Tax Rate of Management Control: The Mexican Income Tax Rates System for Resident and Non-Residents

1

Dirección de Investigación, Universidad La Salle México, Ciudad de México 06140, Mexico

2

Instituto de Investigaciones Económicas, UNAM, Ciudad de México 04510, Mexico

*

Author to whom correspondence should be addressed.

Sustainability 2021, 13(16), 9202; https://0-doi-org.brum.beds.ac.uk/10.3390/su13169202

Submission received: 29 June 2021

/

Revised: 17 July 2021

/

Accepted: 23 July 2021

/

Published: 17 August 2021

(This article belongs to the Special Issue Sustainability and Management Information and Control Systems)

Abstract

:The aim of this study is to show the tax rate of management control of the legislation according to the tax residence of the people who obtain income from wages. The questions considered here are: Is the income tax rate applied to national resident workers and to residents abroad proportionally? Under the same circumstances, in both cases do they pay similar amounts? The empirical analysis was based on the evaluation of the income tax and tax rate of management control in Mexico based on the Suits progressivity index. It was found that, under similar conditions, the amount of the tax to be paid by a resident abroad is less than that paid by a national resident.

1. Introduction

A recurring topic in the tax literature is the principles that rule the establishment of a tax. The main objective of the changes that take place in fiscal law is to increase government revenue. Occasionally, this is carried out whilst disregarding mandatory precepts. According to doctrine, the Congress has the faculty to impose the necessary taxes to cover the budget. This is the case of Mexico, but it may be different in other jurisdictions. Due to its taxation nature, this process originated in the lower chamber whose members represent the majority of people. In the last ten years, tax income has grown. In Mexico, from 2010 to 2020, collection increased by 206.3%, while tax collection did so by 278.1%. The increase in income tax (Impuesto Sobre la Renta, ISR) rose by 295.7%, becoming the tax with the highest levy when compared to others [1]. This increase is largely due to tax withholding of 34,918,517 employed taxpayers who represent 76% of the federal registry of taxpayers. This registry includes 11,826 taxpayers who do not permanently live in Mexico: natural persons who receive salaries abroad but pay taxes because the origin of their wealth is located in Mexico. These taxpayers are the subjects of our research.

According to the Organization for Economic Cooperation and Development (OECD), in Mexico, the “government income mostly depended on oil” [2] (p. 67). However, this criterion changed according to data from the tax management control of the Ministry of Finance and Public Credit. In 2020, the budget revenue estimated to collect 3 billion 505.8 million Mexican pesos in income tax. Tax management control reported that it collected 3 billion million Mexican pesos, which includes an income tax of 1 billion 762.9 million Mexican pesos, including big companies (40.07%) and natural persons (2.53%), withholding wages (56.96%) and including foreign income [3] (p. 6). Tax management control collected 1 billion million Mexican pesos by withholding wages (Impuesto Sobre la Renta, ISR) [3] (p. 10) from taxpayers who provide a subordinate personal service and natural persons in a labor relationship (employer–employee). The latter were the taxpayer group that contributed the most to government revenue in that year and made sustainability possible in public finances.

As another author has mentioned [4], tax management control may differ in progressivity and the effects between employees and business owners, but the key point is to understand the following questions: Are taxpayers of this tax regime the ones who should contribute the most to public expenditure? Additionally, is the contribution to public expenditure provided by taxpayers in this tax regime proportional to their economic capacity without harming their quality of life?

The establishment of a tax is regulated by a tax system that, naturally, involves compliance with constitutional principles, among which is the principle of proportionality (progressivity) and equity, described in Article 31, Section 4, of the Federal Political Constitution [5]. Previous studies provide evidence on the implementation of such constitutional principles [6], where the obligation to contribute to expenditure is included, according to the principle of proportionality, making a difference between tax rates from fiscal residence, whether in Mexico or abroad. Bosses or employers are liable to tax payments; therefore, their obligation is to withhold their employees’ taxes and report the moment that salaries are given to them. To comply with such an obligation, tax withholding involves applying a monthly (annual) rate whose fiscal technique, by doctrine, should comply with the constitutional principle of proportionality, bound by the principle of equality; both are principles of a higher order on which the Mexican tax system is based.

Tax withholding of a natural person living in Mexico involves applying the progressive rate. The fixed rate is added to the lower limit of the income received. For residents who live abroad, the tax rate is proportional. Firstly, an exemption is applied to the income received according to the established limit. Two tax rates are applied to the remaining amount, depending on the income established by law. Both cases include the implementation of the principle of proportionality as established by the income tax law (Ley del Impuesto Sobre la Renta, LISR) [7]. These are the legal principles that motivate our research questions: Is the tax withholding determined with the progressive rate for a person living in Mexico the same as the one determined with a tax rate for a resident living abroad? Does the monthly (annual) rate of a person living in Mexico have the same fiscal meaning as the tax rates for a resident who lives abroad? Do the constitutional progressivity and proportionality [5] limits effectively withhold the tax without harming the human right to the vital minimum?

This study aims to show the behavior of the monthly (annual) rate in tax withholding of a natural person living in Mexico who receives income from salaries granted for a subordinate personal service, as established by Article 96 of the income tax law LISR. We compare that rate against the tax rates of tax withholding applied to a natural person living abroad who receives income from a salary granted for a subordinate service as stated in Article 154 of the income tax law [7], applying the constitutional principle of proportionality (progressivity), according to the salary tax system, and considering the fiscal residence of the subjects studied. We also consider the effect that the implementation of this principle (proportionality–progressivity) has on the taxpayer’s quality of life [5]. The hypothesis is that income tax withholding of natural persons who obtain income for providing a subordinate personal service and live abroad is lower because the rates applied to them follow the principle of proportionality regarding their income. On the contrary, the monthly (annual) rate applied to the tax withholding of a natural person living in Mexico who receives income for providing a subordinate service follows the principle of progressivity. According to doctrine, the second one violates the human right to the vital minimum.

2. Review Literature

We review the information as required by the doctrine. We compile economic– theoretical–legal information in laws, codes, regulations, and other dispositions using the legislative and newspaper research techniques [8]. We study the literature on the figure of tax determination considering income from salary, according to human rights and theoretically legally based on the human right to the vital minimum within the constitutional limits of fiscal matters. We know the tax rates established by legislation to identify the percentages to be applied when determining the tax to withhold from employees, according to their fiscal residence. We review the Official Journals of the Federation to find the origin of the constitutional limits of proportionality and the implementation of the principle [5], Ley del Impuesto Sobre la Renta [7], across the tax history of Mexico.

In Mexico, the need to pay taxes is established by the fiscal residence. Natural persons who receive salaries are forced to pay income tax on all their income, regardless of the location of the source of wealth. In the case of residents living abroad, the obligation remains for those taxpayers who receive an income from a permanent establishment or one whose source of wealth is located in Mexico, when they are not permanently settled in the country, or when they live in Mexico, but their income is not originated in the country (Article 1) [7]. According to these ideas, residents living abroad who receive income from any source of wealth located in the country or have a permanent establishment in the country must pay taxes in Mexico. Natural persons who are Mexican citizens are considered to be residents in Mexico unless proven otherwise.

One of the concerns of the first marketers was understanding the ways to increase wealth; one of them is through international trade [9]. The school of marketers thought the State must intervene in international trade to increase collection by promoting exportations “through the creation of duties” [10] (p. 90). Physiocrats shared the same interest, although they directed it towards agriculture. Both held that wealth affects economic growth and aimed for these variables to affect taxation. The classics also studied wealth in economic growth, as did Adam Smith, who added the variable of “accumulation of factors of production”. The theoretician stated that the origin of wealth “is found both in labor and available resources” [10] (p. 91) and made a relevant contribution to the declaration of principles that should guide the creation of the tax structuring that have since been applied. Smith considered that the obligation to contribute had always been bound to “the acknowledgement of a set of basic principles that guided taxation”. This criterion was supported by Adolph Wagner, Harold M. Sommers, and Neumark Frits [11]. Adam Smith explained his theory of justice defining taxation as an “amount or percentage of private wealth that citizens must deliver under equality criteria” [12] (p. 143). Marin-Barnuevo also acknowledges it when stating before the Spanish Court the following axiom in the 2 April ruling , in which the doctrine of previous years is summarized: “the principle of equality demands that equal legal consequences are applied to equal budgets” [13] (p. 46).

