Bibliometric Mapping of Research Trends on Financial Behavior for Sustainability

,

,  and

and

Abstract

:1. Introduction

1.1. Knowledge in Financial Education

1.2. Savings and Consumption Decisions

2. Materials and Methods

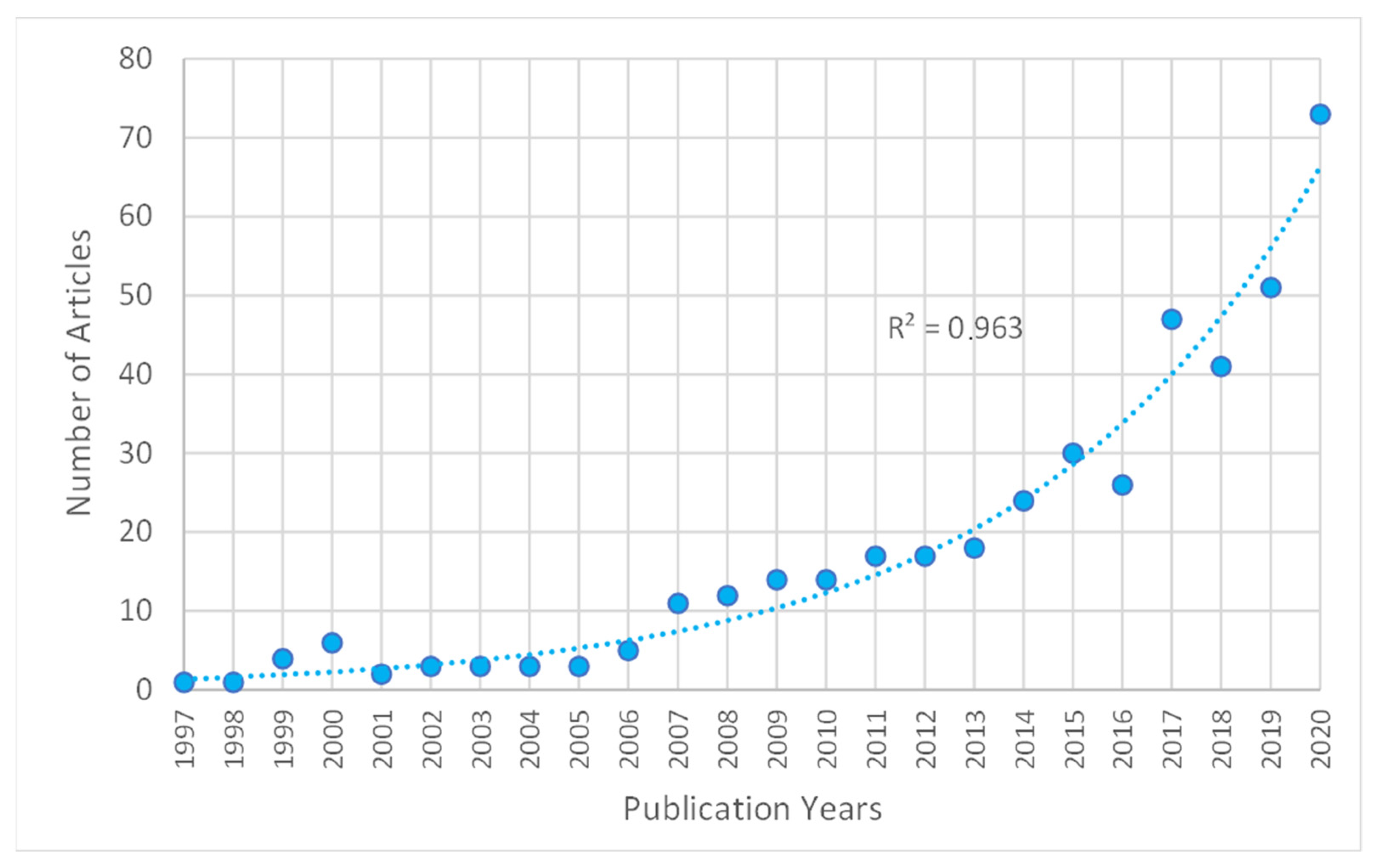

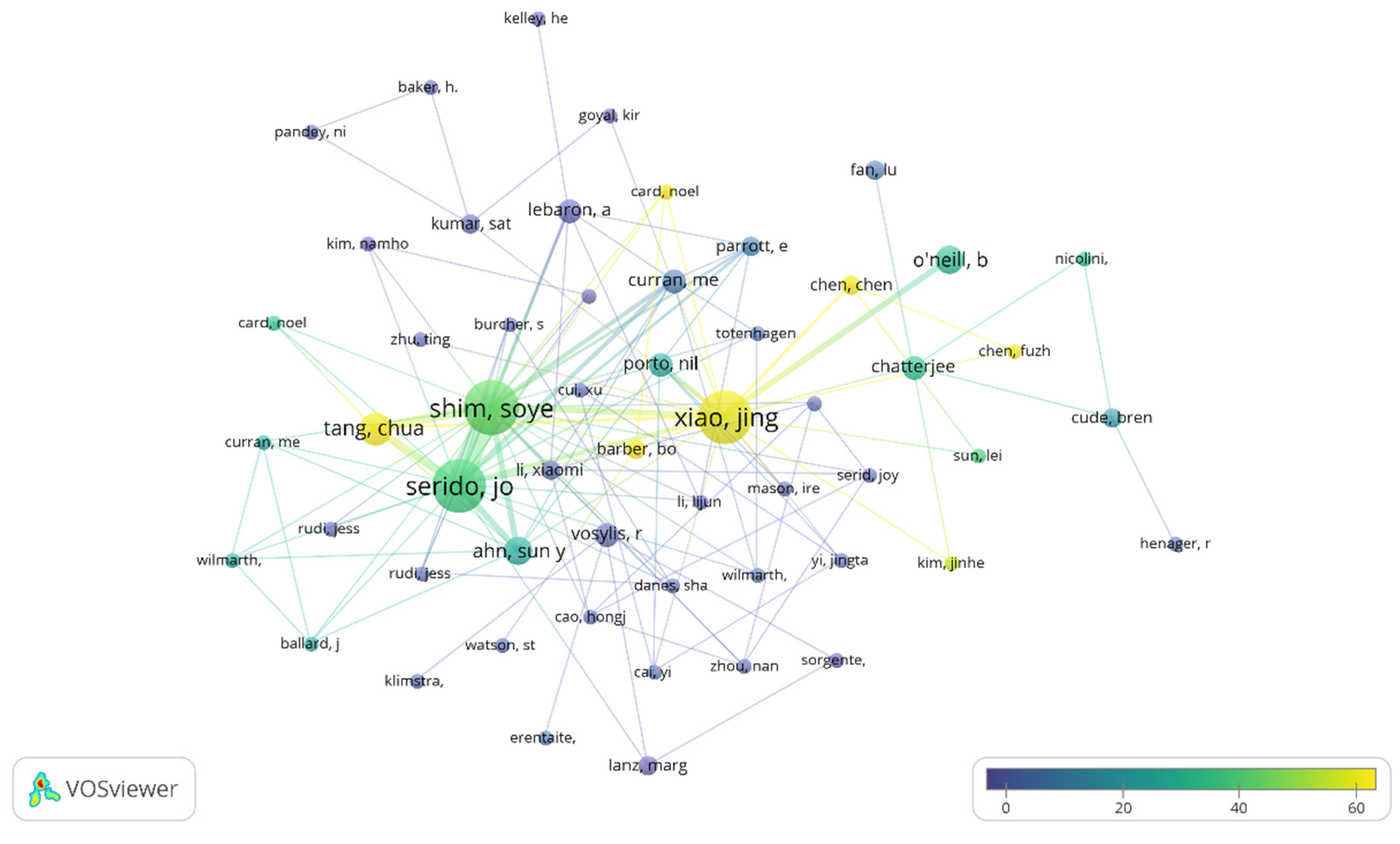

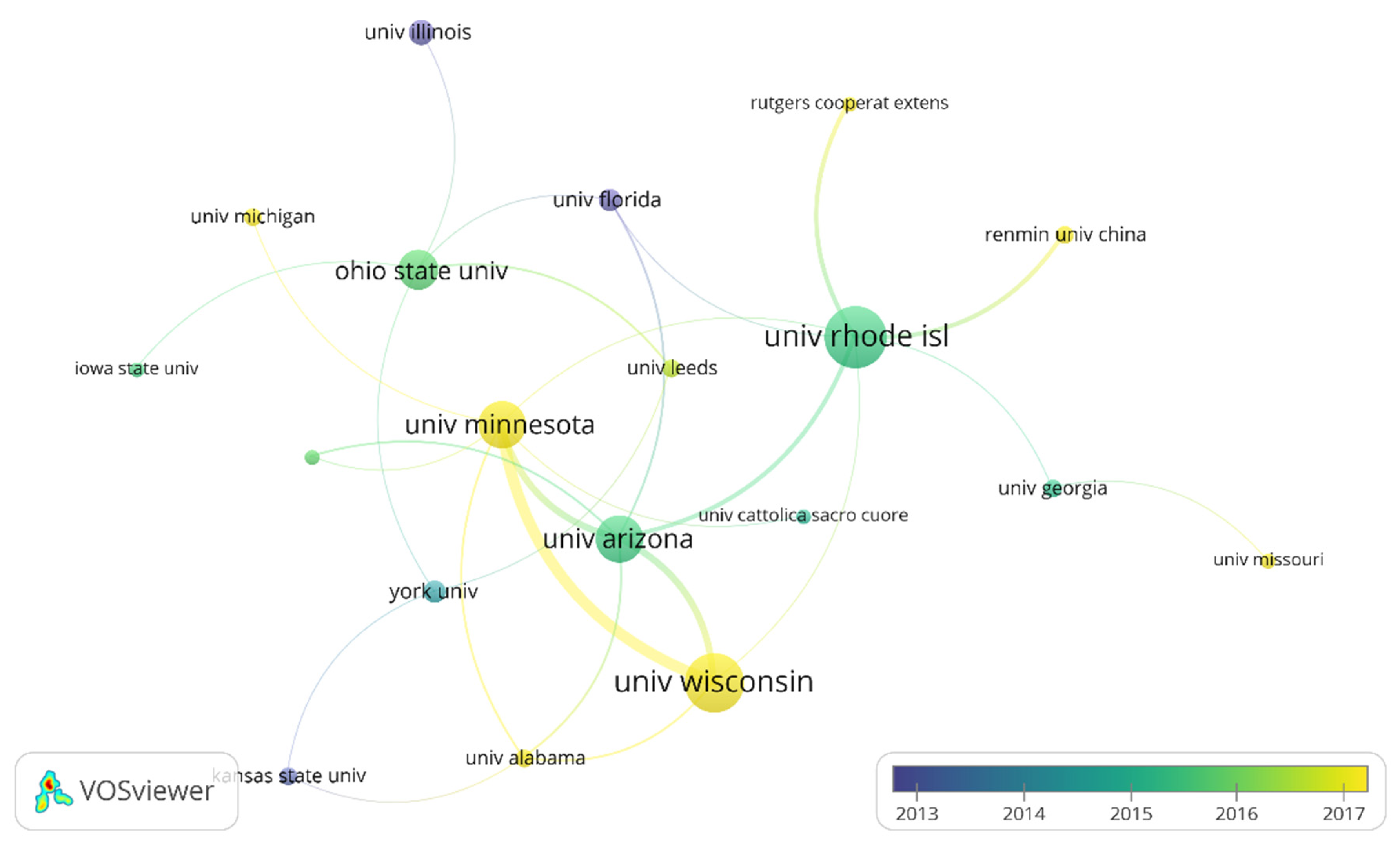

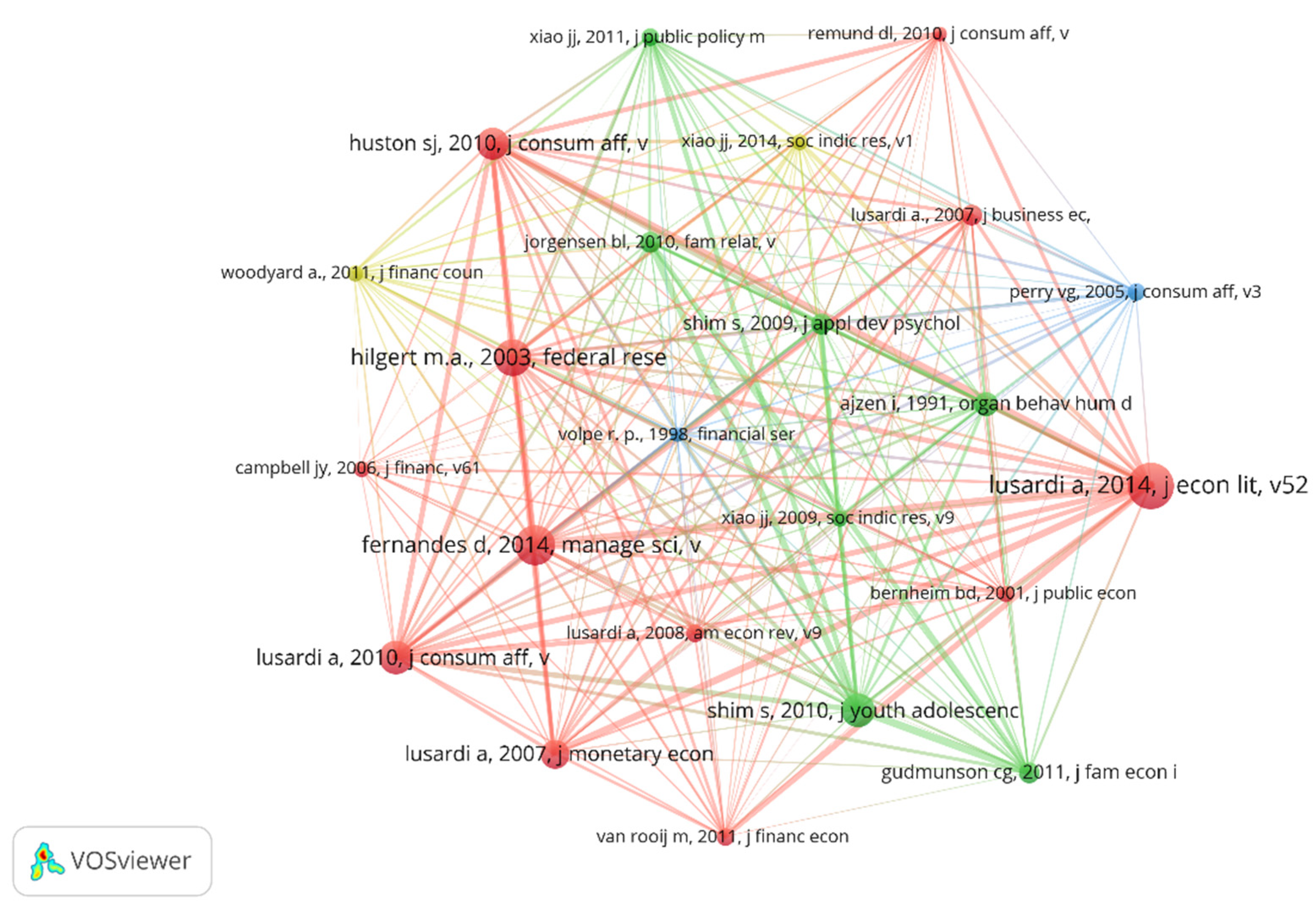

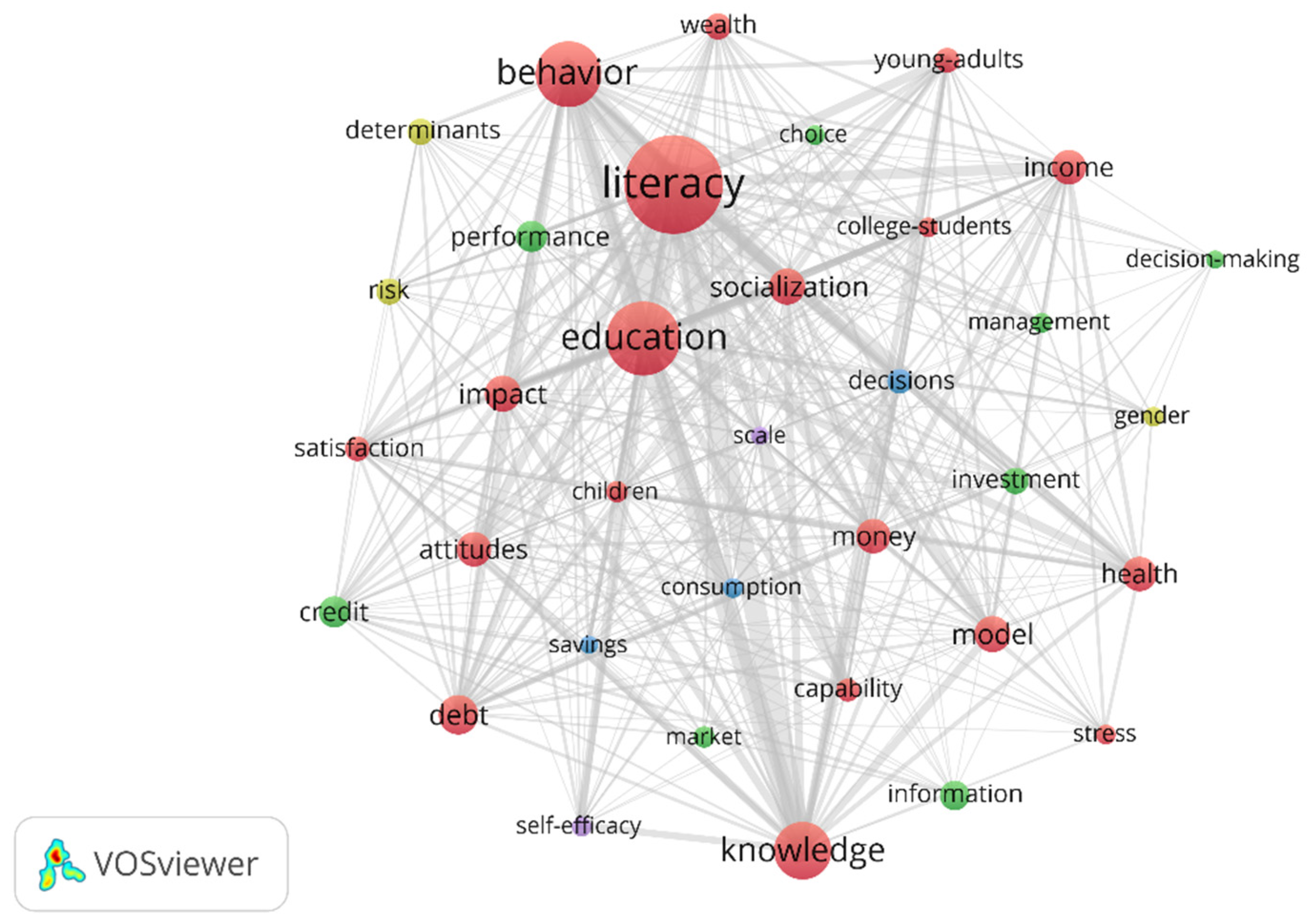

3. Results

4. Discussion

5. Conclusions

Supplementary Materials

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- McCaffery, E.J.; Baron, J. The Humpty Dumpty blues: Disaggregation bias in the evaluation of tax systems. Organ. Behav. Hum. Decis. Process. 2003, 91, 230–242. [Google Scholar] [CrossRef]

- Alsemgeest, L. Arguments for and against financial literacy education: Where to go from here? Int. J. Consum. Stud. 2015, 39, 155–161. [Google Scholar] [CrossRef]

