Analysis and Assessment of Sustainable Entrepreneurship Practices in Polish Small and Medium Enterprises

1

Faculty of Management, Czestochowa University of Technology, Al. Armii Krajowej 19b, 42-201 Czestochowa, Poland

2

Faculty of Materials Science and Technology in Trnava, Slovak University of Technology in Bratislava, Jána Bottu 25, 917-24 Trnava, Slovakia

*

Author to whom correspondence should be addressed.

Sustainability 2021, 13(7), 3595; https://0-doi-org.brum.beds.ac.uk/10.3390/su13073595

Submission received: 18 February 2021

/

Revised: 15 March 2021

/

Accepted: 16 March 2021

/

Published: 24 March 2021

(This article belongs to the Special Issue Methods, Tools, Indexes and Frameworks in Sustainability Assessment)

Abstract

:Entrepreneurship is one of the driving forces behind the development of the national economy. The effect of entrepreneurship in the economic dimension is a business entity, most often a small or medium enterprise. The SME sector plays a significant role in every national economy. Traditionally, people perceived entrepreneurship as a factor measured by the earned profit. Increasing it was the primary goal of enterprises operating on the market. The operating conditions and competitiveness level have meant that enterprises beside economic goals also pursue social and environmental goals. Entrepreneurship is perceived as a determinant of social and ecological development, thus referred to as sustainable entrepreneurship. This article aims to identify and evaluate attitudes towards sustainable entrepreneurship among Polish enterprises. We compare the obtained results with their self-assessment and distinguish different approaches to business activity. The cluster analysis of survey results shows that the Polish SME sector can be divided into five separate groups characterized by a different approach and level of implementation of sustainable development. We also concluded that the Polish enterprises are more focused on social than environmental aspects.

1. Introduction

Traditionally understood, entrepreneurship means a process focused on discovering, creating, and using the entrepreneur’s opportunities [1]. It means that the basis of an entrepreneur’s activities is precisely identifying or recognizing emerging business opportunities [2]. Therefore, entrepreneurship includes many proactive and innovative activities that enable the best use of emerging business chances and opportunities [3].

At this moment, the operating conditions and the competitive environment make enterprises that want to survive and develop focus not only on achieving profits and increasing market share but also on taking actions following sustainable entrepreneurship assumptions [4,5,6,7,8,9,10,11]. Moreover, the implementation of sustainable practices determines the further development of the company and strengthening its competitive position.

Entrepreneurship is an essential factor enabling success, which is most often measured by profit achieved. However, it is also a force to integrate various resources necessary to start a business [12]. New enterprises generate new job positions and multiply the material and non-material benefits of their operation for individuals and the whole economy. In common sense, entrepreneurship means regularly taking up challenges, actions, and activities both in the professional and private sphere. Today, one of the main elements determining the competitiveness of national economies is entrepreneurship [13].

Even though sustainable entrepreneurship has been the subject of much academic research in recent years [10,14,15,16,17,18,19], there is still a research gap in identifying the enterprise’s characteristic attitudes towards sustainable entrepreneurship. Although entrepreneurship has long been recognized as a factor facilitating and even determining social change [20,21,22], the following issues are still relevant:

- Do enterprises have a good understanding of the idea of sustainable entrepreneurship?

- Do enterprises that declare themselves sustainable reflect this belief in their goals and activities?

- In what areas are there problems with operating sustainably?

- In which areas is the concept of sustainable entrepreneurship best implemented?

The first scientific publications on sustainable entrepreneurship were mostly theoretical [5,23]. Over the years, the number of articles in which conclusions were based on empirical research in the context of a specific group of enterprises, entrepreneurs, countries, sectors or industries has increased. Recent publications devoted to this issue clearly show the focus on the opportunities offered by modern technologies, concepts, or regulations in implementing sustainable entrepreneurship. Moreover, the majority of research on sustainable entrepreneurship concerned Western and Asian countries. Simultaneously, there are only a few publications on Polish sustainable enterprises from the SME sector.

Keeping this in mind, the purpose of the article is:

- Recognizing how enterprises perceive their activities in the light of sustainable entrepreneurship.

- Identification of characteristic attitudes of Polish enterprises towards sustainable entrepreneurship.

- Comparison of the obtained results with the own assessment of enterprises.

- Identification of differences in the approach to the business activity of enterprises.

Sustainable entrepreneurship is a unique research area that combines three seemingly opposing aspects: creating economic, social, and environmental value with simultaneous care for the wellbeing of future generations. Nowadays, it is easy to observe that the economic activity conducted by entrepreneurs aims, to some extent, at the integration of these three areas. The adopted goals will contribute to generating and maintaining value over time so that the enterprise fits within the framework of sustainable development and thus operates in the spirit of sustainable entrepreneurship.

2. The Literature Review

2.1. Sustainable Entrepreneurship

Sustainable entrepreneurship” combines a lot with classic entrepreneurship, linking the two terms “sustainable development” and “entrepreneurship”. The fundamental aspects of sustainable activity are less oriented towards management systems and more focused on an entrepreneur’s initiative and skills to achieve market success and make (positive) changes in society and the natural environment. The basis of sustainable entrepreneurship is social entrepreneurship and eco-entrepreneurship, which are two separate areas. While eco-entrepreneurship focuses on the natural environment [24,25,26,27], social entrepreneurship focuses on improving social wellbeing [28,29,30,31]. On the other hand, sustainable entrepreneurship “goes further” since it integrates the social, environmental, and economic aspects. Based on the above considerations, we assumed that the basis was traditionally understood entrepreneurship, based on which social entrepreneurship and eco-entrepreneurship were created, constituting the basis for sustainable entrepreneurship.

The definitions of sustainable entrepreneurship are very diverse, which is presented as a process, activities, research, attitudes, and behaviors. T.J. Dean and J.S. McMullen [18], in their definition, focused on market failures, which constitute an opportunity to discover new economic opportunities, which, in addition to providing economic benefits, also affect the achievement of environmental and social benefits. A. Kuckertz and M. Wagner used the previous definition [5]. However, they emphasized an individual’s role, most often an entrepreneur-, discovering and using emerging opportunities, considering ecological and social aspects. B. Cohen and M.I. Winn [32] emphasized that it is necessary to discover future possibilities for new products and services, bringing benefits in the economic, ecological, psychological, and social aspects. They assumed that the four types of market failure (i.e., ineffective firms, externalities, erroneous pricing mechanisms, and information asymmetries) contribute to environmental degradation on the one hand. The definition formulated by D.A. Shepherd and H. Patzelt [33] also assumed researching the possibilities of developing future products or services from which the organization will achieve economic, environmental, and social benefits. On the other hand, the aspect of innovation is emphasized in the definitions proposed by S. Schaltegger, M. Wagner [34], K. Hockerts, and R. Wustenhagen [4]. They defined sustainable entrepreneurship as innovative activities that result in new services and products that bring economic benefits to organizations and society through social and environmental innovations. In turn, in the definitions provided by W. Young and F. Tilley [35] and D.F Pacheco, T.J. Dean, and DS. Payne [6], sustainable entrepreneurship is understood as a set of behaviors that characterize both an organization and entrepreneurs that focus on achieving economic benefits and activities consistent with sustainable development.

When analyzing the above definitions of sustainable entrepreneurship, one gets the impression that many definitions indicate that social and environmental aspects determine sustainable entrepreneurship. Taking into account that in our research we focused on examining how companies cope with the implementation of social and environmental goals, we applied the definition given by D.A. Shepherd and H. Patzelt [26], according to which “enterprises focus on nature conservation, life support, and community, seeking to see opportunities for future products, processes, and services to achieve benefits-economic, environmental, and social”.

It is also worth mentioning that sustainable entrepreneurship models a person’s overall activity, both his professional and private life. Therefore, it affects the behavior, attitudes, and reactions of the entrepreneur and the company’s organizational culture [36]. Bearing in mind that it is now increasingly challenging to maintain a balance between the economy, the environment, and society, the entrepreneur’s role as a visionary and solution provider is to maintain this balance. They can solve problems or crises and create a new business model based on a vision of SE. Governments are also more willing to help entrepreneurs incubate their ventures or look for a way to move from an uncertain and risky business model to a safer or socio-environmentally responsible one.

2.2. Sustainable Enterprise

The term “sustainable enterprise” is the result of the emergence of a new paradigm known as “sustainability”, which can be translated loosely as “renewable”, “sustainable” or a constantly ongoing process of maintaining balance in certain areas. Concerning the enterprise, this paradigm has two meanings: It emphasizes its ability to maintain business continuity even in a very changeable and dynamic environment, and secondly, it enables the organization to use the conditions that arise as a result of the changes taking place [37]. The concept of “sustainable enterprise” responds to the changes continually taking place in today’s reality in which enterprises operate. Moreover, they must face in order to be able to develop further and strengthen their market position.

Sustainable enterprises generate good enough, decent jobs, and are productive, competitive, and contribute to social inclusion. Environmentally sustainable production can significantly contribute to the achievement of the SDGs (Sustainable Development Goals). Therefore, a sustainable enterprise’s goal is continuous growth and development. This requires constant access to critical resources and the core business’s continual redefinition to meet both customers’ and shareholders’ needs.

Since the concept of sustainable development is a comprehensive and general concept, on its basis, many areas have arisen which, to a greater or lesser extent, implement its main assumptions. In other words, the term “sustainable” is used very often as an adjective that describes activities that are consistent with the assumptions of sustainable development. SMEs play a key role in sustainable entrepreneurship due to their number, contribution to economic and sustainable development, or flexibility in addressing environmental and social problems [36]. They are essential growth sources (on a local, regional, national, and global scale), employment, and decent work. At the same time, enterprises face many difficulties in meeting the challenges: They operate in an environment of laws and regulations that can either favor or inhibit their development. While they have been the primary source of newly created jobs in recent decades, their main characteristics are low productivity and work quality. Therefore, modern enterprises face a challenge in which they should strive for continuous development while taking responsibility for actions affecting the immediate social and environmental environment in the conditions of an increasingly globalized world. The concept of sustainable development changed the modern enterprise’s business perspective and strategies, which moved away from achieving economic and financial profit towards social and ecological order. The enterprise’s financial results are indeed a vital success factor, but next to them, social and ecological responsibility has also become the critical success factor [38,39,40]. There is also evidence that SMEs have adapted to environmental paradigms, especially small and young SMEs [34]. Enterprises, including SMEs, make the most significant contribution to the sustainable development of the economy and society if their core business is about solutions to environmental and social problems, if they provide green products, and if their innovations impact the mass market and society [34].

The common element of sustainable entrepreneurship and sustainable enterprise is the delivery of environmentally and socially friendly products with commercial success. However, sustainable entrepreneurship can also characterize an enterprise with an established market position and has been operating for many years, which, in addition to operating activities aimed at achieving financial profits, initiates, e.g., social changes or undertakes activities aimed at improving the condition of the natural environment.

Crals and Vereeck [41] underlined the strong relationship between sustainable entrepreneurship and sustainable enterprise. They claimed that it is a continuous commitment of business to ethical behavior and contributing to economic development while improving the employee’s quality of life, their families, local communities, society, and, consequently, the whole world and its future generations. This activity is carried out by entrepreneurs focused on making a profit and involved in activities aimed to achieve sustainable development goals in the economic and environmental aspects. Sustainable entrepreneurship is also an innovative, market-oriented, and creativity-driven form of economic and social value creation through ground-breaking, environmentally or socially friendly products or services [42,43].

3. Enterprises from the SME Sector, the Research Background, and Significance/Towards Sustainable Enterprise as the Background Research

The SME sector enterprises play a significant role in almost every national economy around the world. They are the foundations for the national economy’s further development and the global one [44]. Currently, they generate more than 60% of global economic outputs [45]. According to the International Finance Corporation, more than 90% of companies worldwide are enterprises from the SME sector, accounting for more than half of the total employment [46]. OECD assumes that SME enterprises contribute more than 60% of the European’s Union GDP and are also an essential source of innovation and wealth information [47]. In New Zealand, 98% of all businesses are SME enterprises, with more than 2.5 million SMEs in the Asia region accounting for 99.8% of all businesses in Turkey. Moreover, SME enterprises from China account for 99% of the whole country’s businesses, 60% of exports, 40% of GDP, 75% of job opportunities, and are performing an expanding role in adopting sustainable development principles. There are almost 36 million SME enterprises in India, and their contribution accounts for 8% of GDP, but in production, they account for 45% of total manufacturing output and 40% of export [48]. In Poland, the SME sector constitutes the overwhelming majority of enterprises in Poland—99.8%, generating almost 73% of the GDP value and employing almost 10 million employees [49].

This substantial economic significance and influence on the national economies resulted in the need to formulate a definition to distinguish this enterprise from all companies operating on the market. According to OECD, “Small and medium-sized enterprises (SMEs) are non-subsidiary, independent firms which employ fewer than a given number of employees. This number varies across countries [50]. In the EU, the upper limit designating an SME is 250 employees, while in the US, SME can hire up to 500, but in other countries, this limit has been cut to 200 employees only. According to the Commission Recommendation [51] (Table 1):

- The category of micro, small, and medium-sized enterprises (SMEs) covers the enterprises that employ fewer than 250 persons and have an annual turnover not exceeding EUR 50 million and/or an annual balance sheet total not exceeding EUR 43 million.

- A small enterprise is an enterprise that employs fewer than 50 people and whose annual turnover and/or annual balance sheet total does not exceed EUR 10 million.

- Microenterprise is an enterprise that employs fewer than ten people and whose annual turnover and/or annual balance sheet total does not exceed EUR 2 million.

Polish Law adopted the exact definition. However, the phrase “in at least one of the last two financial years” is added [52]. Values expressed in euro are converted into zlotys according to the average exchange rate announced by the National Bank of Poland on the last day of the financial year selected to determine the entrepreneur’s status. For this article and the conducted research, we adopted the definition recommended by CR.

