Identifying Strategic Factors of the Implantation CSR in the Airline Industry: The Case of Asia-Pacific Airlines

Abstract

:1. Introduction

2. Literature Review

2.1. Definition of Corporate Social Responsibility (CSR)

2.2. CSR in the Airline Industry

3. CSR Issues of the Airline Industry

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Dimension | Criteria | Definition | Source | |

|---|---|---|---|---|

| Economic Dimension | EC1 | Corporate Governance | Board structure, responsibilities and committees, corporate governance policy, board diversity, board effectiveness, audit conflict of interest, and transparency of senior management remuneration | Dow Jones Sustainability Indices (DJSI), Global Reporting Initiative (GRI) |

| EC2 | Risk and Crisis Management | Analysis of risks, risk correlation, sensitivity analysis and stress testing, risk response strategy, and crisis preparedness | DJSI, GRI | |

| EC3 | Codes of Conduct/Compliance/Corruption and Bribery | Focus issues, scope of policy, systems/procedures, business relationships, and reporting on breaches | DJSI, GRI G4 (Society) | |

| EC4 | Antitrust Policy | Antitrust policy, coverage of antitrust policy, antitrust compliance, and reporting process etc. | DJSI, GRI G4 (Society) | |

| EC5 | Customer Relationship Management | Satisfaction measurement, customer feedback process, availability of data to the customer center, analysis of customer value, and complaints management | DJSI | |

| EC6 | Brand Management | Brand-related expenses, branding strategies, brand metrics used, and stakeholder perception analysis | DJSI, GRI G4 (Market Presence) | |

| EC7 | Supply Chain Management | Awareness, risk analysis, risk management measures, supply chain management strategy, and transparency | DJSI, GRI G4 (Procurement Practices) | |

| EC8 | Efficiency * | Passenger load factor and share of short-haul flights | DJSI | |

| EC9 | Fleet Management * | Fleet age, measures for improving fuel efficiency | DJSI | |

| EC10 | Reliability * | Arrival delay indicators and management approach | DJSI | |

| Environmental Dimension | EN1 | Climate Change | Direct GHG emissions, indirect GHG emissions, and energy consumption | DJSI, Carbon Disclosure Project (CDP), GRI, International Civil Aviation Organization (ICAO), International Air Transport Association (IATA) |

| EN2 | Biofuel */Alternative Energy | Biofuel usage volume, research program participation, and ground alternative energy usage | DJSI, CDP, GRI, ICAO, IATA | |

| EN3 | Noise * | Noise management approach and reduction of project and investment | ICAO, IATA | |

| EN4 | Environmental Policy/Management System | Coverage of corporate requirements/guidelines, centralized data collection system, environmental management system (EMS) is verified/audited/certified | DJSI, UN GC, GRI G3.1; G4 | |

| EN5 | Operational Eco-Efficiency | Water usage, waste generation, NOx emissions, and SOx emissions | DJSI, CDP, GRI, ICAO, IATA | |

| Social Dimension | SO1 | Environment and Social Reporting (Information Disclosure) | Quality of social and environment reporting, materiality, coverage, assurance, and quantitative data | DJSI |

| SO2 | Labor Practice Indicators and Human Rights | ILO- and UNGC-related indicators, human rights, labor practices, and decent work | DJSI, GRI G4 (Human Rights, Labor Practices, and Decent Work), ILO, UNGC | |

| SO3 | Human Capital Development | Skill mapping and developing process, human capital performance, and learning and development process | DJSI, GRI G4 (Labor Practices and Decent Work) | |

| SO4 | Talent Attraction and Retention | Salary structure, employee turnover rate, and employee satisfaction | DJSI, GRI G4 (Labor Practices and Decent Work) | |

| SO5 | Corporate Citizenship and Philanthropy | Group-wide strategy, performance management process, and KPI | DJSI, GRI G4 (Society ) | |

| SO6 | Stakeholder Engagement | Stakeholder engagement approach, materiality analysis process, and feedback approach | DJSI, GRI | |

| SO7 | Product Responsibility (Safety) | Safety management approach, training system, management process, and audit and safety performance | GRI, ICAO, IATA | |

