Diesel or Electric Jeepney? A Case Study of Transport Investment in the Philippines Using the Real Options Approach

,

,  , and

, and

Abstract

:

1. Introduction

2. Materials and Methods

3. Results

3.1. Traditional Valuation Methods

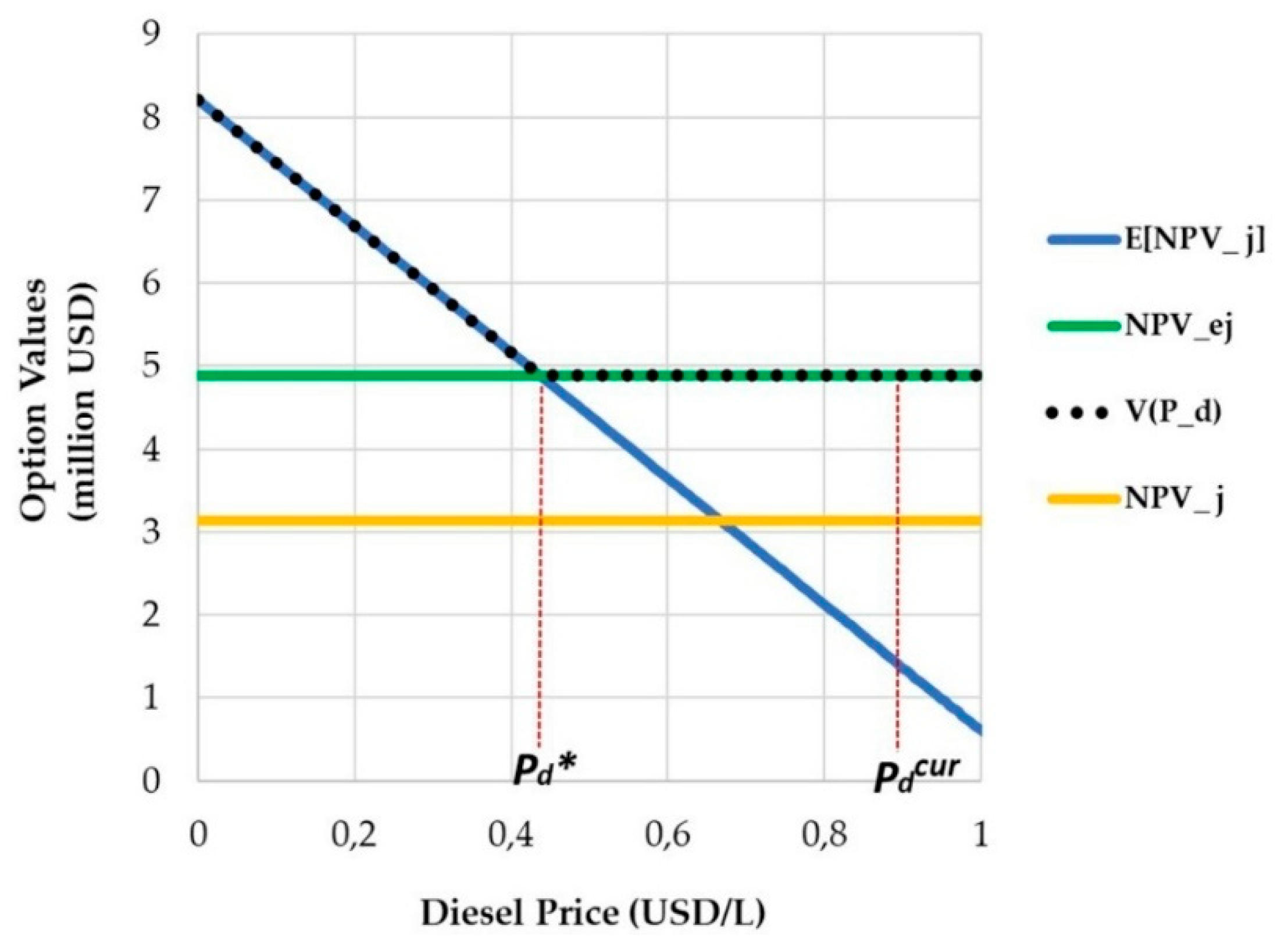

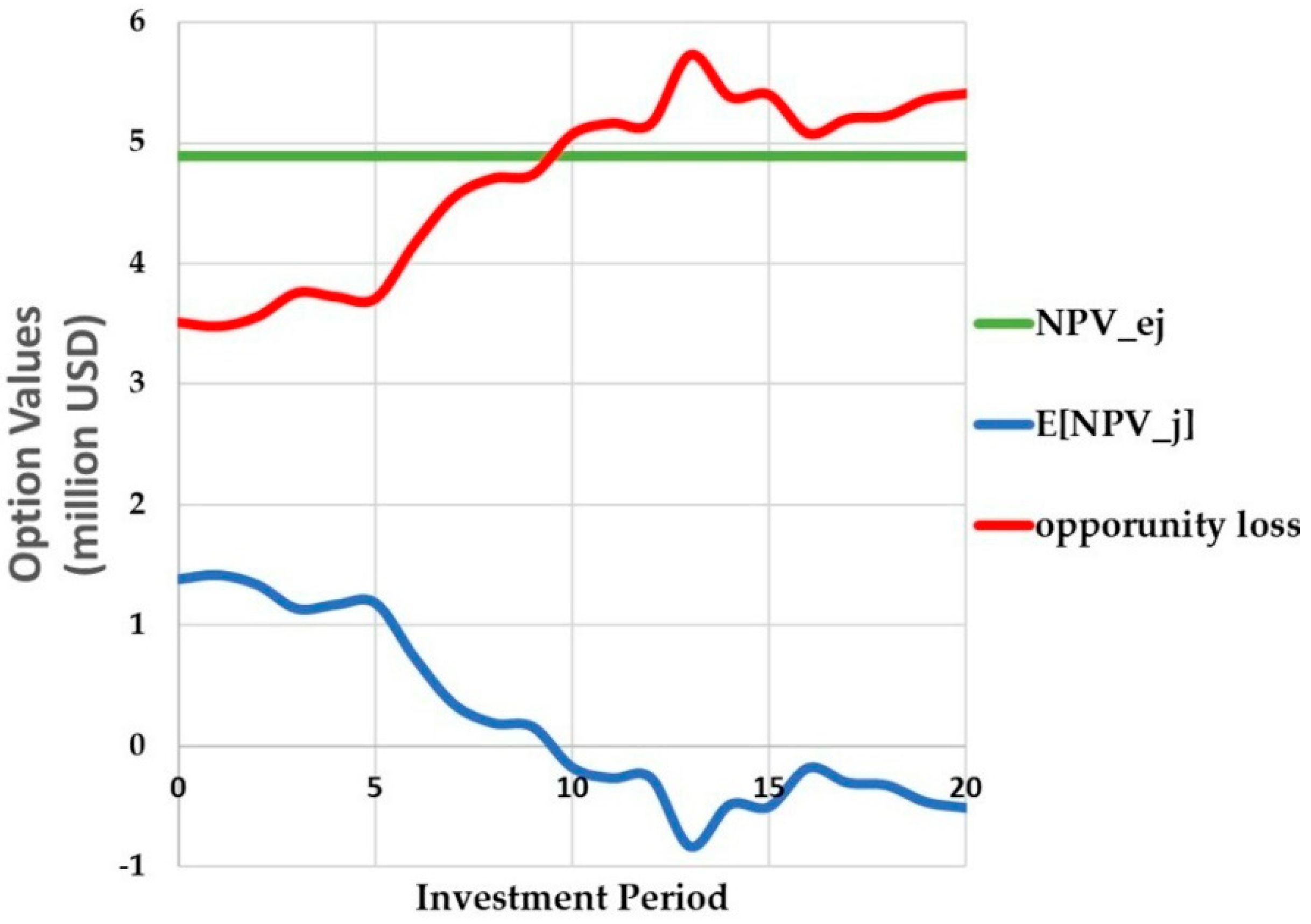

3.2. Baseline Scenario

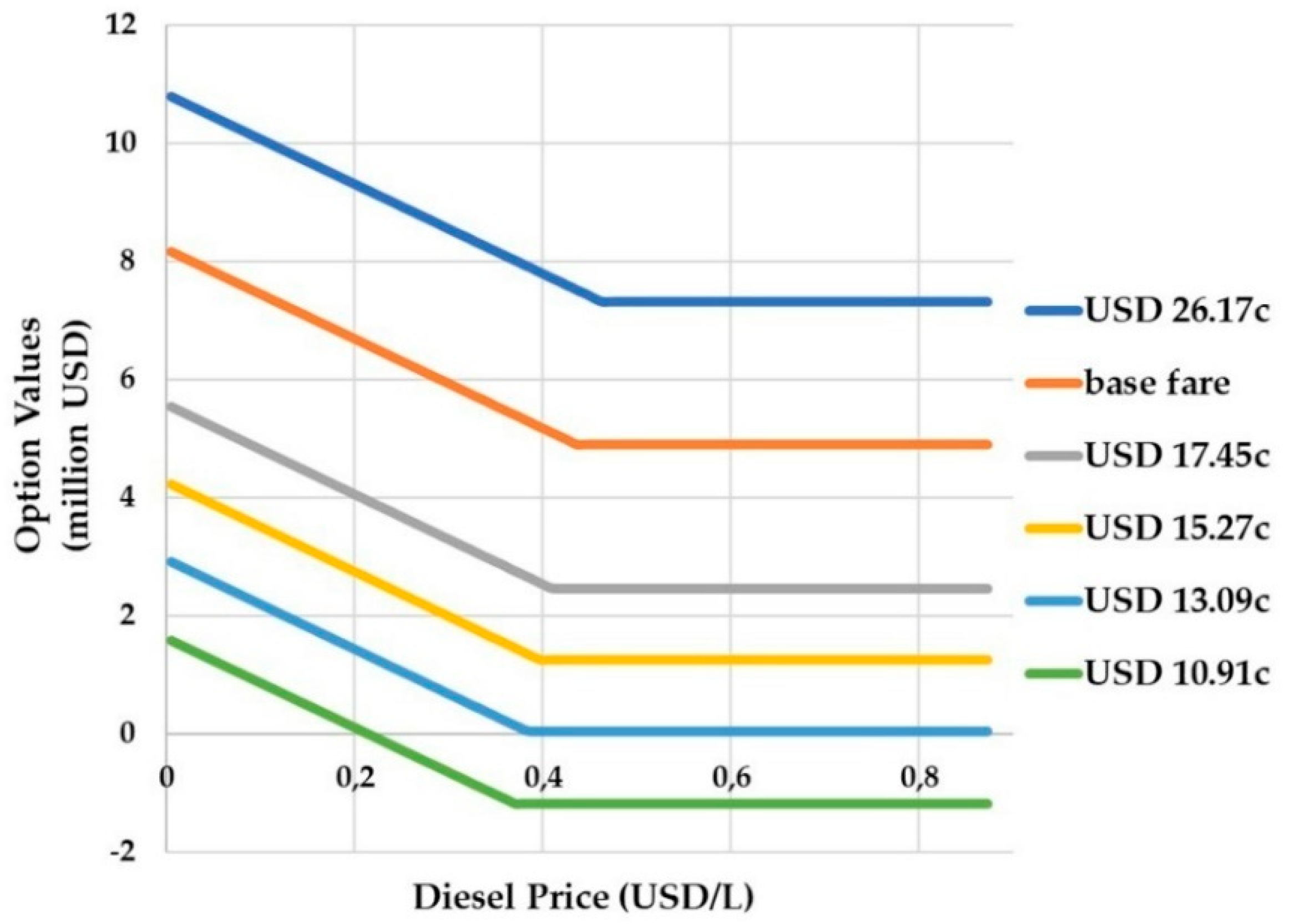

3.3. Jeepney Fare Scenario

3.4. Electricity Price Scenario

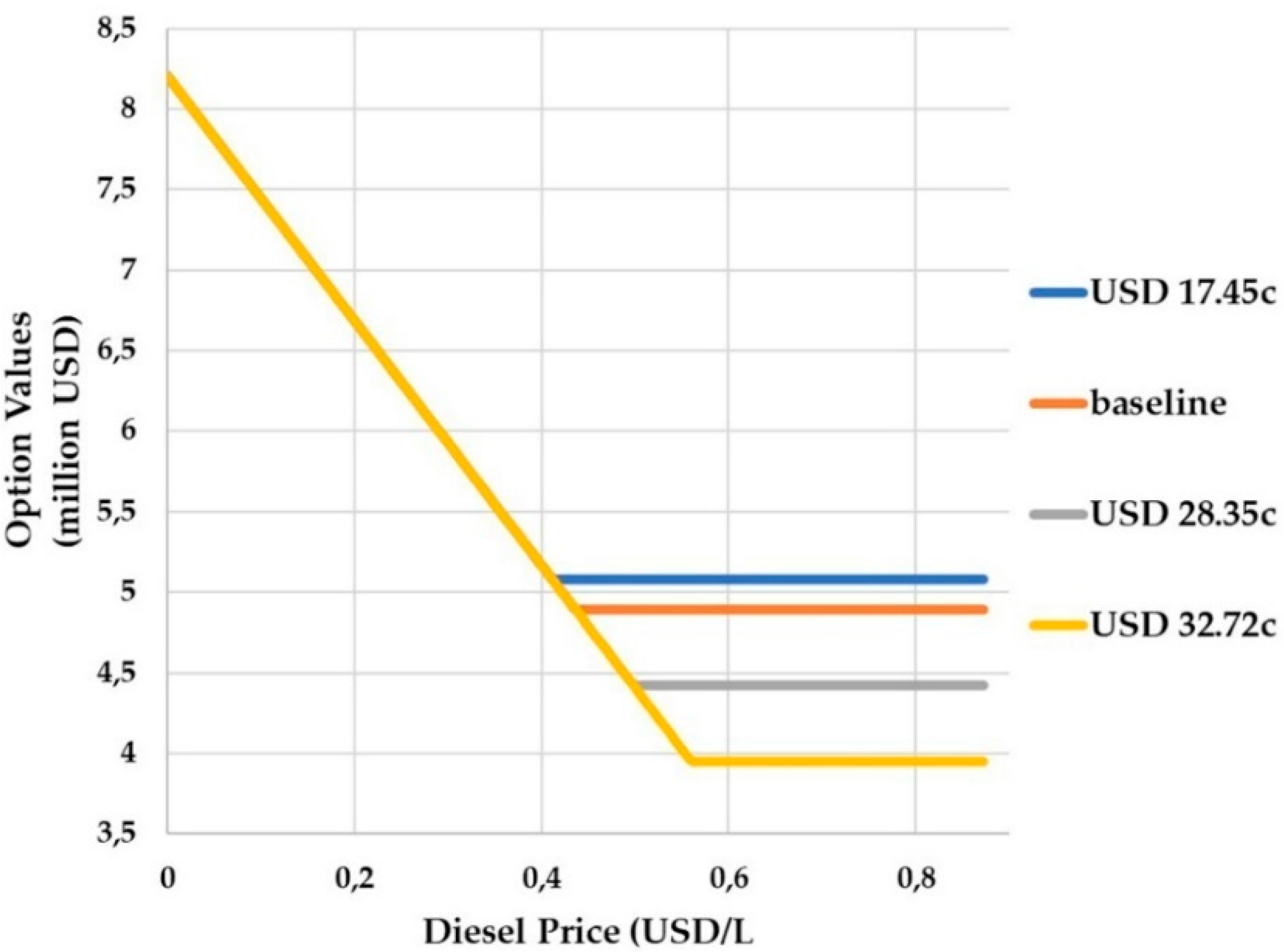

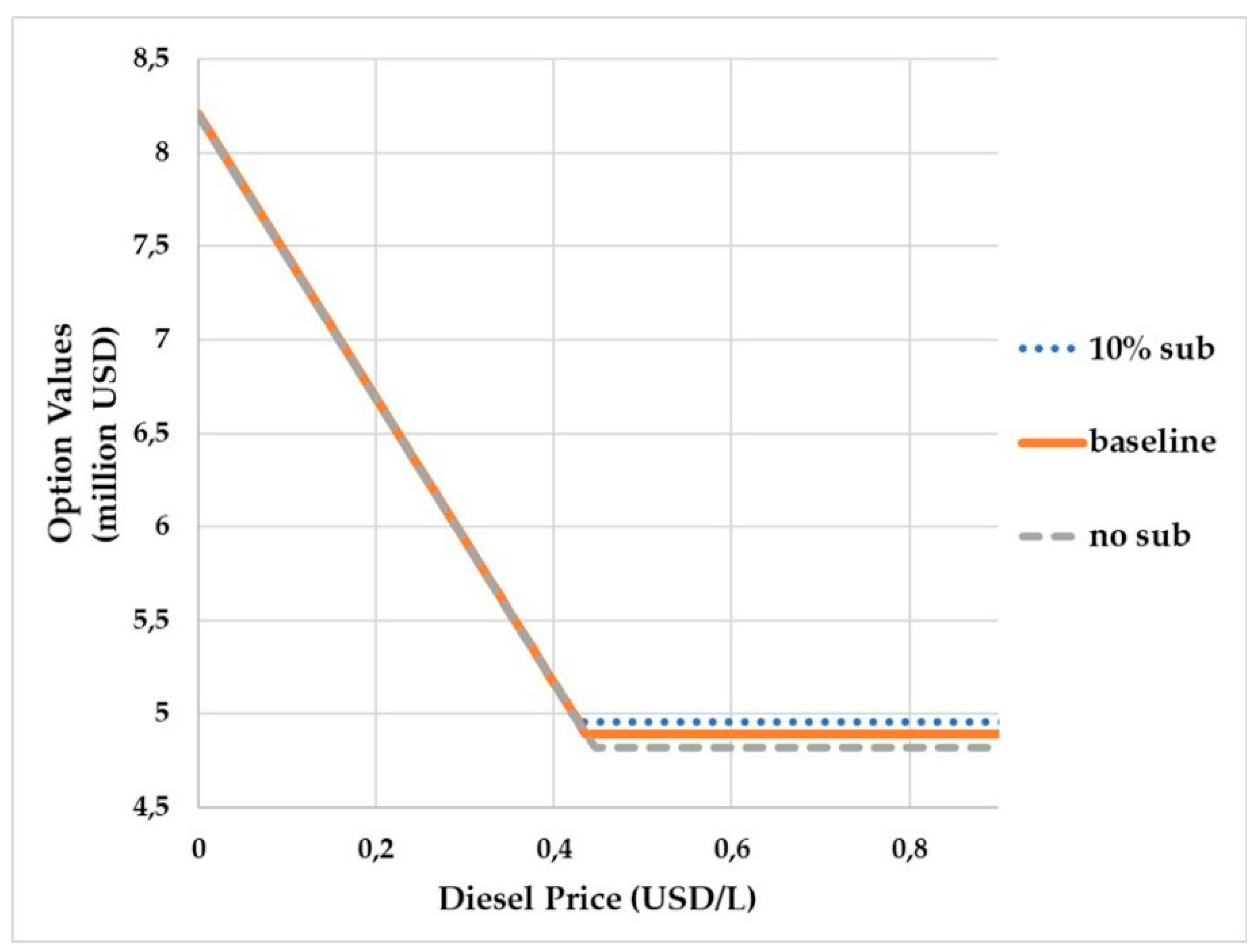

3.5. Government Subsidy Scenario

4. Discussion

5. Conclusions

Supplementary Materials

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

Nomenclature

| Acronyms | Description | |

| ADF | Augmented Dickey–Fuller | |

| CBA | Cost-Benefit Analysis | |

| DOE | Department of Energy | |

| DoTr | Department of Transportation | |

| EV | Electric Vehicles | |

| IRR | Internal Rate of Return | |