- Raut, R.K. Past behaviour, financial literacy and investment decision-making process of individual investors. Int. J. Emerg. Mark. 2020, 15, 1243–1263. [Google Scholar] [CrossRef]

- Sahi, S.K. Psychological biases of individual investors and financial satisfaction. J. Consum. Behav. 2017, 16, 511–535. [Google Scholar] [CrossRef]

- Graziano, P.A.; Slavec, J.; Paneto, A.; McNamara, J.P.; Geffken, G.R.; Reid, A. ADHD Symptomatology and Risky Health, Driving, and Financial Behaviors in College: The Mediating Role of Sensation Seeking and Effortful Control. J. Atten. Disord. 2014, 19, 179–190. [Google Scholar] [CrossRef] [PubMed]

- Aydemir, S.D.; Aren, S. Do the effects of individual factors on financial risk-taking behavior diversify with financial literacy? Kybernetes 2017, 46, 1706–1734. [Google Scholar] [CrossRef]

- Abrantes-Braga, F.D.M.; Veludo-De-Oliveira, T. Help me, I can’t afford it! Antecedents and consequence of risky indebtedness behaviour. Eur. J. Mark. 2020, 54, 2223–2244. [Google Scholar] [CrossRef]

- Ranta, M.; Salmela-Aro, K. Subjective financial situation and financial capability of young adults in Finland. Int. J. Behav. Dev. 2017, 42, 525–534. [Google Scholar] [CrossRef]

- Santini, F.D.O.; Ladeira, W.J.; Mette, F.M.B.; Ponchio, M.C. The antecedents and consequences of financial literacy: A meta-analysis. Int. J. Bank Mark. 2019, 37, 1462–1479. [Google Scholar] [CrossRef]

- Fan, L. A Conceptual Framework of Financial Advice-Seeking and Short- and Long-Term Financial Behaviors: An Age Comparison. J. Fam. Econ. Issues 2020, 42, 90–112. [Google Scholar] [CrossRef]

- Bapat, D.M. Segmenting young adults based on financial management behavior in India. Int. J. Bank Mark. 2019, 38, 548–560. [Google Scholar] [CrossRef]

- Cronqvist, H.; Makhija, A.K.; Yonker, S.E. Behavioral consistency in corporate finance: CEO personal and corporate leverage. J. Financ. Econ. 2012, 103, 20–40. [Google Scholar] [CrossRef]