4. The Research Methodology

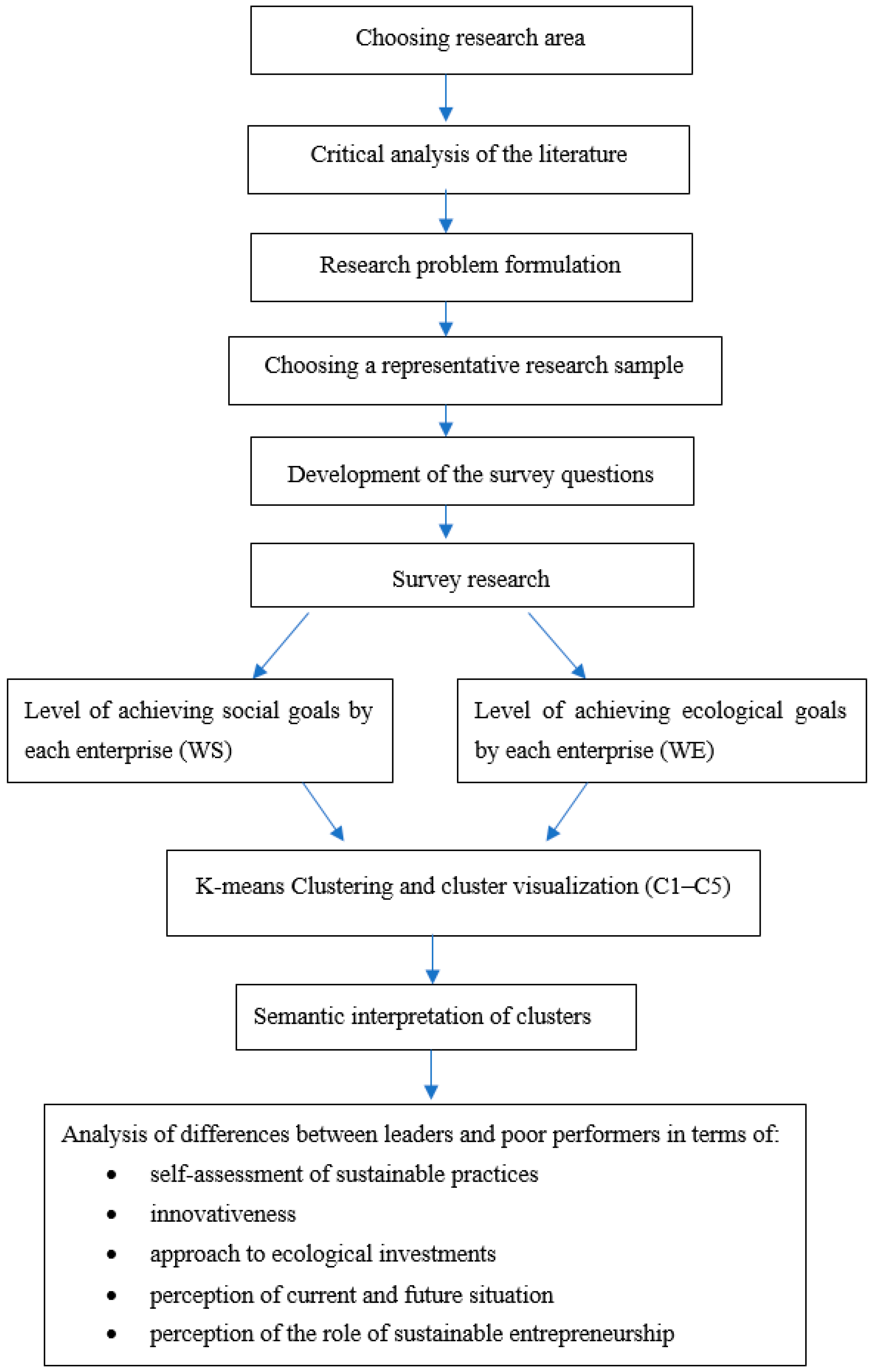

The course of the research included the following stages (Figure 1):

- The research area selection: Based on previously conducted research in sustainable entrepreneurship, it was possible to identify a research area that has not yet been thoroughly investigated—sustainable entrepreneurship in Polish SME enterprises.

- Critical analysis of the current state of knowledge: The analysis of the available literature in sustainable entrepreneurship made it possible to indicate that sustainable entrepreneurship is the subject of many considerations nowadays. However, there is still a research gap in identifying the enterprise’s characteristic attitudes towards sustainable entrepreneurship.

- Research problem formulation: The result of the literature’s analysis is the formulated research problem concerning Polish enterprises’ activities consistent with sustainable entrepreneurship.

- Defining the subject of research: Polish enterprises from the micro, small, and medium-sized enterprises sector were selected as the research subject.

- Defining the purpose of the research: The research aimed to analyze and assess SE in Polish SME enterprises.

- Determining the scope of the conducted research: Based on the formulated research objectives, the scope of the research included: Examining how enterprises cope with the implementation of environmental and social objectives, which enabled assigning enterprises to specific groups (clusters), and then examining how enterprises from particular groups cope with economic goals and their views on the economic situation.

- Selection and preparation of research tools: A survey questionnaire was selected to research Polish enterprises since the survey is a quick and straightforward way to collect large amounts of data on the surveyed enterprises. Based on the literature analysis, a questionnaire was constructed containing 20 questions on sustainable entrepreneurship in Polish SME enterprises.

- Implementation of the survey: The survey was conducted among 400 enterprises representing a representative sample of the survey, using CATI and CAWI methods.

- Verification of the obtained research material: Verifying the obtained primary data did not reveal any errors or omissions.

- Analysis of the obtained results: The obtained results were the primary data, subjected to further analysis. For this purpose, the clustering method was used, as it is a method that allows distinguishing groups from the population without any prior assumptions about the division.

- Discussion and conclusion: Containing comparison with other research results and conclusions.

The conducted literature research indicated that entrepreneurship is a factor that integrates the social, environmental, and economic aspects, inseparable from the company’s activity [20,21,22,33,41,53,54,55,56,57]. Moreover, the result of the literature analysis made it possible to construct a research tool in the form of a questionnaire, to conduct quantitative research. Quantitative methods were used since answers to questions on the Likert scale can be treated as a given feature’s intensity (commitment to a given goal). This enables the construction of indicators, the identification of groups of enterprises, and their comparison.

The issues contained in the questionnaire were focused on the following thematic issues:

- Determining which of the goals in the following aspects: Ecological and social, are realized by the surveyed company.

- The attitude of Polish entrepreneurs to statements in sustainable entrepreneurship and the implementation of specific activities.

- Solutions owned by the enterprise (in line with sustainable entrepreneurship), norms, standards, and procedures.

- Reflecting the enterprise’s current situation, perception, and forecasts as to the further development of the economic situation in Poland.

- An attempt to determine the impact of sustainable entrepreneurship on Polish enterprise’s activities in the coming years.

The answers to individual questions took the form of single, multiple choice answers and answers on the 6-point Likert scale [58,59,60,61]. The scale used in the study consists of six categories of answers: (6—definitely yes, 5—yes, 4—rather yes, 3—rather no, 2—no, 1—definitely no [59]. The analysis of measurement data using the Likert scale involves comparing and interpreting the points counted for individual items or individual respondents. We have chosen the 6-point Likert scale since having an even number of ratings on the scale obliges respondents to the positive or negative end of the scale, resulting in better data. Furthermore, if at any point neutral is desired, then “rather yes” and “rather no” can be averaged together [58,59,60,61].

Before the main study, we conducted a pilot study on 10 companies to eliminate potential inaccuracies so that respondents had no doubts about the nature of the questions. Then, the primary survey among 400 enterprises, a representative sample of the survey, was conducted.

When choosing the study using the representative method, efforts were made to minimize the sample size while maintaining the required certainty and further inference accuracy. The minimum sample size when estimating the probability of success p in the general population was calculated based on the sample size Formula for a vast population:

where Nmin is the minimum sample size, Np is the population size, α2 is the level of significance, e2 is the accepted level of the highest error, and f is the structure index.

It should be emphasized that the structure index’s value and the maximum error should be in the range 0–1. If the value of the structure index in the population is unknown, the value of 0.5 should be given.

As the calculations show, the minimum sample size, with an acceptable confidence level of 1 − α = 0.90 and the maximum estimation error e = 5%, should be 384 questionnaires. Since 400 questionnaires were qualified for the research, this condition was met, and the sample obtained meets one of the representative method’s assumptions. This value results from the relationship that determines the minimum sample size used when selecting the sample by individual sampling. The main study was conducted in August 2019, using the CATI and CAWI methods.

The answers received from all 400 questionnaires were primary data that were further developed. This study covered two stages: In the first stage, an Excel spreadsheet was used, which enabled the graphical representation of necessary information on the research sample. In the second stage, statistical calculations and the cluster analysis were carried out.

5. Results

5.1. Grouping of Enterprises Using the Clustering Method

The first stage of the analysis was to distinguish groups of enterprises according to their environmental and social goals. We have chosen environmental and social goals since these two aspects determine whether a given enterprise pursues sustainable entrepreneurship, the essence of which is to conduct business not only bringing a specific economic profit but also enabling the fulfillment of environmental and social goals [41,62,63,64,65,66].

Two selected questions of the survey focused on the implementation of environmental goals (marked as WE.1., WE.15) and social (WS.1., WS.14) consistent with the concept of sustainable entrepreneurship (Table 2). Answers to these two questions adopted a scale of 1–6 (6—definitely yes, 5—yes, 4—rather yes, 3—probably not, 2—no, 1—definitely no).

The results obtained from the questions on a six-point scale allowed the calculation of indicators showing the company’s involvement in activities consistent with the concept of sustainable development:

- WE—implementation of ecological goals.

- WS—implementation of social goals.

The indicators for the areas mentioned above were calculated by summing up the Likert scale points. As a result, we received a table in which we calculated two indicators for each of the 410 enterprises. The higher value of each indicator illustrates the better implementation of sustainable entrepreneurship activities.

The highest possible values of the WE and WS are, respectively, 90 and 84 (if 6 is the answer to each question). Moreover, the lowest 15 and 14 (if 1 were the answer to each question). Only two enterprises achieved the highest values of both indicators. There were no enterprises that would achieve minimum values (the lowest values achieved by one enterprise were WE = 15 and WS = 19).

The next step was to identify Polish enterprise’s characteristic attitudes towards implementing the SE concept and compare the results with the company’s self-assessment. Here, we took the first question of the survey into account, which was to establish how companies perceive their activities in the light of the presented definition. Possible answers to the questions included the options: Yes, no, I do not know.

The enterprises’ characterization based on answers to the two questions was to determine their behavior. The self-assessment question was to illuminate the respondents’ awareness in the area of sustainable entrepreneurship.

The research focused on identifying the similarities between the studied enterprises, determining the specificity of the selected groups, and then identifying their strengths and weaknesses in implementing the concept of sustainable entrepreneurship.

The implementation of this goal and the size of the data set determined using the cluster analysis method, i.e., unsupervised classification, which consists of assigning individual examined objects to separate groups. No predetermined division was assumed, while the study focused on searching for similarities between enterprises and, on this basis isolating specific characteristic patterns of behavior.

The data were explored using the K-means algorithm which is one of the most popular unsupervised machine learning algorithms. This method decomposes a dataset into a set of disjoint clusters. Unsupervised algorithms make inferences from datasets using only input vectors without referring to known or labelled outcomes. The K-means algorithm identifies the k number of centroids, and then allocates every data point to the nearest centroid. The process is performed iteratively until an optimal partition is reached.

Given a set of observations (x1, x2, and xn), where each observation is a d-dimensional real vector, k-means clustering aims to partition the n observations into k (≤n) sets S = {S1, S2, and Sk} so as to minimize the within—cluster sum of squares (WCSS) (i.e., variance). The objective is to find:

where μi is the mean of points in Si. This is equivalent to minimizing the pairwise squared deviations of points in the same cluster.

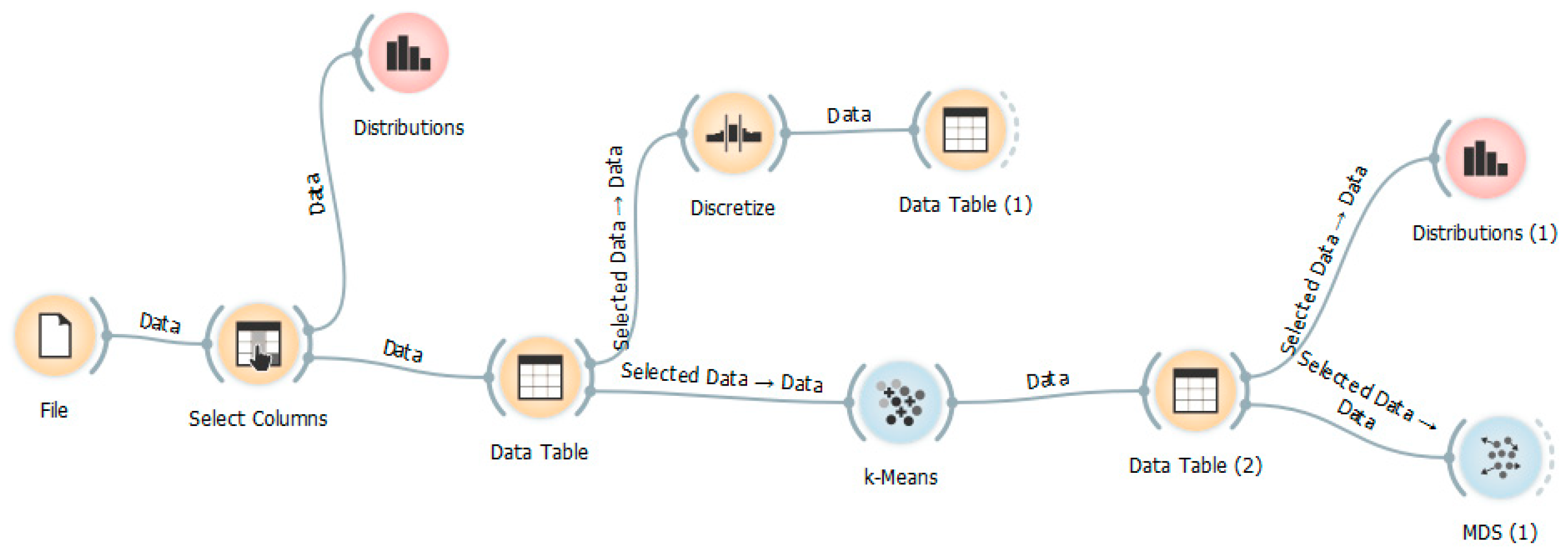

We used the Orange [67] software to perform the analysis. Figure 2 presents the stages of data mining and the tools used.

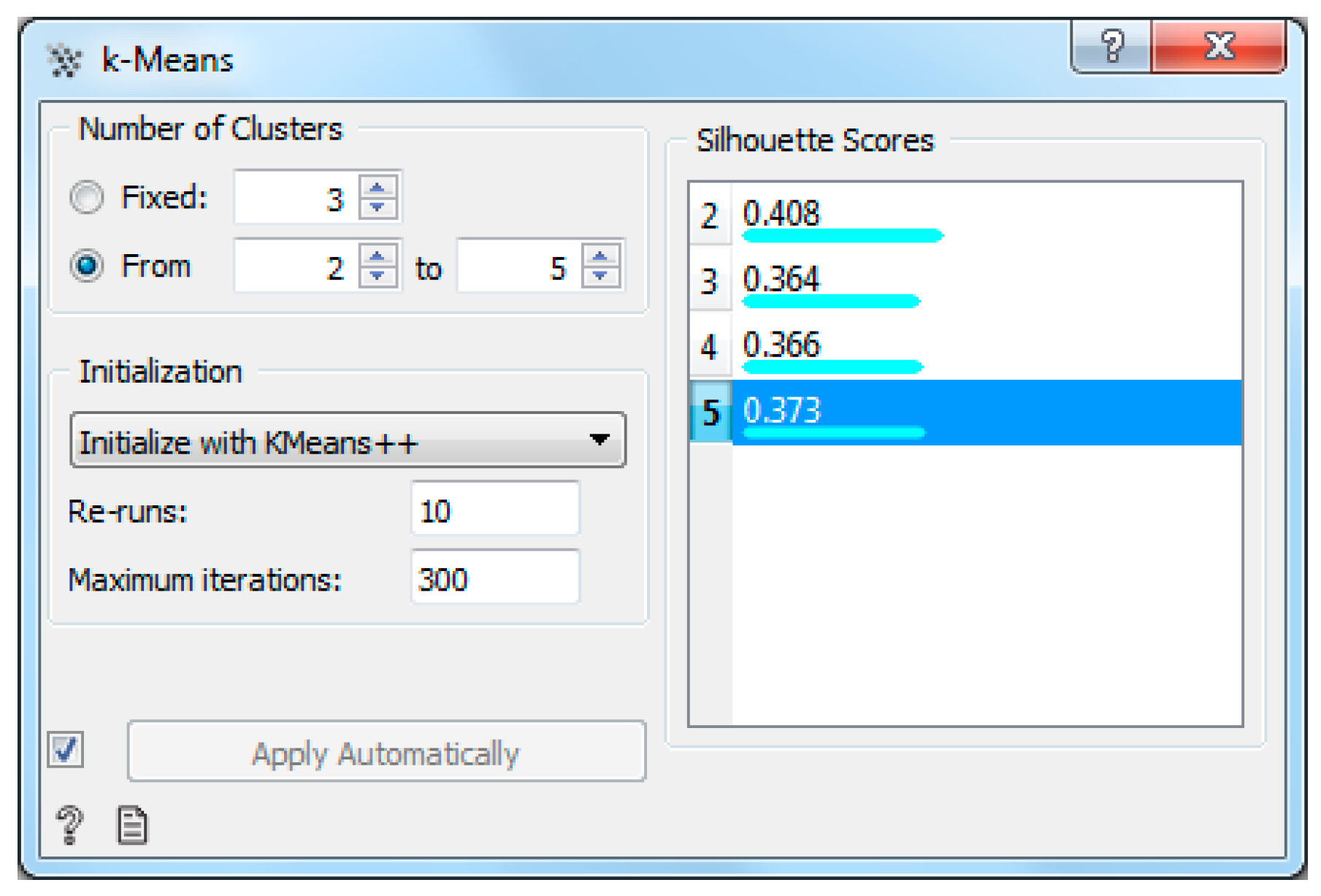

The data mining tool proposed various possible data divisions and the generated cluster’s quality indicator called Silhouette Score (Figure 3). A larger Silhouette Score informs about a more precise assignment of elements to the group (more significant similarity of elements in the cluster).