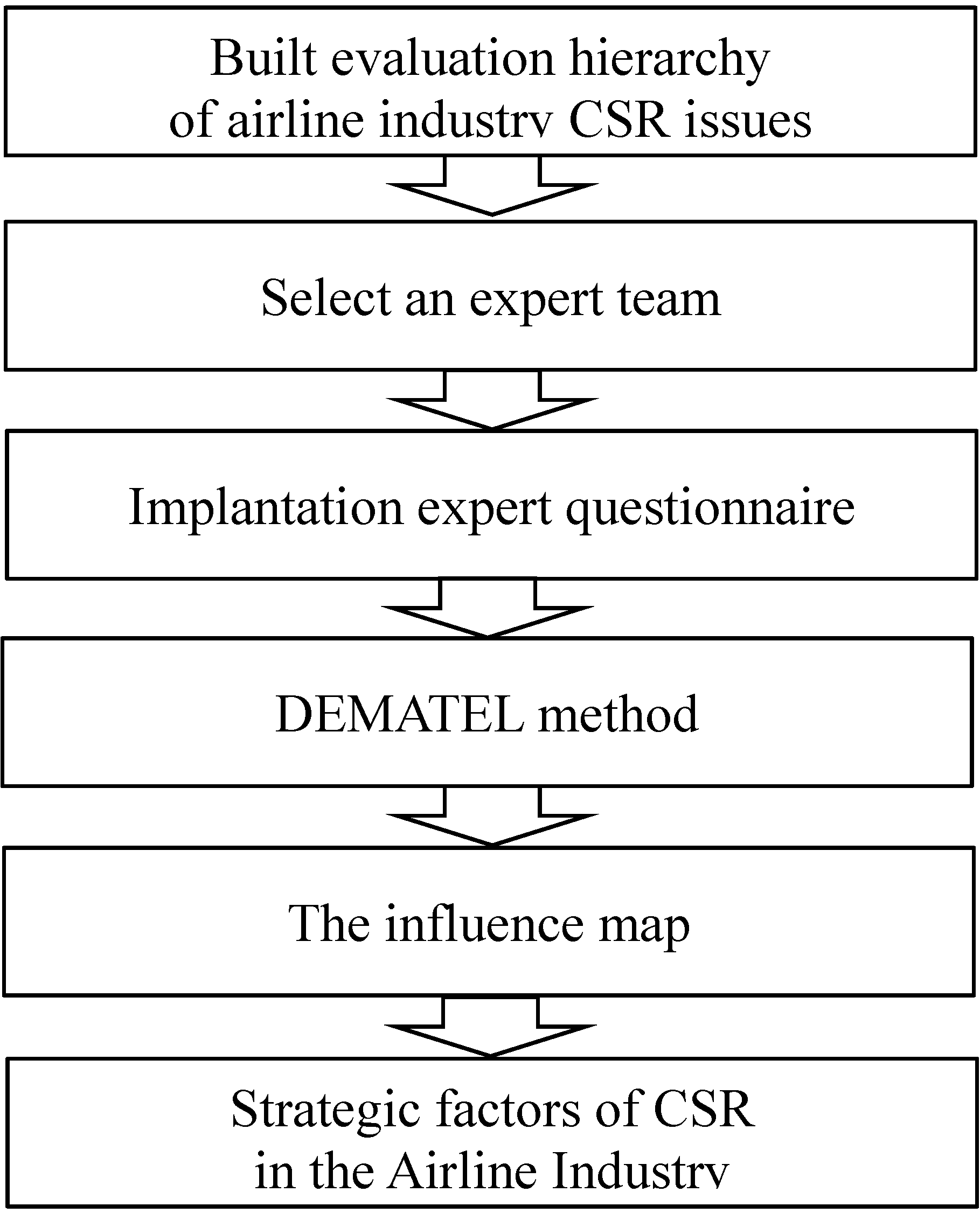

4. Research Method

| Background | Background | Male/Female | Professional Experience | |

|---|---|---|---|---|

| Expert #1 | Global airlines CSR manager | Male | Over 10 years’ airline management experience, responsible for environment division and corporate safety office | |

| Expert #2 | Global airlines CSR project manager | Female | 10 years’ airline experience and now is executive secretary of airline’s CSR committee | |

| Expert #3 | Taiwan civil aeronautics administration (CAA) | Male | Over 10 years’ CAA experience, now responsible for environmental management | |

| Expert #4 | Global airlines CSR manager | Male | Over 10 years’ airline management experience of environmental division | |

| Expert #5 | Professor of air transportation management department | Female | Over 20 journal article publications in airline operation and management field | |

| Expert #6 | Global airlines CSR project manager | Female | 3 years’ airline experience and over 5 years’ CSR project management experience. Responsible for publishing CSR report for airlines. | |