The principle of justice or proportionality presented by Smith considers that this principle is inherent to the individual’s economic capacity. Tax proportionality is directly proportional to tax capacity. This is an economic reason to pay a reasonable proportion of the tax and a constitutional limit to establish the tax. Arnold, Martinez and Zuñiga [14] (p. 68) state that “proportionality became a constitutional principle that protects fundamental rights”. If the income capacity is higher, then there is a higher tax. If more wealth is obtained, then the tax rate will be higher; then, there will be a higher tax payment.

Based in an economic–political and legal system, it establishes a link between the State and the individual; this principle has been considered to have the highest regulatory status. The establishment of a tax carries the constitutional principles (obligation, generality, relation with public expenditure, proportionality, equality, and legality) [5] to be applied. These principles are often protection mechanisms when establishing a tax and, even though they are integrally relevant, we will only consider the principle of proportionality [15]. This is why there are authors who argue that income taxes have less effect, and lead to lower income inequality [16].

Burgoa [17] asserts that proportionality contains taxation elements that demonstrate wealth and that neutralize tax capacity. Then, the economic capacity of the individual determines the amount of tax. In this sense, the tax is inherent to the income. Sanchez underlines the principle of proportionality as the “most important methodological [tool] of constitutionalism” [18] (p. 471), which becomes the constitutional tax limit in a body of control under the faculty of the State.

When the tax principle is applied, the Supreme Court of Justice states that the principle of proportionality is fulfilled “through progressive rates since with them a higher amount of tax is covered by the taxpayers with the highest resources while a smaller tax is paid by taxpayers with lower incomes. In addition, a consistent difference between the levels of income is established” [19].

On the other hand, Article 31, the Constitution of the Mexican United States [5], includes the basis of the right to the vital minimum. This is the guideline for tax legislators “after which they should refrain from imposing taxes to certain concepts or incomes whenever that implies leaving the person without any medium to subsist”. The right to the vital minimum as an expression of the principle of tax proportionality includes all those incomes destined to satisfy the individual’s essential needs and that are not part of the tax capacity. The vital minimum is a principle derived as a projection of the principle of tax proportionality, which identifies the taxpayer’s tax capacity and, at the same time, respects the resources necessary to subsist [20]. It is the result of the principles of the social state of law, human dignity, and solidarity linked to the fundamental rights to life, personal integrity, and equality. The aim of the vital minimum is to “prevent a person from having his or her intrinsic value as a human reduced due to the lack of material conditions that allow for having a decent existence” [21]. According to Tenorio, this right seeks to guarantee that the person “does not become an instrument to other ends […] aiming to protect the person from any form of degradation that compromises his or her intrinsic value, namely regarding basic and essential material conditions to ensure a decent and autonomous survival”.

The Supreme Court of Justice of the Nation has recognized that the right to the vital minimum transcends tax, respecting human dignity stated in Article 25 of the Constitution, becoming a limit for the legislator to impose a tax which “constitutes a guarantee based on human dignity” [22]. It explains that tax capacity must be appreciated based on the person’s real context given that the principle individualizes the persons’ situations and “the State, in terms of disposition, cannot overrule the necessary material resources to have a decent life”, especially when these people have the right to subsist [23].

The pro homine principle is enshrined in Article 29 of the American Convention on Human Rights [24] and considers “recurring to the widest norm, or the most extensive interpretation when dealing with the recognition of protected rights” [25] (p. 92), a principle that is consistent with the first article in the Political Constitution of the Mexican United States regarding norms on human rights interpreted with the Constitution and international treaties so that persons receive the widest protection. Understanding the criterion of this fundamental principle, along with the inherent pro homine principle, Orozco considers that “the norm that represents the greatest protection for the person or that involves the least restriction must prevail”. In this sense, human rights in the constitutional text are materialized, along with those established in the international treaties ratified by the State.

Aguilera and López consider the State as a “legitimized medium to guarantee the fundamental rights of the citizens and is politically illegitimate if it does not” [26] (p. 55). This is the main objective of the protective model when it provides effectiveness and seeks to guarantee fundamental rights. From the expression of L. Ferrajoli, the protective model is conceptualized in three manners: a model of rule of law, law theory, and a basis of the State that recognizes rights [27]. Then, the State is responsible for the protection and guaranteeing of (vital) natural rights of the citizens. The author states that “what is natural, previous and primary, are individuals and their rights, needs, and interests”. In this sense, the State “is only legitimized as long as it aims to protect those rights and individual goods”.

In summary, in its substantial dimension, it is a “condition of validity ensured by the observance of fundamental rights”, social rights that must satisfy or preserve the rights of freedom. The Political Constitution of the Mexican United States forces all authorities, within their capacities, to comply with the obligation to promote, respect, protect, and guarantee human rights. For this reason, the Supreme Court of Justice has explained the principle of progressivity in human rights “that are derived from economic, social, educational, scientific, and cultural norms”, asserting that the principle “demands that as the level of development of a State improves, so should the compromise to guarantee economic, social, and cultural rights” of the citizens [22].

3. Materials and Methods

The aim of this work is to analyze the constitutional principle of proportionality applied to the monthly rate to determine the income tax of a person living in Mexico and compare it against the rates established for a person living abroad when determining income tax. This research is based on our professional experience and aims to explain how a natural person living in Mexico who receives income from salary is subject to tax withholding. This is based on the principle of progressivity, whereas a taxpayer living abroad who receives income from a source whose wealth is located in Mexico is subject to tax withholding based on the principle of proportionality [5,7]. We show the difference between the constitutional principles in tax rates to evidence the economic benefit a resident abroad may have in terms of interpretative, critical, and value use of the protective model.

3.1. Unit of Analysis

We analyzed the monthly–annual rate (Articles 96 and 152) and tax rates (Article 154) considering the fiscal residence of the natural persons who receive income from salaries in a national and foreign subordinate relation [7].

The unit of analysis is constituted by the tax regime of the natural persons living in Mexico with income from salaries granted for a subordinate service included in a comparative study that also contains the salaries of natural persons living abroad who receive income whose source of wealth is located in Mexico. The objective is to determine the difference between the implementation of the rate in Article 96 (national resident) and the rates in income from salary for a resident abroad (Article 154) and compare the application of tax rates for both types of residents to show how the human right to the vital minimum is violated [19,20,21].

The data used in the analysis considered the tax rate tables for national residents and those living abroad (Table 1). We used the lower and upper limits to define the accumulative income of the rate in Article 154 of the income tax and tax exemption as well as the monthly (annual) rate in Article 96 of the income tax.

The doctrine describes tax withholding determination for salaries and national residence by applying the monthly or annual rate of the tax, so we will not refer to the effective rates described by Beltrán but to “statutory marginal tax rates; that is, those that are reflected on the corresponding laws” [28] (p. 182). We deal with the analysis starting with a national resident who does not pay income tax for exempt income (listed in Article 93) and has the right to exert authorized deductions to determine annual tax (Article 152) [7]. In this study, we did not consider exempt income nor authorized deductions because they are not taxed. Therefore, we only considered taxable income for income tax. We located the income between the lower and upper limits to locate the excess and apply the progressive tax rate to it in order to determine the marginal tax and add the result to a fixed rate. The result is the tax the employer must withhold from a natural person who obtains income from a subordinate relationship.

The monthly (or annual) tax rate contains eleven tax ranges that are defined by lower and upper limits where the income is located to apply the percentage of tax rate to the excess. The rate goes from 1.92% in the first range to 35% in the last one, which represents the maximum tax for a natural person (Table 1). The successive increase in the rate shows the apparent progressive behavior of the tax, but which progressivity is it? How is it comparable to the withholding of which residents abroad are subjects as compared against that applied to national residents?

