Effects on Global Forests and Wood Product Markets of Increased Demand for Mass Timber †

1

USDA Forest Service, Forest Products Laboratory, Madison, WI 53726, USA

2

Independent Researcher, Ottawa, ON K1A 0G9, Canada

3

School of Environmental and Forest Sciences, University of Washington, Seattle, WA 98105, USA

*

Author to whom correspondence should be addressed.

†

This article makes up part of a larger 5-phased project which was initiated by The Nature Conservancy (nature.org (accessed on 18 October 2021)) through generous support from The Climate and Land Use Alliance, and the Doris Duke Charitable Foundation (DDCF). The work upon which this project is based was also funded in whole or in part through a cooperative agreement with the USDA Forest Service, Forest Products Laboratory and The Nature Conservancy (17-CA-11111169-031). The Nature Conservancy initiated this project to further our collective understanding of the potential benefits and risks of increasing demand for forest products and ensuring that any increases are sustainable. The Conservancy’s objectives are focused on delivering critical safeguard frameworks to mitigate any potential risks to forest ecosystems as mass timber demand increases. In accordance with Federal Law and U.S. Department of Agriculture policy, this institution is prohibited from discriminating on the basis of race, color, national origin, sex, age, or disability. (Not all prohibited bases apply to all programs) To file a complaint of discrimination, write USDA, Director, Office of Civil Rights, Room 326-W, Whitten Building, 1400 Independence Avenue, SW, Washington, DC 20250-9410 or call (202) 720-5964 (voice and TDD). USDA is an equal opportunity provider, employer, and lender.

Sustainability 2021, 13(24), 13943; https://0-doi-org.brum.beds.ac.uk/10.3390/su132413943

Submission received: 12 November 2021

/

Revised: 4 December 2021

/

Accepted: 8 December 2021

/

Published: 17 December 2021

(This article belongs to the Special Issue Mass Timber and Sustainable Building Construction)

Abstract

:This study evaluated the effects on forest resources and forest product markets of three contrasting mass timber demand scenarios (Conservative, Optimistic, and Extreme), up to 2060, in twelve selected countries in Asia, Europe, North America, and South America. Analyses were carried out by utilizing the FOrest Resource Outlook Model, a partial market equilibrium model of the global forest sector. The findings suggest increases in global softwood lumber production of 8, 23, and 53 million m3 per year by 2060, under the Conservative, Optimistic, and Extreme scenarios, respectively, leading to world price increases of 2%, 7%, and 23%, respectively. This projected price increase is relative to the projected price in the reference scenario, altering prices, production, consumption, trade of forest products, timber harvest, forest growth, and forest stock in individual countries. An increase in softwood lumber prices due to increased mass timber demand would lead to the reduced consumption of softwood lumber for traditional end-use (e.g., light-frame construction), suggesting a likely strong market competition for softwood lumber between the mass timber and traditional construction industries. In contrast, the projected effect on global forest stock was relatively small based on the relatively fast projected biomass growth in stands assumed to be regenerated after harvest.

1. Introduction

The building sector is one of the largest contributors of global greenhouse gas (GHG) emissions, which accounted for about 38% of global energy-related emissions in 2019 [1]. The majority (74%) of these emissions were the result of energy consumption during building operations (e.g., use of fossil fuel for heating and cooking, and use of carbon-intensive electricity), and the rest of the emissions (26%) were estimated to come from the building construction indusf52try that manufactures building construction materials, such as steel, cement, and glass [1]. The global urban population is projected to reach to 68% by 2050 [2]. The global building sector is expected to continue to grow at a substantial rate in the future to accommodate the increasing needs for residential and nonresidential buildings by the growing population. For example, about 230 billion square meters of floor space is expected to be constructed worldwide within the next 40 years [3]. To provide a perspective, this would be equivalent to adding about 110 km2 (approximately the size of Paris) of space every single week through to 2060 [3]. These figures suggest an urgent need to find and utilize sustainable low-carbon solutions for the global building sector. There are several ways to curb the building sector’s emissions. The key strategies proposed to reduce emissions from the building sector include: (1) aggressively reducing fossil energy consumption in the built environment, (2) decarbonizing the power sector by focusing on more-efficient energy sources, and (3) increasing the use of sustainable materials to replace carbon-intensive materials that would reduce building life cycle carbon emissions [1].

Each strategy to combat global emissions has its own merits and trade-offs in relation to environmental benefits, mitigation costs, challenges in its adaptation or implementation, and its impacts on the economic sectors. Our focus in this paper is to understand the effects on the forest and the forest products sector of the sustainable material replacement strategy, especially the increased use of mass timber in buildings in place of carbon-intensive building materials such as steel and concrete. While the carbon consequences of the increased use of mass timber in buildings are not the focus of this paper, a better understanding of the effects of increasing mass timber use worldwide on the global forests and the wood products sector will help identify the potential carbon benefits of expanding mass timber use in buildings.

Mass timber refers to a new family of engineered wood products that are manufactured as large panels by bonding together solid pieces of wood with various directional arrangements, layers, and lengths [4,5,6]. The resulting improved structural properties allow for their use as structural materials in buildings where wood has not been used conventionally, especially in the roofs, walls and floors of offices, public/institutional buildings, schools, and high-rise multifamily and mixed-use buildings [4,5,6]. The use of wood in high-rise buildings was limited until recently due to building code restrictions. However, the recent changes in the 2021 International Building Code (IBC) now allow the use of wood in buildings up to 18 stories [7]. The 2021 IBC provides provisions for three new construction types (Type IV-A, IV-B and IV-C) where the use of mass timber materials is allowed [7]. These building types vary by maximum allowable height, total floor space, floor space per story, and fire protection requirements [7,8]. For example, the type IV-A allows a maximum height of 270 feet or 18 stories, followed by Type IV-B (up to 180 feet or 12 stories) and Type IV-C (up to 85 feet or 9 stories) [4,8].

Several categories of products are included in the family of mass timber, such as Cross-Laminated Timber (CLT), Nail-Laminated Timber (NLT), Glue-Laminated Timber (Glulam), Dowel-Laminated Timber (DLT), Mass Plywood Panel (MPP), Post and Beam, and Heavy Timber Decking [6]. Descriptions of each of these products are available elsewhere (e.g., see [4,5,6]). Several of these products share similar applications, supply chains, and manufacturing processes, and therefore can be substituted for one another [9]. However, the use of CLT in a lateral system (such as structural walls), along with the use of Glulam beam and columns as the gravity system, is the most used approach for constructing mass timber buildings [10]. Accordingly, in this study, the forecasted demand for mass timber in 12 selected countries includes the combined demand for CLT and Glulam in CLT hybrid constructions.

In addition to its favorable structural, seismic, fire, acoustic, and thermal performances in buildings, mass timber offers various environmental, economic, aesthetic, health, and energy benefits that are usually not available with functionally equivalent non-wood materials [4,5,8,11,12]. A growing body of literature suggests that mass timber has a considerably lower carbon footprint than non-wood materials such as steel or concrete [13,14,15]. Therefore, using them in place of carbon-intensive steel and concrete in buildings can substantially reduce fossil-based GHG emissions [16,17,18,19,20,21,22]. In addition, unlike those materials, wood is renewable. Sustainable harvest practices ensure that only a small proportion of forests (1–2% of forest land in North America) get harvested each year. The harvested carbon is less than the growth, ensuring a stable carbon stock in the forests. Thus, mass timber offers a renewable and sustainable alternative to more fossil fuel-intensive, non-wood materials in the building sector.

Until recently, the global market of CLT has been dominated by Europe, which shared more than 80% of global production until 2019 [23,24]. However, recent reports suggest that the North American CLT production level is on par with European production. CLT production and consumption in other world regions, such as Oceania and Asia, is also growing [24]. For instance, out of an estimated 2.8 million m3 of global CLT production in 2020, Europe, North America, Oceania, and Asia shared 48%, 43%, 6%, and 3%, respectively, in 2020 [24]. Although global mass timber production has increased rapidly in recent years, it still constitutes a small fraction of total global wood consumption (less than 1% global softwood lumber consumption) [25]. However, the interest in using mass timber in various types of buildings is increasing worldwide, as demonstrated by the several multifamily units, larger public buildings, office buildings, and mixed-use tall buildings already constructed or planned to be constructed with mass timber [7,26,27]. For example, as of June 2021, 1169 projects involving modern mass timber and Post and Beam in multi-family, commercial, and institutional buildings were recorded across all 50 states in the United States (U.S.), among which 545 were already completed or under construction, and the remaining 624 were in the design phase [26]. Note that the June 2021 numbers represent an increase of about 50% within 15 months, with 784 mass timber projects were recorded in March 2020 [26].

The increasing trend in demand for mass timber is expected to continue far into the future, mainly driven by a growing interest in sustainable low-carbon biobased materials in the construction sector, largely motivated by concern over climate change. For instance, a recent mass timber outlook presented by the Softwood Lumber Board (SLB) for the U.S. indicates a potential incremental mass timber demand of about 9 million m3 by 2035 [28]. This volume corresponds to approximately 11.6 million m3 of softwood (SW) lumber demand, representing about 13% of U.S. SW lumber consumption in 2019 [29]. Analyses at global levels by various research groups forecast that the global market value of CLT will grow at a compound annual growth rate of 12% to 14% between 2021 and 2027 [30,31].

While the magnitudes and trajectories of mass timber demand forecasts vary across studies, one common theme among them is that they all point to rising demand in the mass timber industry, which, if realized, would require substantial volumes of solid wood as raw materials. Thus, when demand for mass timber grows in the future, so will timber harvests, and the production, consumption, and international trade of solid wood products (e.g., lumber) that are needed to manufacture mass timber. Changes in harvests and manufacturing activities could alter forest growth and inventory, product prices, and associated effects on various wood products’ demand, supply, and trade conditions in an individual country [32,33,34]. How mass timber-induced changes in such variables affect global forest resources and wood product markets is less understood, which is something this study aims to investigate.

Information on how these variables will evolve in the future, given contrasting scenarios of mass timber demand worldwide, would help us answer frequently raised questions and/or concerns about the potential adverse effects of mass timber demand on forest resources and the traditional forest products end-use sector. For example, concerns have been raised that the increased use of wood in buildings might negatively impact forest resources due to potential over-harvesting, which could lead to forestland degradation and/or deforestation. Concerns have also been raised that the increased use of wood to produce mass timber may increase market competition for lumber between traditional use (low-rise residential construction and furniture) and mass timber use [22]. Such insights into the potential effects of increased mass timber demand on forests and market conditions in individual countries, regions and the world are helpful to forest product industry managers, forest land managers, and domestic and international policy makers in developing appropriate strategic plans to support, adapt to or counteract the projected effects of mass timber.