5. Results and Discussion

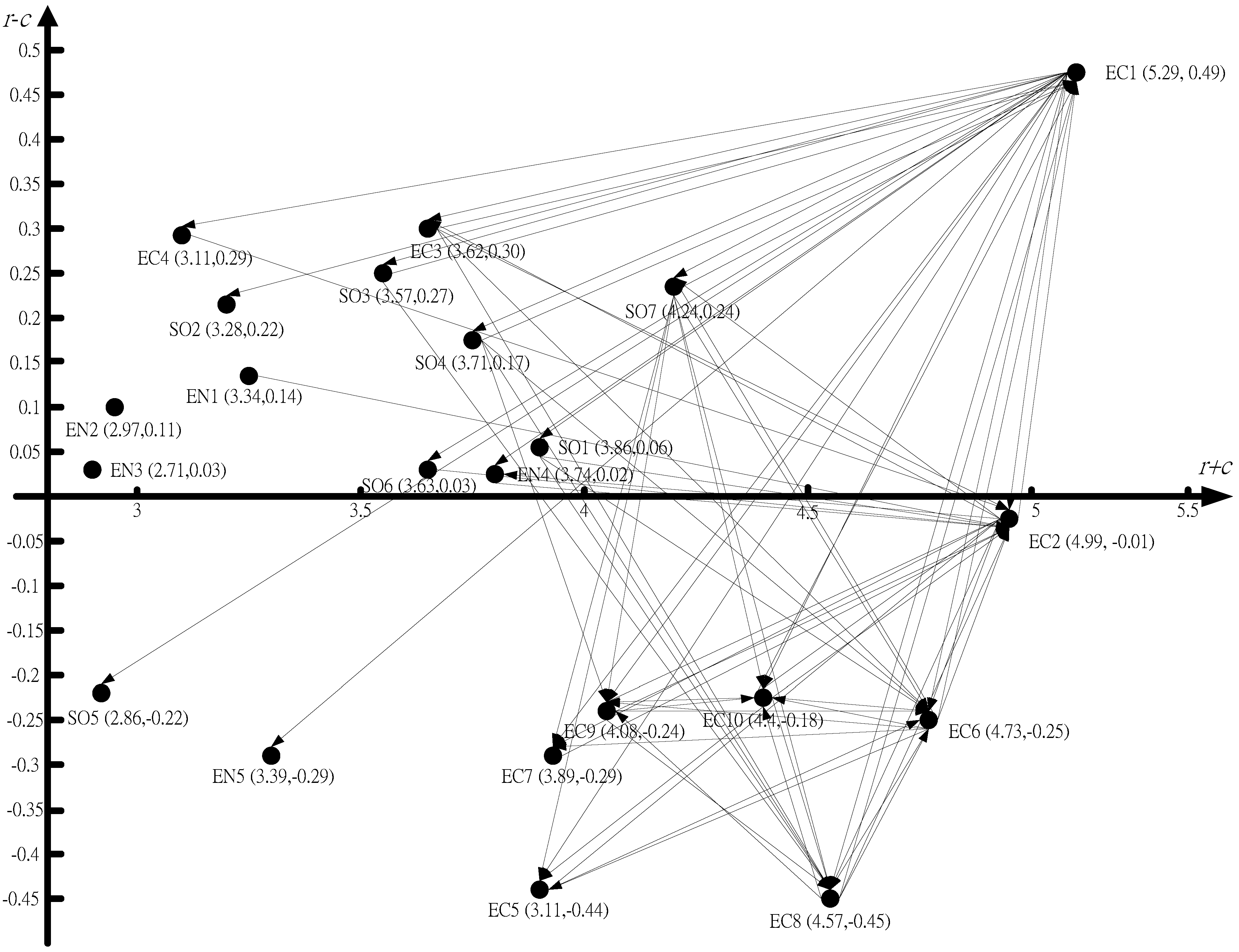

| Code | Criteria | r | c | r + c | r − c |

|---|---|---|---|---|---|

| EC1 | Corporate Governance | 2.89 | 2.40 | 5.29 | 0.49 |

| EC2 | Risk and Crisis Management | 2.49 | 2.50 | 4.99 | −0.01 |

| EC3 | Codes of Conduct/Compliance/Corruption and Bribery | 1.96 | 1.66 | 3.62 | 0.30 |

| EC4 | Antitrust Policy | 1.70 | 1.41 | 3.11 | 0.29 |

| EC5 | Customer Relationship Management | 1.68 | 2.12 | 3.8 | −0.44 |

| EC6 | Brand Management | 2.24 | 2.49 | 4.73 | −0.25 |

| EC7 | Supply Chain Management | 1.80 | 2.09 | 3.89 | −0.29 |

| EC8 | Efficiency | 2.06 | 2.51 | 4.57 | −0.45 |

| EC9 | Fleet Management | 1.92 | 2.16 | 4.08 | −0.24 |

| EC10 | Reliability | 2.11 | 2.29 | 4.4 | −0.18 |

| EN1 | Climate Change | 1.74 | 1.60 | 3.34 | 0.14 |

| EN2 | Biofuel/alternative energy | 1.54 | 1.43 | 2.97 | 0.11 |

| EN3 | Noise | 1.37 | 1.34 | 2.71 | 0.03 |

| EN4 | Environmental Policy/Management System | 1.88 | 1.86 | 3.74 | 0.02 |

| EN5 | Operational Eco-Efficiency | 1.55 | 1.84 | 3.39 | −0.29 |

| SO1 | Environment and Social Reporting (Information Disclose) | 1.96 | 1.90 | 3.86 | 0.06 |

| SO2 | Labor Practice Indicators and Human Rights | 1.75 | 1.53 | 3.28 | 0.22 |

| SO3 | Human Capital Development | 1.92 | 1.65 | 3.57 | 0.27 |

| SO4 | Talent Attraction and Retention | 1.94 | 1.77 | 3.71 | 0.17 |

| SO5 | Corporate Citizenship and Philanthropy | 1.32 | 1.54 | 2.86 | −0.22 |

| SO6 | Stakeholder Engagement | 1.83 | 1.80 | 3.63 | 0.03 |

| SO7 | Product Responsibility (Safety) | 2.24 | 2.00 | 4.24 | 0.24 |

| Senior manager | Interview key excerpts | Criterion comparison |

|---|---|---|

| Senior vice president 1 | Airline customers and clients exhibit high regionality/locality, and CSR strategy must capture local customers | Customer Relationship Management |