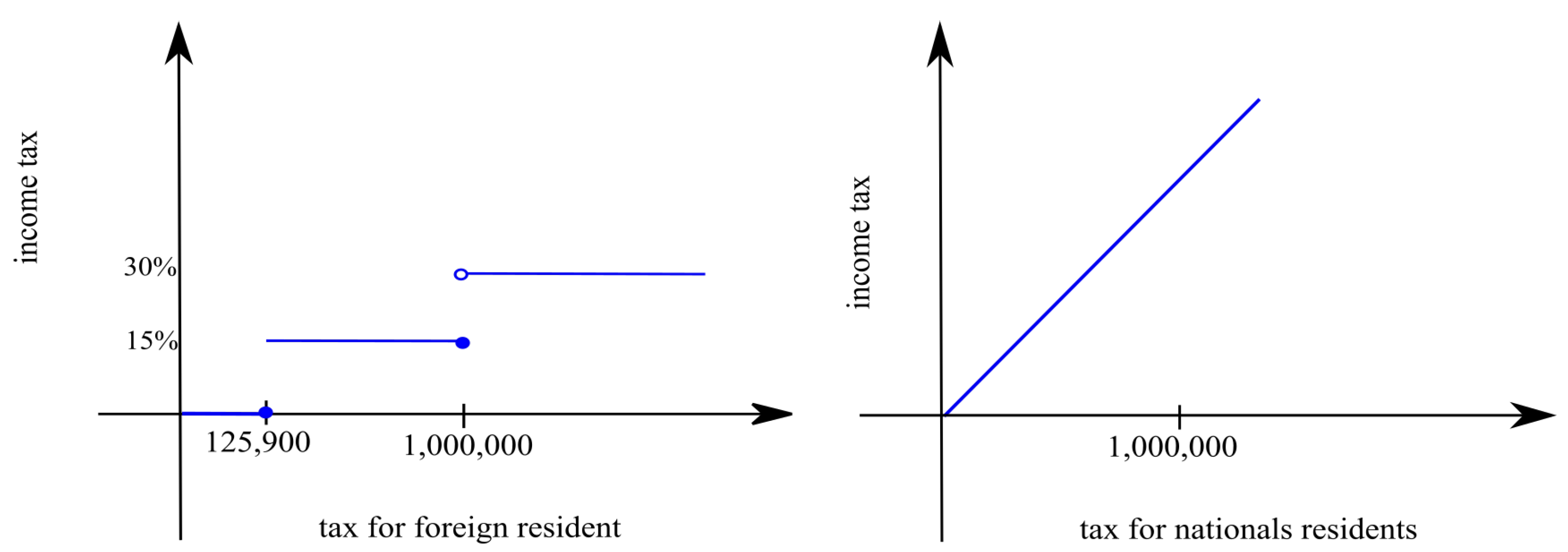

In the case of determination of a tax for a natural person who receives income from salary and lives abroad, an exemption of 125,900 Mexican pesos is firstly applied. Then, a 15% rate is applied to the difference as long as it does not exceed 1,000,000.00 Mexican pesos [7]. A second rate of 30% is added to the next income layer exceeding the same amount of Mexican pesos (Figure 1).

In order to compare the implementation of the principle of proportionality for national and foreign residents, we considered the tax hierarchy of the monthly rate and tax rates (Table 1). The result of the analysis is shown in Table 2. We studied the rate of the income tax to determine the tax withholding and considered the upper level (496.07 Mexican pesos of the first range) as cumulative income. We reduced the lower level whose difference is the excess and added the percentage to the latter, from which we obtained the marginal tax (9.52). Then, we added the fixed rate which is zero in the first range. By applying the legal order, we considered the upper limit again as cumulative income to determine the tax and obtained a marginal tax of 237.72 Mexican pesos, to which the fixed rate was added (9.52 Mexican pesos). The result is a tax withholding of 247.24 Mexican pesos. We applied the fiscal regulation to the following ranges and identify the fixed rate in all the cases is the tax withheld of the previous range (Table 1).

The income tax withheld determined in the previous range is the fixed rate added to the marginal tax determined in the following range. Therefore, the fixed rate is the income tax withheld determined in the previous range. The principle of progressivity is supposed to be present in the continuous growth of the tax rate; however, how progressive is the tax?

Following this notion, we analyzed the increase in the percentage (rate) applied to the excess of the lower limit per range. Range eight, showing lower and upper income limits between 32,736.84 and 62,500.00 Mexican pesos, is the one with the highest increase (6.48%), followed by the one in range four (5.12%), whose income is between 7399.43 and 8601.50 Mexican pesos. Then come ranges two and three with 4.48%. In contrast, ranges nine and ten show lower increases (2%), while range eleven exhibits the lowest increase (1%), the range with income above 250,000.00 Mexican pesos (Table 2).

The analysis shows that the tax rate contains the tax rate of the lower range and that the increase in the rate from one range to the next integrates the highest rate. In this sense, we determined the percentage that represents each of the ranges on the totality of the tax rate, considering that 35% is 100%, the maximum rate.

From this approach, range eight is evidently the one with the highest percentage of tax rate (18.51%), while range eleven has the lowest proportion of maximum tax rate (2.86%).

Even though residents abroad do not have the same fiscal technique, tax structure nor the monthly (annual) rate as national residents do, we calculated withholding, applying the tax rate established for that case, according to Table 1. The income established by law was added to these tax rates, along with an exemption, while a 15% rate was applied to a difference of lower than a million Mexican pesos. The next income over a million pesos received a 30% tax rate. The sum of these two withholdings is the total tax to be withheld. The results are shown in Table 3.

3.2. Measuring Progressivity of the Tax

The Suits index or progressive index is one of the best-known indices for calculating the measure of tax escalation more fully [29,30]. Suits’ index is a statistical quantitative method and is inspired and related to Gini’s well-known index [31,32,33]. Let X be a pre-tax income variable and Y be a general variable that in some cases will represent tax or benefit T and in others, the post-tax income, defined as . We suppose that X and Y are non-negative random variables. The Suits index, which is interpreted as an average measure of tax progressivity, is based on the relative concentration curve () of the Y-variable, which plots its cumulative percentage against the cumulative percentage of pre-tax income X when both variables have been ordered in ascending order of X [34].

The concentration curve is the bivariate analogue of the Lorenz curve. The relative concentration curve allows one to visualize and measure in summary the degree of non-proportionality between any two distributions by analogous distance and area measures.