Information on these forest sector variables in individual countries and regions is also useful for developing a more complete picture of potential carbon mitigation benefits of substituting mass timber for fossil-intensive non-wood materials in the construction sector. For example, the potential carbon benefits that would be accrued via increased wood use in mass timber in a country may be offset or even negated by the depleted forest stock (carbon) in countries that increase their harvests to supply wood to the mass timber-consuming regions [33,35].

While an increased demand for mass timber could have many impacts on forests (studies on the detailed stand-level forest impacts of increased mass timber demand are planned in phase 4 of the larger five-phase study on the climate impacts of mass timber, led by the Nature Conservancy, and this is not part of this study) and the forest industry, this study aims to investigate the dynamic impacts on the global forest sector and wood product markets of increased mass timber use in buildings. These questions are investigated by developing three relatively longer-term alternative scenarios of mass timber consumption, 2020–2060, in selected countries in Asia, Europe, North America, and South America [36], and using those alternative mass timber demand scenarios to influence wood product market conditions in the FOrest Resource Outlook Model (FOROM), a partial market equilibrium model of the global forest sector. The projected impacts for the next 40 years (2020 to 2060) on timber harvests, forest growth and inventory, production, consumption, trade, and prices in individual countries and world regions are evaluated by comparing projected outcomes in the alternative mass timber demand scenarios with a business-as-usual (BAU) scenario that does not consider any increase in mass timber demand.

2. Methods

This section provides a description of the alternative mass timber demand scenarios, the global forest sector model, and the modeling approaches used in evaluating global, regional, and country-level impacts on forests and the forest product markets of forecasted mass timber demand in multiple countries across Europe, North America, Asia, and South America. The analysis and evaluations were carried out by shocking the demand curves of SW lumber in countries forecasted with increased mass timber demand in a global model of the forests and forest products sector, referred to as the FOROM. The FOROM provides market equilibrium solutions of the forest sector variables, such as timber harvests, prices, production, and consumption, and the trade of 20 types of forest products across 60 countries and regions (Table A2). All economic and biophysical parameters in the model were kept the same between the alternative and the business-as-usual (BAU) reference model runs, except for the demand for SW lumber, allowing us to identify the differences in model solutions between the two cases as the impact of increased mass timber demand.

2.1. Mass Timber Demand Scenarios

This study utilized three alternative scenarios of mass timber demand, 2020–2060, projected for 12 selected countries in Ganguly [36], including seven countries in Europe (Austria, France, Germany, Italy, Netherlands, Spain, and UK), USA, China, and three countries in South America (Argentina, Brazil, Chile), to evaluate their impacts on forests and the forest products sector at the global, regional, and individual country levels.

The projections for mass timber demand in the selected countries are based on the estimated historical trends in residential and nonresidential construction by building heights (low-rise or <6 stories, mid-rise or 7 to 12 stories, and high-rise or >13 stories) in those countries and estimated volumes of CLT and Glulam use in those buildings [36]. While the building heights and building types remained the same across scenarios, the actual demand estimates for these two categories of mass timber in selected countries were estimated using new product repeat purchase diffusion modeling, developed specifically for wood products [36,37]. The diffusion model’s base model parameters were varied, leading to a broad range of mass timber market penetration levels and correspondingly varying levels of mass timber use across scenarios in those countries through to 2060 [36]. The three scenarios are referred to as the Conservative, Optimistic, and Extreme scenarios, based on a combination of assumptions and modeling about characteristics of the market and the relative market constraints, including mass timber use intensity, market adoption/diffusion rates, and market penetration levels [36].

In Ganguly [36], all the demand forecast scenarios were based on a generally positive outlook for mass timber construction. The implicit assumption is that mass timber-based constructions will continue to be considered a low-risk viable alternative to traditional building systems. The Conservative scenario estimates were based on the principle that past behavior is the strongest predictor of future behavior. Accordingly, the conservative estimates relied heavily on previous wood innovation adoption trends in the countries/regions, and especially in the housing construction sector. Therefore, in this scenario, China had the lowest, and Europe had the highest mass timber demand. The Optimistic scenario estimates used the conservative parameters as the baseline and added greater levels of information dissemination and willingness-to-adopt new technology factors to the model. The Extreme scenario estimates used optimistic estimates as the baseline, and added higher levels of product satisfaction associated with mass timber and higher rates of information dissemination. In this scenario, mass timber constructions were considered a significant economic/functional improvement over traditional technology. These assumptions led to China’s very high projected mass timber demand levels in the “optimistic” and the “extreme” scenarios [36]. Here it may be noted that the most likely scenario will be somewhere between the Conservative and the Optimistic scenarios. The Extreme scenario was identified as a less likely scenario, but was modeled to develop an estimate of the extreme wood demand scenario. In this paper, we used the Extreme scenario to get an insight of the upper limit of effects on the global forests and wood products sector, though we acknowledge that this scenario is less likely.

2.2. Forest Resource Outlook Model (FOROM)

The projected impacts on the forest product markets of alternative mass timber demand scenarios in individual countries and world regions were evaluated by utilizing the FOROM. FOROM is a partial spatial price equilibrium (SPE) model of the world’s forest sector capable of endogenously modeling changes in forest resources (forest area and forest stock); timber harvests and prices; and production, consumption, trade, and prices of intermediate and final products, given future exogenous changes in socioeconomic growth, climate change, trade liberalization or forest management altering forest products demand, supply or trade conditions [38]. The term partial implies that all other sectors except the forest sector are treated as exogenous to the model. The model currently represents 20 different products (Table A1), and 60 different world regions, including six sub-regions within the U.S. (Table A2 and Figure A2), with the ability to expand regions and commodities when needed. The FOROM has been utilized in providing an outlook of the U.S. forest sector for the U.S. Forest Service 2020 Resource Planning Act (RPA) Assessment [38].

In line with the SPE theory [39,40], the FOROM assumes a competitive market, wherein the calculated equilibrium price and quantity for each year and each region are such that they maximize the sum of consumers’ and producers’ surpluses minus transportation costs, as shown in Equation (1).

where represents economic welfare for all products in all countries; and refer to the price and quantity of wood product k consumed by region j, while and refer to the manufacturing cost and production in region i. The cost of moving product k from region i to j, , is a function of the shipping and handling cost, , and the associated tariffs, .

The market equilibrium solutions for the subsequent years are provided based on a recursive dynamic optimization framework in which the results of the current period are saved and used as the inputs to calculate the market equilibrium in the subsequent periods.

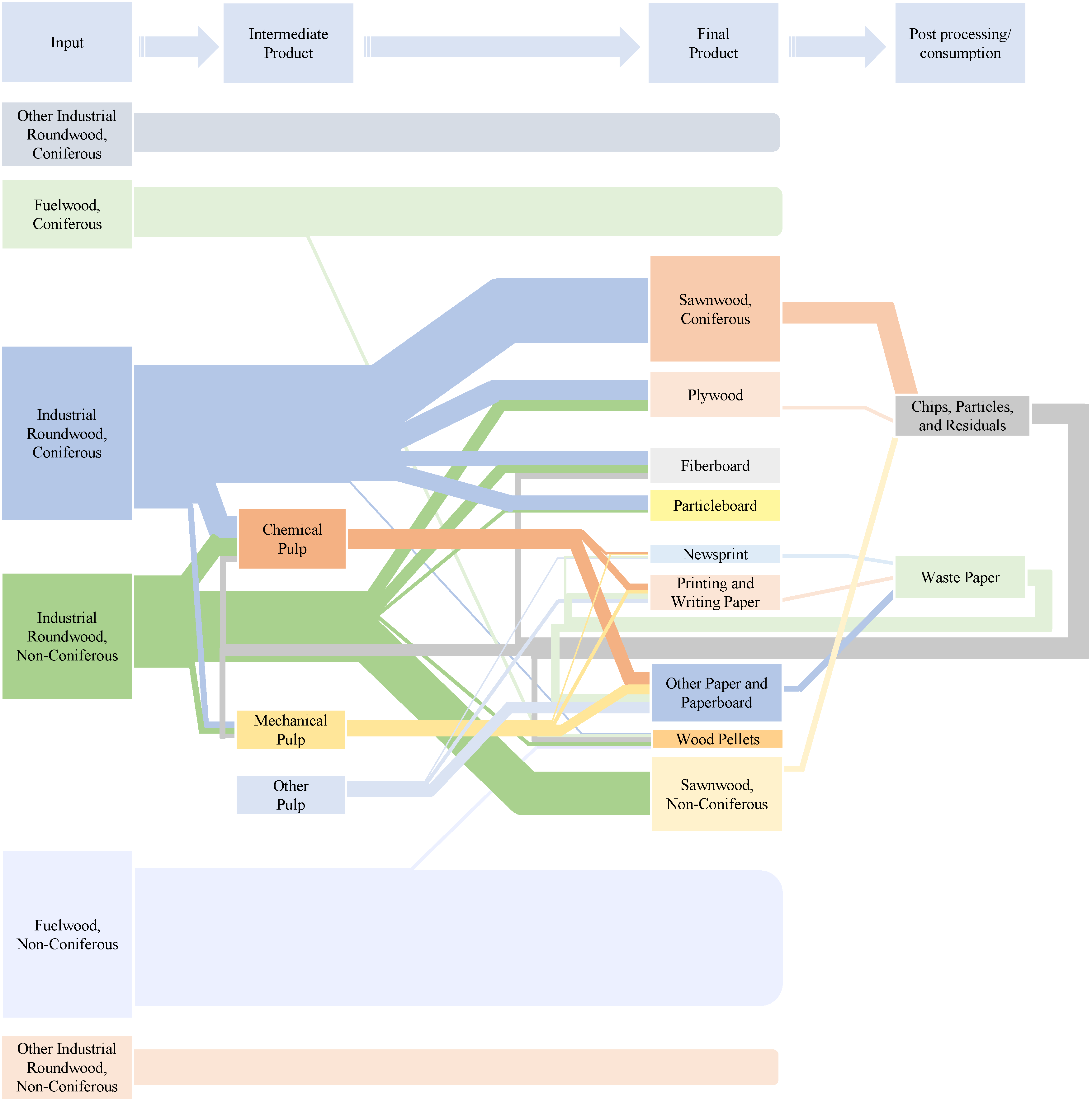

The FOROM provides market outcomes of 20 wood products, including 6 raw wood products representing the upstream supply chain (industrial roundwood, other industrial roundwood, and fuelwood by coniferous (softwood) and non-coniferous (hardwood) species groups), 5 intermediate products (chemical pulp, mechanical pulp, other pulp, waste paper and wood processing by-products such as chips and mill residues) and 9 final products (softwood and hardwood sawnwood (lumber), plywood, fiberboard, particle board, newsprint, printing and writing paper, other paper and paperboard, and wood pellets). The material flow from upstream to downstream markets, as simulated in the FOROM, is outlined in Figure A1.