The best match index was found in the division into two, then into five clusters. We chose the division into five clusters due to the more detailed possibility of semantic interpretation of the results.

The input data were the values of the two indicators, as mentioned earlier, calculated based on each respondent’s responses.

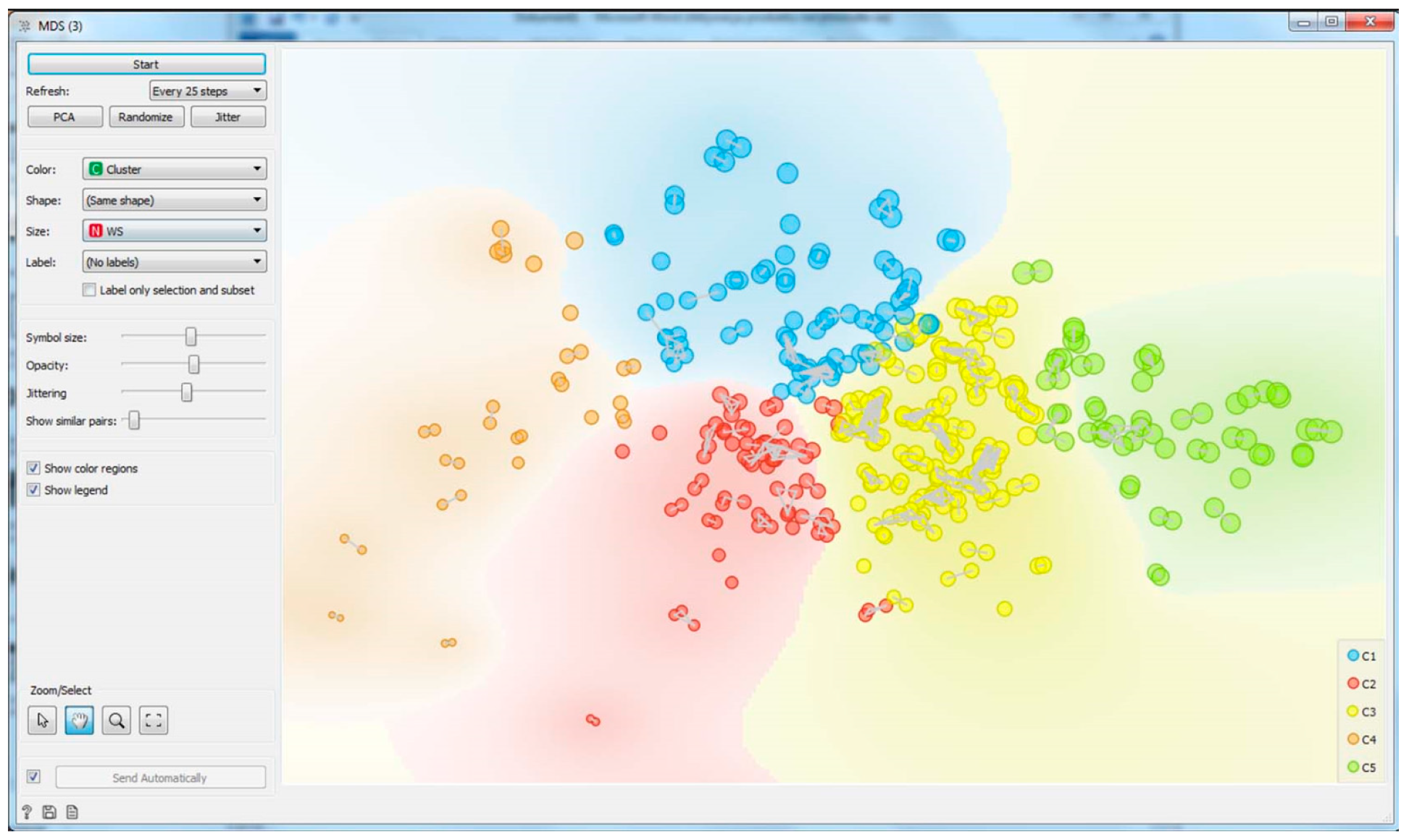

To better assess the cluster’s quality, we visualized them using the MDS algorithm. The visualization shows that the groups are relatively homogeneous (clearly distinguished color areas, objects from the same cluster are gathered close to each other and paired).

The MDS algorithm enables the visualization of the features of the tested objects. The figures below show WS (Figure 4) and WE (Figure 5) values as the marker size (the better the WE or WS index, the bigger the symbol).

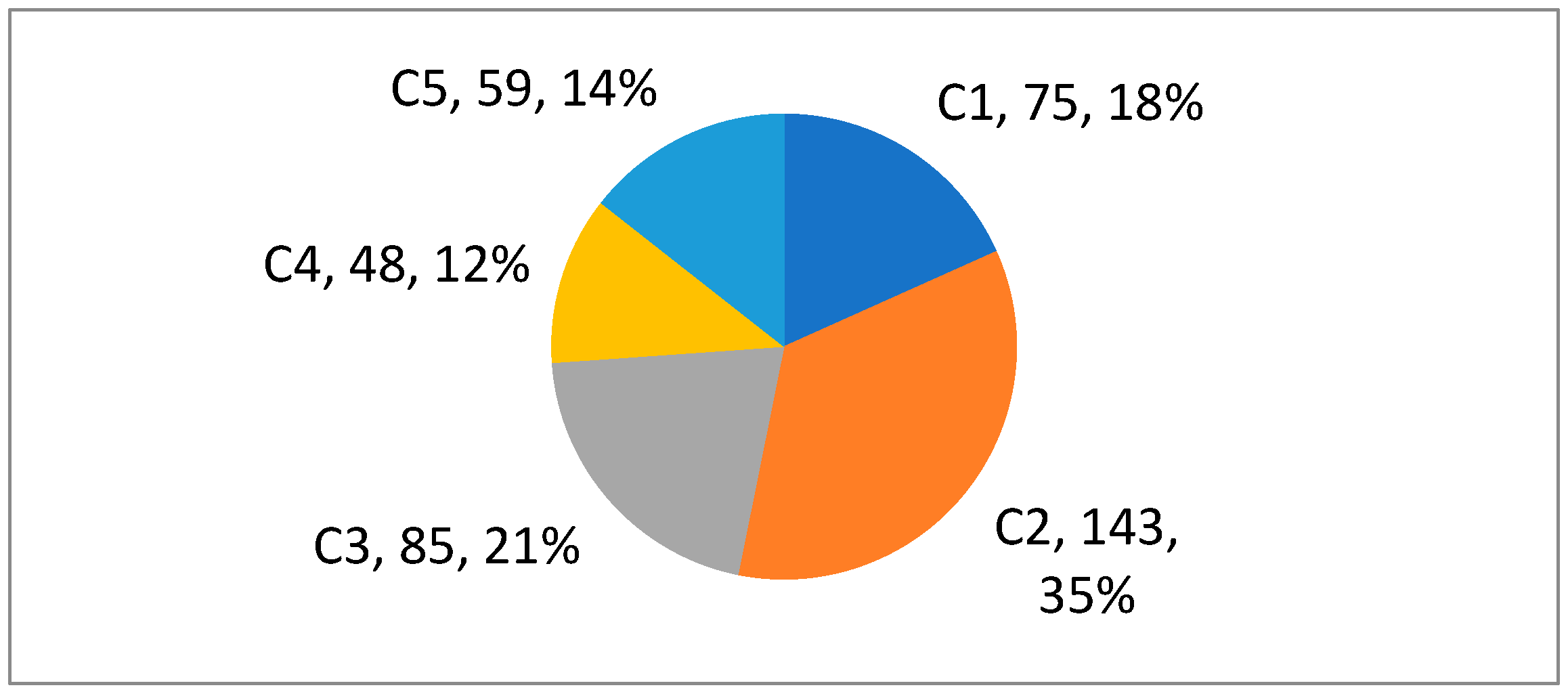

Therefore, enterprises were divided into five clusters due to the specificity of their activities in the social and environmental field. The number of enterprises in individual C1–C5 groups is presented in Figure 6.

The size of the research sample is representative of the population of small and medium-sized enterprises in Poland. Therefore, it can be assumed that the division into groups reflects the characteristics of the studied population.

Additionally, to facilitate the interpretation of clustering results and increase the division’s clarity, the indicator’s values have been divided into three groups: Low, medium, high. The division was performed using the Discretize algorithm available in the Orange software. The method of discretization according to the equal frequency was chosen, which considers the data set’s nature when partitioning (Table 3).

Five groups of enterprises have been distinguished, characterized by a distinctly different approach and sustainable development implementation. Table 4 presents a short characteristic of the selected clusters with their classification according to the level of sustainability.

The analysis of enterprises grouped into clusters revealed their behavior in the ecological and social areas. We analyzed the answers to the question “Does the enterprise operate following the concept of sustainable entrepreneurship.” The answer to this question was to highlight the enterprise’s self-awareness of sustainable development (Table 5).

As it could be assumed, the enterprises from cluster C5, which best implement the PE concept, also assess their activities correctly. Only in the case of two enterprises from this group, the answer was “no”. In clusters C2 and C3, assessed as implementing the SE concept on average, the responses are similar—about 60% of enterprises have confidence that they implement this concept well. On the other hand, in clusters C1 and C4, whose activities were assessed poorly, about half of the enterprises wrongly consider their sustainable activities. A high percentage of “I do not know” answers in all groups leads to the conclusion that Polish enterprise’s knowledge about sustainable entrepreneurship is insufficient. The next task was the semantic interpretation of the division of enterprises into groups. For this purpose, we compiled data describing cluster’s characteristics in the form of tables and charts.