| The freight route must be influenced by oil price and cost, and fleet management should be considered along with CSR strategy | Fleet Management/Operational Eco-Efficiency | |

| Senior vice president 2 | CSR must be based on the health capital and pay attention to shareholder equity | Corporate Governance |

| Cooperate governance transparency is the key factor of CSR | ||

| Environmental protection should be combined with financial performance | Corporate Governance/Efficiency | |

| Operational environmental activities should be based on reduced cost and increased revenue | Corporate Governance/Efficiency/Operational Eco-Efficiency | |

| Brand value comes from customer perception of the airlines, and the basic factors include safety, service quality, and intimacy | Brand Management/ Product Responsibility (Safety)/Customer Relationship Management | |

| Abundant employee reward to encourage CSR activities in their daily work | Human Capital Development | |

| Senior vice president 3 | Bring up cross-function talents to allow CSR deepening in the company | Human Capital Development |

| The core value of the company must reflect on the CSR strategy | Corporate Governance | |

| Trainings exhibit limitations, and CSR can help enhance employee loyalty and coherence | Talent Attraction and Retention | |

| In-flight products should exhibit the eco-design concept, such as low CO2 emissions, recycling, and reusing | Climate Change/Operational Eco-Efficiency | |

| Communication and propaganda are very important, as when the Boeing company delivery flight gave clear information of design and manufacture with the sustainability concept of the flight | Stakeholder Engagement/Environment and Social Reporting (Information Disclosure) | |

| Senior vice president 4 | Improved public relation on the CSR approach for building up company image and public trust | Customer Relationship Management/Brand Management |

| Concrete action, such as the plan for replacing a bus or vent by electric vehicle (EV) | Biofuel/Alternative energy | |

| Innovative environmental measure without cost, such as in reducing the temperature in the landed aircraft to save the energy consumption of air conditioners; the crew can ask the passengers to lower down the window shade before leaving the aircraft | Operational Eco-Efficiency | |

| Senior vice president 5 | Fuel efficiency is the main financial and environmental factor among airlines; we can attempt finding the new flight along with prioritizing safety | Efficiency/Fleet Management/Product Responsibility (Safety) |

| Finances, environment, and safety are the basis of airline CSR; thus, all innovative practices must include these three key factors | Corporate Governance/Product Responsibility (Safety) | |

| Biofuel is the main topic of airlines in the near future; CSR strategy cannot be ignored | Biofuel/Alternative energy | |

| Vice president 1 | CSR should not only focus on charity, but must also construct strategy for all dimensions to strengthen competitiveness | Corporate Citizenship and Philanthropy/Corporate Governance |

| The employee is one of the key stakeholders; truly listening to employees will increase their commitment | Labor Practice Indicators and Human Rights | |

| CSR strategy needs clear KPIs for managers to ensure that every function is on the right track | Corporate Governance |