The supply of raw materials in each country is modeled as a function of their own prices and forest stock, both of which are endogenously estimated by the FOROM. The demand for end-use products (e.g., sawnwood) for a country is modeled as a function of their own prices and exogenously projected gross domestic product (GDP) per capita. The production and consumption of intermediate products in each country are estimated by the specified manufacturing costs and their respective input–output coefficients (e.g., units of industrial roundwood required to produce a unit of manufactured product). The international trade (imports and exports) of a product is modeled between a country and the rest of the world, which is determined by the specified transport costs, manufacturing costs, input–output coefficients, and the endogenously solved domestic and world prices of a product.

Future changes in forest area in individual countries are estimated in the FOROM using a quadratic relationship of forest area with respect to GDP per capita and its squared term, based on the Environmental Kuznets Curve (EKC) theory [34,41,42]. The quadratic relationship of forest area with respect to GDP implies that forest area change is negative at low GDP per capita, becomes positive and increases at higher GDP per capita, and then decreases and approaches zero at very high GDP per capita [32]. In this study, the GDP per capita, and hence the projected forest area, remained the same between the alternative and BAU scenarios.

Forest stock, which shifts the supply curves of raw materials in the FOROM, evolves over time, as the previous year’s stock volume plus the projected current year growth volume minus the harvest quantity. Biological forest growth, the net of mortality, is modeled as a nonlinear function of forest stock density (forest stock divided by forest area), consistent with Global Forest Products Model (GFPM) [34]. The specified nonlinear negative relationship between forest growth and forest stock density implies that forest growth increases with declining stock density and decreases with increasing stock density.

Further details about the FOROM, including its mathematical structure, data input and sources, are provided in Appendix A.

2.3. Simulating Mass Timber Demand in FOROM

Changes to the demand for mass timber (CLT and Glulam combined) are assumed to manifest within the global forest products sector through an additional change in the demand for SW lumber, as shown in Equation (2):

where is the change in demand for softwood lumber (raw material for mass timber) in region j, is the benchmark demand for mass timber at time t, in region j, is the elasticity of demand with respect to the growth rate of GDP per capita, is growth rate of GDP per capita, and is the amount of SW lumber needed to produce 1 m3 of mass timber, which is assumed to be approximately 1.21 m3 based on Chen et al. [13].

The current model set up assumes that mass timber is produced and consumed only domestically (i.e., mass timber is not traded across countries). However, countries can trade the industrial roundwood and SW lumber needed to manufacture mass timber.

3. Results

3.1. Projected Mass Timber Demand

The projected demands for mass timber (CLT and glulam combined) in different countries and regions are shown in Table 1. The results of the demand projections indicate that the total global demands for mass timber (the sum of projected demand in 12 selected countries) are projected to increase to 8, 25, and 58 million m3 by 2060 in the Conservative, Optimistic, and Extreme mass timber demand scenarios, respectively. This projection is consistent with the characteristics of “new product diffusion models”, suggesting a slow initial adoption (trial phase) followed by a faster rate of adoption (growth phase), ultimately reaching full market potential (maturity phase) [43]. While the U.S. and Europe combined are projected to consume more than 80% of the projected total demand for mass timber in the Conservative scenario by 2060, China is projected to demand a substantial volume of mass timber in the Optimistic (38% of global demand by 2060) and the Extreme (62% of global demand by 2060) demand scenarios. The projected annual growth in mass timber demand during 2020–2060 ranged from 3% to 14% in individual countries among the Conservative, the Optimistic, and the Extreme scenarios, respectively (Table 1).

3.2. Impacts on Product Prices

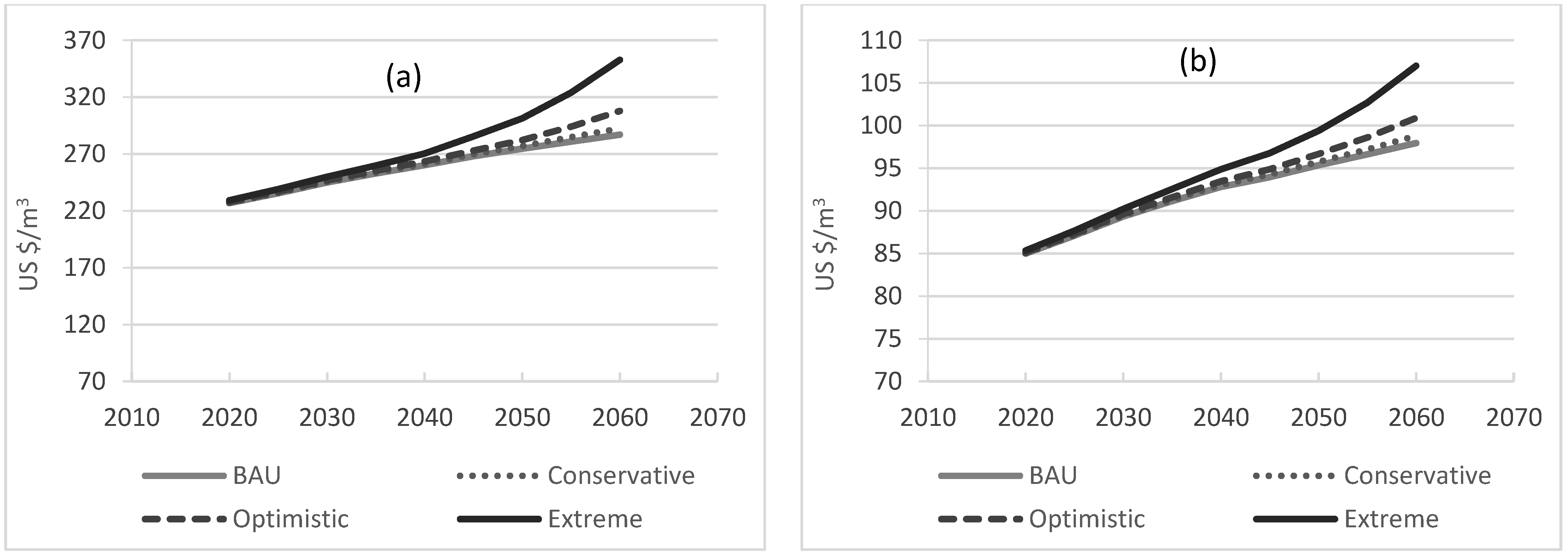

The projected increases in demand for mass timber in multiple countries were shown to drive up prices for SW lumber (raw material needed to manufacture mass timber) and SW industrial roundwood (raw material for SW lumber), not only in countries and regions with projected increases in mass timber demand, but also in a majority of other countries and regions without such extra mass timber demands. For instance, by 2060, the world prices of SW lumber were shown to increase by 2%, 7%, and 23% in the Conservative, Optimistic, and the Extreme scenarios, respectively, compared to the projected price level in the BAU scenario in 2060 (Figure 1a and Table 2). In contrast, the projected magnitudes of price increases in individual countries were relatively much higher (Table 2), consistent with the projected volumes of increases in demand for mass timber (Table 1). For example, in China, where mass timber demand in the Extreme scenario was projected to be 36 million m3 by 2060, the corresponding price increase for SW lumber was 61%, compared to the projected BAU price in the same year (Table 2). Price increases for SW lumber in other countries varied between as low as 1% (e.g., Argentina in the Conservative scenario) and as high as 31% (e.g., Brazil in the Extreme scenario) by 2060, relative to the respective price levels in the BAU scenario (Table 2).

Similar trends were observed in prices of SW industrial roundwood (raw material for SW lumber), with projected world price increases varying between 1% and 9% (Figure 1b), and prices in individual countries (Table 3) varying between 0.1% and 65% (China), by 2060, in the Conservative and Extreme scenarios, respectively, compared to the respective price levels projected in the BAU scenario in 2060. Changes in world prices for other products were small or negligible (not shown).