| GBM | Geometric Brownian Motion | |

| GHG | Greenhouse Gasses | |

| GPS | Global Positioning System | |

| HV | Hybrid Vehicle | |

| IRR | Internal Rate of Return | |

| LTFRB | Land Transportation Franchising and Regulatory Board | |

| MACE | Manila Aerosol Characterization Experiment | |

| NPV | Net Present Value | |

| OFG | Omnibus Franchising Guidelines | |

| PBP | Payback Period | |

| PUJ | Public Utility Jeepney | |

| PUV | Public Utility Vehicle | |

| PHP | Philippine Peso | |

| PUVMP | Public Utility Vehicle Modernization Program | |

| RES | Renewable Energy Sources | |

| ROA | Real Options Approach | |

| ROI | Return on Investment | |

| Symbols | Description | Unit |

| α | gradient of diesel prices | |

| σ | standard deviation of diesel prices | |

| ρ | discount factor | |

| Pej | average annual earnings from e-jeepney | PHP/yr |

| Qej | number of e-jeepney units per fleet; minimum set by the government | unit |

| Pe | price electricity | PHP/kWh |

| Qe | average annual electricity consumed by the fleet | kWh |

| Cej | average annual operations and maintenance cost for e-jeepney | PHP/yr |

| s | government subsidy for e-jeepney fleet | PHP |

| I | annual amortization for e-jeepney fleet | PHP/yr |

| Tej | effective lifetime of e-jeepney | Yr |

| ENPV | Expected Net Present Value | PHP |

| NPVej | net present value of e-jeepney fleet project | PHP |

| Pj | average annual earnings from diesel jeepney | PHP/yr |

| Qj | number of diesel jeepney units per fleet | unit |

| Qd | average annual fuel consumption of diesel jeepney fleet | L/yr |

| Cj | average annual operations and maintenance cost for diesel jeepney | PHP/yr |

| Ij | average investment cost for diesel jeepney | PHP |

| Tj | effective lifetime of diesel jeepney | Yr |

| T | Decision-making period | |

| Pd,0 | initial diesel price | PHP/L |

| current price of diesel | PHP/L | |