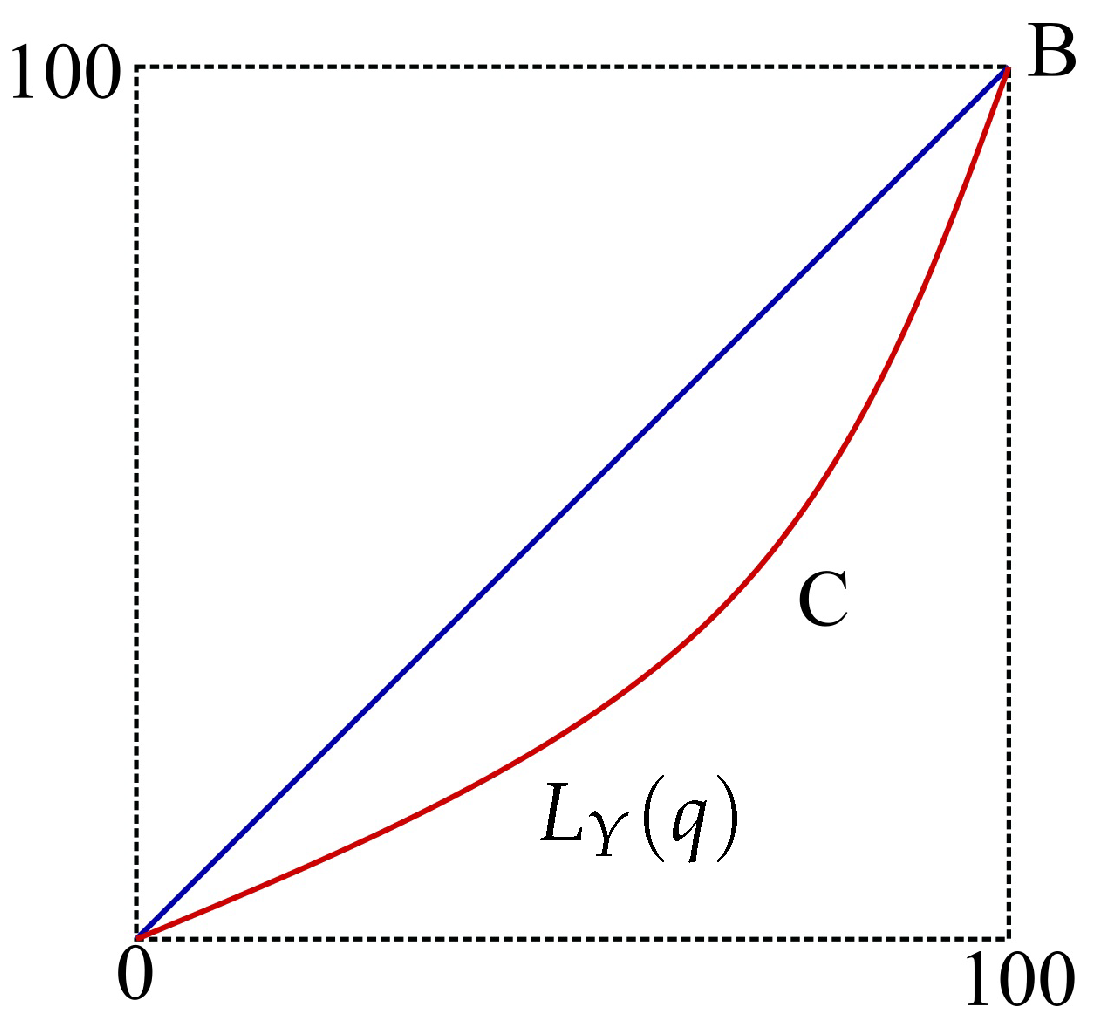

The of the Y-variable plots the cumulative percentage of tax liability (ordered by pre-tax income) against the cumulative percentages of pre-tax income. We denote the of Y as , where q, with , is the value of the Lorenz curve associated with the population rank . The Suits index, is defined as twice the area between proportionality line in Figure 2 and the region below [35]. Thus,

Geometrically, the Suits index is built by considering the ratio between the region area above the proportionality line in Figure 2 and the region below the relative concentration curve () [35].

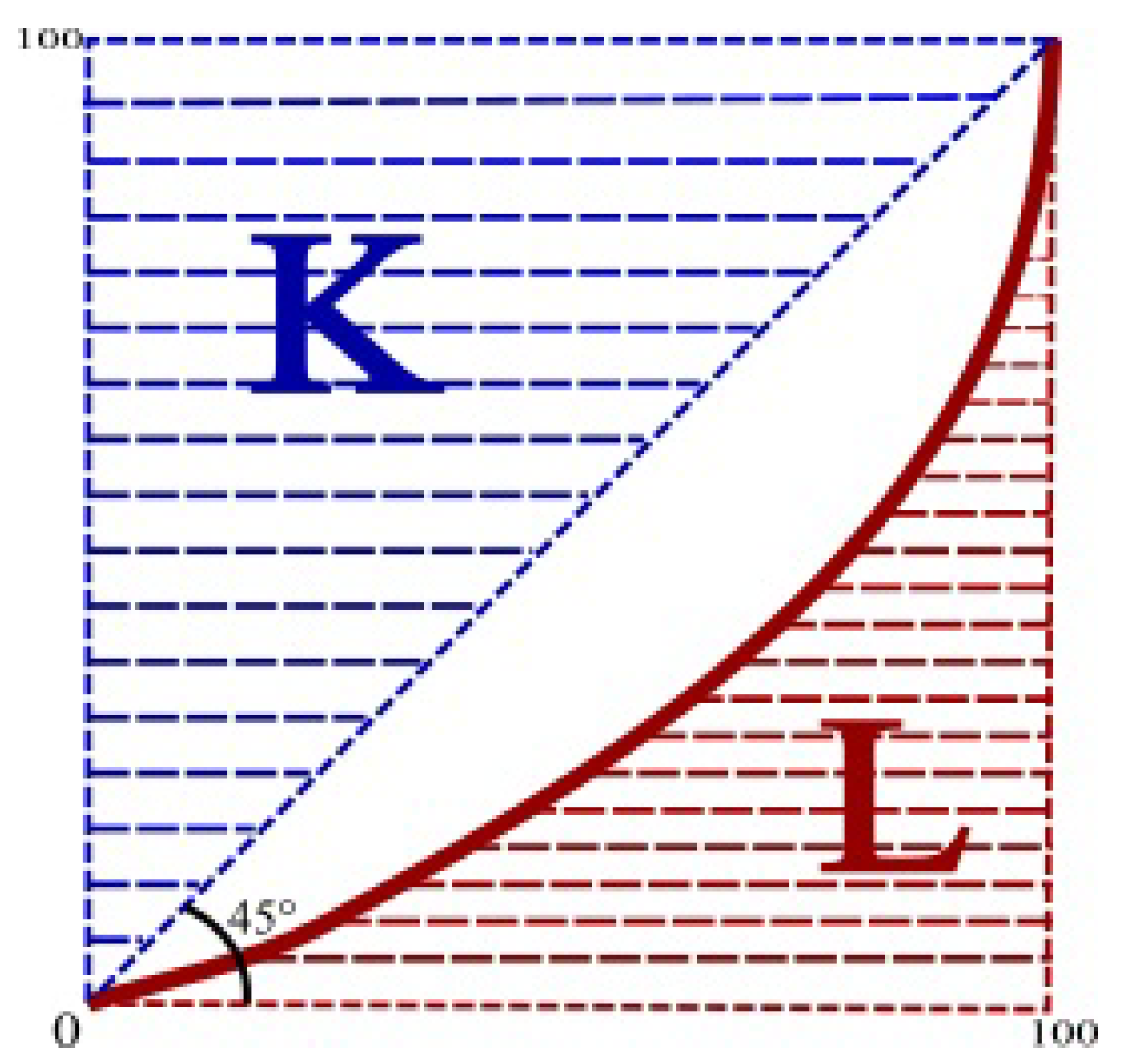

Let L between the curve and the x-axis and K be the area above the curve in a situation of proportionality (). It facilitates exposition to represent the accumulated percent income, measured on the horizontal axis, as a variable y that ranges from 0 to 100. Areas K and L are illustrated in Figure 3. The Suits index is defined with the following formula

By linking the area concept to the integral, we can write the Suits index with the following formula:

where y and are the percentages of total accumulated income and their corresponding accrued tax rates. Suits [35] provided a tool for this progressive index using numerical approximations for the area integral, i.e.,

