclert, A.; Rognlie, M. Inequality and Aggregate Demand. NBER Working Paper 2018, No. 24280. Available online: https://www.nber.org/papers/w24280.pdf (accessed on 7 November 2020).

- Zhang, W. China’s monetary policy: Quantity versus price rules. J. Monetary Econ. 2009, 31, 473–484. [Google Scholar] [CrossRef]

- Fernández-Villaverde, J.; Levintal, O. Solution Methods for Models with Rare Disasters. NBER Working Paper 2020, No. 21997. Available online: http://www.nber.org/papers/w21997.pdf (accessed on 2 December 2020).

- Liu, Z.; Spiegel, M.M.; Zhang, J. Optimal capital account liberalization in China. J. Monet. Econ. 2020, 20. in press. [Google Scholar] [CrossRef]

- Bekiros, S.; Nilavongse, R.; Uddin, G.S. Bank capital shocks and countercyclical requirements: Implications for banking stability and welfare. J. Econ. Dyn. Control. 2018, 93, 315–331. [Google Scholar] [CrossRef]

- Auray, S.; Eyquem, A.; Ma, X. Banks, sovereign risk and unconventional monetary policies. Eur. Econ. Rev. 2018, 108, 153–171. [Google Scholar] [CrossRef] [Green Version]

- Smets, F.; Wouters, R. Shocks and frictions in US business cycles: A Bayesian DSGE approach. Am. Econ. Rev. 2007, 97, 586–606. [Google Scholar] [CrossRef] [Green Version]

- Xiao, B.; Fan, Y.; Guo, X. Exploring the macroeconomic fluctuations under different environmental policies in China: A DSGE approach. Energy Econ. 2018, 76, 439–456. [Google Scholar] [CrossRef]

- Zhang, J.; Zhang, Y. Examining the economic and environmental effects of emissions policies in China: A Bayesian DSGE model. J. Clean Prod. 2020, 266, 122026. [Google Scholar] [CrossRef]

- Jin, H.; Xiong, C. Fiscal stress and monetary policy stance in oil-exporting countries. J. Int. Money Financ. 2021, 111, 102302. [Google Scholar] [CrossRef]

- Eric, C.Y.N. Housing market dynamics in China: Findings from an estimated DSGE model. J. Hous. Econ. 2015, 29, 26–40. [Google Scholar] [CrossRef]

- Bhattarai, K.; Trzeciakiewicz, D. Macroeconomic impacts of fiscal policy shocks in the UK: A DSGE analysis. Econ. Model. 2017, 61, 321–338. [Google Scholar] [CrossRef] [Green Version]

- Gali, J.; Monacelli, T. Monetary policy and exchange rate volatility in a small open economy. Rev. Econ. Stud. 2005, 72, 707–734. [Google Scholar] [CrossRef]

- Prasad, E.; Zhang, B. Distributional Effects of Monetary Policy in Emerging Market Economies. NBER Working Paper 2015, No. 21471. Available online: https://www.nber.org/system/files/working_papers/w21471/w21471.pdf (accessed on 20 December 2020).

- Sydenstricker, E. The incidence of iInfluenza among persons of different economic status during the epidemic of 1918. Public Health Rep. 1931, 46, 154–170. [Google Scholar] [CrossRef]

- Mamelund, S.E. 1918 pandemic morbidity: The first wave hits the poor, the second wave hits the rich. Influenza Other Respir. Viruses 2018, 12, 307–313. [Google Scholar] [CrossRef] [Green Version]

- Arthi, V.; Parman, J. Disease, downturns, and wellbeing: Economic history and the long-run impacts of COVID-19. Explor. Econ. Hist. 2021, 79, 101381. [Google Scholar] [CrossRef]

- Bargain, O.; Aminjonov, U. Poverty and COVID-19 in Africa and Latin America. World Dev. 2021, 142, 105422. [Google Scholar] [CrossRef]