5.2. Semantic Interpretation of Clustering Results

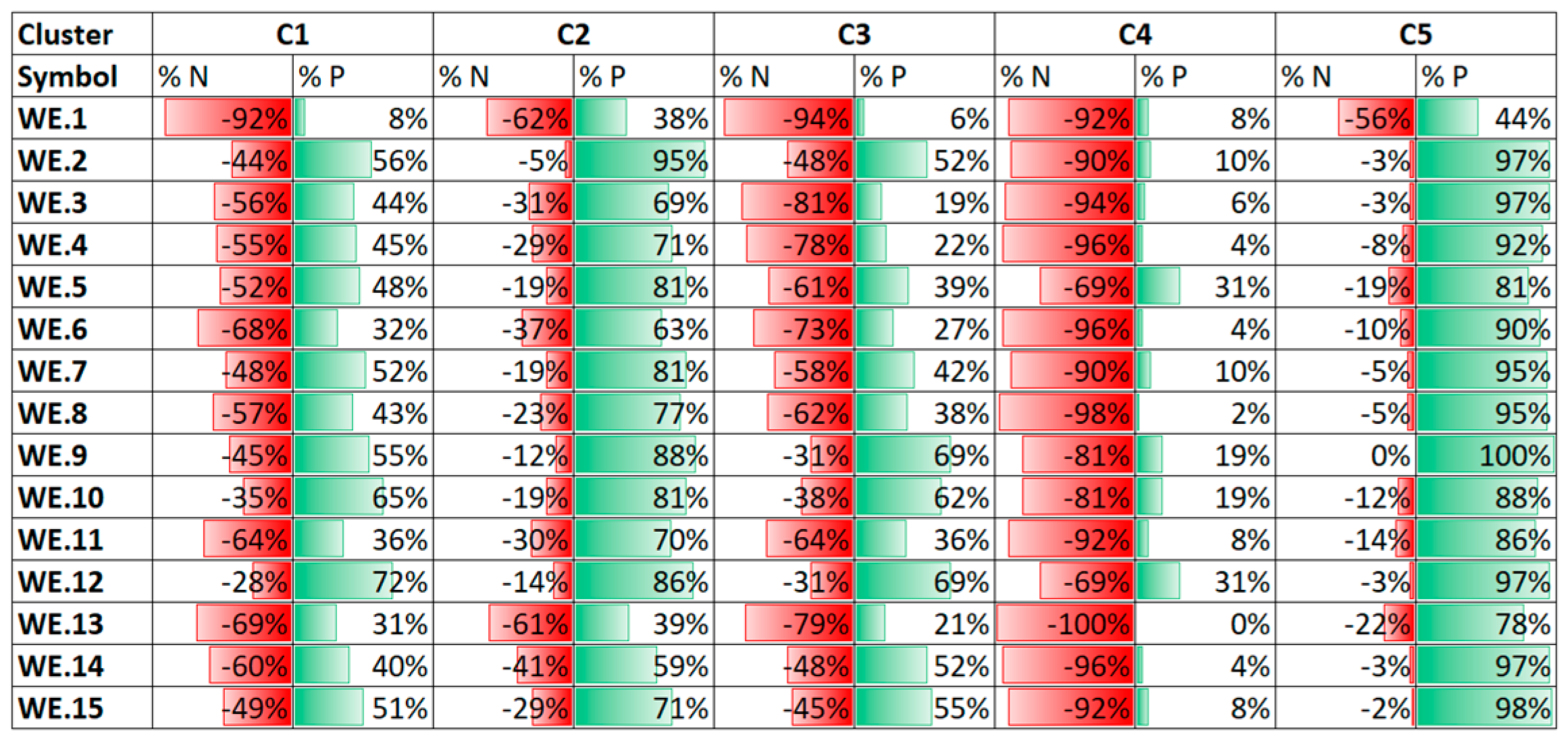

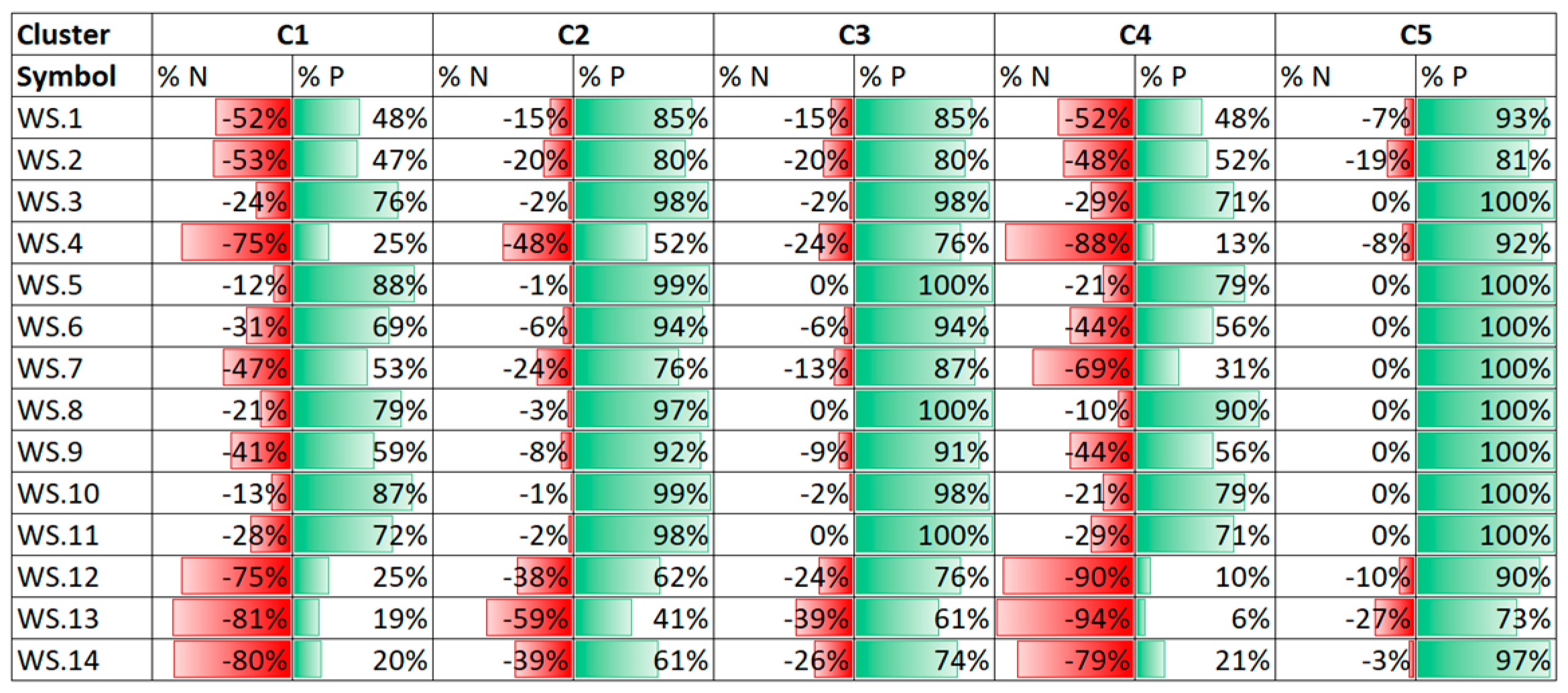

For facilitating the interpretation of clustering results, a summary of answers to the questions was prepared, broken down into individual clusters (Figure 7 and Figure 8). The visualization presents the number of negative (1–3) and positive (4–6) responses that made up WS and WE indicators. We calculated the sum of the negative (1–3) and positive (4–6) answers for each question. We visualized the percentage of negative and positive responses as data bars to make the problems more comfortable to see. The red color of the data bar in the table represents the percentage of negative responses, while green represents positive responses.

There were 75 companies in cluster C1 (18% of the research sample). The list of indicators (Table 6) shows that these enterprises’ main problem is the low achievement of social goals, while environmental goals are poorly or moderately achieved. Five enterprises achieved a high rate of environmental goals implementation. Nevertheless, it was still at the lower limit (61 or 63 points), while the WS ratio for these enterprises was low (Table 6).

Therefore, we can assume that the enterprises from cluster C1 are not very good at implementing sustainable entrepreneurship. We analyzed the answers to the questions to diagnose specific problems.

As can be seen in Table 6, negative responses prevail in nine out of 15 questions. The highest number of negative answers took place in the case of the following questions:

- WE.1. Use of renewable energy sources.

- WE.13. Use of devices regulating water consumption (aerators, stream pressure regulators, timer stops, photocells).

- WE.6. Reduction of radiation, hum, and noise related to the use of electronic equipment.

In the case of questions on social goals, the highest number of negative assessments occurred in the case of the following questions:

- WS.13. Conducting activities for the development of local culture.

- WS.14. Participation in charity events.

- WS.12. Pro-social activity.

- WS.4. Conducting activities for the benefit of the local community, e.g., patronage or sponsorship of cultural events.

In cluster C2 (Table 7), some enterprises cope well with the implementation of environmental goals (lack of low indicators), and on average, with the implementation of social goals.

In the case of questions on implementing ecological goals, the number of negative answers prevailed only for two problems. As in the case of the previously analyzed group, these were the following questions:

- WE.1. Use of renewable energy sources.

- WE.13. Use of devices regulating water consumption (aerators, stream pressure regulators, timer stops, photocells).

The implementation of social goals in the group of enterprises from cluster C2 is much better. Only one of the questions was slightly dominated by negative answers. It was the question WS13 about activities for the development of local culture. The second question with the most negative answers was WS4—activities for the benefit of the local community, e.g., patronage or sponsorship of cultural events. Based on the answers to the questions, we can conclude that these enterprises are more focused on supporting their employees.

Cluster C3 (Table 8) represents enterprises that cope poorly or moderately with implementing environmental goals (no positive ratings) but much better with implementing social goals (no negative ratings).

Comparing the relationship between negative and positive assessments (Figure 7) revealed that enterprises have problems implementing most ecological goals (nine negatives out of 15).

More than 60% of negative answers to the questions:

- WE.1. Use of renewable energy sources.

- WE.3. Reduction of working time of electronic devices.

- WE.13. Use of water intake regulating devices.

- WE.4. Use of efficient heating and emission-reducing systems.

- WE.6. Reduction of radiation, hum, and noise related to the use of electronic equipment.

- WE.11. Producing and selling environmentally friendly products.

On the other hand, the answers to the questions on achieving social goals were very positive. In not even one case, the negative opinions outweighed the positive ones (Figure 8).

The respondents gave 100% of positive answers to the following questions:

- WS.5. Taking care of safety in the workplace.

- WS.8. Striving to create a friendly atmosphere at work.

- WS.11. Development and application of accepted ethical standards related to the conducted activity.

Thus, we can conclude that the analyzed C3 group of enterprises is pro-social and oriented with particular care for the employee’s welfare.

Cluster C4 represents enterprises that are the worst at implementing sustainable entrepreneurship. The implementation rate of environmental goals was low in all cases, while achieving social goals was low in 80% (Table 9).

After a closer look at the answers to the questions from the category of ecological goals (Table 9), we can see that negative opinions prevail in all cases (69% or more). There is an overwhelming number of extremely negative assessments (1 and 2).

Answers to questions from the category of social goals are better than the answers on environmental goals. Similar to other clusters, in this group, the goals related to the development of culture (WS.13), pro-social activity (WS.12), and activities for the local community (WS.4) were also the worst.

Cluster C5 represents leaders of sustainable entrepreneurship in the surveyed group. Unfortunately, it constitutes only 14% of all respondents. Table 10 presents the ranges of the EC and WS indicators for cluster C5.

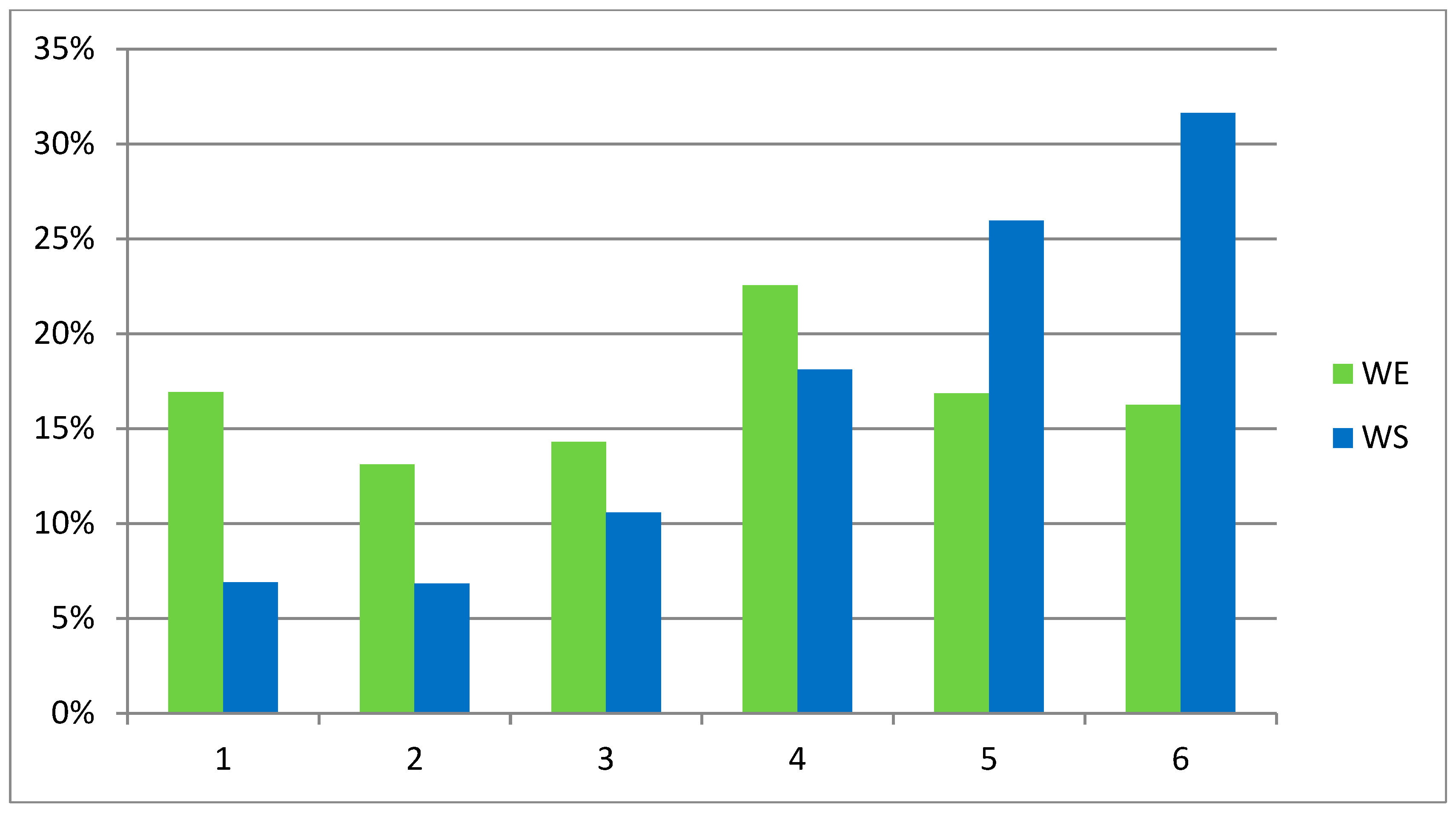

The same problem was revealed in the implementation of environmental goals by enterprises from cluster C5, which occurred in other groups—56% of the respondents gave a negative answer to the question on WE.1 (use of renewable energy sources). The implementation of social goals is excellent in the analyzed group. One hundred percent of the answers were positive for eight out of 14 questions and over 72% for the remaining ones. There were also individual negative responses among the group of leaders. In social goals, these were the questions: WS.1—hiring employees based on employment contracts and WS.2—offering work to people from the closest social environment. Enterprises also gave negative assessments (two and three) in question WS.13—carrying out activities to develop local culture. Based on the research results, we can conclude that environmental goals are a bigger problem for Polish enterprises than implementing social goals. The chart (Figure 9) shows the percentage number of responses on a scale of 1–6 for the categories of social (WS) and environmental (WE) goals.

The environmental problem that was most visible in all the groups identified in the study was the use of renewable energy sources. As the prices of systems for acquiring energy from renewable sources are systematically decreasing, such solution’s profitability grows. Therefore, we can assume that this problem may be caused not by the reluctance or little knowledge of entrepreneurs but by the lack of optimal legislative proposals on the Ministry of Energy. The second ecological problem highlighted was the use of devices regulating water consumption (aerators, stream pressure regulators, timer stops, photocells). It is a significant problem for the entire economy. One of the priorities of the environmental policy actions to rationalize water management should be [68]. In this area, in the country’s economy, it is necessary to regulate the Polish system of supporting ecological investments and disseminate knowledge on the importance of the problem and obtaining funds by enterprises. Other ecological problems visible in the research results are the decrease of radiation, noise, and noise related to electronic equipment and reduced working time of electronic devices. Solving these problems will contribute to the improvement of working conditions and the reduction of electricity consumption costs.

The most critical problems in achieving social goals are the low activity of enterprises in terms of activities for the development of culture and the local community, e.g., patronage or sponsorship of cultural events and charity auctions. These are important activities that should be adequately stimulated by the state (e.g., through an appropriate tax policy). Polish enterprises are more focused on social aspects related to employee’s care, compliance with the labor code, maintaining a good atmosphere in the team, and ensuring safety.

5.3. Identification of Differences in the Approach to the Business Activity of Enterprises

The next part of the study focused on distinguishing differences in the business activity of enterprises. The characteristics that were not subject to clustering were analyzed. For this analysis, two clusters, C4 and C5, representing extreme levels on the scale of sustainable entrepreneurship implementation, were selected. The analysis aimed at examining the characteristics of enterprises that perform best and worst sustainable entrepreneurship. In particular, the analysis of leader’s attitudes indicates the best practices among Polish enterprises.

RQ1:

Is there a difference in the innovativeness of enterprises from clusters C4 and C5?

H1:

The enterprises from cluster C5, which are leaders of sustainable entrepreneurship are more innovative than enterprises from cluster C4.

The implementation of sustainable entrepreneurship requires changing the established patterns of action and new technical solutions associated with investments. Thus, innovation has an economic and organizational dimension. To examine innovativeness, the authors interpreted the responses to the selected survey questions (Table 11):

Selected questions allow examining the features related to innovation. At the same time, we checked whether there was a significant correlation between the answers (Table 12). A high correlation (0.6–0.8) may indicate that the questions have a very similar scope and describe the same phenomenon. Correlations were calculated for the entire studied population of 410 enterprises.