6. Conclusions and Future Research

Limitations and Further Research

Author Contributions

Appendix

| EC1 | EC2 | EC3 | EC4 | EC5 | EC6 | EC7 | EC8 | EC9 | EC10 | EN1 | |

| EC1 | 0.1118 | 0.1708 | 0.1333 | 0.1211 | 0.1420 | 0.1644 | 0.1399 | 0.1709 | 0.1458 | 0.1580 | 0.1068 |

| EC2 | 0.1452 | 0.1012 | 0.1158 | 0.0910 | 0.1286 | 0.1456 | 0.1213 | 0.1469 | 0.1357 | 0.1470 | 0.1067 |

| EC3 | 0.1227 | 0.1225 | 0.0554 | 0.0928 | 0.1021 | 0.1132 | 0.1061 | 0.1168 | 0.0963 | 0.1100 | 0.0613 |

| EC4 | 0.1096 | 0.1152 | 0.1004 | 0.0416 | 0.0816 | 0.1083 | 0.1011 | 0.1032 | 0.0782 | 0.0916 | 0.0522 |

| EC5 | 0.1020 | 0.1077 | 0.0709 | 0.0582 | 0.0588 | 0.1254 | 0.0882 | 0.1019 | 0.0774 | 0.0900 | 0.0587 |

| EC6 | 0.1296 | 0.1333 | 0.0919 | 0.0827 | 0.1352 | 0.0903 | 0.1272 | 0.1390 | 0.1143 | 0.1138 | 0.0814 |

| EC7 | 0.1069 | 0.1163 | 0.0800 | 0.0727 | 0.0934 | 0.1037 | 0.0616 | 0.1098 | 0.0848 | 0.1068 | 0.0686 |

| EC8 | 0.1226 | 0.1232 | 0.0774 | 0.0658 | 0.1111 | 0.1257 | 0.1063 | 0.0838 | 0.1210 | 0.1283 | 0.0752 |

| EC9 | 0.1103 | 0.1200 | 0.0687 | 0.0522 | 0.0967 | 0.1163 | 0.0926 | 0.1323 | 0.0677 | 0.1202 | 0.0849 |

| EC10 | 0.1278 | 0.1373 | 0.0823 | 0.0704 | 0.1255 | 0.1400 | 0.1056 | 0.1408 | 0.1229 | 0.0789 | 0.0763 |

| EN1 | 0.0939 | 0.1123 | 0.0540 | 0.0504 | 0.0742 | 0.0934 | 0.0865 | 0.1030 | 0.0974 | 0.0977 | 0.0479 |

| EN2 | 0.0853 | 0.0889 | 0.0418 | 0.0392 | 0.0609 | 0.0848 | 0.0763 | 0.0886 | 0.0871 | 0.0868 | 0.0915 |

| EN3 | 0.0673 | 0.0791 | 0.0378 | 0.0326 | 0.0710 | 0.0818 | 0.0677 | 0.0819 | 0.0720 | 0.0744 | 0.0619 |

| EN4 | 0.1039 | 0.1139 | 0.0571 | 0.0473 | 0.0874 | 0.1042 | 0.0962 | 0.1018 | 0.0925 | 0.0959 | 0.0966 |

| EN5 | 0.0861 | 0.0867 | 0.0488 | 0.0373 | 0.0677 | 0.0884 | 0.0886 | 0.0924 | 0.0816 | 0.0816 | 0.0850 |

| SO1 | 0.1061 | 0.1155 | 0.0831 | 0.0752 | 0.1008 | 0.1120 | 0.0967 | 0.1123 | 0.1013 | 0.1056 | 0.0781 |

| SO2 | 0.1055 | 0.1042 | 0.0829 | 0.0632 | 0.0831 | 0.1017 | 0.0834 | 0.1111 | 0.0834 | 0.0900 | 0.0528 |

| SO3 | 0.1176 | 0.1080 | 0.0897 | 0.0664 | 0.1004 | 0.1141 | 0.0832 | 0.1240 | 0.1100 | 0.1110 | 0.0637 |

| SO4 | 0.1181 | 0.1087 | 0.0781 | 0.0606 | 0.0982 | 0.1178 | 0.0865 | 0.1219 | 0.1137 | 0.1116 | 0.0614 |

| SO5 | 0.0787 | 0.0716 | 0.0487 | 0.0433 | 0.0828 | 0.0989 | 0.0632 | 0.0719 | 0.0582 | 0.0608 | 0.0460 |

| SO6 | 0.1104 | 0.1161 | 0.0779 | 0.0703 | 0.0907 | 0.1099 | 0.0892 | 0.1075 | 0.0913 | 0.0953 | 0.0683 |

| SO7 | 0.1388 | 0.1517 | 0.0861 | 0.0740 | 0.1303 | 0.1483 | 0.1253 | 0.1432 | 0.1245 | 0.1327 | 0.0801 |

| EN2 | EN3 | EN4 | EN5 | SO1 | SO2 | SO3 | SO4 | SO5 | SO6 | SO7 | |

| EC1 | 0.0957 | 0.0860 | 0.1272 | 0.1171 | 0.1391 | 0.1208 | 0.1265 | 0.1319 | 0.1165 | 0.1232 | 0.1445 |

| EC2 | 0.0824 | 0.0845 | 0.1169 | 0.1040 | 0.1065 | 0.0981 | 0.0999 | 0.0989 | 0.0769 | 0.1055 | 0.1354 |

| EC3 | 0.0556 | 0.0500 | 0.0694 | 0.0652 | 0.0934 | 0.0844 | 0.0912 | 0.1005 | 0.0670 | 0.0847 | 0.0980 |

| EC4 | 0.0471 | 0.0449 | 0.0592 | 0.0577 | 0.0829 | 0.0657 | 0.0688 | 0.0718 | 0.0545 | 0.0773 | 0.0844 |

| EC5 | 0.0537 | 0.0515 | 0.0684 | 0.0673 | 0.0791 | 0.0579 | 0.0642 | 0.0732 | 0.0666 | 0.0738 | 0.0829 |

| EC6 | 0.0693 | 0.0692 | 0.0907 | 0.0866 | 0.1018 | 0.0836 | 0.0910 | 0.1010 | 0.0920 | 0.1045 | 0.1153 |

| EC7 | 0.0606 | 0.0519 | 0.0846 | 0.0866 | 0.0860 | 0.0631 | 0.0635 | 0.0638 | 0.0659 | 0.0740 | 0.1018 |

| EC8 | 0.0723 | 0.0606 | 0.0953 | 0.0915 | 0.0841 | 0.0760 | 0.0861 | 0.0957 | 0.0694 | 0.0932 | 0.0977 |