- Zhao, B. COVID-19 pandemic, health risks, and economic consequences: Evidence from China. China Econ. Rev. 2020, 64, 101561. [Google Scholar] [CrossRef]

- Mises, L.V. The Theory of Money and Credit; The Foundation for Economic Education, Inc.: New York, NY, USA, 1971. [Google Scholar]

- Huerta de Soto, J.H.D. Money, Bank Credit and Economic Cycles, 3rd ed.; Unión Editorial Press: Madrid, Spain, 2006. [Google Scholar]

- Mises, L.V. Human Action: A Treatise on Economics, 4th ed.; The Foundation for Economic Education, Inc.: New York, NY, USA, 1996. [Google Scholar]

- Hayek, F.A. Prices and Production; George Routledge & Sons: London, UK, 1931. [Google Scholar]

- Rothbard, M.N. Man, Economy and State with Power and Market, 2nd ed.; Ludwig von Mises Institute: Auburn, AL, USA, 2004. [Google Scholar]

- Albinowski, M. The role of fractional-reserve banking in amplifying credit booms: Evidence from panel data. Rev. Austrian Econ. 2020. [Google Scholar] [CrossRef] [Green Version]

- Mulligan, R.F. Accounting for the business cycle: Nominal rigidities, factor heterogeneity, and Austrian capital theory. Rev. Austrian Econ. 2006, 19, 311–336. [Google Scholar] [CrossRef]

- Hoffmann, A.; Schnabl, G. Monetary nationalism and international economic instability. Q. J. Austrian Econ. 2013, 16, 135–164. [Google Scholar] [CrossRef]

- Keeler, J.P. Empirical Evidence on the Austrian Business Cycle Theory. Rev. Austrian Econ. 2001, 14, 331–351. [Google Scholar] [CrossRef]

- Newman, P. The depression of 1920–1921: A credit induced boom and a market based recovery? Rev. Austrian Econ. 2016, 29, 387–414. [Google Scholar] [CrossRef]

- Bagus, P. The ZIRP trap—the institutionalization of negative real interest rates. Procesos Merc. Rev. Eur. Econ. Política 2015, 12, 105–163. Available online: http://www.philippbagus.de/wp-content/uploads/2015/05/ZIRP-TRAP-PROCESOS-DE-MERCADO-04-Art%C3%ADculo-Bagus-2.pdf (accessed on 12 March 2021).

- Machaj, J. Can the Taylor rule be a good guidance for policy? the case of 2001-2008 real estate bubble. Prague Econ. Pap. 2016, 25, 381–395. [Google Scholar] [CrossRef]

Figure 1.

Effect of a 1% increase in the probability of a COVID-19 pandemic: impulse response of macroeconomic variables to aggregate demand decline.

Figure 1.

Effect of a 1% increase in the probability of a COVID-19 pandemic: impulse response of macroeconomic variables to aggregate demand decline.

Figure 2.

Effect of a 1% increase in the probability of a COVID-19 pandemic: impulse response of macroeconomic variables to labor demand decline.

Figure 2.

Effect of a 1% increase in the probability of a COVID-19 pandemic: impulse response of macroeconomic variables to labor demand decline.

Figure 3.

Impulse response of macroeconomic variables to a 1% increase in the probability of COVID-19 pandemic shock in aggregate demand when the response parameters of monetary policy change from zero to six. Note: solid lines: response parameters of monetary policy change with inflation gap; dotted lines: response parameters of monetary policy change with output gap.

Figure 3.

Impulse response of macroeconomic variables to a 1% increase in the probability of COVID-19 pandemic shock in aggregate demand when the response parameters of monetary policy change from zero to six. Note: solid lines: response parameters of monetary policy change with inflation gap; dotted lines: response parameters of monetary policy change with output gap.

Figure 4.

Impulse response of macroeconomic variables to a 1% increase in the probability of COVID-19 pandemic shock in labor demand when the response parameters of monetary policy change from zero to six. Note: solid lines: response parameters of monetary policy change with inflation gap; dotted lines: response parameters of monetary policy change with output gap.