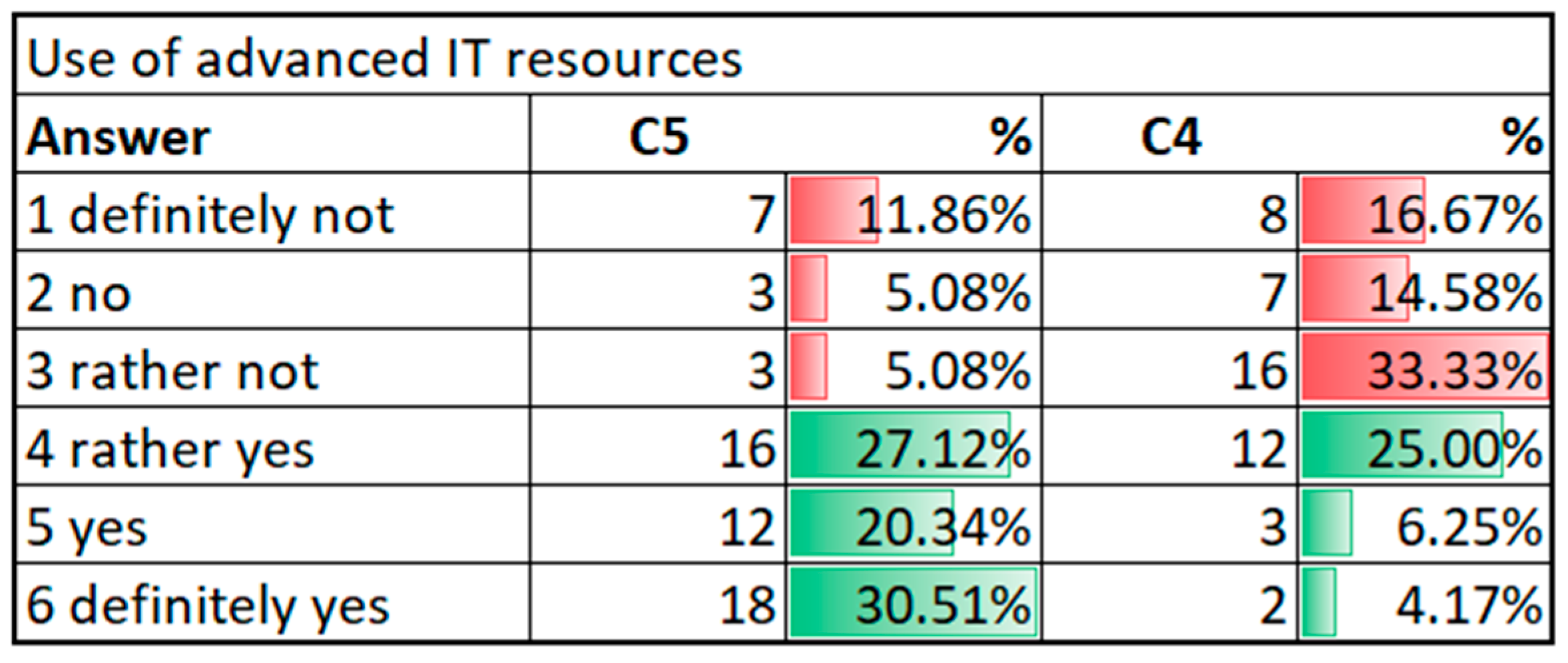

The highest correlation with the value of 0.6 was observed only in questions 6.13 and 6.14. However, it was assumed that it is still a permissible value. Information technology enables the monitoring and measurement of business processes. Accurate and up-to-date data is the basis for making the right decisions. Information technology also brings significant value in terms of optimizing operations and improving overall efficiency. Lower costs, less time needed to complete the process, and less manual work are examples of IT application’s benefits. With fault tracing, monitoring, and predictive maintenance, industrial and commercial components significantly have longer life cycles, leading to less waste. The implementation of advanced information technologies is an innovative activity. When analyzing the enterprise’s responses, we can notice that sustainable entrepreneurship leaders often use advanced IT solutions (Figure 10). In cluster C5, 77.97% of the respondents gave a positive answer, while in cluster C4, only 35.42%.

Red color in the table means the percentage of negative answers (1–3), while green color means the percentage of positive answers (4–6).

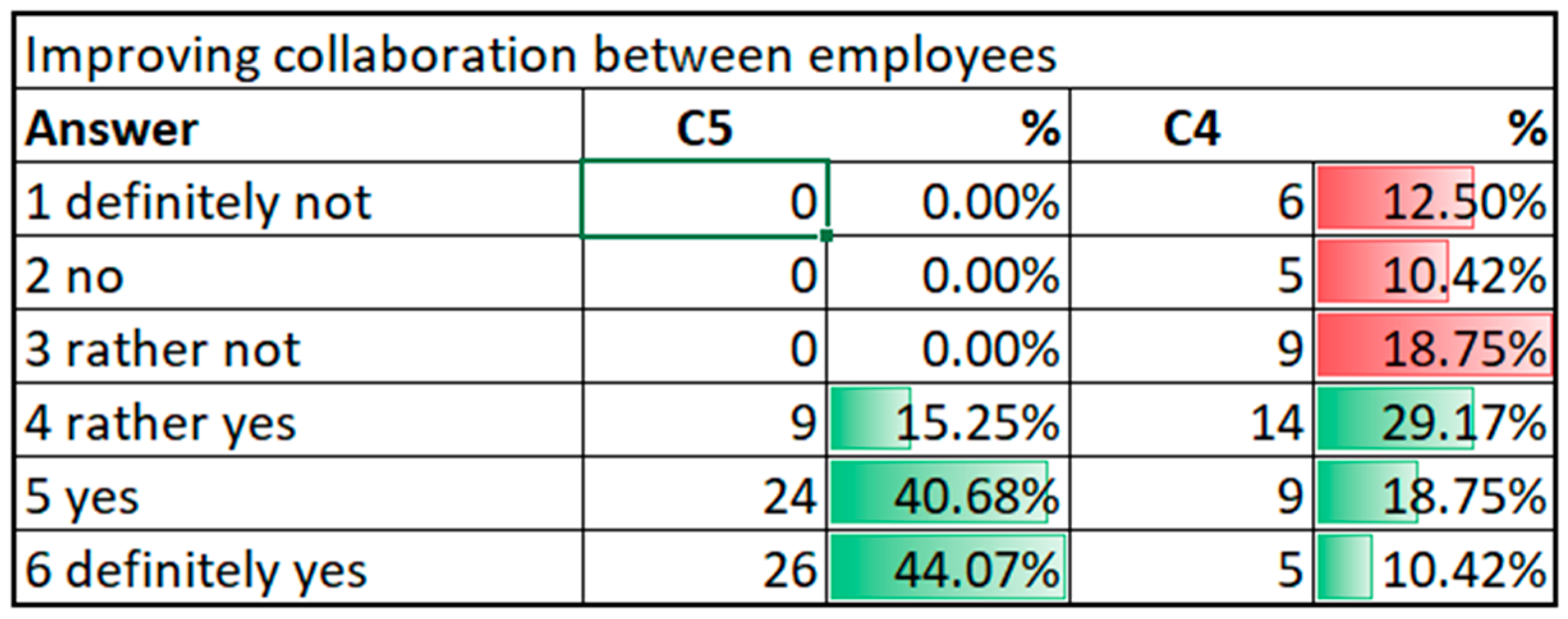

Striving to improve cooperation between employees is another activity that is directly related to the concept of sustainable entrepreneurship and, at the same time, proves an innovative approach to business (Figure 11).

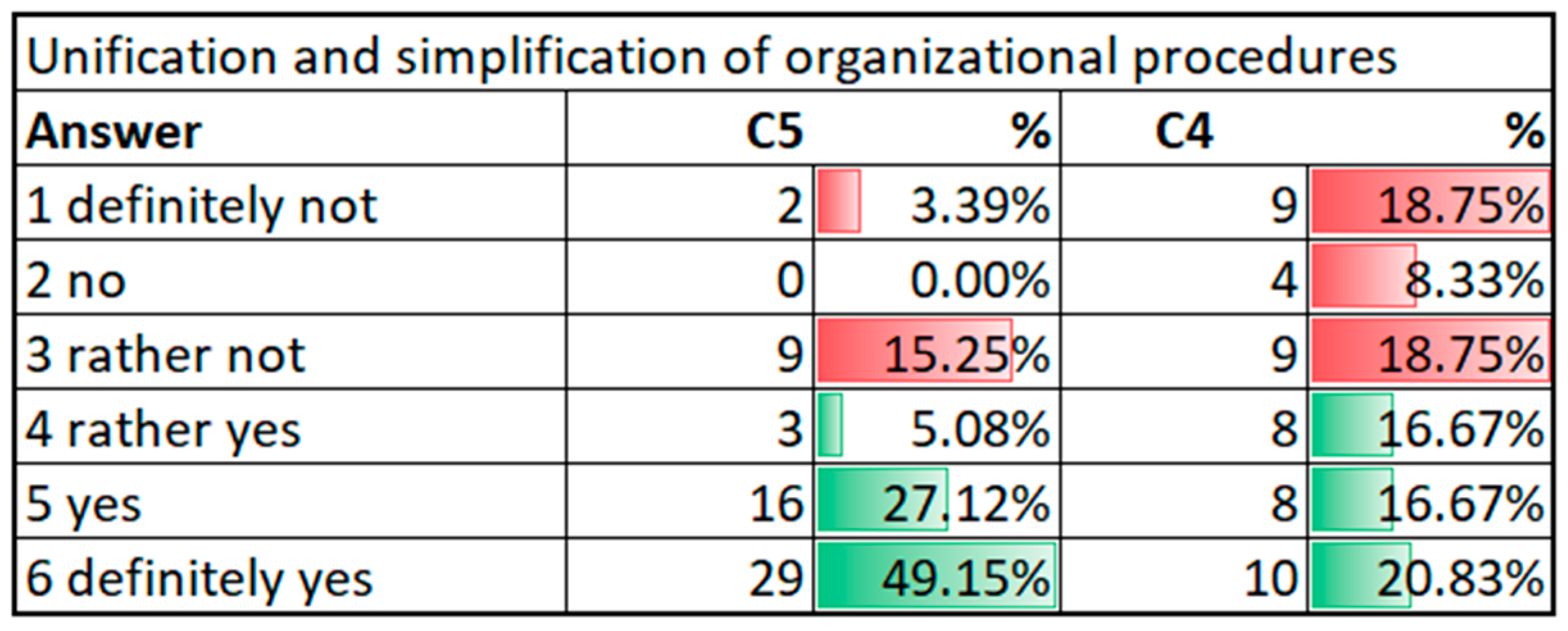

There are also significant differences in the enterprise’s answers from clusters C4 and C5 in this area. All companies from the C5 group of leaders try to improve the company’s cooperation with 44% declaring a strong commitment in this area. Better collaboration between the company’s employees also contributes to increasing their involvement in sustainable entrepreneurship activities and their innovativeness. The enterprise’s innovativeness depends on the amount of expenditure to develop new solutions and the quality of cooperation between employees. Good collaboration between the company’s employees also means a high degree of trust, mutual understanding, and a joint effort to transform the organization into a sustainable enterprise. Moreover, the simplification of organizational procedures can be considered innovative, which is related to the restructuring of processes that requires an unconventional approach. The vast majority of cluster C5 enterprises strive to simplify and standardize organizational procedures (Figure 12). Therefore, we can conclude that this feature is characteristic of sustainable enterprises.

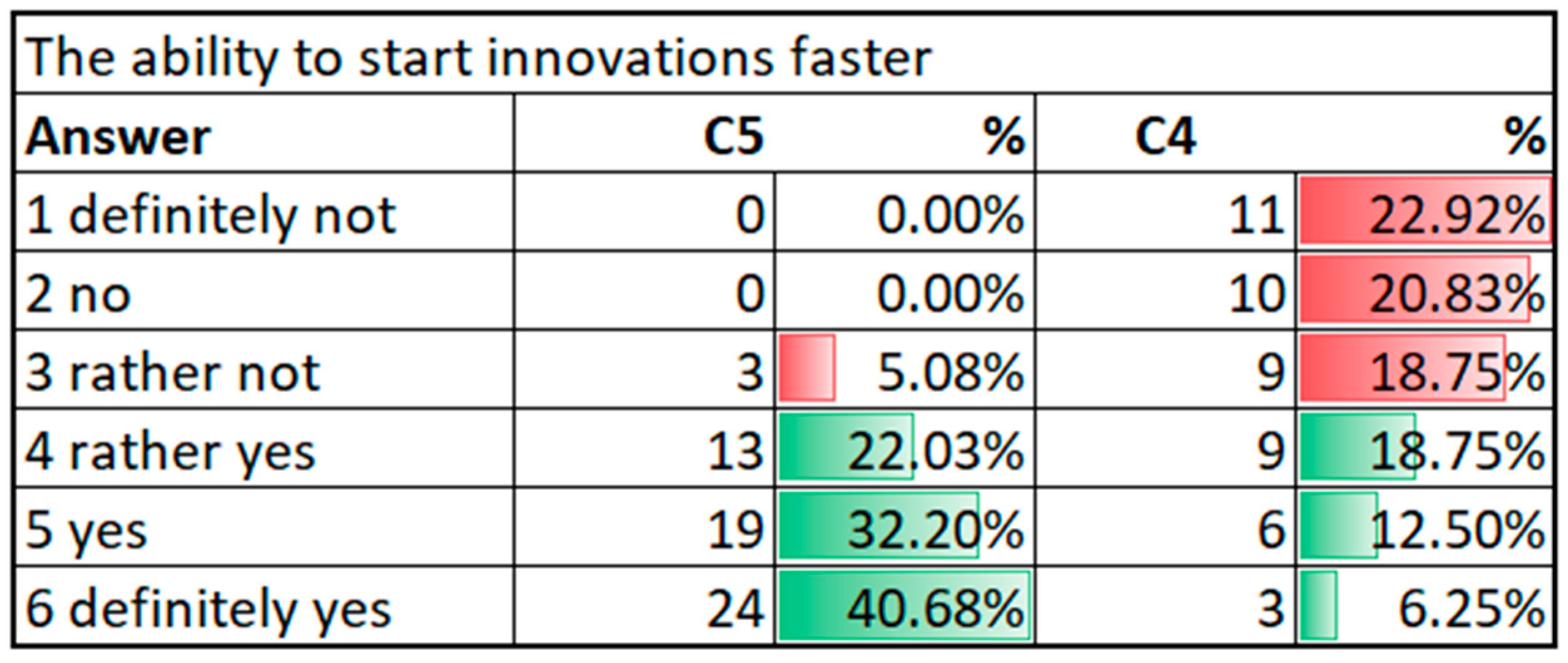

The ability to launch innovation quickly was another phenomenon studied. The answers to the question (Figure 13) directly show the enterprise’s attitudes to implementing innovations and the perception of their role in the business activity. In this area, we can notice a significant difference between companies from clusters C4 and C5.