- Sivaramakrishnan, S.; Srivastava, M.; Rastogi, A. Attitudinal factors, financial literacy, and stock market participation. Int. J. Bank Mark. 2017, 35, 818–841. [Google Scholar] [CrossRef]

- Wu, J.; Guo, S.; Huang, H.; Liu, W.; Xiang, Y. Information and Communications Technologies for Sustainable Development Goals: State-of-the-Art, Needs and Perspectives. IEEE Commun. Surv. Tutor. 2018, 20, 2389–2406. [Google Scholar] [CrossRef] [Green Version]

- Zhu, A.Y.F.; Chou, K.L. Financial Literacy among Hong Kong’s Chinese Adolescents Testing the Validity of a Scale and Evaluating Two Conceptual Models. Youth Soc. 2018, 52, 548–573. [Google Scholar] [CrossRef]

- Swiecka, B.; Yeşildağ, E.; Özen, E.; Grima, S. Financial Literacy: The Case of Poland. Sustainability 2020, 12, 700. [Google Scholar] [CrossRef] [Green Version]

- Fernandes, D.; Lynch, J.; Netemeyer, R.G. Financial Literacy, Financial Education, and Downstream Financial Behaviors. Manag. Sci. 2014, 60, 1861–1883. [Google Scholar] [CrossRef]