| NPVj | net present value of diesel jeepney fleet project | PHP |

References

- IPCC. Climate Change 2014: Mitigation of Climate Change. Contribution of Working Group III to the Fifth Assessment Report of the Intergovernmental Panel on Climate Change; Edenhofer, O.R., Pichs-Madruga, Y., Sokona, E., Farahani, S., Kadner, K., Seyboth, A., Adler, I., Baum, S., Brunner, P., Eickemeier, B., et al., Eds.; Cambridge University Press: Cambridge, UK, 2014; Available online: https://www.ipcc.ch/site/assets/uploads/2018/02/ipcc_wg3_ar5_frontmatter.pdf (accessed on 30 March 2019).

- The International Energy Agency (IEA). Tracking Clean Energy Progress 2017. Available online: https://www.iea.org/publications/freepublications/publication/TrackingCleanEnergyProgress2017.pdf (accessed on 30 March 2019).

- Ajanovic, A. The future of electric vehicles: Prospects and impediments. WIREs Energy Environ. 2015, 4, 236–521. [Google Scholar] [CrossRef]

- BNEF, Electric Vehicle Outlook. 2018. Available online: https://about.bnef.com/electric-vehicle-outlook/ (accessed on 30 March 2019).

- Kecorius, S.; Madueño, L.; Vallar, E.; Alas, H.; Betito, G.; Birmili, W.; Cambaliza, M.O.; Catipay, G.; Galvez, M.C.; Lorenzo, G.; et al. Aerosol particle mixing state, soot number size distributions, and emission factors in a polluted urban environment: Case study of Metro Manila, Philippines. Atmos. Environ. 2017, 170, 169–183. [Google Scholar] [CrossRef]

- Department of Transportation (DoTr). Guidelines on the Availment of the Equity Subsidy under the Public Utility Vehicle (PUV) Modernization Program. 2018. Available online: https://drive.google.com/file/d/1Sq8JbgN1E4hF4a6gbslFdk7DwbX7ulhB/view (accessed on 30 March 2019).

- Philippine Information Agency (PIA). Makati-Mandaluyong eSakay Route Launched. Available online: https://pia.gov.ph/news/articles/1017399 (accessed on 30 March 2019).