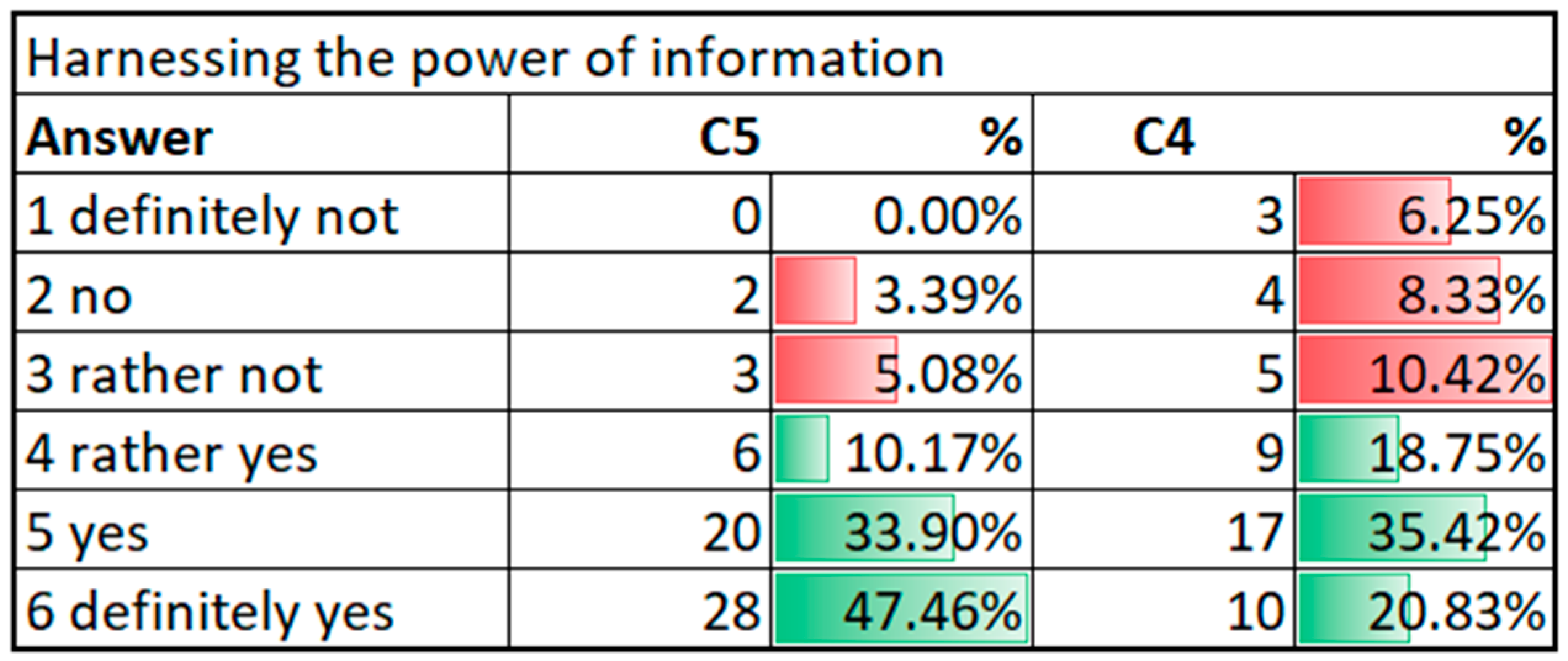

The question related to the possibility of using information, which is currently one of the most valuable sources of knowledge in a company. Figure 14 presents the answers provided by enterprises from clusters C4 and C5.

Both the acquisition and generation of information by an enterprise are associated with sustainable entrepreneurship. Information obtained from the external environment increases the employee’s knowledge, enriching the intellectual capital, enabling them to operate following sustainable entrepreneurship. On the other hand, the enterprise’s information and transfer to the external environment also affect the implementation of activities consistent with sustainable entrepreneurship, most often in the ecological and social dimensions.

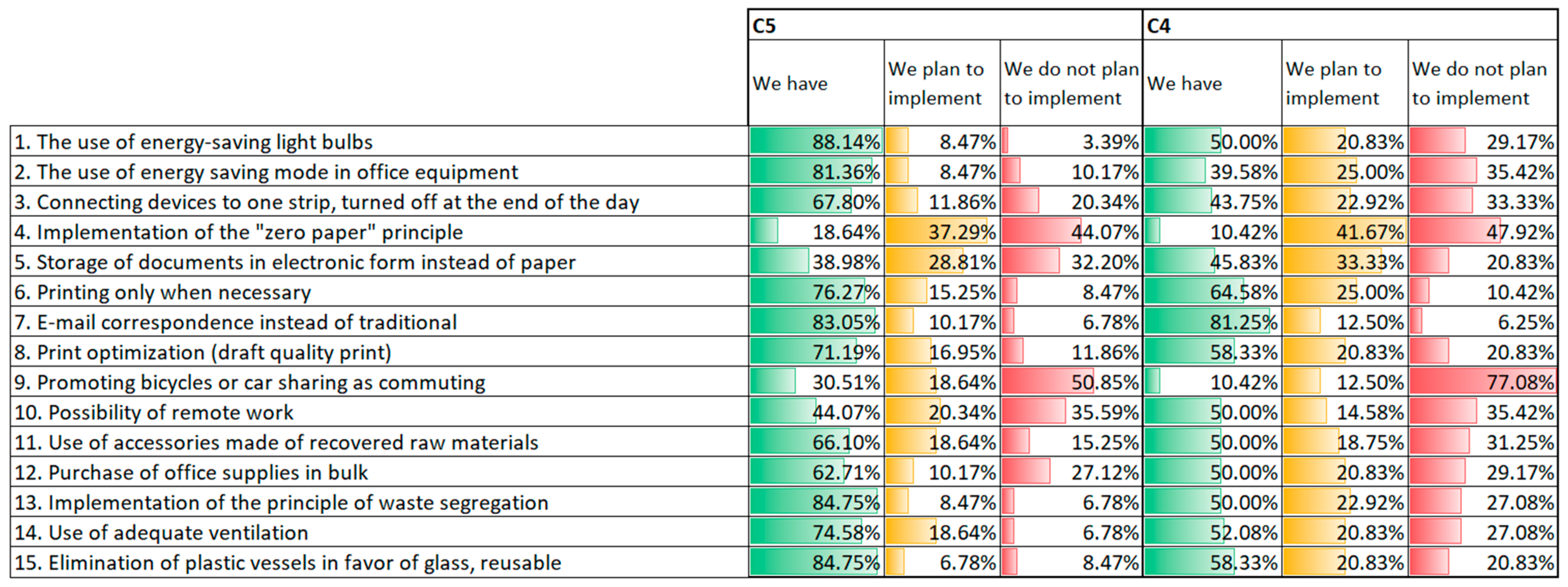

Another question was concerning ecological solutions, in line with the idea of sustainable entrepreneurship. Possible answers are: We do not have it, we plan to implement it, we have it (Figure 15). These solutions applied consistently can significantly improve the natural environment’s condition and indirectly affect the company’s image. Red color in the table means the percentage of negative answers (1–3), while green color means the percentage of positive answers (4–6). Yellow represents neutral responses.

In the case of both clusters, the answers to the questions regarding the implementation of the zero-paper principle, storing documents in electronic form rather than paper, and promoting the use of bicycles or car sharing in commuting are puzzling. As can be seen in both clusters, a small percentage of enterprises apply these principles, and many do not plan to implement them. In the first case, we should bear in mind that implementing the “zero paper” principle is almost impossible since a company operating on the market, cooperating or contacting other business entities or offices, must provide certain documents in a paper version. The implementation of this principle presupposes striving to reduce the paper consumption level rather than eliminating it, which is impossible to meet nowadays. On the other hand, the lack of intention to promote bicycles or carsharing as a means of commuting may result from the fact that enterprises are unwilling to interfere with the way employees commute to work.

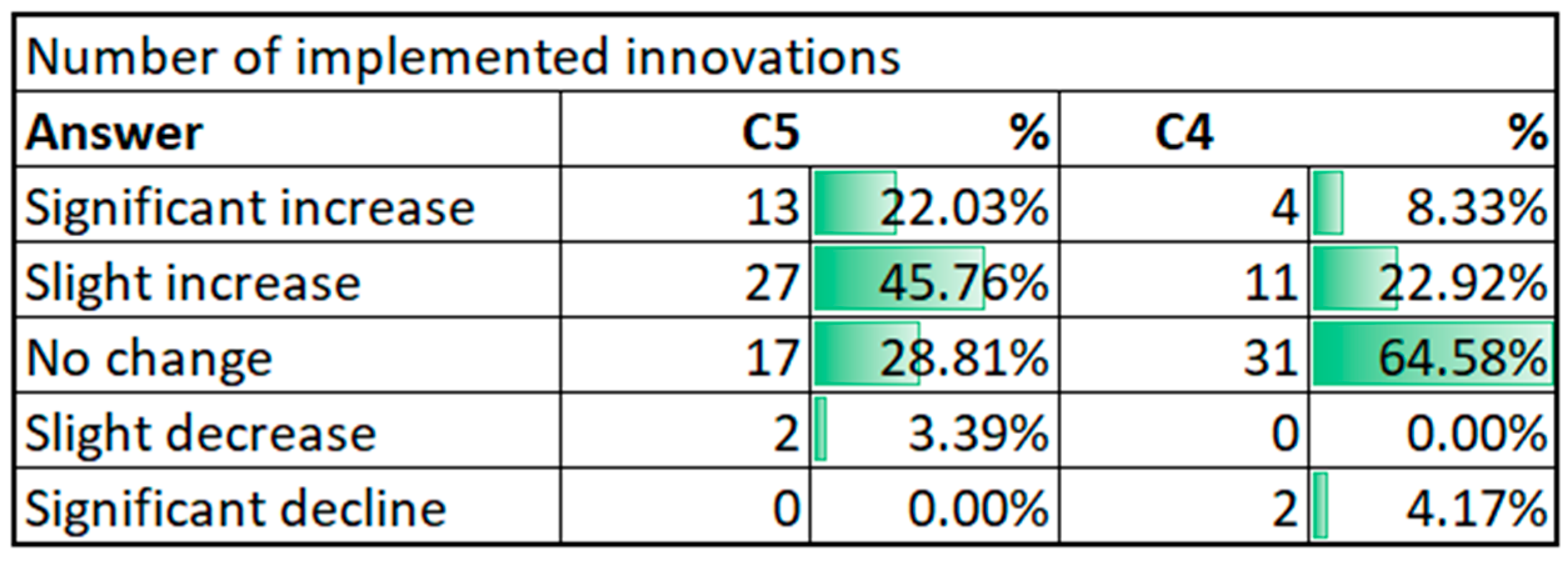

Moreover, while bicycles are becoming an increasingly popular means of transport, the idea of carsharing is still relatively new and yet rarely used. In the next step, we analyzed answers to the question concerning innovative activities. The respondent’s task was to indicate how the expenditure on innovations has developed over the last 5 years and the number of implemented innovations. The correlation coefficient between answers was 0.794933. Therefore, we decided to analyze only the question on the number of implemented innovations (Figure 16). The data bars in the table represent the percentage of respondents who marked a given answer on the questionnaire.

A certain stagnation can be seen in this issue, as almost half of the respondents indicated no change. The answers show the still low level of innovativeness of Polish enterprises. Despite access to many programs supporting innovations, Polish enterprises still show a lower expenditure on innovative activities than others in other EU countries. This outlay, amounting to 0.44% of GDP, places Poland in only the 21st place among the EU countries. Bearing in mind that innovation may be one of the determinants of sustainable entrepreneurship. It can be assumed that increasing the level of expenditure on innovative activities, resulting in a more significant number of implemented innovations, will also contribute to the complete implementation of sustainable entrepreneurship assumptions. Summing up, we can notice that enterprises from cluster C5 are more innovative, which confirms the H1 hypothesis. They more often aim at using advanced IT resources, harnessing the power of information, they want to start innovations faster, and can boast a greater number of implemented innovations.

The second analyzed aspect of activity concerning economic issues was to check how enterprises perceive their economic situation.

RQ2:

Is there a difference in the economic situation of enterprises from clusters C4 and C5?

H2:

Sustainable enterprises from cluster C5 are in a better economic situation than unsustainable enterprises from cluster C4.

RQ3:

Is there a difference in the perception of the future situation by enterprises from clusters C4 and C5?

H3:

The sustainable enterprises from cluster C5 are more optimistic about the future.

For this purpose, the answers to the following questions were interpreted:

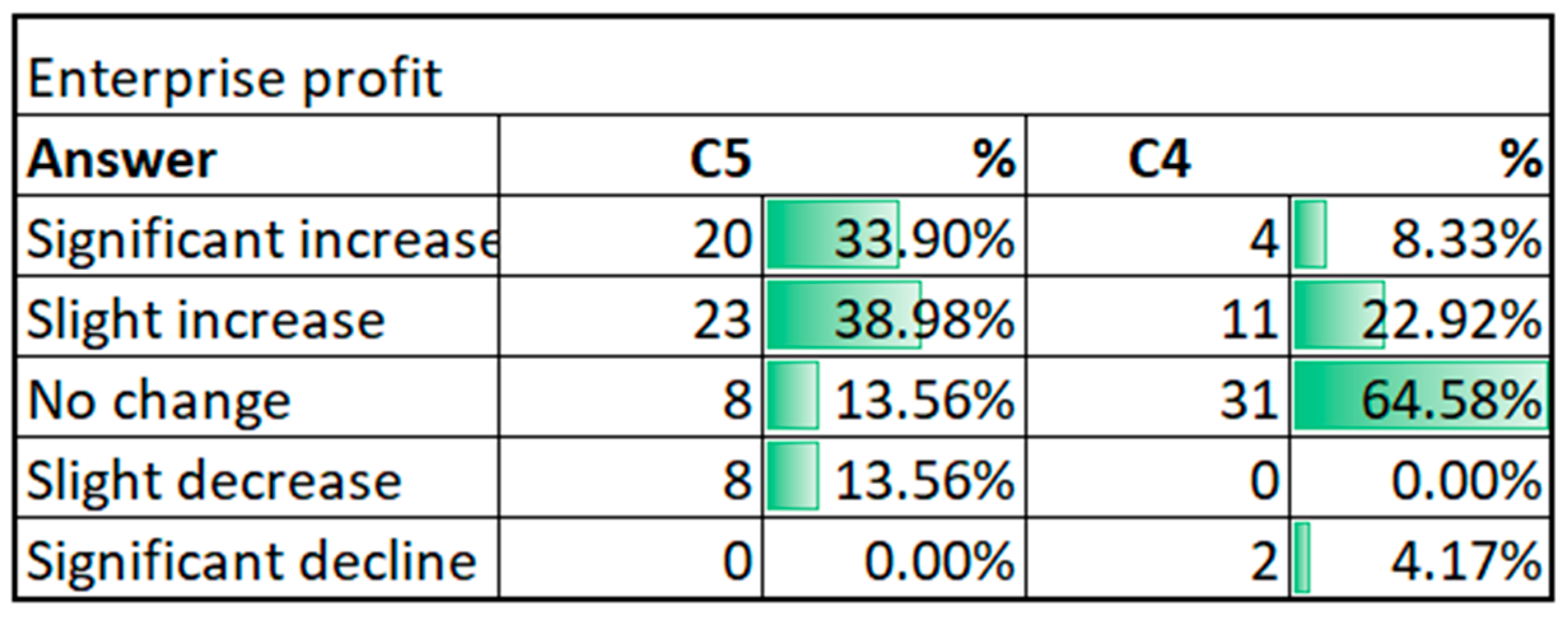

Enterprise profit for the last 5 years:

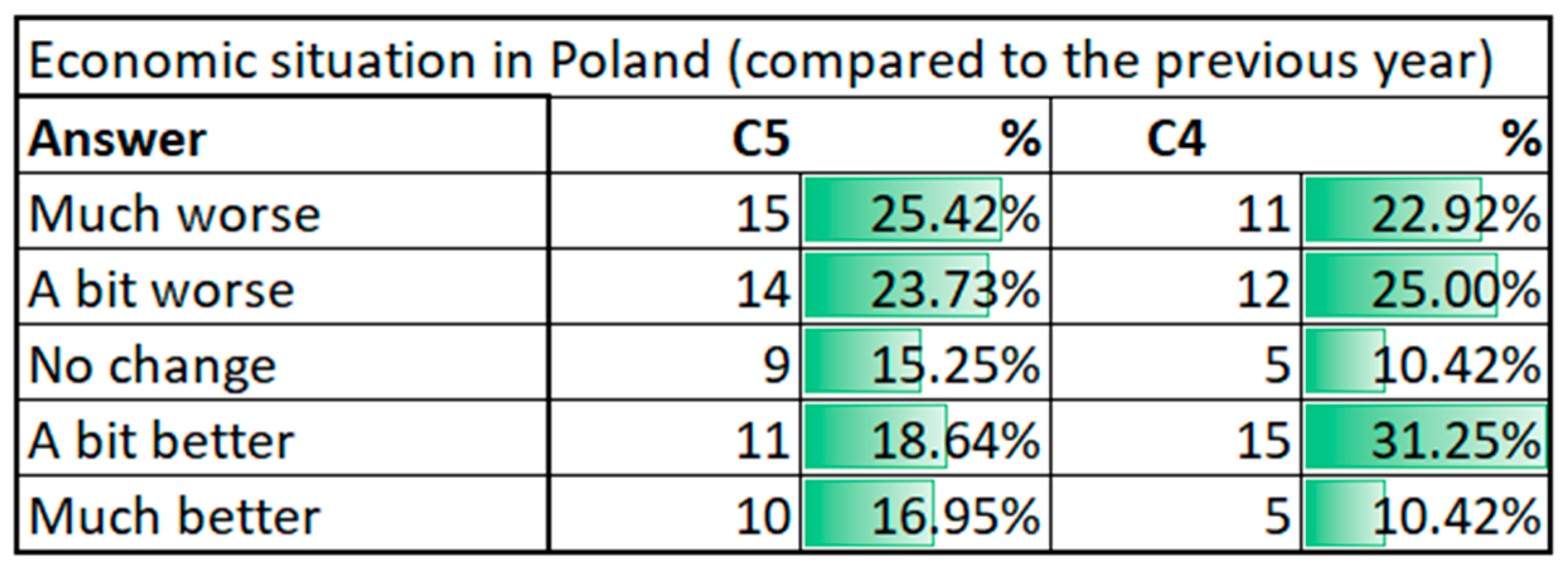

- Perception of the current economic situation in Poland compared to the previous year.