3.3. Impacts on Timber Harvests and Wood Product Markets

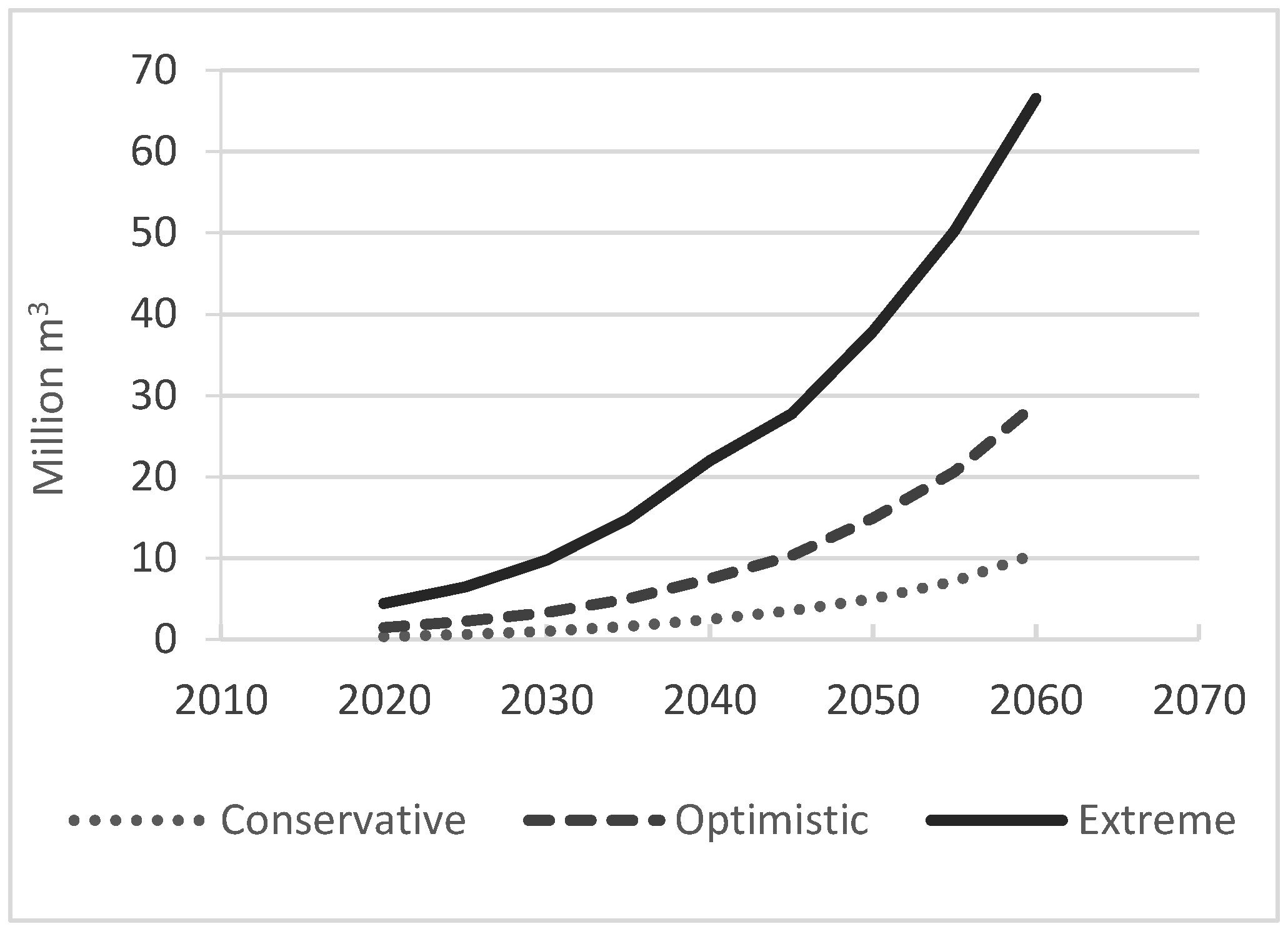

Most of the projected increases in demand for mass timber in multiple countries were met by increased domestic timber harvests (Table 4) and the production of SW industrial roundwood (Table 5) needed to manufacture SW lumber, and by its increased imports or reduced exports (Table 3). As a result, global total SW harvests increased by 10.8, 30.0, and 68.2 million m3 by 2060, representing 0.7%, 1.8%, and 4.2% increases in the Conservative, the Optimistic and the Extreme mass timber demand scenarios, respectively, relative to the projected BAU harvest levels in the same year (Table 4). At the individual country level, SW total harvests increased by up to 58% by 2060 (China in the Extreme scenario). Other countries showing notable increases in coniferous harvests by 2060 (Table 4) include Argentina (12%), France (7%), Canada (5%), New Zealand (5%), Germany (3%), and Chile (3%). Oceania (mainly New Zealand) was projected to supply most of the global import demands for SW industrial roundwood (4.2 million m3 by 2060 in Extreme scenario), followed by Europe (0.9 million m3) and North America (0.1 million m3), reflecting their comparative advantages in SW industrial roundwood production and trade. Unlike SW harvests, total global HW harvests declined slightly (not shown) in response to the increased production of SW byproducts (e.g., residues, chips, particles), which displaced HW industrial demand to some degree. Taking both species together, the global total harvests (Figure 2 and Table 4) increased by 10.5, 29.0, and 66.5 million m3 by 2060 in the Conservative, the Optimistic and the Extreme mass timber demand scenarios, representing 0.2%, 0.7% and 1.6% increases, respectively, relative to BAU harvest levels in 2060.

Most of the additional quantities of mass timber demanded in multiple countries were shown to be met by an expanded domestic production of SW lumber (raw material for mass timber) in those countries (Table 6), and a small portion of the remaining demands were met by imports from other countries (Table 2) where a demand for mass timber was non-existent or was not modeled. The remaining balance of SW lumber demand was met by a diversion of SW lumber consumption away from the traditional sector (e.g., light-frame construction and furniture sectors), suggesting that the higher mass timber demand would lead to market competition for SW lumber between traditional use and mass timber building use. For example, out of some 69 million m3 of SW lumber needed to fulfill projected global demand for mass timber in 2060 in the Extreme scenario (Table 1), about 52 million m3 was provided by increased global production, and the remaining 17 million m3 (about 25%) by the reduced consumption and diversion of SW lumber away from the traditional wood use sector (Table 6).

Among some noteworthy outcomes at the individual country level, China was shown to meet its 2060 demand for mass timber in the Extreme scenario (equivalent to 43 million m3 of SW lumber) by expanding its domestic production of SW lumber by 26.5 million m3 (61%) (Table 6), its increased imports by 5.2 million m3 (12%) (Table 2), and the diversion of SW lumber consumption away from traditional sector by 11.6 million m3 (27%) (Table 6). Canada, where mass timber demand was not modeled, was shown to supply most of the global import demand for SW lumber (5.1 million m3), followed by Europe (1.3 million m3) and Oceania (0.4 million m3) (Table 2). Other countries with notable increases in SW lumber production by 2060 in the Extreme scenario were Spain (29%), Ukraine, Argentina and Brazil (19% each), Turkey (15%), and France and Finland (14% each). Note that Ukraine and Turkey did not have any projected increase in mass timber demand (note shown).

By increasing prices for SW industrial roundwood and making it costly to manufacture products that utilize SW lumber, the key effect of increased mass timber demand on other products was to reduce the production of those products that utilize SW industrial roundwood as the main raw material (e.g., plywood, particleboard). However, the increased fiber residue that came with the increased SW lumber production helped partially offset the increased manufacturing costs of those products, resulting in only slight declines in their production (not shown).

3.4. Impacts on Forest Stock

Our projected impacts on total forest stock represent aggregate country-level impacts, which may differ from the impacts at the individual forest plot or stand level (more detailed analysis of the impacts on forests at the stand and subregional levels is planned in phase 4 of the five-phase project led by the Nature Conservancy). The aggregate amount of future forest stock depends on current forest stock, amount of stock removed as harvest, and net volume added to the stock from forest biomass growth (net of mortality). The forest sector modeling in this study indicated the relatively smaller effects on projected global, regional, and national forest stock of increased mass timber demand scenarios, despite notable increases in harvest levels in individual countries and globally. For example, in the Extreme scenario, where worldwide SW harvests will increase by more than 4.2% by 2060 (Table 4), global forest stock declines only by one-third of a percent, relative to the projected forest stock level in the BAU scenario by 2060 (Table 7). In absolute terms, the projected depletions in global total forest stock by 2060 are 37, 104, and 182 million m3 in the Conservative, Optimistic and Extreme scenarios, representing one-tenth, two-tenths, and three-tenths of a percent declines, respectively, relative to the corresponding projected forest stock level in the BAU scenario by 2060 (Table 7).

The projected effects on forest stocks reflect the forest management assumption embedded in our model, whereby forestland areas between the BAU and alternative scenarios were assumed to remain as forestland. That is, mass timber-induced increases in demand for timber and harvest activities do not lead to deforestation, although our model does consider net changes in forest area (net of deforestation and afforestation) based on the EKC theory, which suggests a quadratic relationship of forest area with GDP per capita [34,41,42]. However, the projected forest area remained the same between the BAU and alternative mass timber demand scenarios because we used the same projected GDP per capita for the alternative and reference scenarios. Implicitly embedded in our model as well is an assumption of regeneration occurring after the harvesting of a forest stand. The model mimics regeneration activity by incorporating an inverse relationship of forest biomass growth with respect to forest stock density (forest stock divided by forest area). With forest area remaining the same between the BAU and alternate scenarios, a loss in forest stock due to mass timber-induced increases in harvests leads to lower forest stock density, which further leads to relatively higher forest biomass growth. Thus, all or parts of the loss in forest stock due to the increased removals required to meet mass timber demand are offset over time by relatively faster biological forest growth (e.g., occurring in younger stands after regeneration). Thus, our modeling indicates that the three contrasting scenarios of mass timber demand in multiple countries could lead to increases in worldwide cumulative removals of about 140 to 1057 million m3 within the next 40 years, and that more than 73% to 82% (103 to 876 million m3) of such extra removals from global forests would be offset by biological growth occurring within this period, leading to only small declines in forest stock over the projection period.

4. Discussion and Conclusions

Based on forest resources and wood products market modeling grounded on sound economic theories and methods, our study contributes to an enhanced understanding of the potential effects of increased mass timber consumption on forest resources and forest product markets in individual countries, regions and the world, which were not available in the past literature. Specifically, the findings of this study help answer several questions that have been raised about the potential effects on aggregate forest resources and the traditional forest industry of future large increases in mass timber consumption in multiple countries.

As demonstrated by our economic analyses that consider global market interactions, the effects of increases in demand for mass timber in a country or a region are not necessarily confined to those countries or regions, but can also be felt across other countries and regions via altered consumption, production, and trade patterns stemming from mass timber-induced changes in the prices of timber and manufactured wood products. Therefore, an evaluation that does not consider such international linkages in forest product markets cannot provide valid insight into the overall effect of mass timber on forests and the forest products sector. Our analyses consider such linkages, and provide an evaluation of relatively longer-term dynamics in forest resources (removal, growth, and standing inventory) and in forest product markets (prices, production, consumption, and trade) in individual countries, given varying trajectories of mass timber consumption envisioned over the next 40 years in 12 countries in Asia, Europe, North America, and South America. Given that forestry is a long-term investment venture (it takes several years or decades to generate income from investment today), and that the forest products industry is relatively slow to adapt to changing market conditions, the information presented in this study about the anticipated longer-term effects of increased mass timber demand on forests and the forest products sector will be helpful to forestland owners, the forest products industry, and related stakeholders in making informed decisions today.

The key findings of our global analyses are: (1) increases in mass timber demand will lead to increases in prices for products that are utilized in mass timber industry supply and value chains, and the magnitude of such increases will depend on the magnitude of mass timber demand; (2) the levels of change in worldwide and countrywide product prices alter the production, consumption and trade of forest products in a country, and accordingly alter its timber harvest, forest growth and forest stock level; (3) the increased demand for mass timber will lead to market competition for SW lumber and industrial roundwood between traditional use and mass timber use, and (4) when forests are managed sustainably, most of the projected depletion in aggregate forest stock due to mass timber-induced increases in removals will be replaced by biological forest growth occurring over time, suggesting relatively smaller impacts on forest stock at aggregate national, regional, and global levels.

Each of these findings has important implications for global forest resources and the forest products industry. For example, the projected increases in timber prices across countries and regions due to higher demand for mass timber will raise the economic value of forestland, and therefore provide an economic incentive against the conversion of forestland to other more profitable land uses in the absence of timber price increase. That is, forest landowners will be more likely to keep forests as forests when timber prices are increasing. Timber price increases will also provide economic incentives for the forest landowners to invest in forest plantations and/or intensified forest management activities, such as thinning [44,45,46]. This is an important positive effect of mass timber on the forest sector, given that forestland owners have been struggling with low forest rents worldwide (low timber prices) in recent years. Our analysis finds that landowners in China, Spain, Malaysia, Argentina, Ukraine, Myanmar, and New Zealand will receive more of such economic incentives (Table S1 in Supplementary Materials), as demonstrated by the relatively higher projected prices for SW industrial roundwood in those countries (10% to 65% increases by 2060 in the Extreme mass timber scenario). However, it should be noted that such market-induced effects on forest resources will depend on various biophysical, economic, and policy variables not modeled in this study, and therefore need further consideration.