Figure 4.

Impulse response of macroeconomic variables to a 1% increase in the probability of COVID-19 pandemic shock in labor demand when the response parameters of monetary policy change from zero to six. Note: solid lines: response parameters of monetary policy change with inflation gap; dotted lines: response parameters of monetary policy change with output gap.

Figure 5.

Welfare loss to a 1% increase in the probability of COVID-19 pandemic shock which affects aggregate demand and labor demand simultaneously when the response parameters of monetary policy change from zero to six. Note: solid lines: response parameters of monetary policy change with inflation gap; dotted lines: response parameters of monetary policy change with output gap.

Figure 5.

Welfare loss to a 1% increase in the probability of COVID-19 pandemic shock which affects aggregate demand and labor demand simultaneously when the response parameters of monetary policy change from zero to six. Note: solid lines: response parameters of monetary policy change with inflation gap; dotted lines: response parameters of monetary policy change with output gap.

Table 2.

Bayesian estimated parameters.

| Parameters | Description | Prior Dist. | Posterior Mean | 90% Interval |

|---|---|---|---|---|

| Persistence of total factor productivity | B(0.7, 0.1) | 0.6286 | [0.6140, 0.6425] | |

| Persistence of aggregated demand | B(0.7, 0.1) | 0.8128 | [0.7918, 0.8288] | |

| Persistence of labor demand | B(0.7, 0.1) | 0.5691 | [0.5504, 0.5873] | |

| Persistence of pandemic probability shock in aggregated demand | B(0.7, 0.1) | 0.7251 | [0.7048, 0.7421] | |

| Persistence of pandemic probability shock in labor demand | B(0.7, 0.1) | 0.8175 | [0.7947, 0.8395] | |

| Persistence of policy rate | B(0.7, 0.1) | 0.6630 | [0.6408, 0.6950] | |

| Monetary policy rule coefficient for inflation gap | G(1.49, 0.2) | 1.3846 | [1.3728, 1.3997] | |

| Monetary policy rule coefficient for output gap | G(0.75, 0.2) | 0.6153 | [0.6033, 0.6271] | |

| Fiscal expenditure rule coefficient for output gap | G(0.5, 0.2) | 0.6607 | [0.6292, 0.6967] | |

| Fiscal expenditure rule coefficient for debt gap | G(0.2, 0.2) | 0.1988 | [0.1804, 0.2187] | |

| Tax rule coefficient for output gap | G(0.5, 0.2) | 0.4584 | [0.4000, 0.4981] | |

| Tax rule coefficient for debt gap | G(0.2, 0.2) | 0.1919 | [0.1699, 0.2147] |

Note: B denotes beta distribution; G denotes gamma distribution.

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Zhang, X.; Zhang, Y.; Zhu, Y. COVID-19 Pandemic, Sustainability of Macroeconomy, and Choice of Monetary Policy Targets: A NK-DSGE Analysis Based on China. Sustainability 2021, 13, 3362. https://0-doi-org.brum.beds.ac.uk/10.3390/su13063362

AMA Style

Zhang X, Zhang Y, Zhu Y. COVID-19 Pandemic, Sustainability of Macroeconomy, and Choice of Monetary Policy Targets: A NK-DSGE Analysis Based on China. Sustainability. 2021; 13(6):3362. https://0-doi-org.brum.beds.ac.uk/10.3390/su13063362

Chicago/Turabian StyleZhang, Xinping, Yimeng Zhang, and Yunchan Zhu. 2021. "COVID-19 Pandemic, Sustainability of Macroeconomy, and Choice of Monetary Policy Targets: A NK-DSGE Analysis Based on China" Sustainability 13, no. 6: 3362. https://0-doi-org.brum.beds.ac.uk/10.3390/su13063362

Note that from the first issue of 2016, this journal uses article numbers instead of page numbers. See further details here.