| EC9 | 0.0824 | 0.0854 | 0.0930 | 0.0923 | 0.0737 | 0.0621 | 0.0717 | 0.0783 | 0.0567 | 0.0740 | 0.0901 |

| EC10 | 0.0703 | 0.0644 | 0.0878 | 0.0865 | 0.0856 | 0.0742 | 0.0843 | 0.0884 | 0.0675 | 0.0828 | 0.1089 |

| EN1 | 0.0917 | 0.0561 | 0.1062 | 0.1059 | 0.0837 | 0.0503 | 0.0505 | 0.0564 | 0.0704 | 0.0777 | 0.0836 |

| EN2 | 0.0384 | 0.0606 | 0.0945 | 0.1032 | 0.0744 | 0.0419 | 0.0447 | 0.0503 | 0.0626 | 0.0627 | 0.0707 |

| EN3 | 0.0551 | 0.0313 | 0.0852 | 0.0850 | 0.0661 | 0.0413 | 0.0409 | 0.0493 | 0.0554 | 0.0610 | 0.0682 |

| EN4 | 0.0882 | 0.0943 | 0.0585 | 0.1099 | 0.0966 | 0.0566 | 0.0598 | 0.0660 | 0.0772 | 0.0875 | 0.0846 |

| EN5 | 0.0747 | 0.0720 | 0.0886 | 0.0484 | 0.0749 | 0.0460 | 0.0546 | 0.0545 | 0.0572 | 0.0693 | 0.0684 |

| SO1 | 0.0667 | 0.0702 | 0.0919 | 0.0881 | 0.0591 | 0.0756 | 0.0763 | 0.0771 | 0.0788 | 0.0872 | 0.0997 |

| SO2 | 0.0447 | 0.0426 | 0.0662 | 0.0622 | 0.0841 | 0.0458 | 0.0955 | 0.1075 | 0.0775 | 0.0821 | 0.0843 |

| SO3 | 0.0494 | 0.0470 | 0.0775 | 0.0823 | 0.0828 | 0.0922 | 0.0536 | 0.1089 | 0.0723 | 0.0837 | 0.0807 |

| SO4 | 0.0528 | 0.0506 | 0.0782 | 0.0802 | 0.0862 | 0.0955 | 0.1086 | 0.0576 | 0.0758 | 0.0871 | 0.0870 |

| SO5 | 0.0420 | 0.0436 | 0.0544 | 0.0538 | 0.0683 | 0.0522 | 0.0608 | 0.0663 | 0.0334 | 0.0696 | 0.0552 |

| SO6 | 0.0599 | 0.0576 | 0.0758 | 0.0747 | 0.0864 | 0.0739 | 0.0804 | 0.0837 | 0.0730 | 0.0529 | 0.0810 |

| SO7 | 0.0766 | 0.0676 | 0.0922 | 0.0936 | 0.1018 | 0.0744 | 0.0787 | 0.0885 | 0.0738 | 0.0867 | 0.0739 |

Conflicts of Interest

References

- Chang, Y.C.; Yu, M.M.; Chen, P.C. Evaluating the performance of chinese airports. J. Air Transp. Manag. 2013, 31, 19–21. [Google Scholar] [CrossRef]

- Wang, Q.; Wu, C.; Sun, Y. Evaluating corporate social responsibility of airlines using entropy weight and grey relation analysis. J. Air Transp. Manag. 2015, 42, 55–62. [Google Scholar] [CrossRef]

- Lee, S.; Park, S.Y. Financial impacts of socially responsible activities on airline companies. J. Hosp. Tour. Res. 2010, 34, 185–203. [Google Scholar] [CrossRef]

- Chen, F.Y.; Chang, Y.H.; Lin, Y.H. Customer perceptions of airline social responsibility and its effect on loyalty. J. Air Transp. Manag. 2012, 20, 49–51. [Google Scholar] [CrossRef]

- Cowper-Smith, A.; de Grosbois, D. The adoption of corporate social responsibility practices in the airline industry. J. Sustain. Tour. 2011, 19, 59–77. [Google Scholar] [CrossRef]

- Searcy, C.; Elkhawas, D. Corporate sustainability ratings: An investigation into how corporations use the dow jones sustainability index. J. Clean. Prod. 2012, 35, 79–92. [Google Scholar] [CrossRef]

- RobecoSam. The sustainability yearbook 2015. Available online: http://yearbook.robecosam.com/files/rs_data/pdf/RobecoSAM_Sustainability_Yearbook_2015.pdf (accessed on 15 June 2015).

- Global Reporting Initiative. Sustainability reporting guidelines g 3.1. Available online: https://www.globalreporting.org/resourcelibrary/G3.1-Guidelines-Incl-Technical-Protocol.pdf (accessed on 15 June 2015).

- Global Reporting Initiative. Sustainability reporting guidelines g4. Available online: https://www.globalreporting.org/reporting/g4 (accessed on 15 June 2015).

- International Air Transport Association (IATA). Available online: http://www.iata.org/about/Pages/index.aspx (accessed on 15 June 2015).

- International Civil Aviation Organization (ICAO). Available online: http://www.icao.int/Pages/default.aspx (accessed on 15 June 2015).