The implication for the traditional forest products industry of a projected increase in SW industrial roundwood prices due to increases in mass timber demand is that it would raise the production cost of products that utilize SW industrial roundwood in the downstream supply chain (e.g., SW lumber, plywood, particleboard, etc.), forcing the prices of those products to increase. As a result, the consumption of those products in the traditional end-use sector would decline. Such an impact was shown to be more severe in the case of SW lumber, which showed about a 4% (17 million m3) global decline in its consumption (Table 6), and its diversion away from the traditional end-use sector towards the mass timber building sector. This is an outcome that can be attributed to a strong market competition for SW lumber between traditional use and mass timber use, resulting from mass timber-induced increases in its price. While other wood products sectors also saw some competition for raw materials due to increased mass timber demand (e.g., SW industrial roundwood use between wood-based panel production vs. lumber production), the effects on their consumption and production were minimal, since part of the expensive industrial roundwood could be substituted by the relatively cheaper by-products resulting from the increased production of SW lumber (e.g., chips and mill residues). These results suggest that an increase in mass timber consumption would bring about an unambiguous increase in global timber and primary product producers’ welfare, but reduced welfare for the consumers of SW lumber in the traditional end-use sector, with unknown net effects on the entire forest products industry. Therefore, any forest sector policy that aims to promote mass timber use should consider this potential market competition and associated impacts on the traditional wood-using sector.

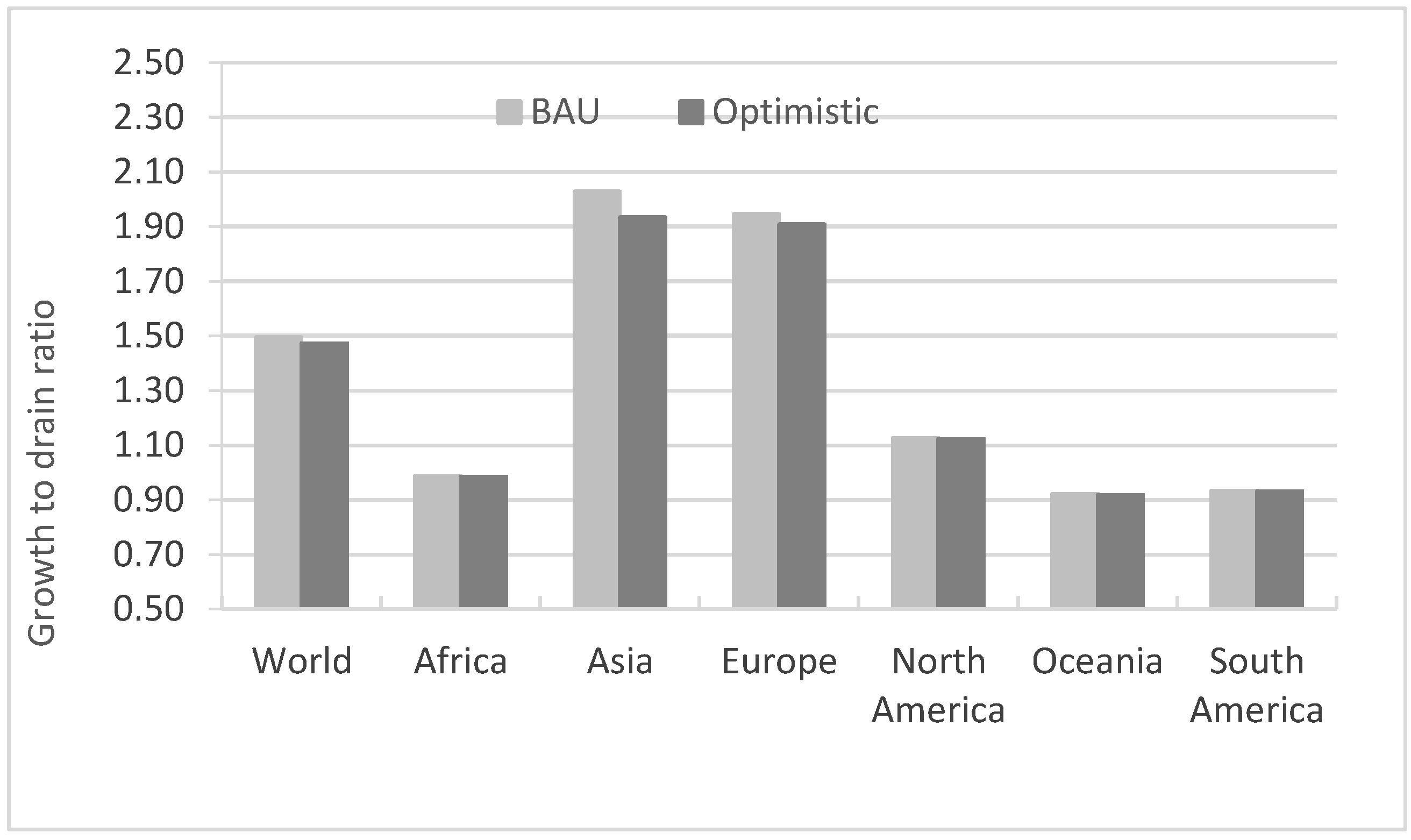

Our study also begins to clarify some ambiguities surrounding the likely effects of increased mass timber demand on forest stock (and forest carbon) at national, regional and global levels. Our biophysical and market analyses indicate that even a large increase in mass timber demand would have minimal impacts on aggregate forest stock, if forests are managed sustainably. Our aggregate national-level finding is in concurrence with similar arguments presented in previous studies describing the forest resource-side impacts of increased mass timber demand, specifically in the US and Canada [6,28,47]. Sustainably managed forests means that forest stands remain as forest stands, and harvested forest stands are replaced by replanting/regeneration, allowing depleted forest stock to recover via the relatively faster growth of regenerated young stands. Based on this important premise, our analysis finds that more than 70 to 83% of the projected global decline in forest inventory would be offset by biological growth occurring over the next 40 years (Table S2 in Supplementary Materials). It should be noted that if the economic incentives provided by timber price increases to invest in plantation and/or intensified management activities were considered, they would further contribute towards increasing biomass growth and offsetting forest stock loss from increased harvests. However, in some countries, especially with insufficient laws and poor forestry governance, higher timber prices may encourage illegal harvest and/or deforestation activities. More research on potential forest impacts at a finer resolution (e.g., forest stand and local context), using our projected aggregate impacts on wood product markets (timber supply, price, manufacturing activities, and trade), is ongoing. Another metric frequently used to evaluate the sustainability of forest management is “growth to drain” ratio, a ratio of forest growth to removals. A growth to drain ratio greater than one indicates that less volume than the growth is being removed (sustainable harvest). Our analysis indicates that this growth to drain ratio would decline only slightly in all scenarios compared to the BAU in all countries, regions, and the world (Figure 3), reinforcing our findings that the aggregate country-, regional-, and global-level effects on forest resources of even large increases in mass timber would be minimal, provided forests are managed sustainably.

The global findings that increased mass timber demand would have minimal impacts on forest stock in a sustainably managed forest are of considerable importance, as they relate to carbon mitigation efforts through increasing mass timber use in buildings. A smaller depletion in global forest stocks (and carbon) means that a higher carbon benefit could be realized by avoiding carbon emissions resulting from the substitution of carbon-intensive non-wood materials with mass timber, and from carbon stored in mass timber products being used in buildings [22]. The effects on forest stocks of increased mass timber demand estimated in this study also provide an insight into a potential leakage effect that could occur due to increased harvests (and depleted forest stock) in a country or region that supplies wood to mass timber-consuming regions. For example, New Zealand, where mass timber was not modeled, is shown to supply most of the world’s import demand for industrial roundwood, depleting their total forest stock by 25 million m3 by 2060 in the Extreme mass timber demand scenario (Table S2). Similarly, Canada, where also mass timber demand was not modeled, was shown to supply most of the global import demand for SW lumber (5.1 out of 9.3 million m3), driving down their total forest stock by 53 million m3 by 2060 in the Extreme mass timber demand scenario (Table S2). These outcomes suggest that any meaningful evaluation of the carbon impacts of increased mass timber consumption in a particular country should also consider potential forest carbon losses in exporting countries or regions.

While the results presented in this study are derived from statistically and economically robust models grounded on sound economic principles and theories, they suffer from some limitations and uncertainties inherent to such modeling efforts. One limitation is that our modeling approach could not incorporate future demand for mass timber in potential mass timber-consuming countries, such as Canada, Japan, Australia, New Zealand, and other countries, given the limited number of countries included in the Ganguly study [36]. Including additional mass timber demand from additional countries would have resulted in higher product prices and related effects on wood product markets and forest stocks than those presented here. Uncertainties in our results may have also been introduced via the forecasted demand for mass timber in various countries, through the various parameters and assumptions used to obtain those forecasts. Therefore, to the extent that those forecasts are uncertain, our results are also uncertain. Another source of uncertainty in our results could stem from the parameters of various equations (Appendix A) utilized in the FOROM, which were assumed to remain unchanged throughout the projection period. These parameters were statistically estimated using historical data, representing past and current market conditions. Therefore, if future market conditions differ from those captured in the historical model, our projections would be uncertain. Finally, we acknowledge that our results did not explicitly consider competition for land between various uses. For example, depending on the economics of land uses (e.g., land rent), land area use can switch from forestry to agriculture and vice versa. However, despite these limitations and uncertainties, we believe that the direction of effects and the key conclusions drawn from our analyses would still be valid, and are useful in providing an insight into the longer-term impacts of future increases in mass timber demand on forests and the forest product markets in individual countries, regions, and the world.

Supplementary Materials

The following are available online at https://0-www-mdpi-com.brum.beds.ac.uk/article/10.3390/su132413943/s1, Table S1: FOROM-projected differences in prices (USD/m3, in constant 2015 USD) of industrial roundwood in 2060 between the alternative mass timber demand and BAU scenarios in selected countries, Table S2: Projected changes in cumulative harvests and growth (million m3), and growth to drain ratio, 2020–2060, across alternative mass timber demand scenarios in selected countries.

Author Contributions

Conceptualization, P.N. and C.M.T.J.; methodology, P.N., C.M.T.J. and I.G.; formal analysis, P.N., C.M.T.J. and I.G.; writing—original draft preparation, P.N.; writing—review and editing, P.N., C.M.T.J. and I.G.; visualization, P.N. and C.M.T.J. All authors have read and agreed to the published version of the manuscript.