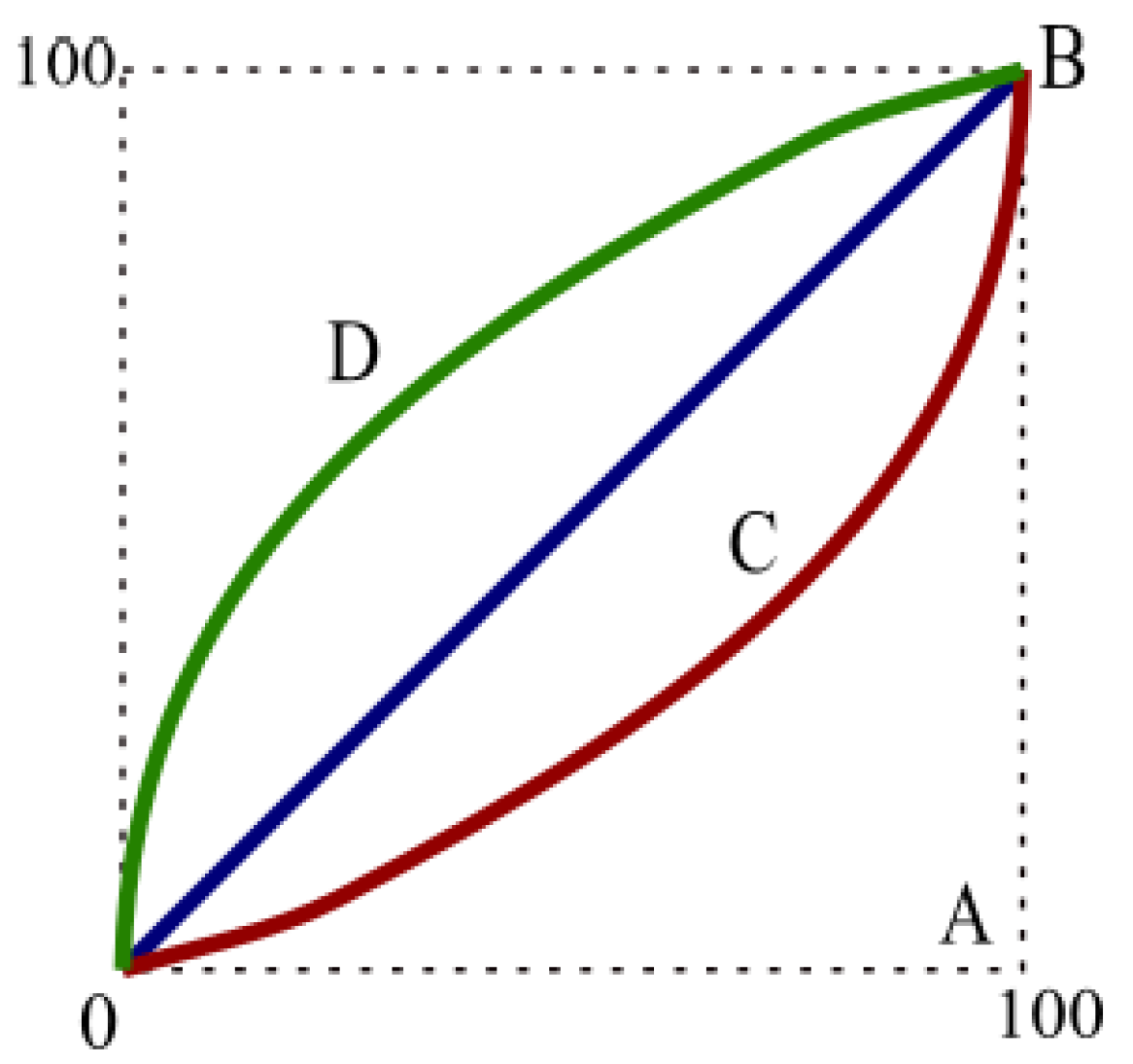

As can be seen, simple calculations are required to estimate the value of the progressive index when avoiding the use of the integral. Like the Gini index, the Suits index ranges from to 1. The key difference between the Suits index and the Gini coefficient is that curves can go above the line of proportionality.

Figure 4 is a graphic representation of this correlation based on the deviation of the Lorenz curve from its diagonal. For a proportional tax, L approaches K, so the Suits index S approaches zero. Since the Lorenz curve corresponding to a progressive tax falls below the line of proportionality, area L is smaller than K. As a result, the index S is positive for a progressive tax. In the limiting case where the highest income bears the entire tax burden, the Lorenz curve lies along sides and , so L equals zero and hence . With a regressive tax, the Lorenz curve arches above the line of proportionality, making the area L larger than K, so S is negative. An index of minus one indicates that a tax system is completely regressive. An index value of zero identifies a tax system as proportional [29].

In summary, Suits’ rate is positive for progressive taxes, negative for regressive taxes, and zero for proportional taxes. Namely, as a tax becomes more regressive, Suits’ index will approach its minimum value of and the more progressive the Suits index will approach 1. It is important to notice that the Suits index is a measure of the average progressivity of a tax system over the full income range. Some tax systems may be progressive over one range of income and regressive over another range [29].

The Suits index also provides a tool for determining the progressiveness index for a system of two or more taxes in terms of weighted averages of the , progressive indexes for x and z rates with average tax rates and , respectively [35]. The formula for calculating the progressiveness rate of this tax system with two tax rates is given by

Consequently, if the value of is positive, the tax system will be progressive. If is negative, the system then will be regressive and when it is a proportional system will be zero.

4. Results

In this application of tax rates, we will present it as a line of proportionality. For this purpose, the distribution of income will be divided into deciles. For a progressive tax, the percentage of the tax burden supported by the first decile is less than 20% and is increasing as shown in the data in Table 4.

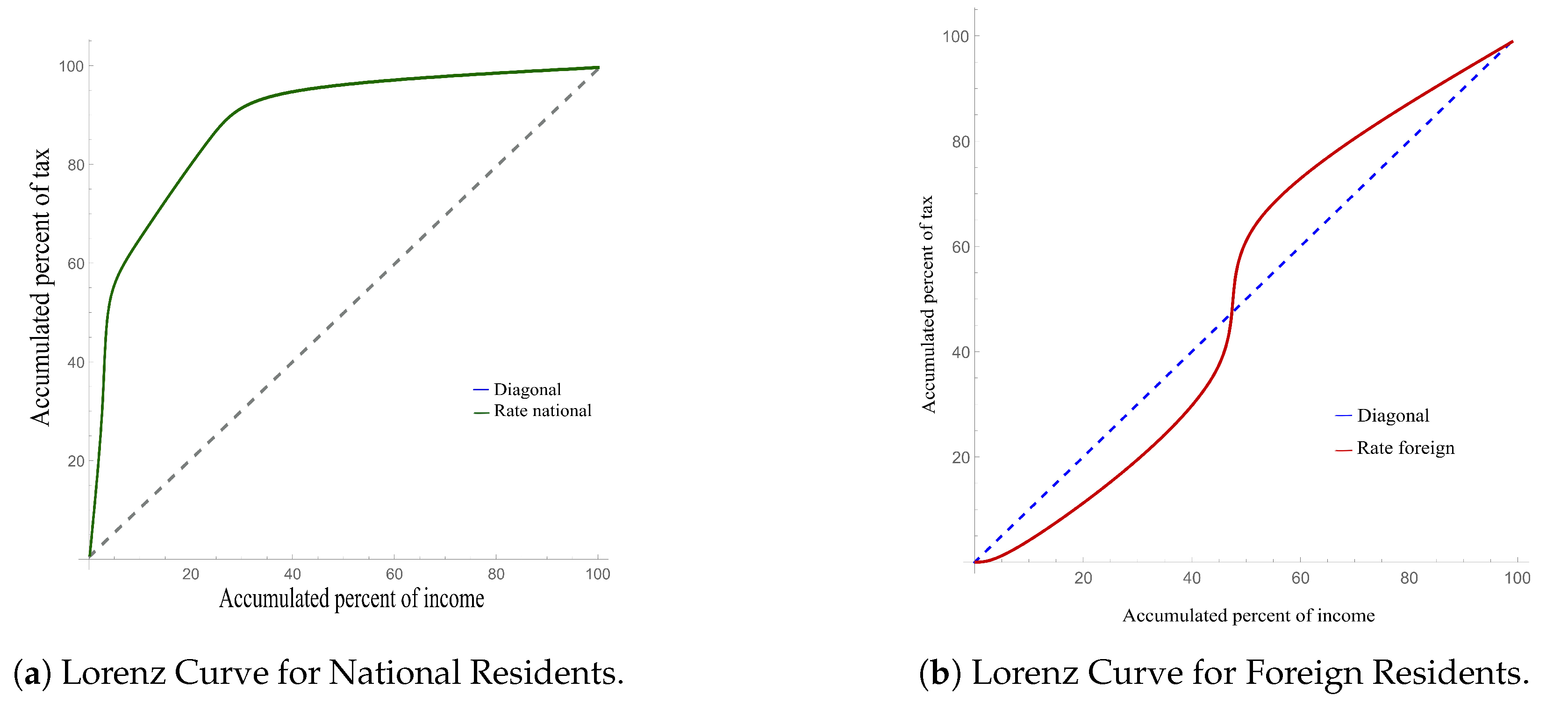

Figure 5a shows that for national residents the Lorenz curve is “arched” above the diagonal, suggesting a negative progressiveness rate. This was confirmed by calculating the Suits index (Equation (3)). For national residents, the information in columns 2 and 4 of Table 4 was considered, and the Suits index for domestic residents was obtained as

Thus, this means that this is a highly regressive tax, confirming the information provided by Figure 5a.