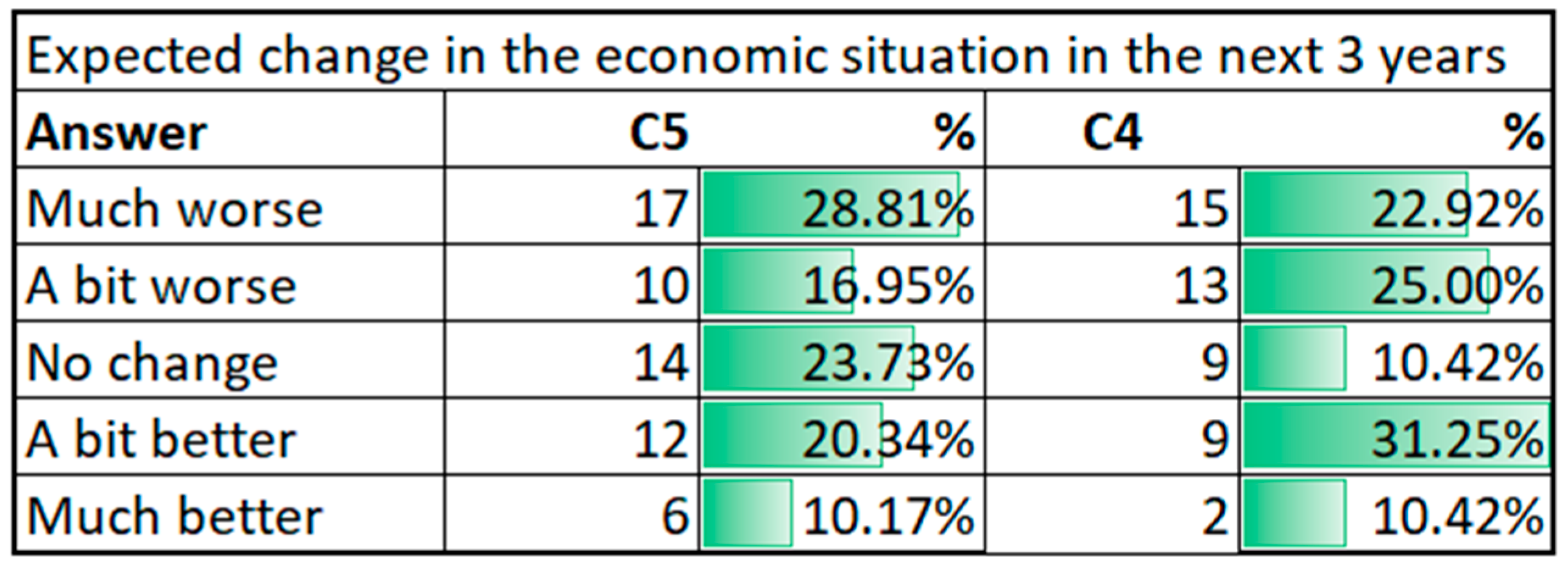

- Expected change in the economic situation in the next 3 years.

Comparing the survey results shows that companies that are leaders in sustainable entrepreneurship do much better economically. For the most part, they recorded a significant or slight increase in profit (Figure 17 and Figure 18). Therefore, the H2 hypothesis can be confirmed.

The obtained results indicate that the distribution of responses is relatively proportional. However, the lowest percentage of responses showing a significant improvement in the country’s economic situation stands out. Such various responses may result from the caution of entrepreneurs who prefer to adopt a conservative attitude (Figure 19).

Enterprises are rather pessimistic about the distant future. Almost half of the companies from both groups believe that the economic situation will deteriorate in the next 5 years. A large number believe that it will remain the same. The rest of the respondents think that the situation will improve. This perception of the future may result in the entrepreneur’s reluctance to act in line with sustainable entrepreneurship. The obtained results can also prove a conservative attitude among entrepreneurs who prefer to assume that the economic situation will deteriorate to be prepared for the worse than to assume its improvement. Therefore, hypothesis H3 on the optimistic attitude of entrepreneurs from cluster C5 should be rejected.

We also analyzed how the surveyed organizations perceive sustainable entrepreneurship in business (Figure 20).

RQ4:

Is there a difference in the perception of the role of sustainable entrepreneurship in both surveyed groups?

H4:

Enterprises from cluster C5 treat sustainable entrepreneurship as a key element of competitiveness, while the enterprises from cluster C4 do not appreciate it at all.

The content of the question was: What do you think will be the impact of Sustainable Entrepreneurship on the activities of enterprises in the next 5 years (multiple answers):

- More and more companies will carry out their activities in the spirit of sustainable entrepreneurship.

- Sustainable entrepreneurship will become the standard in which economic processes will run.

- There will be a mixing of concepts with the adjective “balanced.”

- Failure to consider the concept of sustainable entrepreneurship will contribute to the enterprise’s failure in the market.

- Sustainable entrepreneurship will also affect the attitudes of recipients of services/products offered by the enterprise.

- Sustainable entrepreneurship will contribute to increasing the level of innovation in enterprises.

- Nothing will change.

- Hard to say.

Most companies from both groups believe that more and more enterprises will implement their activities in the spirit of sustainable entrepreneurship. As it results from the literature studies, the actions that, apart from environmental effects, also have a specific economic impact, e.g., replacing light bulbs with energy-saving ones, are part of sustainable entrepreneurship. Therefore, we can assume that sustainable entrepreneurship activities will be carried out over time by every enterprise operating in the market. Many surveyed companies believe that there will be a mixture of concepts containing the adjective “sustainable.” It can be assumed that sustainable development, sustainable production, sustainable enterprises, and sustainable construction will converge, giving rise to new ideas and assumptions. Enterprises from both groups indicated that sustainable entrepreneurship would also affect the recipients of their services and products. It will contribute to disseminating a typical attitude of a sustainable consumer and the phenomenon of sustainable consumption itself. Moreover, companies believe that sustainable entrepreneurship will over time become the standard in which economic processes will run, as in the case of sustainable development, the assumptions in which now take the form of regulations or requirements that companies have to meet. Sustainable entrepreneurship will increase the innovativeness of enterprises since it will force the implementation of innovative solutions. Moreover, the enterprise’s innovativeness may translate into implementing this concept’s assumptions in the broader scope.

On the other hand, the smallest percentage of enterprises from both groups assumes that not considering the sustainable entrepreneurship’s assumptions may lead to the enterprise’s failure in the market. A detailed analysis of the answers to the survey questions allowed us to reject the H4 hypothesis. It can be concluded that enterprises in both groups perceive the role of sustainable entrepreneurship in a similar way.

The modern economic reality is highly profitable and market-oriented. Moreover, many consumers are not aware of the global need for sustainable practices and choices. Therefore, we can safely assume that a company that does not meet the principles of sustainable entrepreneurship but offers an attractive product for a reasonable price will still find customers and will be able to survive in the market and develop. However, quite a large group of respondents indicated answers such as “hard to say” and “nothing will change”, which may still show an individual ignorance of this concept, as well as a lack of willingness to implement its assumptions.

6. Discussion

As indicated by S.B. Moore and S.L. Manring [69], SMEs have a crucial role in managing scarce global environmental and social resources, thus being an essential link in the realization of sustainable entrepreneurship. P. Soto-Acosta et al. [55] assuming that sustainable entrepreneurship leads to business outcomes, examined SME entrepreneur’s views in various aspects. Emphasis was placed on the entrepreneur’s approach to people, the planet, and profit and prioritizing them in business dynamics. These dimensions mentioned above are also considered important factors affecting business outcomes in terms of turnover, customer acquisition and retention, and market share. Their results indicated that the entrepreneur’s balanced approach to people and profit has a significant positive impact on business results. The purpose of the research carried out by G. Hosseini and A. Ramezani [70] was to identify the social and environmental factors that influence sustainable entrepreneurship in small and medium-sized enterprises. The obtained results indicated that the professional experience and education of an entrepreneur contribute to sustainable entrepreneurship. Additionally, among the eight identified factors, according to the participant’s perceptions, the most important factors influencing the sustainable operation of the enterprise are social factors, including customer orientation, as well as human and environmental factors, including recycling and concern for the future of the Earth. The aim of the research carried out by G. Hosseini and A. Ramezani [70] was to identify the social and environmental factors that influence sustainable entrepreneurship in small and medium-sized enterprises. The obtained results indicated that prioritized professional experience and education contribute to the entire sustainable dimensions mentioned above. Among the eight identified factors, according to the participation, the most important factors influencing the enterprise’s sustainable operation are social factors, including customer orientation and human and environmental factors, including recycling and concern for the future of the Earth. E. Crals and L. Vereeck [41] examined why SMEs become sustainable entrepreneurs, including a positive image, motivated staff, cost-effectiveness, risk mitigation, and market opportunities when dealing with other sustainable entrepreneurs. P. Tomski and F. Manzoor’s [71] purpose was to analyze the perception of sustainable entrepreneurship by entrepreneurs who, through the analysis of the environment and companies, shape the way of operating in the field of sustainable entrepreneurship. The article’s aim by A. Gerlach [72] was to systematize the existing conceptual approaches to sustainable entrepreneurship and outline the role that sustainable entrepreneurs can play in implementing innovation. As a result, an innovation management model was proposed to define the sustainable entrepreneur’s role in sustainable development. It has also shown that sustainable entrepreneurship should consider the factors that ensure an innovative environment [34,73] and encourage the emergence of promoters and facilitate entrepreneurial behavior. In turn, E.G. Ceptureanu et al. [74] examined factors positively influencing the use of sustainable entrepreneurial opportunities, with the market orientation and sustainable entrepreneurial orientation definitely and positively influencing sustainable opportunity recognition. Whereas RJAK and Woolthius [75] studied the strategies that sustainable entrepreneurs use to interact with their environment, which led to the conclusion that entrepreneurs, in general, support the belief that sustainable entrepreneurship can contribute very well to the long-term profitability of enterprises. Similar studies were conducted by R. Runyan et al. [3] identifying patterns of social awareness presented by sustainable entrepreneurs and how they can be drawn into the process of managing natural resources. H. Nor-Aishah et al. [76] examined the effects of entrepreneurship leadership on the sustainable performance’s economic, environmental, and social aspects. This study highlighted the importance of this kind of leadership. It indicated that entrepreneurs should treat and develop their skills as a critical step towards achieving sustainable entrepreneurial performance by their enterprises. Subsequent studies have shown that sustainable entrepreneurs obtain financing from unconventional sources and use unconventional but sensible human resource management practices. They are creative in implementing their marketing strategies and are useful in conducting efficient, environmentally friendly operations. They also balance achieving their goals with ecological and social goals [7,62].

7. Conclusions

This article is a preliminary examination of the company’s situation in light of their commitment to implementing the concept of sustainable entrepreneurship. An approach to analyzing survey data using the clustering method and visualization in tables and charts was proposed. The research results obtained in this way indicate problems that require more in-depth analysis and cause-and-effect diagnosis. These analyses will focus on the diagnosis of the issues specific to industries and enterprises of various sizes.

The research aimed to determine how Polish enterprises from the SME sector perceive their activities in light of sustainable entrepreneurship, identify the critical attitudes of Polish enterprises towards sustainable entrepreneurship, and distinguish differences in enterprise’s economic activity. The cluster analysis shows that the Polish SME sector can be divided into five separate groups characterized by a distinctly different approach and level of implementation of the concept of sustainable development. The study indicates that some enterprises implement sustainable entrepreneurship only at the declarative level. However, based on the research results, we can conclude that environmental goals are a bigger problem for Polish enterprises than implementing social goals. We have also presented that enterprises that most fully implement sustainable entrepreneurship use advanced IT solutions often. They are also oriented to improving cooperation between employees, trying to standardize and simplify organizational procedures. Sustainable companies are striving to launch innovations faster. It is evidenced by the more significant number of innovations and the use of the power of information. “Leaders” are also more inclined to implement pro-ecological and pro-social activities. They show a more optimistic attitude than enterprises included in the group that implements sustainable entrepreneurship to the slightest extent.

The studies carried out by the authors make a significant contribution to the field of sustainable entrepreneurship. The results obtained provide valuable information on how entrepreneurs perceive sustainable entrepreneurship and what activities they implement. First of all, we examined whether enterprises declaring their operations as consistent with sustainable entrepreneurship pursue specific goals and actions or whether the adoption of this concept is only declarative.

The results of this research also have important implications not only for the enterprises themselves but also for decision-makers responsible for the implementation of regulations or procedures facilitating the taking of actions consistent with sustainable entrepreneurship. While “leaders”, i.e., enterprises that implement social and environmental activities most fully, may not need such guidelines, it is worth finding out how to help companies that still have problems carrying out such activities. The publication of research on sustainable entrepreneurship aims at increasing awareness of social and environmental problems faced by enterprises in Polish conditions. An exciting and forward-looking direction of the study that the authors intend to undertake is to isolate the factors that induce enterprises to pro-ecological and pro-social behaviors. The identification of such factors can help better plan educational activities and shape sustainable development policies.

Supplementary Materials

The following are available online at https://0-www-mdpi-com.brum.beds.ac.uk/article/10.3390/su13073595/s1.

Author Contributions

Conceptualization (I.P. and P.B.); Formal analysis (H.F.); Funding acquisition (I.P. and P.B.); Methodology (I.P. and P.B.); Visualization (I.P.); Writing—original draft (P.B. and H.F.); Writing—review and editing (I.P. and P.B.). All authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

Due to the large volume of data, this paper’s database is submitted as Supplementary Materials in a separate file which is a supplement/extension of this paper.

Acknowledgments

The realization of this paper has been supported by partial results of the project SDG4 BIZ “Knowledge Alliance for Business Opportunity Recognition in SDGs” (no. 621458-EPP-1-2020-1-FI-EPPKA2-KA).