Funding

This research was funded through a cooperative agreement between the USDA Forest Service, Forest Products Laboratory and The Nature Conservancy (17-CA-11111169-031). The development of the FOrest Resource Outlook Model was supported through an international joint venture agreement between Craig Johnston and the United States Forest Service, Southern Research Station (20-IJ-11330180-050).

Data Availability Statement

Most of the pertinent data are provided in the manuscript and the Supplementary Information. Additional data are available upon request to the corresponding author.

Acknowledgments

Authors would like to thank Delton Alderman, Jesse Henderson and three anonymous reviewers for their review of the original version of this manuscript, as their comments helped improve this paper.

Conflicts of Interest

The authors declare no conflict of interest. The funders had no role in the design of the study; in the collection, analyses, or interpretation of data; in the writing of the manuscript, or in the decision to publish the results.

Appendix A. Structure and Mathematical Formulations of the Forest Resource Outlook Model (FOROM)

Appendix A.1. Objective Function

The FOROM model consists of a static phase and a dynamic phase. In the static phase, the model maximizes economic welfare for all products in all countries following the law of one price, consistent with the spatial price equilibrium (SPE) framework [41,42], where differences in prices between regions are assumed to arise from differences in transport costs (including tariffs and other non-tariff barriers). As such, the objective function maximizes the sum of consumers’ and producers’ surplus net transport costs, subject to different constraints related to material balance, resource feasibility, and equilibrium condition, as shown in Equation (A1):

where and refer to the price and quantity of wood product k consumed by region j, while and refer to the manufacturing cost and production in region i. The cost of moving product k from region i to j, , is a function of the shipping and handling cost, , and the associated tariffs, .

The supply of final demand products f from all regions i to region j, including domestic supply, must be greater than or equal to the demand in region j:

where the shadow price gives the demand price,

Dual Variable

It follows that the sale of wood products k from region i to all regions j must be no larger than what is produced in region i:

where the shadow price gives the demand price,

Dual Variable

Appendix A.2. Consumer Sector

Consumers’ behavior is represented by a set of constant elasticity demand functions for each final demand product, f ⊆ k:

where symbols embellished with a bar indicate benchmark levels and ≤ 0 is the price elasticity of demand. Demand can be linearly approximated by first finding the tangency with the benchmark price and quantity demanded, where small changes in price and quantity are given by

and then rearranged into an inverse constant elasticity of the demand curve

or, simply, in reduced form,

Appendix A.3. Producer Sector

Similarly, each supply region i is assumed to have a set of constant elasticity supply curves for each product k, with price elasticity of supply ≥ 0,

which can be linearly approximated in a similar fashion as described for final product demand using benchmark manufacturing costs and quantities, as

or, simply, in reduced form,

Appendix A.4. Industrial Processing

Industrial processing activity converts a raw, recycled, or intermediate wood material into an intermediate or end wood product. These types of activities are modeled by a matrix of input–output coefficients, {}, which determines the amount of the inputs k used to produce outputs n of downstream products.

Appendix A.5. International Trade

The SPE framework assumes competitive markets for homogenous products, thus price differences between regions are equal to the per unit costs of transportation (and duty, tax and tariff if any) to exhaust all foreseen arbitrage opportunities. All products, k, are tradable in FOROM. The costs of transporting product k from region i to region j can be represented as .

Appendix A.6. Material Balance

To satisfy the material balance in any given country i and product k, production plus imports must equal the sum of consumption, exports, and the input of product k required in manufacturing output n.

The manufacture of byproducts (i.e., sawmilling byproducts, recycled paper) is a function of primary product manufacturing, represented by:

where is the amount of byproduct b ⊆ k recovered per unit of manufactured output n.

In the static phase, equilibrium prices, quantities and net trade levels are obtained by solving the problem of maximizing the objective function, subject to the above-mentioned constraints (2, 3, 11). Once a solution for the current period, t, is determined, the model will enter the dynamic phase, in which the parameters of the model are updated based on exogenous drivers (e.g., GDP growth, population growth, changes in productivity, etc.) and endogenous variables (e.g., harvest levels, standing stock levels, etc.) in preparation for the next iteration cycle.

Appendix A.7. Market Dynamics

Demand is assumed to change over time through exogenous shifts in GDP per capita, , and is translated through the growth rate of per capita GDP, , and the elasticity of demand with respect to the growth rate of per capita GDP, :

The supply of harvestable (roundwood) inputs (i.e., industrial roundwood, fuelwood, other roundwood) is assumed to change over time through exogenous shifts in forest area and forest stock:

where is an exogenous change in the growth rate of forest area at time t, is an endogenously determined growth rate of forest inventory, which changes over time based on the specified nonlinear negative relationship between forest growth and stocking density (I/A), and and are elasticities associated with forest area and inventory, respectively.

The supply of other fiber pulps, derived from recovered paper or from fibrous vegetable materials other than wood (i.e., outside forest), is assumed to change over time through exogenous shifts in per capita GDP, and is translated through the elasticity of supply with respect to per capita GDP, :

Appendix A.8. Data

The Food and Agricultural Organization (FAO) Forestry Production and Trade Database [25] and the FAO Global Forest Resource Assessment (FRA) Report [48,49] constitute the main data sources for the construction of the reference year price, quantity, and trade level. The FAOSTAT provides data on production, import value, import quantity, export value and export quantity, whereas the FRA reports provide data on forest area, forest inventory, and their rates of growths over time. Consumption is calculated as production plus import minus export. Because data on the prices of all 20 forest products are not available in the FAOSTAT database, they were derived as unit values of imports or exports (import or export value in USD divided by import or export quantity), following the method used in [34].

The reference or the base year for the FOROM model was set to 2015, the most recent year for which most of the production, trade and forest resource data are available. A goal programming approach was employed to deal with the missing or inconsistent data (e.g., negative consumption, gap between total import and export), which also produces the revised estimates of input–output coefficients and the manufacturing costs for each country/region. The calculated manufacturing costs, under the assumption of a competitive market equilibrium, are equal to the price of the product’s output minus the cost of the product’s wood and fiber input, leading to zero profit on each market. The per unit transportation cost data represent a percentage of the import unit price of the product (cost, insurance and freight, or CIF), as estimated and used in GFPM [34].

Key model parameters such as price and the income elasticities of demand and supply for various wood products are consistent with the ones used in GFPM [34]. The parameters for non-coniferous sawnwood and wood pellets, products that are not modeled in GFPM, come from Jonsson et al. [50]. Socioeconomic parameters such as GDP and population (and GDP per capita), which drive the demand/supply functions, and forest areas were obtained from the International Institute for Applied System Analysis (IIASA) Shared Socioeconomic Pathways (SSP) Database (https://tntcat.iiasa.ac.at/SspDb/dsd?Action=htmlpage&page=welcome (accessed on 10 August 2021)). In this paper, we used GDP and population projected for SSP2 to drive forest product demand in both BAU and the alternate mass timber demand scenarios.

Downscaling U.S. country-level data into six Resources Planning Act (RPA) Assessment regions required additional information and assumptions. The GDP and population data for U.S. aggregate and sub-regions were obtained from Wear and Prestemon [51], who developed a method to jointly downscale national-scale income and population projections to the county level. This method was designed through the statistical estimation of the relationships between historical personal income and population at the county scale. The downscaled GDP and population data for U.S. are available for all five SSPs in Wear and Prestemon [52].

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Table A1.

Wood product categories represented in FOROM.

| Name | Description | Units |

|---|---|---|

| Industrial roundwood | Sawlogs and veneer logs; pulpwood, round and split; and other industrial roundwood. | m3 |

| Fuelwood | Roundwood that will be used as fuel for purposes such as cooking, heating or power production. | m3 |

| Other roundwood | Industrial roundwood (wood in the rough) other than sawlogs, veneer logs and/or pulpwood. | m3 |

| Sawnwood | Wood that has been produced from both domestic and imported roundwood, either by sawing lengthways or by a profile-chipping process, and that exceeds 6 mm in thickness. | m3 |

| Plywood | A panel consisting of an assembly of veneer sheets bonded together with the direction of the grain in alternate plies generally at right angles. Thin sheets of wood of uniform thickness, not exceeding 6 mm, rotary cut (i.e., peeled), sliced or sawn. | m3 |

| Particleboard | A panel manufactured from small pieces of wood or other ligno-cellulosic materials (e.g., chips, flakes, splinters, strands, shreds, shives, etc.) bonded together by the use of an organic binder together with one or more of the following agents: heat, pressure, humidity, a catalyst, etc. The particle board category is an aggregate category. It includes oriented strandboard (OSB), medium-density particle board (MDP), waferboard and flaxboard. | m3 |

| Fiberboard | A panel manufactured from the fibers of wood or other ligno-cellulosic materials with the primary bond derived from the felting of the fibers and their inherent adhesive properties (although bonding materials and/or additives may be added in the manufacturing process). It includes fibreboard panels that are flat-pressed and moulded fibreboard products. In JQ1 and JQ2, it is an aggregate comprising hardboard, medium/high density fibreboard (MDF/HDF) and other fibreboard. | m3 |

| Mechanical pulp | Wood pulp obtained by grinding or milling pulpwood or residues into fibers, or through refining chips or particles. | t |

| Chemical pulp | Wood pulp obtained by subjecting pulpwood, wood chips, particles or residues to a series of chemical treatments. It includes sulfate (kraft) wood pulp, soda wood pulp and sulfite wood pulp. | t |

| Other pulp | Pulp manufactured from recovered paper or from fibrous vegetable materials other than wood and used for the manufacture of paper, paperboard and fiberboard. | t |

| Newsprint | Paper mainly used for printing newspapers. It is made largely from mechanical pulp and/or recovered paper, with or without a small amount of filler. | t |

| Printing and writing paper | Paper, except newsprint, suitable for printing and business purposes, writing, sketching, drawing, etc. Made from a variety of pulp blends and with various finishes. | t |

| Other paper and paperboard | Other papers and boards for industrial and special purposes. | t |

| Wood pellets | Agglomerates produced either directly by compression or by the addition of a binder in a proportion not exceeding 3% by weight. | t |

| Chips, particles, and residuals | Wood that has been reduced to small pieces and is suitable for pulping, for particle board and/or fiberboard production, for use as a fuel, or for other purposes. | m3 |

| Waste paper | Waste and scraps of paper or paperboard that have been collected for re-use or trade. | t |

Note: Adapted from FAOSTAT definitions. http://www.fao.org/forestry/34572-0902b3c041384fd87f2451da2bb9237.pdf (accessed on 10 August 2021).

Table A2.