- Lopez, N.S.; Soliman, J.; Biona, J.B.M. Life Cycle Cost and Benefit Analysis of Low Carbon Vehicle Technologies. In Sustainable Energy Technology and Policies; De, S., Bandyopadhyay, S., Assadi, M., Mukherjee, D., Eds.; Green Energy and Technology Springer: Singapore, 2018; pp. 131–146. [Google Scholar]

- Balaria, F.E.; Pascual, M.P.; Santos, M.D.; Ortiz, A.F.; Gabriel, A.G.; Mangahas, T.L.S. Sustainability of E-Trike as Alternative Mode of Public Transportation System: The Case of Cabanatuan City, Philippines. Open J. Civ. Eng. 2017, 7, 362–377. [Google Scholar] [CrossRef] [Green Version]

- Sarsalejo, L.F.C.; Preciados, L.S. Comparative Profitability Analysis of Electric, Pedicab, and Gasoline-Fuelled Tricycles. J. Educ. Hum. Resour. Dev. 2018, 6, 1–11. [Google Scholar]

- Agaton, C.B. A Real Options Approach to Renewable and Nuclear Energy Investments in the Philippines; Logos Verlag Berlin: Berlin, Germany, 2019; Volume 71. [Google Scholar]

- Nishihara, M. Hybrid or electric vehicles? A real options perspective. Oper. Res. Lett. 2010, 38, 87–93. [Google Scholar] [CrossRef] [Green Version]

- Kang, N.; Bayrak, A.; Papalambros, P.Y. Robustness and Real Options for Vehicle Design and Investment Decisions Under Gas Price and Regulatory Uncertainties. J. Mech. Des. 2018, 140, 10140401–10140411. [Google Scholar] [CrossRef]

- Kleindorfer, P.R.; Neboian, A.; Roset, A.; Spinler, S. Fleet Renewal with Electric Vehicles at La Poste. INFORMS J. Appl. Anal. 2012, 42, 465–477. [Google Scholar] [CrossRef]

- Yamashita, D.; Niimura, T.; Takamori, H.; Wang, T.; Yokoyama, R. Plug-in Electric Vehicle Markets and Their Infrastructure Investment Policies under Fuel Economy Uncertainty. Int. J. Real Options Strategy 2013, 1, 39–60. [Google Scholar] [CrossRef] [Green Version]

- Avadikyan, A.; Llerena, P. A real options reasoning approach to hybrid vehicle investments. Technol. Forecast. Soc. Chang. 2010, 77, 649–661. [Google Scholar] [CrossRef]

- Ansaripoor, A.H.; Oliveira, F.S. Flexible lease contracts in the fleet replacement problem with alternative fuel vehicles: A real-options approach. Eur. J. Oper. Res. 2018, 266, 316–327. [Google Scholar] [CrossRef]

- He, H.; Fan, J.; Li, Y.; Li, J. When to switch to a hybrid electric vehicle: A replacement optimisation decision. J. Clean. Prod. 2017, 148, 295–303. [Google Scholar] [CrossRef]

- Guo, Q.W.; Chen, S.; Schonfeld, P.; Li, Z. How time-inconsistent preferences affect investment timing for rail transit. Transp. Res. Part B Methodol. 2018, 118, 172–192. [Google Scholar] [CrossRef]

- Li, Z.C.; Guo, Q.W.; Lam, W.H.; Wong, S.C. Transit technology investment and selection under urban population volatility: A real option perspective. Transp. Res. Part B Methodol. 2015, 78, 318–340. [Google Scholar] [CrossRef] [Green Version]

- Department of Energy (DOE). Oil Supply/Demand Report FY 2018 vs FY 2017. Available online: https://www.doe.gov.ph/downstream-oil (accessed on 28 March 2019).

- Fonseca, M.N.; de Oliveira Pamplona, E.; de Mello Valerio, V.E.; Aquila, G.; Rocha, L.C.S.; Junior, P.R. Oil price volatility: A real option valuation approach in an African oil field. J. Pet. Sci. Eng. 2017, 150, 297–304. [Google Scholar] [CrossRef]

- Guedes, J.; Santos, P. Valuing an offshore oil exploration and production project through real options analysis. Energy Econ. 2016, 60, 377–386. [Google Scholar] [CrossRef]

- Agaton, C.B.; Karl, H. A real options approach to renewable electricity generation in the Philippines. Energy Sustain. Soc. 2018, 8, 1. [Google Scholar] [CrossRef] [Green Version]

- National Economic and Development Agency (NEDA). Updated Social Discount Rate for the Philippines. 2016. Available online: http://www.neda.gov.ph/wp-content/uploads/2017/01/Revisions-on-ICC-Guidelines-and-Procedures-Updated-Social-Discount-Rate-for-the-Philippines.pdf (accessed on 13 August 2019).

- Mun, J. Real options analysis versus traditional DCF valuation in layman’s terms. In Managing Enterprise Risk: What the Electric Industry Experience Implies for Contemporary Business; Leggio, K.B., Taylor, M.L., Eds.; Elsevier: Amsterdam, The Netherlands, 2006; pp. 75–106. [Google Scholar]

- US Energy Information Administration. Annual Energy Outlook 2019 with Projections to 2050. Available online: https://www.eia.gov/outlooks/aeo/pdf/aeo2019.pdf (accessed on 23 April 2019).