In the case of taxing of foreign residents, we have the Lorenz curve in Figure 5b, as we can see the graph shows that before the fifth decile the curve arches below the proportionality curve and after that decile is above. Using Equation (3), the Suits index for foreign residents must be

We can also observe a large increase in the progressivity for national residents (Figure 5a) compared to foreign residents (Figure 5b). Note that the Suits index for foreign residents is very close to zero. So, we have a slightly regressive tax. Being a numerical approximation and according to the information in Figure 5b, we can conclude that the tax tends to be proportional.

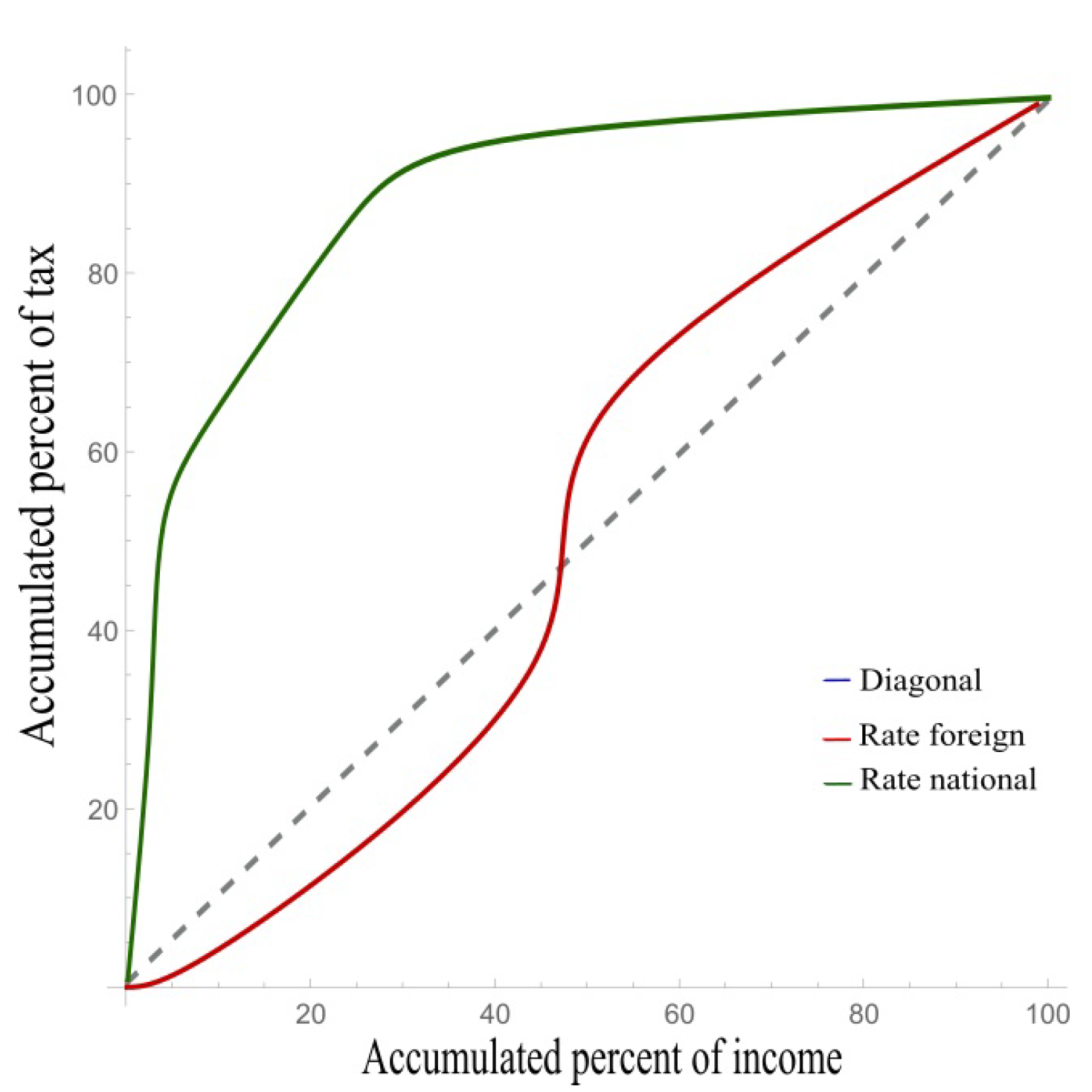

Now, we present the global progressivity index and our results seem to confirm that the total tax system is regressive. This is confirmed by the both taxes (see Figure 6). In fact, the value of the escalation index for the total tax system is the weighted average of the values for domestic and foreign residents (Equation (4)) with and . Using the data in Table 4, we have

As a result, the tax system is slightly regressive.

5. Discussion and Final Considerations

This paper demonstrated that the principle of proportionality applies differently in the case of domestic residents or residents living abroad, which is adversely associated with the right to the living minimum of the national resident, a principle immanent to the obligation to contribute [20,21,22]; these principles are universal because they are principles of economic equality [12,13] and applicable in other tax management controls in many countries that illustrated in the in the Mexican doctrine [11,12,13,14].

It is important to emphasize that a national resident accrues the entire income to a single range of the monthly fee. A foreign resident disaggregates income by first differentiating an exemption; then, a tax rate is applied and after a certain income limit a higher rate applies. The principle of proportionality applies here, as the theorists claim [14,15,16,17]. As noted above, applying the corresponding tax technique results in a monthly income of 250,000 Mexican pesos, and a domestic resident would pay 78,403.66 Mexican pesos [7], while an overseas resident would have to pay only 18,615 Mexican pesos. It is evidence of the inconsistency between income, payment of tax, and residence, Figure 5a, and not as stated by count [22].

This work was verified by Suits’ progressiveness index, analyzing the application of the two tax rates [35]. The tax rate that applies to the different income levels of a national resident together turns out to be highly regressive. By contrast, the tax rate of a foreign resident is sparsely regressive and prone to proportionality [6,19,22,23]. Nadirov and Dehning have talked about the positive and negative effects of progressivity [4]. This is the contribution of our study, which the Suits index distinguishes, in the first place, the principle of proportionality and the progressivity of the income tax evidenced to be not equal (Figure 1 ([22])). Second, it measures the degree of regressivity of tax rates according to the taxpayer’s residence (Figure 6). The Suits index (mathematical-economic indicator) shows the effect that the principle of progressivity has on the income of the worker residing in Mexico, testing our hypothesis. Therefore, this result shows the economic impact of the tax rate on his income, thus affecting his vital minimum, that is, his quality of life. The Suits index is a method that is appropriately related to the doctrine and demonstrates mathematically what statistics could not do.

It is desirable that the government seek to increase revenue from other approaches, as suggested by mercantilists ([9]), and to control the income tax rate, to reduce this effect [16,17,18,19]. Agreeing with the author, tax equity could be achieved as a legal principle of tax rate management control, considered as the first principle [36] (p. 12) of application of the “modern tax system”.

Rethinking the tax mechanics in accordance with the constitutional limits will probably mean reducing tax evasion and increasing the effect on tax collection. It would mean that the justice system would be complying with the provisions of Article 29 of the American Convention (ratified by the Mexican government in 2012), which mentions that human rights cannot be violated by the State, and it offers a more protective position. This omission would violate the pro person principle.

Our study has as a limitation in that it is focused on the tax regime of wages. However, it is this that contributes the most to federal public spending; therefore, the national resident wage regime will continue the regime of greater sustainability of public finances [3]. In addition, it is a regime, which in addition to containing a fixed rate [16], becomes progressive as income increases.

As a conclusion, we think that the State, as a guarantor of human rights, should promote that any reform of its tax laws does not invade the economy of citizens in such a way as to decrease the possibility of a dignified life [20,21,22,23]. Otherwise, the State must define with certainty what it refers to with the right to the minimum of life, which meets the minimum conditions of a dignified life, because then this would be the basis for determining the tax rate and acting as a true guarantor of people [23,28]. This is likely to involve legislators establishing a different causation technique such as for residents abroad.