- Puri, M.; Robinson, D.T. Optimism and economic choice. J. Financ. Econ. 2007, 86, 71–99. [Google Scholar] [CrossRef] [Green Version]

- Hira, T.K. Promoting sustainable financial behaviour: Implications for education and research: Promoting sustainable financial behaviour. Int. J. Consum. Stud. 2012, 36, 502–507. [Google Scholar] [CrossRef]

- Zahera, S.A.; Bansal, R. Do investors exhibit behavioral biases in investment decision making? A systematic review. Qual. Res. Financ. Mark. 2018, 10, 210–251. [Google Scholar] [CrossRef]

- Sanfey, A.G.; Loewenstein, G.; McClure, S.M.; Cohen, J.D. Neuroeconomics: Cross-currents in research on decision-making. Trends Cogn. Sci. 2006, 10, 108–116. [Google Scholar] [CrossRef]

- Aydin, A.E.; Selcuk, E.A. An investigation of financial literacy, money ethics and time preferences among college students—A structural equation model. Int. J. Bank Mark. 2019, 37, 880–900. [Google Scholar] [CrossRef]

- De Beckker, K.; De Witte, K.; Van Campenhout, G. Identifying financially illiterate groups: An international comparison. Int. J. Consum. Stud. 2019, 43, 490–501. [Google Scholar] [CrossRef]

- Brüggen, E.C.; Hogreve, J.; Holmlund, M.; Kabadayi, S.; Löfgren, M. Financial well-being: A conceptualization and research agenda. J. Bus. Res. 2017, 79, 228–237. [Google Scholar] [CrossRef]

- Hanson, T.A.; Olson, P.M. Financial literacy and family communication patterns. J. Behav. Exp. Financ. 2018, 19, 64–71. [Google Scholar] [CrossRef]

- Arnett, J.J. Are college students adults? Their conceptions of the transition to adulthood. J. Adult Dev. 1994, 1, 213–224. [Google Scholar] [CrossRef]

- Feng, X.; Lu, B.; Song, X.; Ma, S. Financial literacy and household finances: A Bayesian two-part latent variable modeling approach. J. Empir. Financ. 2019, 51, 119–137. [Google Scholar] [CrossRef]

- Behrman, J.R.; Mitchell, O.S.; Soo, C.K.; Bravo, D. How Financial Literacy Affects Household Wealth Accumulation. Am. Econ. Rev. 2012, 102, 300–304. [Google Scholar] [CrossRef] [Green Version]

- Lusardi, A.; Mitchell, O.S. The Economic Importance of Financial Literacy: Theory and Evidence. J. Econ. Lit. 2014, 52, 5–44. [Google Scholar] [CrossRef] [Green Version]

- Deuflhard, F.; Georgarakos, D.; Inderst, R. Financial Literacy and Savings Account Returns. J. Eur. Econ. Assoc. 2018, 17, 131–164. [Google Scholar] [CrossRef] [Green Version]

- Lusardi, A.; Samek, A.; Kapteyn, A.; Glinert, L.; Hung, A.; Heinberg, A. Visual tools and narratives: New ways to improve financial literacy. J. Pension Econ. Financ. 2017, 16, 297–323. [Google Scholar] [CrossRef] [Green Version]

- Duca, J.V.; Kumar, A. Financial literacy and mortgage equity withdrawals. J. Urban Econ. 2014, 80, 62–75. [Google Scholar] [CrossRef] [Green Version]

- Huang, J.; Nam, Y.; Sherraden, M.S. Financial Knowledge and Child Development Account Policy: A Test of Financial Capability. J. Consum. Aff. 2013, 47, 1–26. [Google Scholar] [CrossRef] [Green Version]

- Morgan, P.J.; Long, T.Q. Financial literacy, financial inclusion, and savings behavior in Laos. J. Asian Econ. 2020, 68, 101197. [Google Scholar] [CrossRef]

- Bapat, D. Antecedents to responsible financial management behavior among young adults: Moderating role of financial risk tolerance. Int. J. Bank Mark. 2020, 38, 1177–1194. [Google Scholar] [CrossRef]

- Xiao, J.J.; Tang, C.; Shim, S. Acting for Happiness: Financial Behavior and Life Satisfaction of College Students. Soc. Indic. Res. 2009, 92, 53–68. [Google Scholar] [CrossRef]

- Tang, N.; Baker, A. Self-esteem, financial knowledge and financial behavior. J. Econ. Psychol. 2016, 54, 164–176. [Google Scholar] [CrossRef]

- Xiao, J.J.; Chen, C.; Chen, F. Consumer Financial Capability and Financial Satisfaction. Soc. Indic. Res. 2014, 118, 415–432. [Google Scholar] [CrossRef]

- Xiao, J.J.; Ahn, S.Y.; Serido, J.; Shim, S. Earlier financial literacy and later financial behaviour of college students. Int. J. Consum. Stud. 2014, 38, 593–601. [Google Scholar] [CrossRef]

- Kim, K.T.; Anderson, S.G.; Seay, M.C. Financial Knowledge and Short-Term and Long-Term Financial Behaviors of Millennials in the United States. J. Fam. Econ. Issues 2019, 40, 194–208. [Google Scholar] [CrossRef]

- Serido, J.; Shim, S.; Tang, C. A developmental model of financial capability: A framework for promoting a successful transition to adulthood. Int. J. Behav. Dev. 2013, 37, 287–297. [Google Scholar] [CrossRef]

- Xiao, J.J.; Porto, N.; Mason, A.I.M. Financial capability of student loan holders who are college students, graduates, or dropouts. J. Consum. Aff. 2020, 54, 1383–1401. [Google Scholar] [CrossRef]

- Riitsalu, L.; Murakas, R. Subjective financial knowledge, prudent behaviour and income: The predictors of financial well-being in Estonia. Int. J. Bank Mark. 2019, 37, 934–950. [Google Scholar] [CrossRef]