- International Energy Agency (IEA). World Energy Outlook. 2018. Available online: https://www.iea.org/weo2018/ (accessed on 23 April 2019).

- White, P.R. Public Transport: Its Planning, Management and Operation; Routledge: New York, NY, USA, 2017. [Google Scholar]

- Borndoerfer, R.; Karbstein, M.; Pfetsch, M.E. Models for fare planning in public transport. Discret. Appl. Math. 2012, 160, 2591–2605. [Google Scholar] [CrossRef] [Green Version]

- Agaton, C.B. Real Options Analysis of Renewable Energy Investment Scenarios in the Philippines. Renew. Energy Sustain. Dev. 2017, 3, 284–292. [Google Scholar] [CrossRef] [Green Version]

- Fernandez, L. Power Prices: Where We Are and How Do We Reduce the Bill; Philippines’ Department of Trade and Industry (DTI): London, UK, 2015. Available online: http://industry.gov.ph/wp-content/uploads/2015/08/Power-Prices-Where-We-Are-and-How-Can-We-Reduce-Our-Bill-by-Lawrence-Fernandez-MERALCO1.pdf (accessed on 23 April 2019).

- Agaton, C.B. Use coal or invest in renewables: A real options analysis of energy investments in the Philippines. Renewables 2018, 5, 1. [Google Scholar] [CrossRef]

- Sáenz de Miera, G.; del Río González, P.; Vizcaíno, I. Analysing the impact of renewable electricity support schemes on power prices: The case of wind electricity in Spain. Energy Policy 2008, 36, 3345–3359. [Google Scholar] [CrossRef]

- Sorknæs, P.; Djørup, S.R.; Lund, H.; Thellufsen, J.Z. Quantifying the influence of wind power and photovoltaic on future electricity market prices. Energy Convers. Manag. 2019, 180, 312–324. [Google Scholar] [CrossRef]

- Hirth, L. What caused the drop in European electricity prices? A factor decomposition analysis. Energy J. 2018, 39, 143–157. [Google Scholar] [CrossRef]

- De Schepper, E.; Van Passel, S.; Lizin, S. Economic benefits of combining clean energy technologies: The case of solar photovoltaics and battery electric vehicles. Int. J. Energy Res. 2015, 39, 1109–1119. [Google Scholar] [CrossRef]

- Hoarau, Q.; Perez, Y. Interactions between electric mobility and photovoltaic generation: A review. Renew. Sustain. Energy Rev. 2018, 94, 510–522. [Google Scholar] [CrossRef] [Green Version]

- Feng, W.; Figliozzi, M. Vehicle technologies and bus fleet replacement optimization: Problem properties and sensitivity analysis utilizing real-world data. Public Transp. 2014, 6, 137–157. [Google Scholar] [CrossRef]

- Bubeck, S.; Tomaschek, J.; Fahl, U. Perspectives of electric mobility: Total cost of ownership of electric vehicles in Germany. Transp. Policy 2016, 50, 63–77. [Google Scholar] [CrossRef]

- Nian, V.; Hari, M.P.; Yuan, J. A new business model for encouraging the adoption of electric vehicles in the absence of policy support. Appl. Energy 2019, 235, 1106–1117. [Google Scholar] [CrossRef]

- Ji, S.; Cherry, C.R.; Bechle, M.J.; Wu, Y.; Marshall, J.D. Electric Vehicles in China: Emissions and Health Impacts. Environ. Sci. Technol. 2012, 46, 2018–2024. [Google Scholar] [CrossRef]

- Hawkins, T.R.; Singh, B.; Majeau-Bettez, G.; Strømman, A.H. Comparative environmental life cycle assessment of conventional and electric vehicles. J. Ind. Ecol. 2013, 17, 53–64. [Google Scholar] [CrossRef]

- Yong, J.Y.; Ramachandaramurthy, V.K.; Tana, K.M.; Mithulananthan, N. A review on the state-of-the-art technologies of electric vehicle, its impacts and prospects. Renew. Sustain. Energy Rev. 2015, 49, 365–385. [Google Scholar] [CrossRef]

- Buekers, J.; Holderbeke, M.V.; Bierkens, J.; Panisa, L.I. Health and environmental benefits related to electric vehicle introduction in EU countries. Transp. Res. Part D Transp. Environ. 2014, 33, 26–38. [Google Scholar] [CrossRef]

- Biona, J.B.; Mejia, M.; Tacderas, M.; dela Cruz, N.; Dematera, K.; Romero, J. Alternative Technologies for the Philippine Utility Jeepney: A Cost-Benefit Study; Blacksmith Institute and Clean Air Asia: Pasig City, Philippines, 2017. [Google Scholar]