In future research, we intend to study progressivity in other tax systems, trying to understand changes and tax rates as management control.

Author Contributions

E.M.-R.: objective, issue, conceptual and tax law framework, research design, and analysis and discussion of results. M.A.-M.: introduction, issue, analysis, and discussion of results. C.L.: issue, Suits method and measurement of tax progressivity, and discussion of results. All authors discussed and agreed on the conclusions. All authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

Not applicable.

Acknowledgments

We thank La Salle México University for their support in carrying out this research. We recognize the contribution of our study is a product of the project “Wage regime and the minimum living”.

Conflicts of Interest

The authors declare no conflict of interest.

References

- SAT. Datos abiertos. In Servicio de Administración Tributaria; SAT: Ciudad de México, Mexico, 2021. Available online: http://www.sat.gob.mx/cifras_sat/Paginas/inicio.html (accessed on 10 July 2021).

- Organization for Economic Cooperation and Development (OECD). Estudios Económicos de la OCDE. México. 2011. Available online: http://0-dx-doi-org.brum.beds.ac.uk/10.1787/9789264115934-es/ (accessed on 30 April 2021).

- SAT. Informe Tributario y de Gestión, Cuarto Trimestre 2020. Secretaría de Hacienda y Crédito Público. Available online: http://omawww.sat.gob.mx/cifras_sat/Documents/ITG_2020_4T.pdf (accessed on 20 November 2020).

- Nadirov, O.; Dehning, B. Tax Progressivity and Entrepreneurial Dynamics. Sustainability 2020, 12, 3584. [Google Scholar] [CrossRef]

- Diario Oficial de la Federación, Constitución Política de los Estados Unidos Mexicano, lunes 5 de Febrero de 1917. May 2021. Available online: https://www.dof.gob.mx/index_113.php?year=1917&month=02&day=05/ (accessed on 28 May 2021).

- Mancilla-Rendón, E.; Astudillo, M. La equidad en el impuesto sobre la renta: El caso de los asalariados residentes en México y los residentes en el extranjero. Rev. Audit. Governanca Contab. 2012, 1, 40–62. [Google Scholar]

- Diario Oficial de la Federación, Ley del Impuesto Sobre la Renta. 11 December 2013. 2021. Available online: http://www.dof.gob.mx/index.php?year=1964&month=12&day=31 (accessed on 23 April 2021).

- Ponce de León, L. Metodología del Derecho, 13th ed.; Porrúa: Mexico City, Mexico, 2013. [Google Scholar]

- Cruz Vásquez, M.; Mendoza Velázquez, A.; Pico González, B. Inversión extranjera directa, apertura económica y crecimiento económico en América Latina. Contaduría Adm. 2019, 64, 1–21. [Google Scholar] [CrossRef] [Green Version]

- Aguado, I.; Echebarria, M.; Barrutia, J. El desarrollo sostenible a lo largo de la historia del pensamiento económico. Rev. Econ. Mund. 2009, 21, 87–110. [Google Scholar]

- Simón, L. Los principios de justicia tributaria en la historia constitucional cubana. Cuest. Const. 2011, 25, 201–266. [Google Scholar] [CrossRef]

- Masbernat, P. Justicia y sistema tributario. Una mirada desde la perspectiva inglesa. Díkaion 2014, 23, 135–169. [Google Scholar] [CrossRef]

- Marín-Barnuevo, D. La protección de la familia en el sistema tributario. In Justicia Tributaria y Derechos Humanos; En Ortega, J., Ed.; Instituto de Investigaciones Jurídicas, UNAM: Mexico City, Mexico, 2016; pp. 41–82. Available online: https://archivos.juridicas.unam.mx/www/bjv/libros/9/4259/4.pdf (accessed on 31 July 2021).

- Arnold, R.; Martínez, J.; Zúñiga, F. El principio de proporcionalidad en la jurisprudencia del tribunal constitucional. Estud. Const. 2012, 10, 65–116. [Google Scholar] [CrossRef] [Green Version]

- Piza, R.J. El régimen fiscal en la Constitución de 1991. Rev. Derecho Estado 2008, 21, 51–80. [Google Scholar]

- Popescu, M.E.; Militaru, E.; Stanila, L.; Vasilescu, M.D.; Cristescu, A. Flat-Rate versus Progressive Taxation? An Impact Evaluation Study for the Case of Romania. Sustainability 2019, 11, 6405. [Google Scholar] [CrossRef] [Green Version]

- Burgoa, C. Principios tributarios en serio. Rev. Posgrado Derecho UNAM 2009, 8, 193–209. [Google Scholar]

- Sánchez, R. Recepción jurisprudencial del principio de proporcionalidad en México. Cuest. Const. 2009, 21, 471–489. [Google Scholar] [CrossRef]

- SCJN. 1a. XCVIII/2007. Primera Sala. Novena Época. Semanario Judicial de la Federación y su Gaceta. Tomo XXV. 2007; p. 792. Available online: https://sjf.scjn.gob.mx/sjfsist/paginas/DetalleGeneralV2.aspx?ID=172546&Clase=DetalleTesisBL&Semanario=0 (accessed on 9 October 2019).

- Quintero, S.P.D.; Quintero, M.D.; Sánchez, P.G. Sobre el derecho fundamental al mínimo vital o a la subsistencia: Análisis jurisprudencial. Encuentros 2019, 17, 80–95. [Google Scholar]

- Tenorio, X. Conceptos constitucionales de la Contribución o del Derecho al Mínimo Vital. Prax. Justicia Fisc. Adm. 2015, 7, 1–21. [Google Scholar]

- SCJN. Tesis P.VII/2013 (9a.) suprema corte de justicia de la nación, libro 1, tomo I, décima época. In Gaceta del Semanario Judicial de la Federación; Tesis Aislada Constitucional 159820; SCJN: Ciudad de México, Mexico, 2013; p. 136. Available online: https://sjf.scjn.gob.mx/sjfsist/Paginas/DetalleGeneralV2.aspx?id=159820&Clase=DetalleTesisBL (accessed on 9 May 2019).

- Tribunales Colegiados de Circuito. Décima época. Semanario Judicial de la Federación y su Gaceta; Libro XIX, Amparo en Revisión 184/2012. 2013; p. 2254. Available online: https://www.scjn.gob.mx/sites/default/files/gaceta/documentos/2016-12/XIX_ABR.pdf (accessed on 4 August 2021).

- American Convention on Human Rights, San José de Costa Rica. 7–22 November 1969. Available online: https://www.corteidh.or.cr/historia.cfm?lang=en (accessed on 15 July 2021).

- Orozco, J. Los derechos humanos y el nuevo artículo 1o. constitucional. IUS. Rev. Inst. Cienc. Jurídicas Puebla 2011, 5, 85–98. [Google Scholar]

- Aguilera, R.; López, R. Los Derechos Fundamentales en la Teoría Jurídica Garantista de Luigi Ferrajoli; Instituto de Investigaciones Jurídicas, UNAM: México City, Mexico, 2011; pp. 49–82. Available online: https://archivos.juridicas.unam.mx/www/bjv/libros/6/2977/4.pdf (accessed on 31 July 2021).

- Gascón, M. La teoría general del garantismo a propósito de la obra de L. Ferrajoli “Derecho y Razón”. Jurídica Anu. Dep. Derecho Univ. Iberoam. 2001, 31, 195–213. [Google Scholar]

- Beltrán, F. Estimación de la recaudación potencial en el impuesto al trabajo y a los ingresos al capital: Comparativo entre México y estados unidos. Rev. Mex. Econ. Finanz. 2014, 9, 175–194. [Google Scholar] [CrossRef] [Green Version]

- Anderson, J.E.; Roy, A.G.; Shoemaker, P.A. Confidence Intervals for the Suits Index. Natl. Tax J. 2003, 56, 81–90. [Google Scholar] [CrossRef] [Green Version]

- Hierro Recio, L.A.; Atienza Montero, P.; Gómez-Álvarez Díaz, R. El origen de la desigualdad y la progresividad en la distribución de la financiación de las Comunidades Autónomas de régimen común. Cuad. Econ. 2008, 31, 35–58. [Google Scholar] [CrossRef] [Green Version]

- Andres, R.; Calonge, S. Inference on Income Inequality and Tax Progressivity Indices: U-Statistics and Bootstrap Methods; Working Papers 09, ECINEQ; Society for the Study of Economic. 2005. Available online: https://ideas.repec.org/p/inq/inqwps/ecineq2005-09.html (accessed on 15 July 2021).