- Govindan, K.; Kannan, D.; Kannan, D. Evaluating the drivers of corporate social responsibility in the mining industry with multi-criteria approach: A multi-stakeholder perspective. J. Clean. Prod. 2014, 84, 214–232. [Google Scholar] [CrossRef]

- Hsu, C.C.; Liou, J.J.H. An outsourcing provider decision model for the airline industry. J. Air Transp. Manag. 2013, 28, 40–46. [Google Scholar] [CrossRef]

- Hsu, C.W.; Lee, W.H.; Chao, W.C. Materiality analysis model in sustainability reporting: A case study at lite-on technology corporation. J. Clean Prod. 2013, 57, 142–151. [Google Scholar] [CrossRef]

- Lin, R.J. Using fuzzy dematel to evaluate the green supply chain management practices. J. Clean Prod. 2013, 40, 32–39. [Google Scholar] [CrossRef]

- Ou Yang, Y.P.; Shieh, H.M.; Tzeng, G.H. A vikor technique based on dematel and anp for information security risk control assessment. Inf. Sci. 2013, 232, 482–500. [Google Scholar] [CrossRef]

- Liou, J.J.H. Developing an integrated model for the selection of strategic alliance partners in the airline industry. Knowl.-Based Syst. 2012, 28, 59–67. [Google Scholar] [CrossRef]

- Tsai, W.H.; Hsu, J.L. Corporate social responsibility programs choice and costs assessment in the airline industry—A hybrid model. J. Air Transp. Manag. 2008, 14, 188–196. [Google Scholar] [CrossRef]

- Liou, J.J.H.; Yen, L.; Tzeng, G.H. Building an effective safety management system for airlines. J. Air Transp. Manag. 2008, 14, 20–26. [Google Scholar] [CrossRef]

- Coles, T.; Fenclova, E.; Dinan, C. Tourism and corporate social responsibility: A critical review and research agenda. Tour. Manag. Perspect. 2013, 6, 122–141. [Google Scholar] [CrossRef] [Green Version]

- Amini, M.; Bienstock, C.C. Corporate sustainability: An integrative definition and framework to evaluate corporate practice and guide academic research. J. Clean. Prod. 2014, 76, 12–19. [Google Scholar] [CrossRef]

- Elkington, J. Cannibals with Forks: Triple Bottom Line of 21st Century Business; Capstone Publishing Ltd.: Mankato, MN, USA, 1998. [Google Scholar]

- The World Business Council on Sustainable Development (WBCSD). Corporate Social Responsibility: Meeting Changing Expectations; WBCSD: Geneva, Switzerland, 1999. [Google Scholar]

- Zhao, Z.Y.; Zhao, X.J.; Davidson, K.; Zuo, J. A corporate social responsibility indicator system for construction enterprises. J. Clean Prod. 2012, 29–30, 277–289. [Google Scholar] [CrossRef]

- Lynes, J.K.; Andrachuk, M. Motivations for corporate social and environmental responsibility: A case study of scandinavian airlines. J. Int. Manag. 2008, 14, 377–390. [Google Scholar] [CrossRef]

- Lee, S.; Seo, K.; Sharma, A. Corporate social responsibility and firm performance in the airline industry: The moderating role of oil prices. Tour. Manag. 2013, 38, 20–30. [Google Scholar] [CrossRef]

- Fenclova, E.; Coles, T. Charitable partnerships among travel and tourism businesses: Perspectives from low-fares airlines. Int. J. Tour. Res. 2011, 13, 337–354. [Google Scholar] [CrossRef] [Green Version]

- Mak, B.L.M.; Chan, W.W. A study of environmental reporting: International japanese airlines. Asia Pac. J. Tour. Res. 2007, 12, 303–312. [Google Scholar] [CrossRef]

- Mak, B.L.M.; Chan, W.W.H.; Wong, K.; Zheng, C. Comparative studies of standalone environmental reports—European and asian airlines. Transp. Res. Part D Transp. Environ. 2007, 12, 45–52. [Google Scholar] [CrossRef]

- Chang, D.S.; Kuo, L.C.R. The effects of sustainable development on firms’ financial performance? An empirical approach. Sustain. Dev. 2008, 16, 365–380. [Google Scholar] [CrossRef]

- International Civil Aviation Organization (ICAO). 2013 environmental report. Available online: http://www.icao.int/environmental-protection/Pages/EnvReport13.aspx (accessed on 15 June 2015).

- Carbon Disclosure Project (CDP). Climate change program. Available online: https://www.cdp.net/en-US/Programmes/Pages/CDP-Investors.aspx (accessed on 15 June 2015).

- United Nations. Global compact. Available online: https://www.unglobalcompact.org/ (accessed on 15 June 2015).

- International Labour Organization. Available online: https: www.ilo.org/ (accessed on 15 June 2015).