Countries and regions represented in FOROM in the current study.

| Africa | Asia | Europe | Central America | North America | Oceania | South America | World |

|---|---|---|---|---|---|---|---|

| Nigeria | China | Austria | Rest of Central America | Canada | Australia | Argentina | Rest of World |

| South Arica | India | Belarus | Mexico | New Zealand | Brazil | ||

| Rest of Africa | Indonesia | Belgium | United States | Rest of Oceania | Chile | ||

| Japan | Estonia | North Central | Uruguay | ||||

| Malaysia | Finland | North East | Rest of South America | ||||

| Myanmar | France | Pacific Coast | |||||

| Russian Federation | Germany | Rocky Mountain | |||||

| Thailand | Latvia | South Central | |||||

| Turkey | Norway | South East | |||||

| Viet Nam | Poland | Rest of North America | |||||

| Rest of Asia | Portugal | ||||||

| Romania | |||||||

| Russian Federation | |||||||

| Slovakia | |||||||

| Spain | |||||||

| Sweden | |||||||

| Ukraine | |||||||

| United Kingdom | |||||||

| Rest of Europe |

Figure A1.

Forest product flow chart in FOROM.

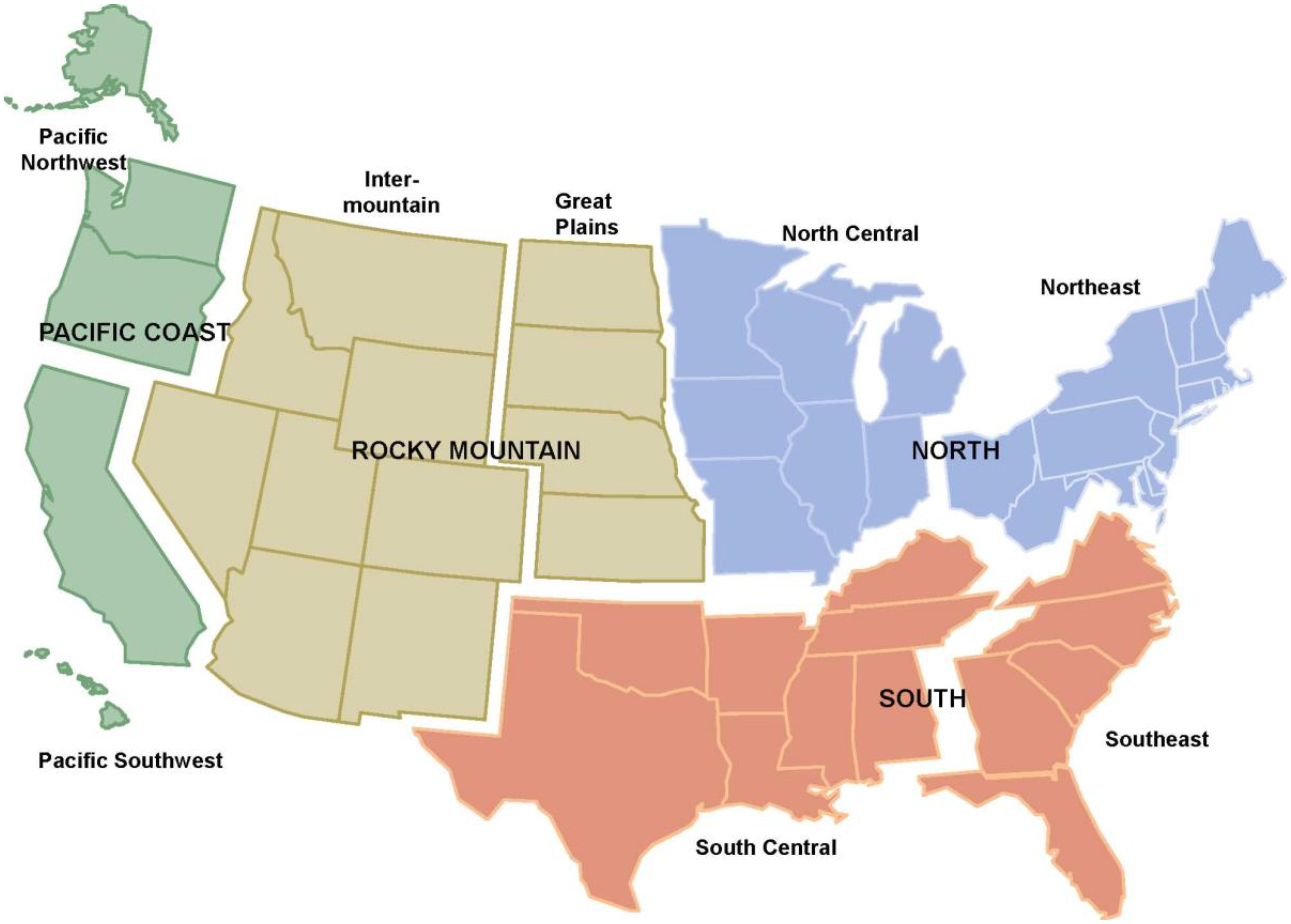

Figure A2.

United States regions under the Resource and Planning Act Assessment.

References

- UNEP. 2020 Global Status Report for Buildings and Construction: Towards a Zero-Emissions, Efficient and Resilient Buildings and Construction Sector. Available online: https://globalabc.org/sites/default/files/inline-files/2020%20Buildings%20GSR_FULL%20REPORT.pdf (accessed on 17 July 2021).

- UNDESA. World Urbanization Prospects: The 2018 Revision (ST/ESA/SER.A/420). Available online: https://population.un.org/wup/Publications/Files/WUP2018-Report.pdf (accessed on 17 July 2021).

- UNEP; IEA. Towards a Zero-Emission, Efficient, and Resilient Buildings and Construction Sector: Global Status Report 2017. Available online: https://www.worldgbc.org/sites/default/files/UNEP%20188_GABC_en%20%28web%29.pdf (accessed on 17 July 2021).

- Think Wood. Mass Timber in North America: Expanding the Possibilities of Wood Building Design. Available online: https://1r4scx402tmr26fqa93wk6an-wpengine.netdna-ssl.com/wp-content/uploads/2020/08/AR0820_CEU_THINKWOOD-REPRINT-2.pdf (accessed on 18 July 2021).

- Karacabeyli, E.; Gagnon, S. Canadian CLT Handbook. 2019. Available online: https://web.fpinnovations.ca/clt/ (accessed on 2 August 2021).

- Anderson, R.; Dawson, E.; Muszynski, L. 2021 International Mass Timber Report. Available online: https://www.masstimberreport.com/ (accessed on 3 August 2021).

- Breneman, S.; Timmers, M.; Richardson, D. Tall Wood Buildings and the 2021 IBC: Up to 18 Stories of Mass Timber. Wood Works Wood Products Council. Available online: https://www.awc.org/pdf/education/des/AWC-DES607A-TallWood2021IBC-190619-color.pdf (accessed on 3 August 2021).

- Cover, J. Mass Timber: The New Sustainable Choice for Tall Buildings. Int. J. High-Rise Build. 2020, 9, 87–93. [Google Scholar]

- Kenney, D.; Brickman, J.; Clemans, T.; Mundorff, K.; Tokarczyk, J. Advanced Wood Product Manufacturing Study for Cross-Laminated Timber Acceleration in Oregon & SW Washington. Available online: https://www.oregon4biz.com/assets/docs/CLT_Mfg_2017OregonBEST.pdf (accessed on 3 August 2021).

- Dolan, J.; Wilson, A.; Brandt, K.; Bender, D.; Wolcott, M. Structural design process for estimating cross-laminated timber use factors for buildings. BioResources 2019, 14, 7247–7265. [Google Scholar]

- Jeleč, M.; Varevac, D.; Rajčić, V. Cross-laminated timber (CLT)—A state of the art report. Građevinar 2018, 70, 75–95. [Google Scholar]

- Spiritos, J.; Fernholz, K. Creating Affordable Housing Opportunities with Mass Timber; Dovetail Partners Inc.: Minneapolis, MN, USA, 2021; Available online: https://www.dovetailinc.org/upload/tmp/1616011215.pdf (accessed on 7 August 2021).

- Chen, C.X.; Pierobon, F.; Ganguly, I. Life cycle assessment (LCA) of cross-laminated timber (CLT) produced in western Washington: The role of logistics and wood species mix. Sustainability 2019, 11, 1278. [Google Scholar] [CrossRef] [Green Version]

- Lan, K.; Kelly, S.; Nepal, P.; Yao, Y. Dynamic life cycle carbon and energy analysis for cross-laminated timber in the Southeastern United State. Environ. Res. Lett. 2020, 15, 124036. [Google Scholar] [CrossRef]

- Puettmann, M.; Sinha, A.; Ganguly, I. Life Cycle Assessment of Cross Laminated Timbers Produced in Oregon. CORRIM–Consortium for Research on Renewable Industrial Materials. Available online: https://corrim.org/wp-content/uploads/2019/02/Life-Cycle-Assessment-of-Oregon-Cross-Laminated-Timber.pdf (accessed on 10 August 2021).

- Liang, S.; Gu, H.; Bergman, R.; Kelley, S.S. Comparative life-cycle assessment of a mass timber building and concrete alternative. Wood Fiber Sci. 2020, 52, 217–229. [Google Scholar] [CrossRef]

- Pierobon, F.; Huang, M.; Simonen, K.; Ganguly, I. Environmental benefits of using hybrid CLT structure in midrise nonresidential construction: An LCA based comparative case study in the U.S. Pacific Northwest. J. Build. Eng. 2019, 26, 100862. [Google Scholar] [CrossRef]

- Teshnizi, Z.; Pilon, A.; Storey, S.; Lopez, D.; Froese, T.M. Lessons learned from Life cycle assessment and life cycle costing of two residential towers at the University of British Columbia. Procedia CIRP 2018, 68, 172–177. [Google Scholar] [CrossRef]

- ASMI. A Life Cycle Assessment of Cross-Laminated Timber Produced in Canada; Athena Sustainable Materials Institute: Ottawa, ON, Canada, 2013; Available online: http://www.athenasmi.org/wp-content/uploads/2013/10/CtoG-LCA-Canadian-CLT.pdf (accessed on 18 August 2021).

- Grann, B. A Comparative Life Cycle Assessment of Two Multistory Residential Buildings: Cross-Laminated Timber vs. Concrete Slab and Column with Light Gauge Steelwalls. FPinovations. Available online: https://library.fpinnovations.ca/en/viewer?file=%2fmedia%2fWP%2f3062.pdf#phrase=false&pagemode=bookmarks (accessed on 21 August 2021).

- Howe, J.; Fernholz, K. Building with Wood = Proactive Climate Protection; Dovetail Partners Inc.: Minneapolis, MN, USA, 2021; Available online: https://www.dovetailinc.org/report_pdfs/2015/building_with_wood.pdf (accessed on 1 September 2021).