- Johan, I.; Rowlingson, K.; Appleyard, L. The Effect of Personal Finance Education on The Financial Knowledge, Attitudes and Behaviour of University Students in Indonesia. J. Fam. Econ. Issues 2021, 42, 351–367. [Google Scholar] [CrossRef]

- Henager, R.; Cude, B.J. Financial Literacy of High School Graduates: Long- and Short-Term Financial Behavior by Age Group. J. Fam. Econ. Issues 2019, 40, 564–575. [Google Scholar] [CrossRef]

- Reyers, M. Financial capability and emergency savings among South Africans living above and below the poverty line. Int. J. Consum. Stud. 2019, 43, 335–347. [Google Scholar] [CrossRef]

- Xiao, J.J.; Chatterjee, S.; Kim, J. Factors associated with financial independence of young adults. Int. J. Consum. Stud. 2014, 38, 394–403. [Google Scholar] [CrossRef]

- Montalto, C.P.; Phillips, E.L.; McDaniel, A.; Baker, A.R. College Student Financial Wellness: Student Loans and Beyond. J. Fam. Econ. Issues 2018, 40, 3–21. [Google Scholar] [CrossRef]

- Xiao, J.J.; O’Neill, B. Consumer financial education and financial capability. Int. J. Consum. Stud. 2016, 40, 712–721. [Google Scholar] [CrossRef] [Green Version]

- Ouachani, S.; Belhassine, O.; Kammoun, A. Measuring financial literacy: A literature review. Manag. Financ. 2020, 47, 266–281. [Google Scholar] [CrossRef]

- Xiao, J.J.; O’Neill, B. Propensity to plan, financial capability, and financial satisfaction. Int. J. Consum. Stud. 2018, 42, 501–512. [Google Scholar] [CrossRef] [Green Version]

- Cui, X.; Xiao, J.J.; Yi, J.; Porto, N.; Cai, Y. Impact of family income in early life on the financial independence of young adults: Evidence from a matched panel data. Int. J. Consum. Stud. 2019, 43, 514–527. [Google Scholar] [CrossRef]

- Acedo-Ramirez, M.A.; Ayala-Calvo, J.C.; Navarrete-Martinez, E. Determinants of Capital Structure: Family Businesses versus Non-Family Firms. Financ. Uver Czech J. Econ. Financ. 2017, 67, 80–103. [Google Scholar]

- Walczak, D.; Pieńkowska-Kamieniecka, S. Gender differences in financial behaviours. Eng. Econ. 2018, 29, 123–132. [Google Scholar] [CrossRef] [Green Version]

- Moore, D.L. Survey of Financial Literacy in Washington State: Knowledge, Behavior, Attitudes, and Experiences; Washington State Department of Financial Institutions: Washington, DC, USA, 2003. [Google Scholar] [CrossRef]

- Potocki, T.; Cierpiał-Wolan, M. Factors shaping the financial capability of low-income consumers from rural regions of Poland. Int. J. Consum. Stud. 2018, 43, 187–198. [Google Scholar] [CrossRef]

- Norvilitis, J.; Szablicki, P.B.; Wilson, S.D. Factors Influencing Levels of Credit-Card Debt in College Students1. J. Appl. Soc. Psychol. 2003, 33, 935–947. [Google Scholar] [CrossRef]

- Kawamura, T.; Mori, T.; Motonishi, T.; Ogawa, K. Is Financial Literacy Dangerous? Financial Literacy, Behavioral Factors, and Financial Choices of Households. J. Jpn. Int. Econ. 2021, 60, 101131. [Google Scholar] [CrossRef]

- Shkvarchuk, L.; Slav’yuk, R. The Financial Behavior of Households in Ukraine. J. Competitiveness 2019, 11, 144–159. [Google Scholar] [CrossRef]

- Białowolski, P.; Chávez-Juárez, F. Household Financial Portfolios in an Emerging Economy—The Case of Chile. Emerg. Mark. Financ. Trade 2021, 57, 1811–1827. [Google Scholar] [CrossRef]

- Steinert, J.; Cluver, L.D.; Meinck, F.; Doubt, J.; Vollmer, S. Household economic strengthening through financial and psychosocial programming: Evidence from a field experiment in South Africa. J. Dev. Econ. 2018, 134, 443–466. [Google Scholar] [CrossRef]

- Kreiner, C.T.; Leth-Petersen, S.; Willerslev-Olsen, L.C. Financial Trouble Across Generations: Evidence from the Universe of Personal Loans in Denmark. Econ. J. 2019, 130, 233–262. [Google Scholar] [CrossRef] [Green Version]

- Kłopocka, A.M. Does Consumer Confidence Forecast Household Saving and Borrowing Behavior? Evidence for Poland. Soc. Indic. Res. 2016, 133, 693–717. [Google Scholar] [CrossRef] [Green Version]

- Clark, G.L. The Significance of Financial Competence and Risk Tolerance in Home-Related Expenditure by Jurisdiction and Regime. Zeitschrift für Wirtschaftsgeographie 2021, 65, 12–27. [Google Scholar] [CrossRef]

- Sirgy, M.J. The Psychology of Material Well-Being. Appl. Res. Qual. Life 2018, 13, 273–301. [Google Scholar] [CrossRef]

- Vega-Muñoz, A.; Arjona-Fuentes, J.M. Social networks and graph theory in the search for distant knowledge in the field of industrial engineering. In Handbook of Research on Advanced Applications of Graph Theory in Modern Society; Pal, M., Samanta, S., Pal, A., Eds.; IGI-Global: Hershey, PA, USA, 2020; Volume 17, pp. 397–418. [Google Scholar] [CrossRef]

- Aleixandre-Tudó, J.L.; Castelló-Cogollos, L.; Aleixandre, J.L.; Aleixandre-Benavent, R. Trends in funding research and international collaboration on greenhouse gas emissions: A bibliometric approach. Environ. Sci. Pollut. Res. 2021, 28, 32330–32346. [Google Scholar] [CrossRef] [PubMed]