- Holland, S.P.; Mansur, E.T.; Muller, N.Z.; Yates, A.J. Are there environmental benefits from driving electric vehicles? The importance of local factors. Am. Econ. Rev. 2016, 106, 3700–3729. [Google Scholar] [CrossRef]

- Ziefle, M.; Beul-Leusmann, S.; Kasugai, K.; Schwalm, M. Public perception and acceptance of electric vehicles: Exploring users’ perceived benefits and drawbacks. In International Conference of Design, User Experience, and Usability; Marcus, A., Ed.; Springer: Cham, Switzerland, 2014; Volume 8159, pp. 628–639. [Google Scholar]

- Frost & Sullivan. The Future of Electric Vehicles in Southeast Asia: Position Paper. 2018. Available online: https://asia.nissannews.com/en/releases/release-568d250ed392364df4a81d7c61017eee/images/074b20d9e25174eab8146462b7be1932083d9d3a (accessed on 14 August 2019).

- Sovacool, B.K.; Kester, J.; Heida, V. Cars and kids: Childhood perceptions of electric vehicles and sustainable transport in Denmark and the Netherlands. Technol. Forecast. Soc. Chang. 2019, 144, 182–192. [Google Scholar] [CrossRef]

- She, Z.Y.; Sun, Q.; Ma, J.J.; Xie, B.C. What are the barriers to widespread adoption of battery electric vehicles? A survey of public perception in Tianjin, China. Transp. Policy 2017, 56, 29–40. [Google Scholar] [CrossRef]

- Xing, J.; Leard, B.; Li, S. What Does an Electric Vehicle Replace? No. w25771; National Bureau of Economic Research: Cambridge, MA, USA, 2019. [Google Scholar]

- Springel, K. Network Externality and Subsidy Structure in Two-Sided Markets: Evidence from Electric Vehicle Incentives; United States Environmental Protection Agency: Washington, DC, USA, 2016. [Google Scholar]

- Luo, C.; Huang, Y.F.; Gupta, V. Stochastic dynamic pricing for EV charging stations with renewable integration and energy storage. IEEE Trans. Smart Grid 2017, 9, 1494–1505. [Google Scholar] [CrossRef]

- He, F.; Yin, Y.; Zhou, J. Deploying public charging stations for electric vehicles on urban road networks. Transp. Res. Part C Emerg. Technol. 2015, 60, 227–240. [Google Scholar] [CrossRef]

- Wang, C.; He, F.; Lin, X.; Shen, Z.J.M.; Li, M. Designing locations and capacities for charging stations to support intercity travel of electric vehicles: An expanded network approach. Transp. Res. Part C Emerg. Technol. 2019, 102, 210–232. [Google Scholar] [CrossRef]

- Clement-Nyms, K.; Haesen, E.; Driesen, J. The Impact of Charging Plug-In Hybrid Electric Vehicles on a Residential Distribution Grid. IEEE Trans. Power Syst. 2010, 25, 371–380. [Google Scholar] [CrossRef]

- Richardson, P.; Flynn, D.; Keane, A. Optimal Charging of Electric Vehicles in Low-Voltage Distribution Systems. IEEE Trans. Power Syst. 2012, 27, 268–279. [Google Scholar] [CrossRef]

- DOE. Summary of Installed Capacity, Dependable Capacity, Power Generation and Consumption. 2018. Available online: https://www.doe.gov.ph/sites/default/files/pdf/energy_statistics/01_2018_power_statistics_as_of_29_march_2019_summary.pdf (accessed on 23 April 2019).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Valuation Method | E-Jeepney | Modernized Diesel Jeepney |

|---|---|---|

| Net present value (NPV) (USD) | 4.892 million | 3.138 million |

| Payback period (PBP) (years) | 4.09 | 3.28 |

| Return on investment (ROI) (30 years) | 373% | 490% |

| Internal rate of return (IRR) | 32.36 | 43.89 |

© 2019 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Agaton, C.B.; Guno, C.S.; Villanueva, R.O.; Villanueva, R.O. Diesel or Electric Jeepney? A Case Study of Transport Investment in the Philippines Using the Real Options Approach. World Electr. Veh. J. 2019, 10, 51. https://0-doi-org.brum.beds.ac.uk/10.3390/wevj10030051

Agaton CB, Guno CS, Villanueva RO, Villanueva RO. Diesel or Electric Jeepney? A Case Study of Transport Investment in the Philippines Using the Real Options Approach. World Electric Vehicle Journal. 2019; 10(3):51. https://0-doi-org.brum.beds.ac.uk/10.3390/wevj10030051

Chicago/Turabian StyleAgaton, Casper Boongaling, Charmaine Samala Guno, Resy Ordona Villanueva, and Riza Ordona Villanueva. 2019. "Diesel or Electric Jeepney? A Case Study of Transport Investment in the Philippines Using the Real Options Approach" World Electric Vehicle Journal 10, no. 3: 51. https://0-doi-org.brum.beds.ac.uk/10.3390/wevj10030051