- Nepal, P.; Skog, K.E.; McKeever, D.; Bergman, R.D.; Abt, K.L.; Abt, R.C. Carbon mitigation impacts of increased softwood lumber and structural panel use for nonresidential construction in the United States. For. Prod. J. 2016, 66, 77–87. [Google Scholar] [CrossRef] [Green Version]

- Muszynski, L.; Hansen, E.; Fernando, S.; Schwarzmann, G.; Rainer, J. Insights into the global cross-laminated timber industry. Bioprod. Bus. 2017, 2, 77–92. [Google Scholar]

- UNECE/FAO. Forest Products Annual Market Review 2019–2020. Available online: https://unece.org/sites/default/files/2021-04/SP-50.pdf (accessed on 11 July 2021).

- FAO. Forestry Production and Trade Database. Available online: http://www.fao.org/faostat/en/#data/FO (accessed on 7 August 2021).

- WoodWorks. Building Trends: Mass Timber. Available online: https://www.woodworks.org/publications-media/building-trends-mass-timber/ (accessed on 3 July 2021).

- CTBUH. Tall Buildings in Numbers. Available online: https://global.ctbuh.org/resources/papers/3350-TBIN.pdf (accessed on 27 June 2021).

- SLB. Mass Timber Outlook. Available online: https://softwoodlumberboard.org/wp-content/uploads/2021/03/SLB-Mass-Timber-Outlook-2021-Final-Condensed.pdf (accessed on 2 August 2021).

- Brandeis, C.; Taylor, M.; Abt, K.L.; Alderman, D.; Buehlmann, U. Status and Trends for the U.S. Forest Products Sector: A Technical Document Supporting the Forest Service 2020 RPA Assessment; General Technical Report SRS-258; USDA Forest Service, Southern Research Station: Ashville, NC, USA, 2021. [Google Scholar]

- Market Research Future. Cross Laminated Timber Market to Reach USD 3562.6 Million by 2027. Available online: https://www.globenewswire.com/en/news-release/2021/06/24/2252306/0/en/Cross-Laminated-Timber-Market-to-reach-USD-3-562-6-Million-by-2027-Report-by-Market-Research-Future-MRFR.html (accessed on 17 July 2021).

- Global Market Insights. Industry Trends. Available online: https://www.gminsights.com/industry-analysis/cross-laminated-timber-clt-market?utm_source=GoogleAds&utm_medium=Adwords&utm_campaign=HVAC-PPC&gclid=EAIaIQobChMI17P_h6CB8gIVGITICh1QKgjGEAAYAyAAEgJkcfD_BwE (accessed on 17 July 2021).

- Nepal, P.; Buongiorno, J.; Johnston, C.M.T.; Prestemon, J.; Guo, J. Global Forest Products Trade Model. In International Trade in Forest Products: Lumber Trade Disputes, Models and Examples; Kooten, G.C., van Voss, L., Eds.; CABI: Wallingford, UK, 2021; pp. 110–141. [Google Scholar]

- Johnston, C.M.T.; Radeloff, V.C. Global mitigation potential of carbon stored in harvested wood products. Proc. Natl. Acad. Sci. USA 2019, 116, 4526–14531. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Buongiorno, J. Global modelling to predict timber production and prices: The GFPM approach. For. Int. J. For. Res. 2015, 88, 291–303. [Google Scholar] [CrossRef]

- Nepal, P.; Ince, P.J.; Skog, K.E.; Chang, S.J. Forest carbon benefits, costs and leakage effects of carbon reserve scenarios in the United States. J. For. Econ. 2013, 19, 286–306. [Google Scholar] [CrossRef]

- Ganguly, I. Mass-Timber Adoption Projections in 12 Countries for Building Construction. Available online: https://www.cintrafor.org/mass-timber-demand.html (accessed on 22 August 2021).

- Ganguly, I. Modeling Alternatives and Visualization of Product Adoption and Usage in the Residential Construction Industry. Ph.D. Thesis, University of Washington, Seattle, WA, USA, 2008. [Google Scholar]

- Johnston, C.M.T.; Guo, J.; Prestemon, J.P. The Forest Resource Outlook Model (FOROM): A Technical Document Supporting the Forest Service 2020 RPA Assessment; General Technical Report SRS-254; USDA Forest Service, Southern Research Station: Ashville, NC, USA, 2021. [Google Scholar]

- Samuelson, P.A. Spatial price equilibrium and linear programming. Am. Econ. Rev. 1952, 42, 283–301. [Google Scholar]

- Takayama, T.; Judge, G. Spatial and Temporal Price and Allocation Models (Contributions to Economic Analysis); North-Holland: Amsterdam, The Netherlands, 1971. [Google Scholar]

- Dinda, S. Environmental Kuznets curve hypothesis: A survey. Ecol. Econ. 2004, 49, 431–455. [Google Scholar] [CrossRef] [Green Version]

- Nepal, P.; Korhonen, J.; Prestemon, J.P.; Cubbage, F.W. Projecting global and regional forest area under the Shared Socioeconomic Pathways using an updated Environmental Kuznets Curve model. Forests 2019, 10, 387. [Google Scholar] [CrossRef] [Green Version]

- Ganguly, I.; Beyreuther, T.; Hoffman, M.; Swenson, S.; Eastin, I. Forecasting the Demand for Cross Laminated Timber (CLT) in the Pacific Northwest. Available online: http://www.cintrafor.org/uploads/1/1/8/0/118098170/c4_news_2017.3_summer.pdf (accessed on 7 September 2021).

- Nepal, P.; Abt, K.L.; Skog, K.E.; Abt, R.C.; Jeffrey, P.P. Projected market competition for wood biomass between traditional products and energy: A simulated interaction of US regional, national, and global forest product markets. For. Sci. 2019, 65, 14–26. [Google Scholar] [CrossRef]

- Daigneault, A.; Favero, A. Global forest management, carbon sequestration and bioenergy supply under alternative shared socioeconomic pathways. Land Use Pol. 2021, 103, 105302. [Google Scholar] [CrossRef]

- Anderson, R.; Atkins, D.; Beck, B.; Dawson, E.; Gale, C.B. North American Mass Timber: State of the Industry 2020. Available online: https://masstimberreport.docsend.com/view/n6c8qap47cjd99ac (accessed on 3 June 2021).

- O’Connor, J.; Podesto, L.; Barry, A.; Grann, B. Environmental performance of cross-laminated timber. In CLT Handbook: Cross Laminated Timber; Karacabeyli, E., Douglas, B., Eds.; FPInnovations and Binational Softwood Lumber Council: Surrey, BC, Canada, 2013; pp. 443–493. [Google Scholar]

- FAO. Global Forest Resources Assessment 2015; FAO: Rome, Italy, 2015. [Google Scholar]

- FAO. Global Forest Resources Assessment 2010; FAO: Rome, Italy, 2010. [Google Scholar]

- Jonsson, R.; Rinaldi, F.; San-Miguel-Ayanz, J. The Global Forest Trade Model–GFTM; Report LB-NA-27360-EN-N; Publications Office of the European Union: Luxembourg, 2015. [Google Scholar]

- Wear, D.N.; Prestemon, J.P. Spatiotemporal downscaling of global population and income scenarios for the United States. PLoS ONE 2019, 14, e0219242. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Wear, D.N.; Prestemon, J.P. Socioeconomic data for Forest Service 2020 RPA Assessment; Forest Service Research Data Archive: Fort Collins, CO, USA, 2019. [Google Scholar]

Figure 1.

Projected world price of (a) softwood lumber and (b) softwood industrial roundwood in the BAU and the alternative mass timber demand scenarios.

Figure 1.

Projected world price of (a) softwood lumber and (b) softwood industrial roundwood in the BAU and the alternative mass timber demand scenarios.

Figure 2.

Projected changes in global total harvests in the alternative mass timber demand scenarios, relative to the projected harvest levels in the BAU scenario, 2020–2060.

Figure 2.

Projected changes in global total harvests in the alternative mass timber demand scenarios, relative to the projected harvest levels in the BAU scenario, 2020–2060.

Figure 3.

Projected coniferous growth to drain ratio in world regions by 2060 between the BAU and the Extreme mass timber demand scenarios.

Figure 3.

Projected coniferous growth to drain ratio in world regions by 2060 between the BAU and the Extreme mass timber demand scenarios.

Table 1.

The projected demand (thousand m3) for mass timber (CLT and Glulam combined, [36]) specified in FOROM in three alternative scenarios.

Table 1.

The projected demand (thousand m3) for mass timber (CLT and Glulam combined, [36]) specified in FOROM in three alternative scenarios.

| Alternative Mass Timber Demand Scenarios (Thousand m3) | |||||||||

|---|---|---|---|---|---|---|---|---|---|

| Conservative | Optimistic | Extreme | |||||||

| Country/Region | 2020 | 2040 | 2060 | 2020 | 2040 | 2060 | 2020 | 2040 | 2060 |

| Asia | 8 | 53 | 803 | 65 | 677 | 9399 | 523 | 5812 | 35,867 |

| China | 8 | 53 | 803 | 65 | 677 | 9399 | 523 | 5812 | 35,867 |

| Europe | 186 | 1224 | 3478 | 728 | 2363 | 4982 | 1672 | 3338 | 6220 |

| Austria | 8 | 51 | 154 | 31 | 98 | 218 | 71 | 137 | 268 |

| France | 61 | 391 | 1103 | 237 | 735 | 1533 | 535 | 1014 | 1868 |

| Germany | 29 | 198 | 495 | 114 | 382 | 711 | 262 | 539 | 888 |

| Spain | 30 | 196 | 610 | 117 | 386 | 892 | 273 | 557 | 1134 |

| United Kingdom | 32 | 217 | 670 | 128 | 437 | 1000 | 301 | 638 | 1290 |

| Rest of Europe | 26 | 171 | 446 | 101 | 326 | 628 | 229 | 454 | 773 |

| North America | 19 | 323 | 3064 | 128 | 1655 | 6534 | 653 | 3465 | 9253 |

| United States | 19 | 323 | 3064 | 128 | 1655 | 6534 | 653 | 3465 | 9253 |

| South America | 3 | 62 | 794 | 30 | 749 | 3901 | 246 | 3175 | 6385 |

| Argentina | 0 | 3 | 45 | 2 | 31 | 255 | 15 | 148 | 449 |

| Brazil | 1 | 27 | 336 | 13 | 328 | 1752 | 107 | 1459 | 2958 |

| Chile | 2 | 33 | 413 | 15 | 389 | 1894 | 124 | 1569 | 2979 |