Conflicts of Interest

The authors declare no conflict of interest.

References

- Venkataraman, S. The distinctive domain of entrepreneurship. Adv. Entrep. Firm Emerg. Growth 1997, 3, 119–138. [Google Scholar]

- Moroz, P.W.; Hindle, K. Entrepreneurship as a process: Toward harmonizing multiple perspectives. Entrep. Theory Pract. 2012, 36, 781–818. [Google Scholar] [CrossRef]

- Runyan, R.; Droge, C.; Swinney, J. Entrepreneurial orientation versus small business orientation: What are their relationships to firm performance? J. Small Bus. Manag. 2008, 46, 567–588. [Google Scholar] [CrossRef]

- Hockerts, K.; Wüstenhagen, R. Greening Goliaths versus emerging Davids: Theorizing about the role of incumbents and new entrants in sustainable entrepreneurship. J. Bus. Ventur. 2010, 25, 481–492. [Google Scholar] [CrossRef]

- Kuckertz, A.; Wagner, M. The influence of sustainability orientation on entrepreneurial intentions: Investigation the role of business experience. J. Bus. Ventur. 2010, 25, 524–539. [Google Scholar] [CrossRef]

- Pacheco, D.F.; Dean, T.J.; Payne, D.S. Escaping the green prison: Entrepreneurship and the creation of opportunities for sustainable development. J. Bus. Ven. 2010, 25, 464–480. [Google Scholar] [CrossRef]

- Carayannis, E.G.; Provance, M.; Givens, N. Knowledge arbitrage, serendipity, and acquisition formality: Their effects on sustainable entrepreneurial activity in regions. IEEE Trans. Eng. Manag. 2011, 58, 564–577. [Google Scholar] [CrossRef]

- Ploum, L.; Blok, V.; Lans, T.; Omta, O. Exploring the relation between individual moral antecedents and entrepreneurial opportunity recognition for sustainable development. J. Clean. Prod. 2018, 172, 1582–1591. [Google Scholar] [CrossRef]

- Ramos-González, M.M.; Rubio-Andrés, M.; Sastre-Castillo, M.Á. Building corporate reputation through sustainable entrepreneurship: The mediating effect of ethical behavior. Sustainability 2017, 9, 1663. [Google Scholar] [CrossRef]

- Fellnhofer, K.; Kraus, S.; Bouncken, R. Sustainable entrepreneurship: A current review of literature. Int. J. Bus. Res. 2014, 14, 163–172. [Google Scholar] [CrossRef]

- Tur-Porcar, A.; Roig-Tierno, N.; Mestre, A.L. Factors affecting entrepreneurship and business sustainability. Sustainability 2018, 10, 452. [Google Scholar] [CrossRef]

- Schaltegger, S.; Wagner, T. Types of Sustainable Entrepreneurship and Conditions for Sustainability Innovation: From the Administration of a Technical Challenge to the Management of an Entrepreneurial Opportunity. In Sustainable Innovation and Entrepreneurship; Wüstenhagen, R., Hamschmidt, J., Sharma, S., Starik, M., Eds.; Edward-Elgar: Cheltenham, UK, 2011; pp. 27–48. [Google Scholar]

- Laszuk, M. Rozwój przedsiębiorczości w instytucji publicznej—Aktywizacja menedżerów. In Przedsiębiorczość, Jednostka, Organizacja, Kontekst; Postuła, A., Majczyk, J., Darecki, M., Eds.; Wydawnictwo Naukowe Wydziału Zarządzania Uniwersytetu Warszawskiego: Warsaw, Poland, 2015; pp. 50–67. [Google Scholar]

- Hall, J.K.; Daneke, G.A.; Lenox, M.J. Sustainable development and entrepreneurship: Past contributions and future directions. J. Bus. Ventur. 2010, 25, 439–448. [Google Scholar] [CrossRef]

- Koe, W.-L.; Majid, I.A. Socio-cultural factors and intention towards sustainable entrepreneurship. Eurasian J. Bus. Econ. 2014, 7, 145–156. [Google Scholar]

- Melay, I.; Kraus, S. Green entrepreneurship: Definitions of related concepts. Int. J. Strategy Manag. 2012, 12, 1–13. [Google Scholar]

- Schaefer, K.; Corner, P.D.; Kearins, K. Social, environmental and sustainable entrepreneurship research what is needed for sustainability-as-flourishing? Organ. Environ. 2015, 28, 394–413. [Google Scholar] [CrossRef]

- Dean, T.J.; McMullen, J.F. Towards a theory of sustainable entrepreneurship: Reducing environmental degradation through entrepreneurial action. J. Bus. Ventur. 2007, 22, 50–76. [Google Scholar] [CrossRef]

- Dixon, S.E.A.; Clifford, A. Ecopreneurship: A new approach to managing the triple bottom line. J. Organ. Chang. Manag. 2007, 20, 326–345. [Google Scholar] [CrossRef]

- Kraus, S.; Burtscher, J.; Niemand, T.; Roig-Tierno, N.; Syrjä, P. Configurational Paths to Social Performance in SMEs: The Interplay of Innovation, Sustainability, Resources and Achievement Motivation. Sustainability 2017, 10, 444. [Google Scholar] [CrossRef]

- Gundry, L.K.; Kickul, J.R.; Gri_ths, M.D.; Bacq, S.C. Creating Social Change Out of Nothing: The Role of Entrepreneurial Bricolage in Social Entrepreneurs’ Catalyst Innovations. Soc. Sustain. Entrep. 2011, 13, 1–24. [Google Scholar]

- Geissdoerfer, M.; Savaget, P.; Bocken, N.M.P.; Hultink, E.J. The Circular Economy—A new Sustainability Paradigm? J. Clean. Prod. 2017, 143, 757–768. [Google Scholar] [CrossRef]

- Patzelt, H.; Shepherd, D.A. Recognizing opportunities for sustainable development. Entrep. Theory Pract. 2011, 35, 631–652. [Google Scholar] [CrossRef]

- Ejlal, M.; Seyed, M.Z.; Rialp-Criado, A. International ecopreneurs: The case of eco-entrepreneurial new ventures in the renewable energy industry. J. Int. Entrep. 2019, 17, 103–126. [Google Scholar]

- Galkina, T.; Hultman, M. Ecopreneurship: Assessing the field and outlining the research potential. Small Enterp. Res. 2016, 23, 58–72. [Google Scholar] [CrossRef]

- Gibbs, D. Sustainability entrepreneurs, ecopreneurs and the development of a sustainable economy. Greener Manag. Int. 2006, 55, 63–78. [Google Scholar] [CrossRef]

- Isaak, R. The making of the ecopreneur. Greener Manag. Int. 2002, 38, 81–91. [Google Scholar] [CrossRef]

- Alarifi, G.; Robson, P.; Kromidha, E. The Manifestation of Entrepreneurial Orientation in the Social Entrepreneurship Context. J. Soc. Entrep. 2019, 10, 307–327. [Google Scholar] [CrossRef]

- Austin, J.; Stevenson, H.; Wei-Skillern, J. Social and Commercial Entrepreneurship: Same, Different, or Both? Entrep. Theory Pract. 2006, 30, 1–22. [Google Scholar] [CrossRef]

- Bornstein, D. How to Change the World: Social Entrepreneurs and the Power of New Ideas; Oxford University Press: New York, NY, USA, 2004; pp. 154–157. [Google Scholar]

- Jackson, S.; Maleganos, J.; Alamantariotou, K. Lessons from sustainable entrepreneurship towards social innovation in healthcare: How green buildings can promote health and wellbeing. Sus. Entrep. Soc. Inn. 2016, 2, 143–169. [Google Scholar]

- Cohen, B.; Winn, M.I. Market imperfections, opportunity and sustainable entrepreneurship. J. Bus. Ventur. 2007, 22, 29–49. [Google Scholar] [CrossRef]

- Shepherd, D.A.; Patzelt, H. The new field of sustainable entrepreneurship: Studying entrepreneurial action linking what is to be sustained with what is to be developed. Entrep. Theory Pract. 2001, 35, 137–163. [Google Scholar] [CrossRef]

- Schaltegger, S.; Wagner, M. Sustainable entrepreneurship and sustainability innovation: Categories and interactions. Bus. Strategy Environ. 2011, 20, 222–237. [Google Scholar] [CrossRef]

- Young, W.; Tilley, F. Can Businesses Move Beyond Efficiency? The Shift toward Effectiveness and Equity in the Corporate Sustainability Debate. Bus. Strategy. Environ. 2006, 15, 402–415. [Google Scholar] [CrossRef]

- Masurel, E. Why SMEs invest in environmental measures: Sustainability evidence from small and medium-sized printing firms. Bus. Strategy Environ. 2007, 16, 190–201. [Google Scholar] [CrossRef]

- Grudzewski, W.; Hejduk, I. Przedsiębiorstwo przyszłości. Zmiany paradygmatów zarządzania. Master Bus. Adm. 2011, 1, 95–111. [Google Scholar]

- Santos, G.; Rebelo, M.; Barros, S.; Pereira, M. Certification and Integration of Environment with Quality and Safety—Path to Sustained Success; Intech Open Access Publisher: Rijeka, Croatia, 2012. [Google Scholar]

- Hubbard, G. Measuring organizational performance: Beyond the triple bottom line. Bus. Strategy Environ. 2009, 18, 177–191. [Google Scholar] [CrossRef]

- Zairi, M.; Peters, J. The impact of social responsibility on business performance. Manag. Audit. J. 2002, 17, 174–178. [Google Scholar] [CrossRef]

- Crals, E.; Vereeck, L. The affordability of sustainable entrepreneurship certification for SMEs. Int. J. Sustain. Dev. World Ecol. 2005, 12, 173–183. [Google Scholar] [CrossRef]

- Pinchot, G. Intrapreneuring; Gabler: Wiesbaden, Germany, 1998. [Google Scholar]

- Gapp, R.; Fisher, R. Developing an intrapreneur-led three-phase model of innovation. Int. J. Entrep. Behav. Res. 2007, 13, 330–348. [Google Scholar] [CrossRef]

- Kot, S. Sustainable Supply Chain Management in Small and Medium Enterprises. Sustainability 2018, 4, 1143. [Google Scholar] [CrossRef]

- Small and Medium Enterprises (SMEs) Finance. Improving SMEs’ Access to Finance and Finding Innovative Solutions to Unlock Sources of Capital. Available online: https://www.worldbank.org/en/topic/smefinance (accessed on 30 November 2020).

- Annual Report 2020: Transformation. Available online: https://www.ifc.org/wps/wcm/connect/corp_ext_content/ifc_external_corporate_site/annual+report/download (accessed on 27 October 2020).

- Williamson, D.; Lynch-Wood, G.; Ramsay, J. Drivers of Environmental Behaviour in Manufacturing SMEs and the Implications for CSR. J. Bus. Ethics 2006, 67, 317–330. [Google Scholar] [CrossRef]

- Enhancing the Contributions of SMEs in a Global and Digitalised Economy. Available online: https://www.oecd.org/industry/C-MIN-2017-8-EN.pdf (accessed on 27 October 2020).

- Raport o Stanie Sektora Małych i Średnich Przedsiębiorstw w Polsce. Available online: https://www.parp.gov.pl/storage/publications/pdf/ROSS-2020_30_06.pdf53 (accessed on 27 October 2020).

- Available online: https://stats.oecd.org/glossary/detail.asp?ID=3123 (accessed on 5 December 2020).

- User Guide to the SME Definition. Available online: https://ec.europa.eu/regional_policy/sources/conferences/state-aid/sme/smedefinitionguide_en.pdf (accessed on 5 December 2020).

- Nowa Definicja, M.Ś.P. Available online: https://www.parp.gov.pl/files/74/87/1155.pdf (accessed on 6 December 2020).

- Belz, F.M.; Binder, J.K. Sustainable entrepreneurship: A convergent process model. Bus. Strategy Environ. 2015, 26, 1–17. [Google Scholar] [CrossRef]

- Sung, C.S.; Park, J.Y. Sustainability Orientation and Entrepreneurship Orientation: Is There a Tradeo_Relationship between Them? Sustainability 2018, 10, 379. [Google Scholar] [CrossRef]

- Soto-Acosta, P.; Cismari, D.M.; Vatamanescu, E.-M.; Ciochina, R.S. Sustainable Entrepreneurship in SMEs: A Business Performance Perspective. Sustainability 2016, 8, 342. [Google Scholar] [CrossRef]

- Edgeman, R. Sustainable Enterprise Excellence: Towards a framework for holistic data-analytics. Corp. Gov. Int. J. Bus. Soc. 2013, 13, 527–540. [Google Scholar] [CrossRef]

- Richomme-Huet, K.; De Freyman, J. What sustainable entrepreneurship looks like: An exploratory study from a student perspective. In Social Entrepreneurship Leveraging Economic, Political, and Cultural Dimensions; Springer: Berlin, Germany, 2011; pp. 155–178. [Google Scholar]

- Brown, S. Likert Scale Examples for Surveys; Iowa State University Extension: Ames, IA, USA, 2010. [Google Scholar]

- Chomeya, R. Quality of Psychology Test between Likert Scale 5 and 6 Points. J. Soc. Sci. 2010, 6, 399–403. [Google Scholar]

- Chang, L. A Psychometric Evaluation of 4-Point and 6-Point Likert-Type Scales in Relation to Reliability and Validity. Appl. Psychol. Meas. 1994, 18, 205–215. [Google Scholar] [CrossRef]

- Thompson, C. The Case for the Six-Points Likert Scale, Quantum Workplace. Available online: https://www.quantumworkplace.com/future-of-work/the-case-for-the-six-point-likert-scale (accessed on 10 December 2019).

- Choi, D.Y.; Gray, E.R. The venture development processes of “sustainable” entrepreneurs. Manag. Res. News 2008, 31, 558–569. [Google Scholar] [CrossRef]

- Majid, I.A.; Koe, W.L. Sustainable Entrepreneurship (SE): A Revised Model Based on Triple Bottom Line (TBL). Int. J. Acad. Res. Bus. Soc. Sci. 2012, 2, 293–310. [Google Scholar]

- O’Neill, G.D., Jr.; Hershauer, J.C.; Golden, J.S. The cultural context of sustainability entrepreneurship. Greener Manag. Int. 2009, 55, 33–46. [Google Scholar] [CrossRef]

- De Palma, R.; Dobes, V. An integrated approach towards sustainable entrepreneurship—Experience from the TEST project in transitional economies. J. Clean. Prod. 2010, 18, 1807–1821. [Google Scholar] [CrossRef]

- Katsikis, I.N.; Kyrgidou, L.P. The concept of sustainable entrepreneurship: A conceptual framework and empirical analysis. In Proceedings of the Academy of Management 2007 Annual Meeting: Doing Well by Doing Good, AOM 2007, Philadelphia, PA, USA, 3–8 August 2007. [Google Scholar]

- Demsar, J.; Curk, T.; Erjavec, A.; Gorup, C.; Hocevar, T.; Milutinovic, M.; Mozina, M.; Polajnar, M.; Toplak, M.; Staric, A.; et al. Orange: Data Mining Toolbox in Python. J. Mach. Learn. Res. 2011, 14, 2349–2353. [Google Scholar]

- Action Strategy of the National Fund for Environmental Protection and Water Management for 2013–2016 with a View to 2020. Available online: http://nfosigw.gov.pl/en/nfepwm/strategy/ (accessed on 6 December 2020).