- Wu, W.W.; Lee, Y.T. Developing global managers’ competencies using the fuzzy dematel method. Expert Syst. Appl. 2007, 32, 499–507. [Google Scholar] [CrossRef]

- Chiu, Y.J.; Chen, H.C.; Tzeng, G.H.; Shyu, J.Z. Marketing strategy based on customer behaviour for the LCD-TV. Int. J. Manag. Decis. Mak. 2006, 7, 143–165. [Google Scholar] [CrossRef]

- Hori, S.; Shimizu, Y. Designing methods of human interface for supervisory control systems. Control Eng. Pract. 1999, 7, 1413–1419. [Google Scholar] [CrossRef]

- Hsu, C.W.; Kuo, T.C.; Chen, S.H.; Hu, A.H. Using dematel to develop a carbon management model of supplier selection in green supply chain management. J. Clean Prod. 2013, 56, 164–172. [Google Scholar] [CrossRef]

- Tsai, W.H.; Chou, W.C. Selecting management systems for sustainable development in smes: A novel hybrid model based on dematel, anp, and zogp. Expert Syst. Appl. 2009, 36, 1444–1458. [Google Scholar] [CrossRef]

- Tzeng, G.H.; Chiang, C.H.; Li, C.W. Evaluating intertwined effects in e-learning programs: A novel hybrid mcdm model based on factor analysis and dematel. Expert Syst. Appl. 2007, 32, 1028–1044. [Google Scholar] [CrossRef]

- Teng, J.Y. Project Evaluation: Methods and Applications; National Taiwan Ocean University: Keelung, Taiwan, 2002. [Google Scholar]

- Saaty, T.L.; Vargas, L.G. Decision Making in Economic, Political, Social, and Technological Environments with the Analytic Hierarchy Process; RWS Publications: Pittsburgh, PA, USA, 1994. [Google Scholar]

- Lee, C.C.; Chiang, C.; Chen, C.T. An evaluation model of e-service quality by applying hierarchical fuzzy TOPSIS method. Int. J. Electron. Bus. Manag. 2012, 10, 38–49. [Google Scholar]

- Tzeng, G.-H.; Huang, C.-Y. Combined dematel technique with hybrid mcdm methods for creating the aspired intelligent global manufacturing and logistics systems. Ann. Oper. Res. 2012, 197, 159–190. [Google Scholar] [CrossRef]

- Ammann, M.; Oesch, D.; Schmid, M.M. Corporate governance and firm value: International evidence. J. Empir. Financ. 2011, 18, 36–55. [Google Scholar] [CrossRef]

- Olson, D.L.; Wu, D. Innovative csr: From risk management to value creation. J. Clean. Prod. 2010, 18, 1767–1768. [Google Scholar] [CrossRef]

- Air France KLM. 2013 CSR report. Available online: http://www.airfranceklm.com/sites/default/files/publications/2013_radd-en.pdf (accessed on 15 June 2015).

- Lufthansa group. 2013 sustainability report. Available online: http://www.lufthansagroup.com/fileadmin/downloads/en/responsibility/balance-2014-epaper/ (accessed on 15 June 2015).

- Qantas. 2013 Integrated ESG analysis. Available online: http://www.qantas.com.au/infodetail/about/investors/qantas-sustainability-review-2013.pdf (accessed on 15 June 2015).

- ANA Holdings. Annual report 2014. Available online: http://www.anahd.co.jp/en/investors/data/pdf/annual/14/14_00.pdf (accessed on 15 June 2015).

- Cathay Pacific. Sustainable development report 2013. Available online: http://downloads.cathaypacific.com/cx/aboutus/sd/2013/index.html (accessed on 15 June 2015).

- European Commission. European advanced biofuel flight path. Available online: http://ec.europa.eu/energy/en/topics/biofuels/biofuels-aviation (accessed on 15 June 2015).

- International Civil Aviation Organization (ICAO). Balanced approach to aircraft noise management. Available online: http://www.icao.int/environmental-protection/Pages/noise.aspx (accessed on 15 June 2015).

- Wang, S.W. Do global airline alliances influence the passenger’s purchase decision? J. Air Transp. Manag. 2014, 37, 53–59. [Google Scholar] [CrossRef]

- Saeidi, S.P.; Sofian, S.; Saeidi, P.; Saeidi, S.P.; Saaeidi, S.A. How does corporate social responsibility contribute to firm financial performance? The mediating role of competitive advantage, reputation, and customer satisfaction. J. Bus. Research 2015, 68, 341–350. [Google Scholar] [CrossRef]

- European Commission. Directorate-general for climate action. Available online: http://ec.europa.eu/clima/policies/transport/aviation/documentation_en.htm (accessed on 15 June 2015).

© 2015 by the authors; licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Chang, D.-S.; Chen, S.-H.; Hsu, C.-W.; Hu, A.H. Identifying Strategic Factors of the Implantation CSR in the Airline Industry: The Case of Asia-Pacific Airlines. Sustainability 2015, 7, 7762-7783. https://0-doi-org.brum.beds.ac.uk/10.3390/su7067762

Chang D-S, Chen S-H, Hsu C-W, Hu AH. Identifying Strategic Factors of the Implantation CSR in the Airline Industry: The Case of Asia-Pacific Airlines. Sustainability. 2015; 7(6):7762-7783. https://0-doi-org.brum.beds.ac.uk/10.3390/su7067762

Chicago/Turabian StyleChang, Dong-Shang, Sheng-Hung Chen, Chia-Wei Hsu, and Allen H. Hu. 2015. "Identifying Strategic Factors of the Implantation CSR in the Airline Industry: The Case of Asia-Pacific Airlines" Sustainability 7, no. 6: 7762-7783. https://0-doi-org.brum.beds.ac.uk/10.3390/su7067762