- Corbet, S.; Dowling, M.; Gao, X.; Huang, S.; Lucey, B.; Vigne, S.A. An analysis of the intellectual structure of research on the financial economics of precious metals. Resour. Policy 2019, 63, 101416. [Google Scholar] [CrossRef]

- De Filippo, D.; Serrano-López, A.E. From academia to citizenry. Study of the flow of scientific information from projects to scientific journals and social media in the field of “Energy saving”. J. Clean. Prod. 2018, 199, 248–256. [Google Scholar] [CrossRef]

- Erkens, M.; Paugam, L.; Stolowy, H. Non-financial information: State of the art and research perspectives based on a bibliometric study. Comptabilité Contrôle Audit 2015, 21, 15–92. [Google Scholar] [CrossRef] [Green Version]

- Ferramosca, S.; Verona, R. Framing the evolution of corporate social responsibility as a discipline (1973–2018): A large-scale scientometric analysis. Corp. Soc. Responsib. Environ. Manag. 2020, 27, 178–203. [Google Scholar] [CrossRef]

- Clarivate Web of Science. Available online: https://0-www-webofknowledge-com.brum.beds.ac.uk/ (accessed on 26 August 2020).

- Frenken, K.; Hardeman, S.; Hoekman, J. Spatial scientometrics: Towards a cumulative research program. J. Inf. 2009, 3, 222–232. [Google Scholar] [CrossRef] [Green Version]

- Gureev, V.N.; Mazov, N.A. Themes of the publications of an organization as a basis for forming an objective and optimal repertoire of scientific periodicals. Sci. Tech. Inf. Process. 2013, 40, 195–204. [Google Scholar] [CrossRef]

- Karakose, T.; Demirkol, M. Exploring the emerging COVID-19 research trends and current status in the field of education: A bibliometric analysis and knowledge mapping. Educ. Process Int. J. 2021, 10, 7–27. [Google Scholar] [CrossRef]

- Hache, E.; Palle, A. Renewable energy source integration into power networks, research trends and policy implications: A bibliometric and research actors survey analysis. Energy Policy 2019, 124, 23–35. [Google Scholar] [CrossRef]

- Klingelhöfer, D.; Braun, M.; Brüggmann, D.; Groneberg, D.A. Glyphosate: How do ongoing controversies, market characteristics, and funding influence the global research landscape? Sci. Total Environ. 2021, 765, 144271. [Google Scholar] [CrossRef] [PubMed]

- Köseoglu, M.A.; Okumus, F.; Putra, E.D.; Yildiz, M.; Dogan, I.C. Authorship Trends, Collaboration Patterns, and Co-Authorship Networks in Lodging Studies (1990–2016). J. Hosp. Mark. Manag. 2018, 27, 561–582. [Google Scholar] [CrossRef]

- Linnenluecke, M.K.; Marrone, M.; Singh, A.K. Sixty years of Accounting & Finance: A bibliometric analysis of major research themes and contributions. Account. Financ. 2020, 60, 3217–3251. [Google Scholar] [CrossRef]

- Lojo, A.; Li, M.; Cànoves, G. Co-authorship Networks and Thematic Development in Chinese Outbound Tourism Research. J. China Tour. Res. 2019, 15, 295–319. [Google Scholar] [CrossRef]

- Luo, J.; Han, H.; Jia, F.; Dong, H. Agricultural Co-operatives in the western world: A bibliometric analysis. J. Clean. Prod. 2020, 273, 122945. [Google Scholar] [CrossRef]

- Meseguer-Sánchez, V.; Abad-Segura, E.; Belmonte-Ureña, L.J.; Molina-Moreno, V. Examining the Research Evolution on the Socio-Economic and Environmental Dimensions on University Social Responsibility. Int. J. Environ. Res. Public Health 2020, 17, 4729. [Google Scholar] [CrossRef] [PubMed]

- Moya, S.; Prior, D. Who publish in Spanish accounting jornals? A bibliometric analysis 1996–2005. Rev. Esp. Financ. Contab. 2008, 37, 353–374. [Google Scholar]

- Nazaripour, M.; Reshadi, M.A.M.; Mirbagheri, S.A.; Nazaripour, M.; Bazargan, A. Research trends of heavy metal removal from aqueous environments. J. Environ. Manag. 2021, 287, 112322. [Google Scholar] [CrossRef]

- Centobelli, P.; Cerchione, R.; Mittal, A. Managing sustainability in luxury industry to pursue circular economy strategies. Bus. Strat. Environ. 2021, 30, 432–462. [Google Scholar] [CrossRef]

- Shelton, R.D. Scientometric laws connecting publication counts to national research funding. Scientometrics 2020, 123, 181–206. [Google Scholar] [CrossRef]

- Uribe-Toril, J.; Ruiz-Real, J.L.; Haba-Osca, J.; Valenciano, J.D.P. Forests’ First Decade: A Bibliometric Analysis Overview. Forests 2019, 10, 72. [Google Scholar] [CrossRef] [Green Version]

- Zhang, D.; Zhang, Z.; Managi, S. A bibliometric analysis on green finance: Current status, development, and future directions. Financ. Res. Lett. 2019, 29, 425–430. [Google Scholar] [CrossRef]

- Dobrov, G.M.; Randolph, R.H.; Rauch, W.D. New options for team research via international computer networks. Scientometrics 1979, 1, 387–404. [Google Scholar] [CrossRef]

- Price, D.D.S. A general theory of bibliometric and other cumulative advantage processes. J. Am. Soc. Inf. Sci. 1976, 27, 292–306. [Google Scholar] [CrossRef] [Green Version]

- Bulick, S. Book Use as a Bradford-Zipf Phenomenon. Coll. Res. Libr. 1978, 39, 215–219. [Google Scholar] [CrossRef]

- Morse, P.M.; Leimkuhler, F.F. Technical Note—Exact Solution for the Bradford Distribution and Its Use in Modeling Informational Data. Oper. Res. 1979, 27, 187–198. [Google Scholar] [CrossRef] [Green Version]