- Tran, C.; Zakariyya, N. Tax progressivity in australia: Facts, measurements and estimates. In ANU Working Papers in Economics and Econometrics; 2019-667; Australian National University, College of Business and Economics, School of Economics: Canberra, Australia, 2019; Available online: https://taxpolicy.crawford.anu.edu.au/sites/default/files/publication/taxstudies_crawford_anu_edu_au/2019-03/complete_tran_zakariyya_tax_progressivity_mar_2019.pdf (accessed on 31 July 2021).

- Sterner, T. Distributional effects of taxing transport fuel. Energy Policy 2012, 41, 75–83. [Google Scholar] [CrossRef]

- Arcarons, J.; Calonge, S. Testing Tax-Progressivity and Income-Redistribution: The Suits Approach; 2013. Available online: https://www.semanticscholar.org/paper/Testing-Tax-Progressivity-and-Income-Redistribution-Arcarons-Calonge/ac83f4194c9c3d01f3bb8133591caaec137d9620#related-papers (accessed on 31 July 2021).

- Suits, D. Messurement of tax progressivity. Am. Econ. Rev. 1977, 67, 747–752. [Google Scholar]

- Hu, B.; Dong, H.; Jiang, P.; Zhu, J. Analysis of the Applicable Rate of Environmental Tax through Different Tax Rate Scenarios in China. Sustainability 2020, 12, 4233. [Google Scholar] [CrossRef]

Figure 1.

Fd.: Self-elaboration on study.

Figure 2.

Relative concentration curve () of the Y-variable. Data source: Own elaboration.

Figure 3.

Suits index as a proportion of areas K and L. Data source: Own elaboration.

Figure 4.

Picture of Lorenz curve and concentration curve for Suits index. Data source: Own elaboration.

Figure 4.

Picture of Lorenz curve and concentration curve for Suits index. Data source: Own elaboration.

Figure 5.

Graph of the tax on domestic residents and graph of the tax on foreign residents.

Figure 6.

Lorenz curve of national residents and residents living abroad.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Table 1.

Self-elaboration on Article 96 Tax Income Law (Impuesto Sobre la Renta, ISR) (Mexican pesos).

Table 1.

Self-elaboration on Article 96 Tax Income Law (Impuesto Sobre la Renta, ISR) (Mexican pesos).

| Monthly Rate Analysis ISR Withholding | ||||||

|---|---|---|---|---|---|---|

| Range | Monthly Income | National Residents | Rate % | |||

| Lower Limit | Upper Limit | Fixed Rate | Marginal Rate | Tax Withheld | ||

| 1 | 0.01 | 496.07 | 0.00 | 9.52 | 9.52 | 1.92 |

| 2 | 496.08 | 4210.41 | 9.52 | 237.72 | 247.24 | 6.40 |

| 3 | 4210.42 | 7399.42 | 247.24 | 346.96 | 594.20 | 10.88 |

| 4 | 7399.43 | 8601.50 | 594.20 | 192.36 | 786.56 | 16.00 |

| 5 | 8601.51 | 10,298.35 | 786.56 | 304.07 | 1090.63 | 17.92 |

| 6 | 10,298.36 | 20,770.29 | 1090.63 | 2236.80 | 3327.43 | 21.36 |

| 7 | 20,770.30 | 32,736.83 | 3327.43 | 2814.53 | 6141.96 | 23.52 |

| 8 | 32,736.84 | 62,500.00 | 6141.96 | 8928.95 | 15,070.91 | 30.00 |

| 9 | 62,500.01 | 83,333.33 | 15,070.91 | 6666.66 | 21,737.57 | 32.00 |

| 10 | 83,333.34 | 250,000.00 | 21,737.57 | 56,666.66 | 78,404.23 | 34.00 |

| 11 | 250,000.01 | 250,000.00 | 78,404.23 | 0.00 | 78,404.23 | 35.00 |

Table 2.

Self-elaboration on study (percentage).

| Monthly Rate Analysis Income Tax Withholding (Impuesto Sobre la Renta, ISR) | |||

|---|---|---|---|

| Range | Rate | Increase | Proportion |

| 1 | 1.92% | 1.92% | 5.49% |

| 2 | 6.40% | 4.48% | 12.80% |

| 3 | 10.88% | 4.48% | 12.80% |

| 4 | 16.00% | 5.12% | 14.63% |

| 5 | 17.92% | 1.92% | 5.49% |

| 6 | 21.36% | 3.44% | 9.83% |

| 7 | 23.52% | 2.16% | 6.17% |

| 8 | 30% | 6.48% | 18.51% |

| 9 | 32% | 2% | 5.71% |

| 10 | 34% | 2% | 5.71% |

| 11 | 35% | 1% | 2.86% |

| 35% | 100% | ||

Table 3.

Self-elaboration on Article 154 Tax Income Law (Impuesto Sobre la Renta, ISR) (Mexican pesos).

Table 3.

Self-elaboration on Article 154 Tax Income Law (Impuesto Sobre la Renta, ISR) (Mexican pesos).

| Rate Tax Foreign Resident | |

|---|---|

| Income | 1,000,000.00 |

| Exemption | 125,900.00 |

| Difference | 874,100.00 |

| <1,000,000 | 15.00% |

| ISR Withholding | 131,115.00 |

| >1,000,000 | 30.00% |

| ISR Withholding | 300,000.00 |

| ISR Withholding | 431,115.00 |

Table 4.

Income analysis and withholding tax to accumulate.

| National Resident | Abroad Resident | ||||

|---|---|---|---|---|---|

| Range | Income Monthly | Tax Fixed% | Tax % | Income % | Tax % |

| 1 | 0.20 | 0 | 5.65 | 0 | 0 |

| 2 | 1.68 | 0.04 | 18.82 | 0 | 0 |

| 3 | 2.96 | 1.14 | 32.00 | 0 | 0 |

| 4 | 3.44 | 2.73 | 47.06 | 0 | 0 |

| 5 | 4.12 | 3.62 | 52.71 | 0 | 0 |

| 6 | 8.31 | 5.02 | 62.82 | 0 | 0 |

| 7 | 13.09 | 15.31 | 69.18 | 6.3 | 0 |

| 8 | 25.00 | 28.25 | 88.24 | 43.71 | 33.33 |

| 9 | 33.33 | 69.33 | 94.12 | 50.00 | 66.67 |

| 10 | 100.00 | 100.00 | 100.00 | 100.00 | 100.00 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Mancilla-Rendón, E.; Astudillo-Moya, M.; Lozano, C. Tax Rate of Management Control: The Mexican Income Tax Rates System for Resident and Non-Residents. Sustainability 2021, 13, 9202. https://0-doi-org.brum.beds.ac.uk/10.3390/su13169202

AMA Style

Mancilla-Rendón E, Astudillo-Moya M, Lozano C. Tax Rate of Management Control: The Mexican Income Tax Rates System for Resident and Non-Residents. Sustainability. 2021; 13(16):9202. https://0-doi-org.brum.beds.ac.uk/10.3390/su13169202

Chicago/Turabian StyleMancilla-Rendón, Enriqueta, Marcela Astudillo-Moya, and Carmen Lozano. 2021. "Tax Rate of Management Control: The Mexican Income Tax Rates System for Resident and Non-Residents" Sustainability 13, no. 16: 9202. https://0-doi-org.brum.beds.ac.uk/10.3390/su13169202

Note that from the first issue of 2016, this journal uses article numbers instead of page numbers. See further details here.