- Pontigo, J.; Lancaster, F.W. Qualitative aspects of the Bradford distribution. Scientometrics 1986, 9, 59–70. [Google Scholar] [CrossRef]

- Kumar, S. Application of Bradford’s Law to Human-Computer Interaction Research Literature. DESIDOC J. Libr. Inf. Technol. 2014, 34, 232–240. [Google Scholar] [CrossRef]

- Swokowski, E.W. Calculus with Analytic Geometry, 4th ed.; Grupo Editorial Planeta: Mexico City, Mexico, 1988; p. 547. [Google Scholar]

- Lotka, A.J. The frequency distribution of scientific productivity. J. Wash. Acad. Sci. 1926, 16, 317–321. [Google Scholar]

- Hirsch, J.E. An index to quantify an individual’s scientific research output. Proc. Natl. Acad. Sci. USA 2005, 102, 16569–16572. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Crespo, N.; Simoes, N. Publication Performance Through the Lens of the h-index: How Can We Solve the Problem of the Ties? Soc. Sci. Q. 2019, 100, 2495–2506. [Google Scholar] [CrossRef]

- Zipf, G.K. Selected Studies of the Principle of Relative Frequency in Language; Harvard University Press: Cambridge, MA, USA, 1932. [Google Scholar]

- Mikhaylov, A.; Mikhaylova, A.; Hvaley, D. Knowledge Hubs of Russia: Bibliometric Mapping of Research Activity. J. Sci. Res. 2020, 9, 1–10. [Google Scholar] [CrossRef]

- Moravcsik, M.J. Applied scientometrics: An assessment methodology for developing countries. Scientometrics 1985, 7, 165–176. [Google Scholar] [CrossRef]

- Zhang, D.; Xu, J.; Zhang, Y.; Wang, J.; He, S.; Zhou, X. Study on sustainable urbanization literature based on Web of Science, scopus, and China national knowledge infrastructure: A scientometric analysis in CiteSpace. J. Clean. Prod. 2020, 264, 121537. [Google Scholar] [CrossRef]

- Nájera-Sánchez, J.J. A Systematic Review of Sustainable Banking through a Co-Word Analysis. Sustainability 2019, 12, 278. [Google Scholar] [CrossRef] [Green Version]

- Vega-Muñoz, A.; Fuentes, J.M.A.; Ariza-Montes, A.; Han, H.; Law, R. In search of ‘a research front’ in cruise tourism studies. Int. J. Hosp. Manag. 2020, 85, 102353. [Google Scholar] [CrossRef]

- Abarcar, P.; Barua, R.; Yang, D. Financial Education and Financial Access for Transnational Households: Field Experimental Evidence from the Philippines. Econ. Dev. Cult. Chang. 2020, 69, 373–404. [Google Scholar] [CrossRef]

- Kirbiš, I.Š.; Vehovec, M.; Galić, Z. Relationship between Financial Satisfaction and Financial Literacy: Exploring Gender Differences. Drustvena Istraz. 2017, 26, 165–185. [Google Scholar] [CrossRef] [Green Version]

- Marginson, S. What drives global science? The four competing narratives. Stud. High. Educ. 2021, 1–19. [Google Scholar] [CrossRef]

- Gendron, Y.; Rodrigue, M. On the centrality of peripheral research and the dangers of tight boundary gatekeeping. Crit. Perspect. Account. 2021, 76, 102076. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Source Title | Total, in Articles | WoS Categories | Journal Impact Factor (JIF) | Best JIF Quartile |

|---|---|---|---|---|

| Journal of Family and Economic Issues | 24 | Economics; Family Studies | Not Available | Not Available |

| Journal of Consumer Affairs | 23 | Business; Economics | 2.131 | Q2 |

| International Journal of Consumer Studies | 21 | Business | 3.864 | Q3 |

| International Journal of Bank Marketing | 16 | Business | 4.412 | Q2 |

| Journal of Economic Psychology | 11 | Economics; Psychology, Multidisciplinary | 2.037 | Q2 |

| Emerging Adulthood | 8 | Family Studies; Psychology, Developmental; Psychology, Social | 1.560 | Q4 |

| Journal of Behavioral and Experimental Economics | 7 | Economics | 1.382 | Q3 |

| Frontiers in Psychology | 7 | Psychology, Multidisciplinary | 2.988 | Q2 |

| European Journal of Finance | 6 | Business, Finance | 1.809 | Q3 |

| Sustainability | 6 | Environmental Studies; Environmental Sciences; Green & Sustainable Science & Technology | 3.251 | Q2 |

| Journal of Behavioral Finance | 6 | Business, Finance; Economics | 0.314 | Q3 |

| Social Indicators Research | 6 | Social Sciences, Interdisciplinary; Sociology | 2.614 | Q2 |

| Total, Articles = | 141 | Q2 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

López-Medina, T.; Mendoza-Ávila, I.; Contreras-Barraza, N.; Salazar-Sepúlveda, G.; Vega-Muñoz, A. Bibliometric Mapping of Research Trends on Financial Behavior for Sustainability. Sustainability 2022, 14, 117. https://0-doi-org.brum.beds.ac.uk/10.3390/su14010117

López-Medina T, Mendoza-Ávila I, Contreras-Barraza N, Salazar-Sepúlveda G, Vega-Muñoz A. Bibliometric Mapping of Research Trends on Financial Behavior for Sustainability. Sustainability. 2022; 14(1):117. https://0-doi-org.brum.beds.ac.uk/10.3390/su14010117

Chicago/Turabian StyleLópez-Medina, Tania, Isabel Mendoza-Ávila, Nicolás Contreras-Barraza, Guido Salazar-Sepúlveda, and Alejandro Vega-Muñoz. 2022. "Bibliometric Mapping of Research Trends on Financial Behavior for Sustainability" Sustainability 14, no. 1: 117. https://0-doi-org.brum.beds.ac.uk/10.3390/su14010117